|

|

市場調査レポート

商品コード

1408579

航空機コックピットディスプレイシステム:市場シェア分析、産業動向・統計、2024~2029年成長予測Aircraft Cockpit Display System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機コックピットディスプレイシステム:市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

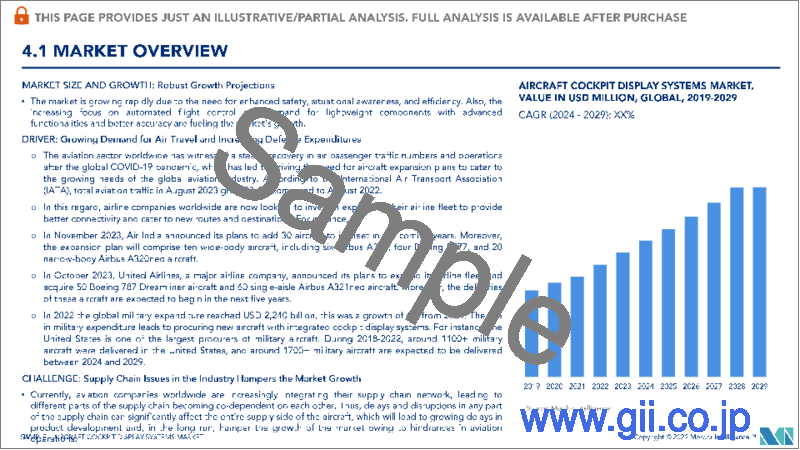

航空機コックピットディスプレイシステム市場は、2024年に29億5,000万米ドルと評価され、予測期間(2024-2029年)のCAGRは5%を記録し、2029年には37億6,000万米ドルに成長すると予測されています。

航空機コックピットディスプレイシステム市場は、主に新規航空機の需要と既存航空機のアビオニクスのアップグレードに依存しています。航空産業は成長しており、新しい航空機の調達は世界のすべての地域で大規模に行われています。コックピット・コンポーネントを含む航空機のサプライ・チェーン全体に対して、巨大な需要を生み出しています。

市場は、安全性、状況認識、効率性の向上に対するニーズの高まりにより急成長しています。また、自動飛行制御への注目の高まりと、高度な機能性とより優れた精度を備えた軽量コンポーネントの需要が、市場の成長に拍車をかけています。しかし、システム障害によるディスプレイのブラックアウトや複雑性の増大が、予測期間中の市場成長を抑制すると予測されています。

航空機コックピットディスプレイシステム市場動向

多機能ディスプレイセグメントが予測期間中に市場を独占する

現代の軍用機のコックピットは、パイロットが要求に応じて外部ディスプレイプロセッサやFLIR、レーダー、武器、カメラなどのビデオセンサに至るまで複数のビデオソースを見ることができるように、ビデオや画像のオプションを改善するための全面ガラス張りの大判マルチファンクションディスプレイを備えています。各国の防衛計画で近代化とアップグレードプログラムが増加する中、新世代の軍用機にはパイロットの状況認識を高めるためにさまざまなタイプの多機能ディスプレイが組み込まれています。例えば、2021年7月、ロシアは新型チェックメイト戦闘機を正式に発表しました。この戦闘機は2023年に初飛行を行い、2026年に量産を開始する予定です。コックピットには、標準的なヘッドアップディスプレイとともに、大型のディスプレイ1つと小型のカラーマルチファンクションディスプレイ数台が搭載されています。また、インドの次期第5世代戦闘機である先進中型戦闘機(AMCA)には、縦向きに配置されたマルチファンクションディスプレイ(MFD)が採用されます。

さらにインドは、20年以上使用されている200機のスホーイ30 MKI戦闘機のアップグレードを計画しています。インドの航空機に対するスーパー・スホーイの標準的なアップグレードには、現地で製造されたレーダー、全面ガラス張りのコックピット、飛行制御コンピューターが含まれます。このように、軍用コックピットにおける多機能ディスプレイの採用拡大が、予測期間中の市場を牽引すると予想されます。

予測期間中、アジア太平洋地域が最も高いCAGRで推移する見込み

アジア太平洋地域は、予測期間中に最も高い成長率を記録すると予測されています。これは主に、インドと中国による航空分野への投資の増加と、航空交通量の増加による民間航空機の需要の高まりによるものです。IATAによると、アジア太平洋の航空会社は2022年の国際航空旅客輸送量で前年比363.3%増を記録し、地域の中で最も高い前年比成長率を維持しました。さらに、同時期に輸送能力は129.9%増加し、搭乗率は37.3%ポイント上昇して74.0%となりました。

2022年11月、中国航空用品(CASC)はエアバス・ジェット機140機の大量購入契約を正式に締結しました。この170億米ドルに相当する発注は、CASCの既存の発注を含んでいます。また、2022年7月、エアバスは中国国際航空、中国東方航空、中国南方航空、深セン航空との間で、合計292機のA320ファミリーの航空機発注契約を締結しました。これは、中国航空市場の極めて前向きな回復の勢いを示すものでした。このような航空機の受注は、これらの航空機に搭載される航空機コックピットディスプレイシステムの高い需要を促進し、予測期間中の市場成長機会の急激な上昇につながると期待されています。

航空機コックピットディスプレイシステム産業概要

航空機コックピットディスプレイシステム市場は、THALES、Collins Aerospace(RTX Corporation)、Elbit Systems Ltd.、Garmin Ltd.、Aspen Avionicsなどのプレイヤーの存在により、適度に統合されています。MROコングロマリットを形成しサービス品質を高めるためのM&Aによる無機的成長により、予測期間中に市場は統合されると予測されます。例えば、2022年にAspen AvionicsはAIROグループの一員となることで基本合意しました。この合意の下、アスペン・アビオニクスは現在と同様に、一般航空市場セグメントをサポートする事業を継続します。AIROグループの一員として、アスペンは一般航空向けアビオニクスだけでなく、民間および軍用航空向けの有人および無人飛行プラットフォーム向けアビオニクス・ソリューションへの投資、リソース、新技術を拡大していく。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- プライマリー・フライト・ディスプレイ(PFD)

- 多機能ディスプレイ(MFD)

- エンジン表示・乗員警報システム(EICAS)

- ディスプレイサイズ別

- 5インチ未満

- 5~10インチ

- 10インチ以上

- 用途別

- 軍事用

- 商業用

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Honeywell International Inc.

- Collins Aerospace(RTX Coroporation)

- THALES

- Elbit Systems Ltd.

- L3Harris Technologies, Inc.

- Garmin Ltd.

- Dyon Avionics

- Aspen Avionics

- Avidyne Corporation

- Northrop Grumman Corporation

第7章 市場機会と今後の動向

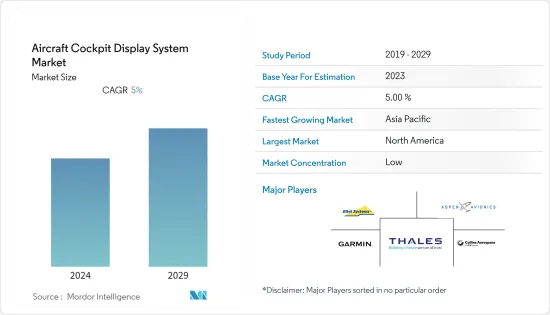

The Aircraft Cockpit Display Systems Market is valued at USD 2.95 billion in 2024 and is expected to grow to USD 3.76 billion by 2029, registering a CAGR of 5% during the forecast period (2024-2029).

The aircraft cockpit display system market is primarily dependent on the demand for new aircraft and upgrades of avionics for existing aircraft. The aviation industry is growing, and the procurement of new aircraft is being done on a large scale in all the regions of the world. It is generating a huge demand for the entire supply chain of the aircraft, which includes the cockpit components.

The market is growing rapidly due to the growing need for enhanced safety, situational awareness, and efficiency. Also, the increasing focus on automated flight control and demand for lightweight components with advanced functionalities and better accuracy are fueling the growth of the market. However, display blackouts due to system failure and increased complexity are projected to restrain the market growth during the forecast period.

Aircraft Cockpit Display System Market Trends

The Multi-Functional Displays Segment to Dominate the Market During the Forecast Period

Modern military aircraft cockpits feature all-glass, large-format multi-functional displays for improving video and imaging options so that the pilots can view multiple video sources ranging from external display processors and video sensors, including FLIR, radar, weapons, and cameras, based on their requirements. With increasing modernizing and upgradation programs taken up by various countries in their defense plans, newer-generation military aircraft are incorporating various types of multi-functional displays to enhance pilot situational awareness. For instance, in July 2021, Russia officially unveiled its new Checkmate fighter, which is expected to take its first flight in 2023, with series production to begin in 2026. The cockpit features one large and several smaller color multi-function displays along with a standard heads-up display. Also, India's upcoming fifth-generation fighter aircraft, Advanced Medium Combat Aircraft (AMCA), will feature a multi-function display (MFD) placed in portrait orientation.

Additionally, India is planning to upgrade 200 Sukhoi 30 MKI combat aircraft that was in service for over 20 years. The Super Sukhoi standard upgrade to Indian aircraft will include locally manufactured radars, a full-glass cockpit, and flight-control computers. Thus, the growing adoption of multi-functional displays in military cockpits is expected to drive the market during the forecast period.

Asia-Pacific is Expected to Register the Highest CAGR During the Forecast Period

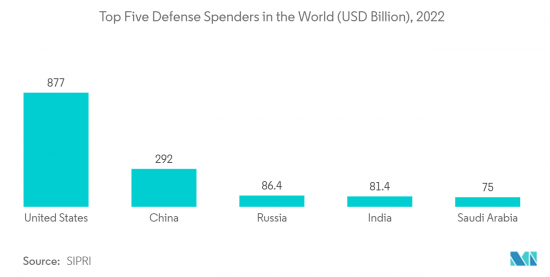

Asia-Pacific is anticipated to register the highest growth rate during the forecast period. It is mainly due to the increasing investments from India and China in the aviation sector and the rising demand for commercial aircraft due to increased air traffic. According to IATA, Asia-Pacific Airlines posted a 363.3% YoY increase in international air passenger traffic during 2022, maintaining the strongest year-over-year rate among the regions. Additionally, the capacity rose 129.9%, and the load factor climbed 37.3 percentage points to 74.0% during the same timeframe.

In November 2022, China Aviation Supplies (CASC) officially signed a bulk purchasing agreement for 140 Airbus jets. The order worth USD 17 billion deal comprised CASC's pre-existing orders. Also, in July 2022, Airbus confirmed the signature of multiple aircraft orders with Air China, China Eastern, China Southern, and Shenzhen Airlines for a total of 292 A320 family aircraft. It demonstrated an extremely positive recovery momentum for the Chinese aviation market. Such orders for aircraft are expected to drive high demand for aircraft cockpit display systems to be installed on these aircraft, leading to an exponential rise in market growth opportunities during the forecast period.

Aircraft Cockpit Display System Industry Overview

The Aircraft Cockpit Display Systems Market is moderately consolidated with the presence of players such as THALES, Collins Aerospace (RTX Corporation), Elbit Systems Ltd., Garmin Ltd., and Aspen Avionics. The market is forecasted to consolidate during the forecast period on account of inorganic growth via mergers and acquisitions to create MRO conglomerates and enhance service quality. For instance, in 2022, Aspen Avionics agreed in principle to become a member of the AIRO Group of companies. Under this agreement, Aspen Avionics will continue to operate as it does presently, supporting the general aviation market segment. As part of the AIRO Group, Aspen will expand its investments, resources, and new technologies in not only avionics for general aviation but also to offer avionics solutions for manned and unmanned flight platforms for both commercial and military aviation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Primary Flight Display (PFD)

- 5.1.2 Multifunction Display (MFD)

- 5.1.3 Engine Indicating and Crew Alerting System (EICAS)

- 5.2 Display Size

- 5.2.1 Less Than 5 Inches

- 5.2.2 5 to 10 Inches

- 5.2.3 Greater Than 10 Inches

- 5.3 Application

- 5.3.1 Military

- 5.3.2 Commercial

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 Collins Aerospace (RTX Coroporation)

- 6.2.3 THALES

- 6.2.4 Elbit Systems Ltd.

- 6.2.5 L3Harris Technologies, Inc.

- 6.2.6 Garmin Ltd.

- 6.2.7 Dyon Avionics

- 6.2.8 Aspen Avionics

- 6.2.9 Avidyne Corporation

- 6.2.10 Northrop Grumman Corporation