|

市場調査レポート

商品コード

1408320

対話型患者ケアシステム-市場シェア分析、産業動向・統計、2024~2029年成長予測Interactive Patient Care Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 対話型患者ケアシステム-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

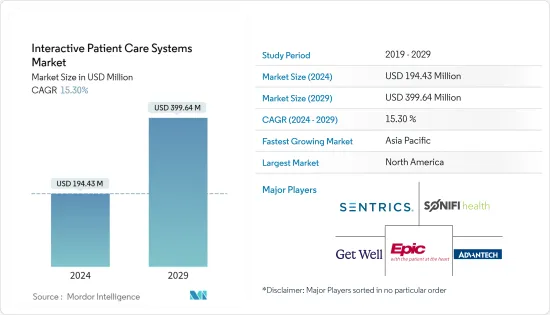

対話型患者ケアシステム市場規模は、2024年に1億9,443万米ドルと推定され、2029年には3億9,964万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは15.30%で成長します。

COVID-19パンデミックは当初、対話型患者ケアシステム市場に大きな影響を与えました。パンデミックによる入院患者の増加により、双方向型患者ケアソリューションの利用が増加しました。例えば、Deutsches Arzteblatt International誌が2022年11月に発表した記事によると、ドイツで研究が行われ、パンデミック初期にCOVID-19による入院患者数が大幅に増加したことが示され、病院での対話型患者ケアシステムの使用も増加することが予想されました。このように、COVID-19の流行は市場の成長に大きな影響を与えました。しかし、パンデミックが沈静化するにつれて、本調査の予測期間中、市場はパンデミック以前の成長レベルを経験することが予想されます。

慢性疾患の罹患率の上昇と相まって、患者エンゲージメントソリューションに対するニーズが高まっていること、技術の進歩が進み、双方向患者ケアシステムの採用が増加していることなどの要因が、市場の成長を押し上げると予想されます。

がん、糖尿病、心血管疾患などの慢性疾患の世界の有病率の上昇は、市場成長を促進する重要な要因です。これにより、入院患者と外来患者の両方の環境において、対話型患者ケアシステムなどの患者参加型ソリューションのニーズが高まると予想されます。例えば、Chinese Medical Journalが2022年2月に発表した記事によると、2022年に中国と米国で新たに診断されたがん患者は推定482万人と237万人です。したがって、がんの負担の増大は、対話型患者ケアシステムの採用を促進し、調査市場の成長を引き起こすと予想されます。

さらに、Journal of Environmental Research and Public Healthが2023年2月に発表した論文によると、デジタルヘルス技術は世界中の医療インフラで急速に採用されています。この情報源はまた、米国遠隔医療協会のような組織が、心臓病、喘息、糖尿病のような慢性疾患のための対話型患者エンゲージメントサービスを提供していると述べています。このように、対話型患者ケアシステムの採用が増加していることも、市場成長を促進する大きな要因となっています。

さらに、市場の主要企業による新製品の発売や戦略的活動は、調査対象市場の成長にプラスの影響を与えています。例えば、2021年1月、GetWellNetworkは、医療機関がAI対応コミュニケーション技術を通じてパーソナライズされたアウトリーチを拡大することを可能にする革新的な企業向け消費者エンゲージメントプラットフォームであるDocent Healthを買収しました。このような買収により、同市場は予測期間中に大きく成長すると予想されます。

したがって、慢性疾患の有病率の上昇、対話型患者ケアシステムの採用の増加、市場参入企業による戦略的活動の高まりなどの上記の要因によって、調査市場は分析期間中に成長すると予測されます。しかし、熟練した専門家の不足が市場成長の妨げになる可能性が高いです。

対話型患者ケアシステム市場の動向

入院患者ソリューションセグメントは予測期間中に大幅な成長が見込まれる

入院患者向けソリューションとは、回復やリハビリのために患者が入院する病院やクリニックにおける双方向患者ケアシステムを指します。様々な慢性疾患による入院患者数の世界の増加や、がん、糖尿病、喘息などの慢性疾患の有病率の増加などの要因が、予測期間中に調査セグメントの成長を促進すると予想されています。

例えば、カナダ健康情報研究所が2023年2月に発表したデータによると、2022年のカナダの急性入院患者数は約290万人で、2021年の270万人から増加しました。このように、カナダにおける入院率の高さも、対話型患者ケアシステムの採用を後押しし、同分野の成長を促進すると見られています。

さらに、世界的に様々な慢性疾患の有病率が上昇していることも、入院患者を増加させ、双方向型患者ケアシステムの需要を増加させるため、セグメントの成長を促進すると予想されます。例えば、2022年3月にPubMedが発表した論文によると、スウェーデン南部のプライマリ医療センターで調査を行ったところ、心不全(HF)の全有病率は2.06%だった。HF患者の99.07%は多疾患を合併していました。このように、対象集団の高い負担とCVDの持続的なリスクは、セグメントの成長を促進すると予想されます。

したがって、入院患者向けソリューション分野は予測期間中に大きく成長すると予想されます。これは、入院率の上昇や様々な慢性疾患の有病率の増加など、上述の要因によるものです。

予測期間中、北米が市場で大きなシェアを占める見込み

北米は、技術的に高度な製品を容易に入手でき、双方向患者ケアシステムの採用が増加していることから、大きな市場シェアを占めると予想されます。さらに、同地域における様々な慢性疾患の有病率の上昇や高齢者人口の増加も、北米の調査市場の成長に寄与する主要因の一つです。

例えば、2022年7月にカナダ健康情報研究所が更新したデータによると、2022年には約240万人のカナダ人が心臓病を患っていると推定されています。このように、国全体で疾患の負担が増加していることから、対話型患者ケアシステムの導入が増加し、市場の成長を促進すると予想されます。

さらに、同国の市場参入企業による事業拡大や製品発売などの活動が活発化していることも、同分野の成長を高めると予想されます。例えば、2022年3月、GetWell社はポピュレーションヘルスの提供を拡大しました。これには対話型の患者ケアプラットフォームが含まれ、支払者やリスクのあるプロバイダーが、より多くの会員を取り込むためのプログラムを技術的に有効化し、拡大できるよう支援します。

したがって、さまざまな慢性疾患の高い有病率や市場参入企業の活動の増加など、上記の要因によって、調査市場の成長は北米地域で予測されます。

対話型患者ケアシステム産業概要

対話型患者ケアシステム市場は、世界的と地域的に事業を展開する複数の企業が存在するため、その性質上、断片化されています。競合情勢には、市場シェアを持ち、知名度の高い国際企業や地元企業の分析が含まれます。主要市場参入企業には、GetWellNetwork, Inc.、Epic Systems Corporation、SONIFI Health Incorporated、Advantech、Sentricsなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の発生率の上昇と患者参加型ソリューションへのニーズの高まり

- 技術の進歩と双方向患者ケアシステムの採用増加

- 市場抑制要因

- 熟練した専門家の不足

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- タイプ別

- 入院患者向けソリューション

- 外来患者向けソリューション

- 製品別

- ハードウェア

- ソフトウェア

- エンドユーザー別

- 病院

- クリニック

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- GetWellNetwork, Inc.

- Epic Systems Corporation

- SONIFI Health Incorporated

- Advantech Co., Ltd.

- Sentrics

- Evideon

- Aceso Interactive Inc

- PDi Communication Systems, Inc.

- Lincor

- InterSystems Corporation

- Hopitel Inc

- Oneview Healthcare

第7章 市場機会と今後の動向

The Interactive Patient Care Systems Market size is estimated at USD 194.43 million in 2024, and is expected to reach USD 399.64 million by 2029, growing at a CAGR of 15.30% during the forecast period (2024-2029).

The COVID-19 pandemic initially substantially impacted the interactive patient care system market. The increased hospitalizations during the pandemic increased the usage of interactive patient care solutions. For instance, according to an article published by the Journal of Deutsches Arzteblatt International in November 2022, a study was conducted in Germany, which showed that the number of inpatient admissions due to COVID-19 significantly increased during the early pandemic, which also expectedly increased the usage of interactive patient care systems in the hospitals. Thus, the COVID-19 outbreak affected the market's growth significantly. However, as the pandemic subsided, the market is expected to experience pre-pandemic growth levels during the study's forecast period.

Factors such as the rising incidence of chronic diseases coupled with the increased need for patient engagement solutions and the increasing technological advancements and rising adoption of interactive patient care systems are expected to boost the market growth.

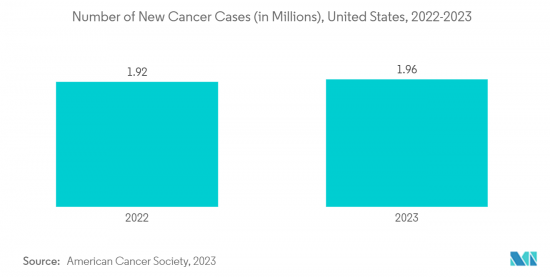

The rising prevalence of chronic diseases worldwide, such as cancer, diabetes, and cardiovascular diseases, is a significant factor driving the market growth. It is expected to boost the need for patient engagement solutions such as interactive patient care systems in both inpatient and outpatient settings. For instance, according to an article published by the Chinese Medical Journal in February 2022, an estimated 4,820,000 and 2,370,000 new cancer cases were diagnosed in China and the United States in 2022. Hence, the growing burden of cancers is expected to drive the adoption of interactive patient care systems, which will cause the growth of the studied market.

Moreover, according to an article published by the Journal of Environmental Research and Public Health in February 2023, digital health technologies are being rapidly adopted in healthcare infrastructures worldwide. The source also stated that organizations like the American Telemedicine Association provide interactive patient engagement services for chronic diseases like heart disease, asthma, and diabetes. Thus, the rising adoption of interactive patient care systems is also a significant factor driving market growth.

In addition, new product launches and strategic activities by major players in the market are positively affecting the growth of the studied market. For instance, in January 2021, GetWellNetwork acquired Docent Health, an innovative enterprise consumer engagement platform that enables healthcare organizations to scale personalized outreach through AI-enabled communication technology. Thus, owing to such acquisitions, the studied market is expected to grow significantly over the forecast period.

Therefore, owing to the factors above, such as the rising prevalence of chronic diseases, the increasing adoption of interactive patient care systems, and the rising strategic activities by market players, the studied market is anticipated to grow over the analysis period. However, the lack of skilled professionals is likely to impede market growth.

Interactive Patient Care Systems Market Trends

Inpatient Solutions Segment is Expected to Witness Significant Growth Over the Forecast Period

Inpatient solutions refer to interactive patient care systems in hospitals and clinics where the patients are kept for recovery and rehabilitation. Factors such as the rising number of hospitalizations worldwide due to various chronic diseases and the increasing prevalence of chronic diseases such as cancer, diabetes, and asthma, among others, are expected to boost the growth of the studied segment during the forecast period.

For instance, according to the data published by the Canadian Institute for Health Information in February 2023, there were almost 2.9 million acute inpatient hospitalizations in Canada in 2022, which increased from 2.7 million in 2021. Thus, the high hospitalization rate in Canada is also expected to boost the adoption of interactive patient care systems, likely driving segment growth.

Moreover, the rising prevalence of various chronic diseases worldwide is also expected to drive segment growth, as it would also increase inpatient hospitalizations, thus increasing the demand for interactive patient care systems. For instance, according to the article published by PubMed in March 2022, when the research was conducted in primary healthcare centers in southern Sweden, the overall prevalence of heart failure (HF) was 2.06%. 99.07% of the patients with HF were associated with multimorbidity. Thus, the target population's high burden and persistent risk of CVD are expected to drive segment growth.

Therefore, the inpatient solutions segment is expected to grow significantly over the forecast period. It is due to the abovementioned factors, such as the rising hospitalization rates and the increasing prevalence of various chronic diseases.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is expected to hold a significant market share due to the easy availability of technologically advanced products and the increased adoption of interactive patient care systems. Moreover, the rising prevalence of various chronic diseases and the increasing geriatric population in the region are also among the key factors contributing to the growth of the studied market in North America.

For instance, according to the data updated by the Canadian Institute for Health Information in July 2022, it was estimated that about 2.4 million Canadians had heart disease in 2022. Thus, with the increasing burden of conditions across the country, interactive patient care system adoption is expected to increase, driving market growth.

Moreover, the rising activities, such as expansions and product launches by market players in the country, are also expected to enhance segment growth. For instance, in March 2022, GetWell expanded its population health offerings. It includes interactive patient care platforms to help payers and at-risk providers tech-enable and scale their programs to engage more members.

Therefore, owing to the factors mentioned above, such as the high prevalence of various chronic diseases and the increasing activities by market players, the growth of the studied market is anticipated in the North American region.

Interactive Patient Care Systems Industry Overview

The interactive patient care systems market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes analyzing a few international and local companies that hold market shares and are well known. Some of the key market players include GetWellNetwork, Inc., Epic Systems Corporation, SONIFI Health Incorporated, Advantech Co., Ltd., and Sentrics, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Chronic Diseases Coupled With The Increased Need for Patient Engagement Solutions

- 4.2.2 Increasing Technological Advancements and Rising Adoption of Interactive Patient Care Systems

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type

- 5.1.1 Inpatient Solutions

- 5.1.2 Outpatient Solutions

- 5.2 By Product

- 5.2.1 Hardware

- 5.2.2 Software

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Clinics

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 GetWellNetwork, Inc.

- 6.1.2 Epic Systems Corporation

- 6.1.3 SONIFI Health Incorporated

- 6.1.4 Advantech Co., Ltd.

- 6.1.5 Sentrics

- 6.1.6 Evideon

- 6.1.7 Aceso Interactive Inc

- 6.1.8 PDi Communication Systems, Inc.

- 6.1.9 Lincor

- 6.1.10 InterSystems Corporation

- 6.1.11 Hopitel Inc

- 6.1.12 Oneview Healthcare