|

市場調査レポート

商品コード

1429210

世界の化学種子処理:市場シェア分析、産業動向、統計、成長予測(2024~2029年)Global Chemical Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の化学種子処理:市場シェア分析、産業動向、統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 134 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

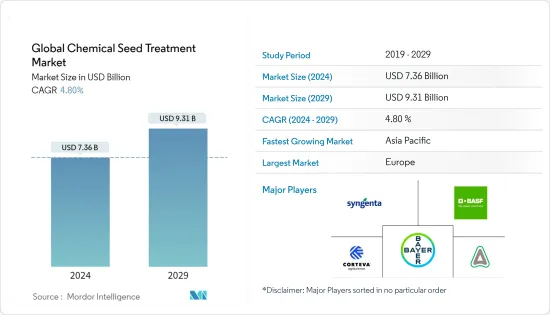

世界の化学種子処理市場規模は2024年に73億6,000万米ドルと推定・予測され、2029年には93億1,000万米ドルに達し、予測期間(2024-2029年)のCAGRは4.80%で成長すると予測されます。

COVID-19パンデミックが種子処理剤市場に与える影響は、主に輸送障壁のため、ごくわずかです。封鎖や混乱による影響は、あらゆる種類の農業活動に対して政府によって免除されているため、コロナ発生によるそのような影響はないです。実際、農薬会社は農家のパニック的な購買行動により、昨年と比較して2桁の利益を上げています。種子処理に対する農民の意識の高まりが、政府からの支援につながっています。種子処理剤で適切に処理された種子を保管し、種子の腐敗を防ぐために、発展途上国の政府によって、国や村レベルで複数の種子バンクが管理されています。種子処理剤の使用をめぐる政府の規制やキャンペーンの奨励が市場を牽引しています。種子処理の世界市場は、殺虫剤、殺菌剤、その他の化学薬剤で構成され、そのうち化学薬剤が最も支配的な用途セグメントを形成しています。

化学種子処理剤市場の動向

高品質種子のコスト増加が市場を牽引

ハイブリッドや遺伝子組み換え種子に関連する高コストは、世界的に種子処理市場の成長を促進する主な要因です。種子処理は、燻蒸や農薬の葉面散布に関連する規制問題の増加により、農家が良質な種子への投資を保護する手段として徐々に考慮されるようになっています。望ましい農学的形質を備えた高品質の種子に対する需要の増加により、種子のコストは上昇すると予想されます。企業も農家も、高品質の種子を保存するために、種子処理ソリューションに支出する用意があります。2019年の米国農務省の推計によると、トウモロコシの種子は1995年以来約300%のコストがかかっていますが、収量は35%しか伸びていません。フレーマーは、複数回の化学薬品の投与を必要としない種子を選択することで、運用コストを削減しようとしています。これらの人工種子の初期保護は、種子処理製品を使用することで確保されています。

アジア太平洋地域での使用の増加

地域的には、アジア太平洋地域が種子処理剤のトップ消費者で、市場シェアは約60.0%です。アジアで生産される主な作物には、コメ、テンサイ、果物・野菜、穀物、穀類が含まれます。韓国、中国、日本、そして最近ではベトナムなどのアジア諸国は、短期および多年生作物の両方に種子保護/強化製品をより多く適用しています。シンジェンタ、BASF、バイエルなど、さまざまな大手種子処理企業がこれらの地域で事業を展開しており、自社製品に関する認知度を高め、種子処理製品を使用する利点を紹介するため、定期的に圃場試験や研修会を開催しています。農業慣行の増加と高品質の農産物の要求は、この地域における種子処理市場の成長を促進すると予測される要因です。

化学種子処理産業の概要

化学種子処理市場は統合されています。市場の主要企業が市場の大部分を占め、多様で増加する製品ポートフォリオを有しています。市場シェアの優位性という点では、Syngenta International AGのシェアが24.0%で、Bayer CropScience AG、Corteva Agriscience、BASF SE、Syngentaがこれに続いています。同市場におけるこれらの大手企業は、事業拡大や投資、合併・買収、提携、合弁事業、契約などを通じて存在感を高めることに注力しています。これらの企業は北米、アジア太平洋、欧州で強い存在感を示しています。また、これらの地域全体に強力な流通網とともに製造施設を有しています。この市場の主要企業は、事業拡大や製品革新、M&A、提携、合弁事業、契約などを通じて存在感を高めることに注力しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 用途

- 殺虫剤

- 殺菌剤

- その他の化学品

- 作物

- トウモロコシ

- 大豆

- 小麦

- 米

- カノーラ

- 綿花

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- スペイン

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- タイ

- ベトナム

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Syngenta International AG

- Bayer CropScience AG

- BASF SE

- DowDuPont Inc.

- ADAMA Agricultural Solutions Ltd

- Advanced Biological Systems

- BioWorks Inc.

- Germains Seed Technology

- Incotec Group BV

- Nufarm Limited

- Plant Health Care

- Precision Laboratories

- Valent Biosciences Corporation

- Verdesian Life Sciences

第7章 市場機会と今後の動向

第8章 COVID-19の市場への影響評価

The Global Chemical Seed Treatment Market size is estimated at USD 7.36 billion in 2024, and is expected to reach USD 9.31 billion by 2029, growing at a CAGR of 4.80% during the forecast period (2024-2029).

The impact of the COVID-19 pandemic on the seed treatment market has been minimal, mainly due to transportation barriers. The impact of lockdowns or disruptions has been exempted by the government for all types of agricultural activities, hence there has been no such effect of corona outbreak. Indeed, the agrochemical companies have made double-digit profits as compared to last year, due to panic buying behavior from farmers. Growing awareness among farmers over the use of seed treatment has resulted in support from the government. Multiple seed banks are being managed by the governments of developing countries, at the national, as well as village levels, in order to store seeds that are properly treated by seed treatment chemicals, hence preventing the rotting of seeds. Encouraging government regulations and campaigns over the use of seed treatment is driving the market. The global market for seed treatment comprises chemical agents, including insecticides, fungicides, and other chemicals, of which chemical agents form the most dominant application segment.

Chemical Seed Treatment Market Trends

Increase in Cost of High-Quality Seeds driving the Market

High costs associated with hybrids and genetically modified seeds is a major factor driving the growth of the seed treatment market, globally. Seed treatment is gradually being considered by farmers as a mode to protect investments made on good quality seeds, due to an increase in regulatory issues relating to fumigation, as well as the foliar application of pesticides. Cost of seeds is expected to increase, owing to a increase in the demand for high-quality seeds, with desirable agronomic traits. Both companies and farmers are ready to spend on seed treatment solutions, in order to save high-quality seeds. According to USDA estimates of 2019, corn seeds cost about 300% since 1995, while the yield grew by only 35%. Framers are trying to cut down operating costs by selecting seeds that do not require multiple doses of chemicals. The initial protection of these engineered seeds is ensured by using seed treatments products.

Increasing Usage in the Asia Pacific region

Geographically, Asia Pacific is the top consumer of seed treatment with a market share of around 60.0%. Major crops produced in Asia include rice, sugar beet, fruits & vegetables, cereals, and grains. Asian countries, such as Korea, China, Japan, and recently Vietnam, are applying more of seed protection/enhancement products for both short-term and perennial crops. Various leading seed treatment companies like Syngenta, BASF, and Bayer are operating in these regions and they regularly organize field trials and training sessions to increase the awareness regarding their products, as well as to present the benefits of using seed treatment products. The increasing agricultural practices and requirement of high-quality agricultural produce are factors that are projected to drive the seed treatment market growth in this region.

Chemical Seed Treatment Industry Overview

The market for chemical seed treatment is consolidated. Top players in the market occupy a major portion of the market, having a diverse and increasing product portfolio. In terms of market share dominance, Syngenta International AG with 24.0% share is followed by Bayer CropScience AG, Corteva Agriscience, BASF SE, and Syngenta. These major players in this market are focusing on increasing their presence through expansions & investments, mergers & acquisitions, partnerships, joint ventures, and agreements. These companies have a strong presence in North America, Asia Pacific, and Europe. They also have manufacturing facilities, along with strong distribution networks across these regions. The major players in this market are focusing on increasing their presence through expansions & product innovations, mergers & acquisitions, partnerships, joint ventures, and agreements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of Substitute Products

- 4.4.4 Threat of New Entrants

- 4.4.5 Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Insecticide

- 5.1.2 Fungicide

- 5.1.3 Other Chemicals

- 5.2 Crop

- 5.2.1 Corn/Maize

- 5.2.2 Soybean

- 5.2.3 Wheat

- 5.2.4 Rice

- 5.2.5 Canola

- 5.2.6 Cotton

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Germany

- 5.3.2.5 Russia

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Thailand

- 5.3.3.5 Vietnam

- 5.3.3.6 Australia

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Syngenta International AG

- 6.3.2 Bayer CropScience AG

- 6.3.3 BASF SE

- 6.3.4 DowDuPont Inc.

- 6.3.5 ADAMA Agricultural Solutions Ltd

- 6.3.6 Advanced Biological Systems

- 6.3.7 BioWorks Inc.

- 6.3.8 Germains Seed Technology

- 6.3.9 Incotec Group BV

- 6.3.10 Nufarm Limited

- 6.3.11 Plant Health Care

- 6.3.12 Precision Laboratories

- 6.3.13 Valent Biosciences Corporation

- 6.3.14 Verdesian Life Sciences