|

市場調査レポート

商品コード

1408319

植込み型除細動器:市場シェア分析、産業動向と統計、2024~2029年の成長予測Implantable Defibrillators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 植込み型除細動器:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

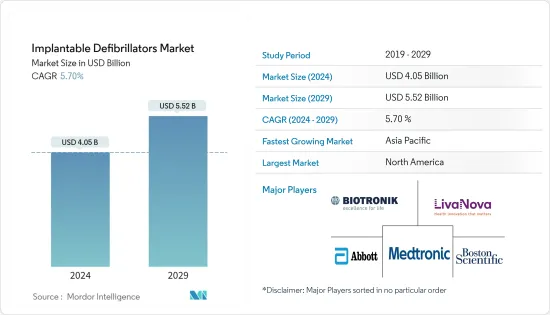

植込み型除細動器市場規模は、2024年に40億5,000万米ドルと推定され、2029年には55億2,000万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは5.70%で成長すると予測されます。

COVID-19は、COVID-19患者の心停止の増加により、パンデミック期間中に植込み型除細動器市場に大きな影響を与えました。最初のパンデミック時には市場は減少したが、COVID-19患者における植込み型除細動器の需要により増加しました。例えば、2022年6月にJournal of Cardiac Failureに掲載された研究によると、心不全患者に植込まれた植込み型除細動器(ICD)は、心房細動(AF)などの心臓の状態のマーカーに関する有益な情報を提供しました。そのため、COVID-19パンデミック時に植込み型除細動器の採用が増加し、パンデミック後期の市場成長を促進すると予想されました。

植込み型除細動器市場の成長を促進する要因としては、心室細動、心室頻拍などの不整脈、心筋梗塞や先天性心疾患などの心臓疾患の有病率の増加が挙げられます。

心不全のような心臓病の有病率の増加は、市場の成長を促進すると予想されます。例えば、2022年の米国心臓協会の年次報告書によると、米国における心不全の有病率は2021年には約600万人で、総人口の1.8%を占めています。さらに、米国疾病予防管理センターによると、2023年7月、2022年に米国で心筋梗塞を患った18歳以上の成人の割合は、総人口の3%でした。このような心筋梗塞の大規模な有病率は、植込み型除細動器の採用を増加させ、市場の成長を促進すると予想されます。

また、英国心臓財団によると、2022年8月、米国では約760万人が心臓・循環器疾患に罹患しています。英国のような先進国における心血管疾患の大規模な有病率は、植込み型除細動器に対する需要をエスカレートさせ、調査期間における対象市場の成長を促進します。

近年の技術進歩の高まりと植込み型除細動器の成功率の向上は、市場成長をさらに押し上げると予想されます。例えば、2022年8月にMedtronic PLCが発表した臨床研究では、突然の心停止を止めることを目的とした新しい低侵襲除細動器インプラント(Medtronic EV ICDシステム)の有効性が実証されました。この血管外植込み型除細動器システムは、その主要コンポーネントを左脇の下に含むもので、振動を抑え、頻脈を予防し、患者が除細動ショックを回避するためのバックアップペーシング療法を提供します。

したがって、心臓不整脈やその他の心臓病の有病率の増加は、心停止への早期アクセスのための植込み型除細動器の需要を増加させると予想されます。さらに、予測期間中に調査対象市場の成長を押し上げると予想されます。しかし、植込み型除細動器に対する厳しい規制の枠組みが市場の成長を阻害すると予想されます。

植込み型除細動器市場の動向

皮下植込み型除細動器(S-ICD)が予測期間中に最も速い成長を示すと予測されます。

皮下植込み型除細動器(S-ICD)は、心臓のリズムを分析するための皮下電極を使用して、心室頻拍/心室細動を効果的に感知、識別、変換します。心臓突然死を予防するための確立された治療法であり、特定の患者において経静脈植込み型除細動器(ICD)システムの代替となります。

同分野の成長を促進する要因としては、主要市場参入企業の取り組みが活発化していることや、人々の間でS-ICDに対する認識が高まっていることが挙げられます。

主要市場参入企業は、皮下植込み型除細動器の安全性と有効性を明らかにするために絶えず取り組んでおり、これが同分野の成長を促進すると予想されます。例えば、2021年12月、Boston Scientific Corporationは、皮下植込み型除細動器の有効性、性能、安全性を評価するためにS-ICDに関する研究を実施しました。その結果、S-ICDシステムは、心臓や胸骨下部に触れることなく保護することができるため、その場所に挿入されたリードに関連する多くの困難を防ぐことができることが示唆されました。

さらに、皮下植込み型除細動器にはさまざまな利点があり、同分野の成長を促進すると予想されています。例えば、2021年7月にArrhythmia &Electrophysiology Review(AER)誌に掲載された研究によると、S-ICDは、気胸や心臓穿孔、全身感染など、新規植込みによる短期的・長期的な危険の多くを患者が回避するのに役立ちます。さらに、S-ICDは多施設共同臨床試験を受け、その有効性が実証され、新たな知見では、状況によっては経静脈的ICDよりも優れている可能性さえ示されました。したがって、皮下植込み型除細動器に関連する利点が需要を増加させ、調査対象セグメントの成長を牽引しています。

したがって、皮下植込み型除細動器には大きなメリットがあるため、このセグメントは予測期間中に最も急速に成長すると予想されます。

予測期間中、北米が調査対象市場の主要シェアを占める見込み

北米は、予測期間を通じて植込み型除細動器市場全体で大きなシェアを占めると予想されます。その背景には、高い医療支出、不整脈、粗動、細動などの心血管疾患におけるICDの有効性に対する認知度の高まり、同地域における主要な主要市場参入企業の存在があります。

さらに、米国除細動器市場は、パートナーシップによる技術的進歩の高まりと、支援的な償還政策により北米内で成長しています。さらに、心血管疾患に対する政府助成金の増加や研究開発活動の活発化などが、米国における植込み型除細動器の採用を促進し、市場成長を後押しします。

米国の人口の間で不整脈などの心血管疾患(CVD)の有病率が上昇していることから、適切な疾患管理のために除細動器の採用が増加しています。例えば、Arrhythmia Alliance Report 2023によると、米国では毎年、65歳以下の米国人の約50人に1人、65歳以上の米国人の10人に1人が心房細動に罹患し、約2,100人に1人が心室性不整脈を経験しています。そのため、不整脈の発生率は高く、植込み型除細動器に対する需要を押し上げると予測され、市場成長の原動力となることが期待されます。

さらに、米国の病院やクリニックでの植込み型除細動器の採用が増加しており、同地域の市場成長を促進すると予測されています。例えば、2021年12月、国際的な臨床試験の一環として、クリーブランドクリニックは世界で初めて2人の患者にリードレスペースメーカー除細動器システムの移植に成功しました。心拍数の低下や増加に対する治療を約束するこの革新的なデバイスは、リードレスペースメーカーと皮下植込み型除細動器の技術を組み合わせたものです。

そのため、この地域では植込み型除細動器の採用が増加し、心臓リズム障害の有病率が高まっていることから、市場成長の原動力になると予想されます。

植込み型除細動器産業概要

植込み型除細動器市場は、確立された市場参入企業によって高度に統合されています。競合要因としては、植込み型除細動器に関する研究開発の活発化、規制当局からの承認取得の増加、市場参入企業が採用する主要取り組みなどが挙げられます。市場に参入している企業には、Boston Scientific Corporation、Microport Scientific Corporation、Medtronic PLC、Abbott、Biotronikなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心不整脈とその他の心臓疾患の有病率の増加

- 植込み型除細動器分野における技術の進歩

- 市場抑制要因

- 厳しい規制枠組み

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- タイプ別

- シングルチャンバー型

- デュアルチャンバー型

- 両心室型(心臓再同期療法)

- ルート別

- 経静脈/従来型ICD

- 皮下(S-ICD)

- エンドユーザー別

- 病院

- 専門クリニック

- 外来手術センター

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Boston Scientific Corporation

- LivaNova PLC

- Microport Scientific Corporation

- Medtronic Plc

- Abbott

- Biotronik

第7章 市場機会と今後の動向

The Implantable Defibrillators Market size is estimated at USD 4.05 billion in 2024, and is expected to reach USD 5.52 billion by 2029, growing at a CAGR of 5.70% during the forecast period (2024-2029).

COVID-19 significantly impacted the implantable defibrillator market during the pandemic due to the rise in cardiac arrest among COVID-19 patients. The market declined during the initial pandemic but increased due to the demand for implantable defibrillators in COVID-19 patients. For instance, according to the study published in the Journal of Cardiac Failure in June 2022, implantable cardioverter defibrillators (ICDs) implanted in patients with heart failure provided helpful information on markers of cardiac status such as atrial fibrillation (AF). Thus, it was expected to increase adoption of implantable defibrillators during the COVID-19 pandemic, thereby driving market growth during the late pandemic.

The factors driving the growth of the implantable defibrillators market include the increasing prevalence of cardiac arrhythmias such as ventricular fibrillation, ventricular tachycardia, and other heart diseases such as myocardial infarction or congenital heart diseases.

The rising prevalence of heart diseases such as heart failure is anticipated to drive market growth. For instance, according to the American Heart Association's annual report in 2022, the prevalence rate of heart failure in the United States was around 6 million in 2021, accounting for 1.8% of the total population. Furthermore, according to the Centers for Disease Control and Prevention, in July 2023, the percentage of adults aged 18 and over living with myocardial infarction in the United States in 2022 was 3% of the total population. Such a massive prevalence of myocardial infarction is anticipated to increase the adoption of implantable defibrillators, driving market growth.

In addition, according to the British Heart Foundation, in August 2022, around 7.6 million people in the United Kindom suffered from heart and circulatory diseases 2022. The massive prevalence of cardiovascular disease in developed countries such as the United Kingdom escalates the demand for implantable defibrillators, fueling the target market growth in the studied period.

The rising technological advancements and improved success rates of implantable defibrillators in recent years are anticipated to boost market growth further. For instance, in August 2022, clinical research presented by Medtronic PLC demonstrated the effectiveness of a novel minimally invasive defibrillator implant (Medtronic EV ICD system) intended to stop a sudden cardiac arrest. The extravascular implantable defibrillator system, which includes its primary component under the left armpit, offers backup pacing therapy to reduce vibrations, prevent tachycardia, and help patients avoid defibrillation shock.

Therefore, the increasing prevalence of cardiac arrhythmia and other heart diseases is expected to increase the demand for implantable defibrillators for early access to cardiac arrest. It is further expected to boost the growth of the studied market over the forecast period. However, the stringent regulatory framework for implantable defibrillators is anticipated to impede market growth.

Implantable Defibrillators Market Trends

Subcutaneous Implantable Cardioverter Defibrillator (S-ICD) is Anticipated to Show the Fastest Growth Over the Forecast Period.

The Subcutaneous Implantable Cardioverter Defibrillator (S-ICD) effectively senses, discriminates, and converts ventricular tachycardia/ventricular fibrillation using a subcutaneous electrode to analyze the heart rhythm. It is an established therapy for preventing sudden cardiac death and an alternative to a transvenous implantable cardioverter-defibrillator (ICD) system in selected patients.

The factors driving the segment's growth include the rising initiatives from the key market players and the increasing awareness of S-ICD among people.

Key market players are constantly working to identify the safety and effectiveness of subcutaneous implantable defibrillators, which are anticipated to drive segment growth. For instance, in December 2021, Boston Scientific Corporation conducted a study on S-ICD to assess the subcutaneous implantable defibrillator's efficacy, performance, and safety. The findings suggested that the S-ICD system prevents many difficulties connected with leads inserted in those locations because it offers protection without touching the heart or substernal area.

Furthermore, the various advantages of subcutaneous implantable defibrillators are anticipated to propel segment growth. For instance, according to the study published in the Arrhythmia & Electrophysiology Review (AER) Journal in July 2021, S-ICDs help patients avoid many of the short and long-term dangers of de novo implantation, including pneumothorax and heart perforation, and systemic infection. Additionally, S-ICDs underwent multicentre clinical studies where they demonstrated their efficacy, and new findings indicated that they might even be superior to Transvenous ICDs in some circumstances. Therefore, benefits associated with subcutaneous implantable defibrillators increase the demand and drive the growth of the segment studied.

Therefore, owing to the significant benefits of subcutaneous implantable defibrillators, the segment is anticipated to grow fastest over the forecast period.

North America is Expected to Hold a Major Share of the Studied Market Over the Forecast Period

North America is expected to hold a significant share of the overall implantable defibrillators market throughout the forecast period. It is due to the high healthcare expenditures, rising awareness of ICD's effectiveness in cardiovascular disorders such as arrhythmias, flutters, and fibrillations, and the presence of major key market players in the region.

Furthermore, the United States defibrillator market is growing within North America due to rising technological advancements through partnerships and the supportive reimbursement policy. In addition, the increase in government funding for cardiovascular diseases and the increase in research and development activities, among others, will drive the adoption of implantable defibrillators in the United States, driving market growth.

The rising prevalence of cardiovascular diseases (CVD), such as arrhythmias, among the population of the United States led to increased adoption of defibrillators for proper disease management. For instance, according to the Arrhythmia Alliance Report 2023, about 1 in 50 Americans under age 65, whereas 1 in 10 Americans over age 65 suffer from atrial fibrillation annually, and around 1 in 2,100 persons experience ventricular arrhythmias in the United States annually. Therefore, the considerable incidence of arrhythmia is projected to boost the demand for implantable defibrillators, which is anticipated to drive market growth.

Moreover, the rising adoption of implantable defibrillators in the hospitals and clinics of the United States is anticipated to drive market growth in the region. For instance, in December 2021, as part of an international clinical trial, Cleveland Clinic successfully implanted leadless pacemaker defibrillator systems in the first two patients in the world. The innovative device, which promises to provide treatment for low and increased heart rates, combines the technology of a leadless pacemaker with a subcutaneous implantable cardioverter defibrillator.

Therefore, the rising adoption of implantable defibrillators and the increasing prevalence of cardiac rhythm disorders in the region is anticipated to drive market growth.

Implantable Defibrillators Industry Overview

The market for implantable defibrillators is highly consolidated with established market players. The factors owing to the competition include the rising research and development on implantable defibrillators, rising approvals from regulatory agencies, and the key initiatives adopted by the market players. Some players operating in the market include Boston Scientific Corporation, Microport Scientific Corporation, Medtronic PLC, Abbott, and Biotronik, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Cardiac Arrhythmia and Other Heart Diseases.

- 4.2.2 Technological Advancements in the Field of Implantable Defibrillators

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Framework

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type

- 5.1.1 Singel Chambered

- 5.1.2 Dual Chambered

- 5.1.3 Biventricular (cardiac resynchronization therapy)

- 5.2 By Route

- 5.2.1 Transvenous/Traditional ICD

- 5.2.2 Subcutaneous (S-ICD)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Speciality Clinics

- 5.3.3 Ambulatory Surgical Centers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Boston Scientific Corporation

- 6.1.2 LivaNova PLC

- 6.1.3 Microport Scientific Corporation

- 6.1.4 Medtronic Plc

- 6.1.5 Abbott

- 6.1.6 Biotronik