|

市場調査レポート

商品コード

1408559

航空分析:市場シェア分析、産業動向と統計、2024~2029年の成長予測Aviation Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空分析:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

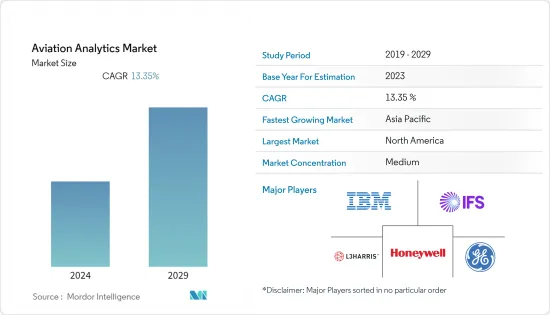

航空分析市場の2024年の市場規模は36億5,000万米ドルで、予測期間(2024~2029年)のCAGRは13.35%を記録し、2029年には68億2,000万米ドルに成長すると予測されています。

データ分析は、効率の改善、顧客体験の向上、セキュリティの強化、コストの削減といった価値あるメリットをもたらすため、航空業界で重要な役割を果たしています。事業運営の最適化に対する需要の高まりは、航空分析市場を牽引する主な要因の1つです。市場の成長は、航空業界においてビジネス機能全体で高度なアナリティクスソリューションの採用が増加していることにも起因しています。航空会社は、航空運行管理のさまざまな局面でアナリティクスを広く採用しています。例えば、航空会社は機械学習アルゴリズムを組み込んだアナリティクスを使用して、各ルートの距離や高度、航空機の種類や重量、天候などに関するフライトデータを収集・分析しています。その結果に基づいて、システムはフライトに必要な最適な燃料量を推定します。さらに、空港業務のデジタル化と人的干渉の軽減に重点を置く傾向が強まっていることも、航空分析市場にチャンスをもたらしています。しかし、従来の機器と最新技術の統合に関する専門知識の不足が、予測数年間における市場の成長を抑制すると思われます。

航空分析市場動向

予測期間中に最も高い成長を遂げるのは航空会社セグメント

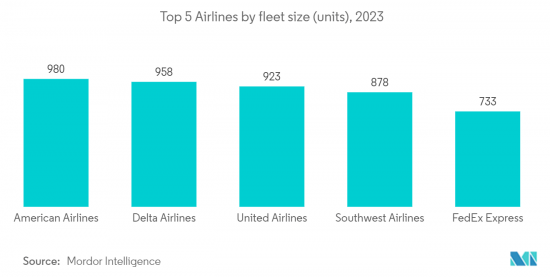

増加する旅客輸送量のニーズに対応するため、世界の航空会社は既存の機体の拡張と近代化を進めています。例えば、2022年11月、エチオピア航空グループは、2035年までに保有機数を140機(現在)から271機に増やすと発表しました。これを達成するため、同航空は少なくとも130機の航空機の追加を検討しており、古い航空機の入れ替えも行っています。同様に、ウィズ・エアも2023年6月に、2024年末までに保有機材を200機以上に拡大する計画を発表しました。同社は2030年までに500機以上の航空機を保有することを目指しています。2021年9月、ユナイテッド航空は、ボーイングとエアバスの単通路機270機を発注し、保有機数と平均サイズを増加させました。このように、保有機数の増加は、機体管理、燃料管理、収益管理などの複数のアプリケーションに対する航空分析の需要を同時に生み出すことになります。

航空会社は、事業運営にアナリティクスの利用を採用する傾向を強めています。この点に関して、2022年5月、アメリカン航空とマイクロソフト・コーポレーションは、テクノロジーを利用して顧客とアメリカン航空のチームメンバーにとってより良い、よりつながりのある体験を創造するために提携しました。この提携の一環として、アメリカン航空は航空会社のアプリケーションと主要なワークロードにMicrosoft Azureを優先的なクラウドプラットフォームとして使用します。

アジア太平洋地域が予測期間中に急成長

アジア太平洋地域は、予測期間中に最も高い成長を示すと予想されています。IATAによると、アジア太平洋地域の航空会社の2023年7月のトラフィックは、2022年7月と比較して105.8%増加し、引き続き地域をリードしています。トラフィックの増加に対応するため、この地域の航空会社は新しい航空機を発注しています。2023年6月、インドのMRO協会が発表したところによると、インドの航空会社は年間100~110機の航空機を追加し、2027年までに1,200機近くの航空機を導入し、毎年15%ずつ航空機のキャパシティを拡大する予定です。エア・インディアは、当面の需要を満たすために積極的に新型機を導入するため、2024年までにナローボディ機が50機、ワイドボディ機が19機増加します。同様に、2023年4月、チャイナエアラインはボーイングB787型機を8機発注しました。機材規模の拡大により、運航と機材管理の課題を合理化するための航空分析の活用が求められています。また、この地域の航空会社が自社のビジネスに航空分析を採用している例もあります。2023年6月、RTXの事業会社であるコリンズ・エアロスペースと日本航空(JAL)は、JALがボーイングB787型機にコリンズ・エアロスペースのAscentiaメンテナンス・パフォーマンス・モニタリング・ソリューションを採用すると発表しました。アジア太平洋諸国における熟練労働力とワークスペースの確保も、同地域の航空分析市場を牽引する要因です。

航空分析業界の概要

航空分析市場は、IBM Corporation、IFS、Honeywell International Inc.、L3Harris Technologies, Inc.、GE Digital(General Electric Company)などの有力企業が市場シェアの大きな割合を占めており、統合されています。航空業界の大手企業との長期契約を獲得するため、これらの企業間の競争は激しいです。これらのプレーヤーは、特に資産管理やセールス&マーケティングなどの機能に焦点を当てた幅広い航空分析ソリューションを提供しています。契約、買収、事業拡大、新製品の発売、提携・契約といった様々な成長戦略が、航空分析市場におけるプレゼンスをさらに拡大するために大手企業によって採用されています。例えば、2021年12月、TAP Air PortugalとLufthansa Technik AGは、AVIATARが航空会社のエアバス全機種にデジタルサポートを提供することで合意しました。TAPエア・ポルトガルは、コンディション・モニタリング、イベント分析、フリートマップを含むAVIATAR製品を活用し、航空機運航のデジタル最適化とコスト削減を実現します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- エンドユーザー別

- 航空会社

- 空港

- ビジネス機能別

- セールス&マーケティング

- 財務

- MROオペレーション

- サプライチェーン

- 用途別

- リスク管理

- 在庫管理

- 燃料管理

- 収益管理

- 顧客分析

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- LexisNexis Risk Solutions

- GE Digital(General Electric Company)

- Collins Aerospace

- Honeywell International Inc.

- L3Harris Technologies, Inc.

- IBM Corporation

- IFS

- The Boeing Company

- IGT Solutions Pvt. Ltd.

- OAG Aviation Worldwide Limited

第7章 市場機会と今後の動向

The Aviation Analytics Market is valued at USD 3.65 billion in 2024 and is expected to grow to USD 6.82 billion by 2029, registering a CAGR of 13.35% during the forecast period (2024-2029).

Data analytics plays a critical role in the airline industry as it provides valuable benefits such as improved efficiency, enhanced customer experience, increased security, and reduced costs. The increasing demand for optimized business operations is one of the major factors driving the market for aviation analytics. The market growth is also attributed to the rising adoption of advanced analytics solutions across business functions in the aviation industry. Airlines are widely adopting analytics for various aspects of airline operation management. For instance, airlines use analytics with built-in machine learning algorithms to collect and analyze flight data regarding each route's distance and altitude, aircraft type and weight, weather, etc. Based on the findings, systems estimate the optimal amount of fuel needed for a flight. Additionally, an increase in focus on digitalizing airport operations and reducing human interference is also creating opportunities for the aviation analytics market. However, a lack of expertise in integrating conventional devices with modern technology will restrain the growth of the market in the forecast years.

Aviation Analytics Market Trends

Airlines Segment to Witness Highest Growth During the Forecast Period

To meet the needs of rising passenger traffic, airlines globally are expanding and modernizing their existing fleet. For instance, in November 2022, Ethiopian Airlines Group announced to increase their fleet size from 140 (currently) to 271 aircraft by 2035. To achieve this, the airline is considering the addition of at least 130 aircraft, with the replacement of older aircraft as well. Similarly, in June 2023, Wizz Air also announced its plans to expand its fleet to over 200 aircraft by the end of 2024. The company aspires to build a fleet of over 500 aircraft by 2030. In September 2021, United Airlines placed an order for 270 single-aisle Boeing and Airbus planes to increase the number of planes in its fleet and their average size. Thus, an increase in fleet size will create a simultaneous demand for aviation analytics for multiple applications such as fleet management, fuel management, revenue management, etc.

Airlines are increasingly adopting the use of analytics for their business operations. In this regard, in May 2022, American Airlines and Microsoft Corporation partnered to use technology to create better, more connected experiences for customers and American Airlines team members. As a part of the partnership, American Airlines will use Microsoft Azure as its preferred cloud platform for its airline applications and key workloads.

Asia-Pacific to Demonstrate Rapid Growht During the Forecast Period

Asia-Pacific is expected to showcase the highest growth during the forecast period. As per IATA, airlines in Asia-Pacific saw a 105.8% increase in July 2023 traffic compared to July 2022, continuing to lead the regions. To cope with the rising traffic, airlines in the region are placing new aircraft orders. In June 2023, it was announced by the MRO Associations of India that Indian airlines are poised to expand their fleet capacity by 15% annually, with an addition of 100 to 110 aircraft per year, leading to close to 1,200 aircraft by 2027. Air India's fleet will grow by 50 narrowbody and 19 widebody aircraft by 2024 as it aggressively inducts new planes to meet immediate demand. Likewise, in April 2023, China Airlines placed an order for eight Boeing B787 aircraft. An increase in fleet size demands the use of aviation analytics to streamline operations and fleet management challenges. Also, there are instances of airlines in the region adopting aviation analytics for their businesses. In June 2023, Collins Aerospace, an RTX business, and Japan Airlines (JAL) announced that JAL would use Collins Aerospace's Ascentia maintenance performance monitoring solution on its Boeing B787 fleet. Availability of skilled labor and workspace in countries of Asia-Pacific are additional factors driving the aviation analytics market in the region.

Aviation Analytics Industry Overview

The aviation analytics market is consolidated with prominent players owning the major percentage of market shares, such as IBM Corporation, IFS, Honeywell International Inc., L3Harris Technologies, Inc., and GE Digital (General Electric Company). The intensity of rivalry is high among them, mostly for obtaining long-term contracts with big players in the aviation industry. These players offer a wide range of aviation analytics solutions that focus on functions including wealth management and sales & marketing, among others. Various growth strategies such as contracts, acquisitions, expansions, new product launches, and partnerships & agreements are being adopted by the leading players to further expand their presence in the aviation analytics market. For instance, in December 2021, TAP Air Portugal and Lufthansa Technik AG agreed that AVIATAR would provide digital support for the airline's complete Airbus fleet. TAP Air Portugal will leverage AVIATAR products, including condition monitoring, event analytics, and fleet maps, to digitally optimize its aircraft operations and realize cost savings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Airlines

- 5.1.2 Airports

- 5.2 Business Function

- 5.2.1 Sales & Marketing

- 5.2.2 Finance

- 5.2.3 MRO Opertions

- 5.2.4 Supply Chain

- 5.3 Application

- 5.3.1 Risk Management

- 5.3.2 Inventory Management

- 5.3.3 Fuel Management

- 5.3.4 Revenue Management

- 5.3.5 Customer Analytics

- 5.3.6 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 LexisNexis Risk Solutions

- 6.2.2 GE Digital (General Electric Company)

- 6.2.3 Collins Aerospace

- 6.2.4 Honeywell International Inc.

- 6.2.5 L3Harris Technologies, Inc.

- 6.2.6 IBM Corporation

- 6.2.7 IFS

- 6.2.8 The Boeing Company

- 6.2.9 IGT Solutions Pvt. Ltd.

- 6.2.10 OAG Aviation Worldwide Limited