|

市場調査レポート

商品コード

1408270

C型肝炎:市場シェア分析、産業動向と統計、2024~2029年の成長予測Hepatitis C - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| C型肝炎:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

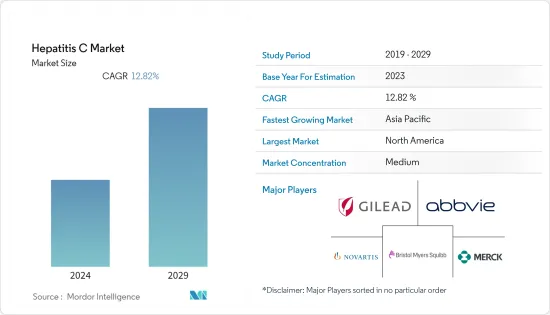

C型肝炎市場は予測期間中に12.82%のCAGRで推移する見込み

主要ハイライト

- COVID-19パンデミックはC型肝炎市場に大きな影響を与え、パンデミック期の市場成長率に影響を与えました。例えば、2022年6月にJournal of Managed Care &Specialty Pharmacyが発表した研究によると、C型肝炎(HCV)患者は治療へのアクセスが悪かった。COVID-19のパンデミックの中、治療コースを完了する可能性はかなり低かった。この研究では、流行期を通じてHCV DAA治療と検査モニタリングのアドヒアランスの低下が観察されました。

- さらに、上記の研究では、COVID-19後の環境における患者のための遠隔医療という選択肢が、HCV患者の治療へのアクセスを向上させる上でさらなる利点となりうることが強調されました。したがって、COVID-19後の診断と治療へのアクセスが改善されたことで、C型肝炎検査と薬剤の需要は名目上増加しました。例えば、2023年5月にInquiryが発表した記事によると、COVID-19の大流行は、C型肝炎ウイルス(HCV)、ヒト免疫不全ウイルス(HIV)、とこの種のケアを必要とする他の慢性疾患の患者へのサービスを提供するための遠隔医療の利用を強化しました。

- さらに、パンデミック後、HCVとHIVの単独感染者と重複感染者の間で、薬剤師が提供する遠隔医療サービスの受容性が認められました。このように、分析によると、COVID-19の影響は流行の初期段階では深刻でした。しかし、パンデミック後の時代における遠隔医療のようなデジタルオプションの認知度の向上とアクセシビリティの成長により、市場は今後数年間安定した成長を示すと予測されます。

- C型肝炎の疾病負担の増加、認知度の向上と診断の進歩、先進的な治療製品の急増といった要因が、市場の成長を促進すると予想されます。例えば、2022年6月の世界保健機関(WHO)の更新によると、推定5,800万人がC型慢性肝炎ウイルスに感染しており、世界全体で毎年約150万人が新たに感染しています。推定320万人の青少年と子供がC型慢性肝炎に感染していました。このように、C型肝炎の負担が大きいため、その治療と早期診断に対する需要が高まり、市場の成長に繋がっています。

- さらに、Current Opinion in Infectious Diseasesが発表した論文によると、2022年7月、C型肝炎ウイルス(HCV)を標的とする直接作用型抗ウイルス薬(DAA)レジメンが幼児向けに承認されました。産後治療プログラムは垂直感染を防ぐが、ケアへのリンク率や治療完了率の低さが障害となっています。これらの課題は、妊娠中のDAA使用によって回避されました。このように、C型肝炎の治療法の進歩に伴い、これらの需要も増加し、市場成長の原動力になると予想されます。

- さらに、米国では2022年5月が、ウイルス性肝炎に関する認識を高め、その影響を認識し、スティグマを減少させるための肝炎啓発月間として制定されました。また、2021年9月、NACCHOは、NASTADとNational Viral Hepatitis Roundtableと提携して、Hepatitis Network for Education and Testing(HepNET)を立ち上げ、薬物を注射する人々(PWID)の満たされていないニーズを特定して対処し、ウイルス性肝炎の教育、予防、検査、ケアへの連携、治療へのアクセスを改善しました。このように、認知度の向上に伴い、C型肝炎の診断と治療に対する需要は増加し、市場の成長を後押しする可能性が高いです。

- このように、上記のすべての要因が予測期間中の市場成長を押し上げると予想されます。しかし、治療費の高騰、社会的スティグマ、未診断例などが市場成長を抑制しています。

C型肝炎市場の動向

抗ウイルス薬セグメントがC型肝炎市場で大きなシェアを占める見込み

- 抗ウイルス薬は、C型肝炎の治療に使用される抗菌薬の一種です。これらの薬剤は通常、HCVウイルスの増殖を阻害することで効果を発揮します。このセグメントの成長は、C型肝炎感染の負担が大きいこと、他の治療法よりも抗ウイルス薬の採用と利点が増加していることに起因しています。

- 例えば、2022年9月にAmerican Association for the Study of Liver Diseasesが発表した論文によると、インドにおけるHCV感染の推定国家有病率は0.32%で、4,420万人のHCV陽性者が世界のHCV負担のかなりの部分を占めています。このように、C型肝炎の負担が大きいことから、抗ウイルス薬の需要が増加し、セグメント別の成長につながると予想されます。

- さらに、2022年6月の世界保健機関(WHO)の更新によると、抗ウイルス薬はC型肝炎感染の95%以上を治癒させる。WHOは、C型慢性肝炎に感染しているすべての成人、青年、3歳までの小児に対し、汎遺伝子型直接作用型抗ウイルス薬(DAA)による治療を推奨しています。2022年、WHOは成人に対する汎遺伝子型治療薬と同じものを用いて青年と小児を治療する新たな推奨を盛り込みましたこのように、他の治療法よりも抗ウイルス療法の採用が増加していることから、このセグメントは今後数年間で成長すると予想されています。

- このように、上記の要因により、抗ウイルス薬の使用量は予測期間中に大きく成長すると予想されます。

北米がC型肝炎市場で大きなシェアを占める見込み

- C型肝炎感染の増加と、同地域で肝炎治療薬が市販されていることから、北米はC型肝炎市場で大きなシェアを占めると予想されます。例えば、米国病院協会が発表した記事によると、2022年8月、米国の成人は毎年200万人以上がC型肝炎ウイルスに感染しています。オピオイドの流行により、感染者は毎年約6万人増加しています。したがって、C型肝炎感染の増加に伴い、その診断と治療に対する需要が増加し、最終的にこの地域の市場成長を押し上げる可能性が高いです。

- さらに、主要市場参入企業の存在、認知度向上プログラムの増加、新薬や検査の採用が、北米地域の市場成長を後押ししています。例えば、2022年2月、Task Force for Global Healthは、世界の臨床症例登録の中で、妊娠中に直接作用型抗ウイルス薬(DAAs)に曝露されたC型肝炎患者の母子ペアの転帰を評価する臨床試験を後援しました。さらに、AbbVie Inc.は2021年10月、米国において、グレカプレビル(GLE)/ピブレンタスビル(PIB)の経口錠による治療を受けるC型肝炎ウイルス(HCV)急性感染症の青年期と成人期の参加者における逆境と疾患活動性の変化を評価する臨床試験を開始しました。このような事例は、同地域の市場成長に有利に働く可能性が高いです。

- このように、上記の要因により、北米は予測期間中に顕著な成長を遂げると予想されます。

C型肝炎産業概要

C型肝炎市場は、世界的と地域的に事業を展開する企業が存在するため、その性質上、適度に集中しています。競合情勢としては、Gilead Sciences, Inc.、AbbVie Inc.、Bristol-Myers Squibb Company、Merck & Co., Inc.、Novartis AGなどが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- C型肝炎の疾病負担の増大

- 認知度の向上と診断の進歩

- 先進治療薬の入手可能性の急増

- 市場抑制要因

- 高額な治療費

- 社会的スティグマと未診断例

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-100万米ドル)

- タイプ別

- 診断

- 肝生検

- 血液検査

- その他の診断

- 治療

- 抗ウイルス薬

- 免疫調節薬

- その他の治療

- 診断

- エンドユーザー別

- 病院とクリニック

- 診断ラボ

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Gilead Sciences, Inc.

- AbbVie Inc.

- Bristol-Myers Squibb Company

- Merck & Co., Inc.

- Novartis AG

- Johnson & Johnson

- GlaxoSmithKline plc

- F. Hoffmann-La Roche Ltd

- Eli Lilly and Company

- Takeda Pharmaceutical Company Limited

- Cipla Inc.

- Daiichi Sankyo Company, Limited

- Astellas Pharma Inc.

第7章 市場機会と今後の動向

目次

Product Code: 50000919

The hepatitis C market is poised to register a CAGR of 12.82% over the forecast period.

Key Highlights

- The COVID-19 pandemic significantly impacted the hepatitis C market and influenced the market growth rate during the pandemic phase. For instance, according to a study published by the Journal of Managed Care & Specialty Pharmacy in June 2022, patients with hepatitis C (HCV) had poorer access to treatment. They were much less likely to complete the treatment course amid the COVID-19 pandemic. The study observed decreased adherence to HCV DAA therapy and laboratory monitoring through the outbreak phase.

- Furthermore, the above study highlighted the telehealth option for patients in a post-COVID-19 environment that could provide an additional advantage in increasing access to care for patients with HCV. Hence, with better access to diagnosis and treatment post-COVID-19, the demand for hepatitis C tests and drugs observed a nominal increase. For instance, according to an article published by Inquiry in May 2023, the COVID-19 pandemic enhanced the use of telehealth to deliver services to those with hepatitis C virus (HCV), human immunodeficiency virus (HIV), and other chronic diseases in need of this type of care.

- Additionally, there was a post-pandemic acceptability of pharmacist-delivered telehealth services among HCV and HIV monoinfected and coinfected patients. Thus, as per the analysis, the impact of COVID-19 was severe in the initial stages of the outbreak; however, with increased awareness and growth in the accessibility of digital options such as telehealth in the post-pandemic era, the market is anticipated to witness stable growth over the coming years.

- Factors such as the growing disease burden of hepatitis C, increasing awareness and advances in diagnosis, and a surge in the availability of advanced therapeutic products are expected to drive market growth. For instance, according to the World Health Organization (WHO) update in June 2022, an estimated 58 million people had chronic hepatitis C virus infection, with about 1.5 million new infections occurring every year globally. An estimated 3.2 million adolescents and children had chronic hepatitis C infection. Thus, with a high burden of hepatitis C, the demand for its treatment and early diagnosis increases, leading to market growth.

- Furthermore, according to an article published by Current Opinion in Infectious Diseases, in July 2022, direct-acting antiviral (DAA) regimens targeting hepatitis C virus (HCV) were approved for young children. Postpartum treatment programs prevent vertical transmission but are hampered by low linkage rates to care and treatment completion. These challenges were avoided by DAA use in pregnancy. Thus, with the advancement in treatment modalities for hepatitis C, the demand for these is also expected to increase, driving market growth.

- Furthermore, May 2022 was observed as Hepatitis Awareness Month to raise awareness about, recognize the impact of, and decrease the stigma associated with viral hepatitis in the United States. Also, in September 2021, NACCHO partnered with NASTAD and the National Viral Hepatitis Roundtable to launch the Hepatitis Network for Education and Testing (HepNET) to identify and address the unmet needs of people who inject drugs (PWID) and improve their access to viral hepatitis education, prevention, testing, linkage to care, and treatment. Thus, with increasing awareness, the demand for hepatitis C diagnosis and treatment will likely increase, boosting market growth.

- Thus, all factors mentioned above are expected to boost market growth over the forecast period. However, the higher cost of treatment, social stigma, and undiagnosed cases are restraining the market growth.

Hepatitis C Market Trends

Antiviral Drugs Segment is Expected to Hold a Major Share in the Hepatitis C Market

- Antiviral drugs are one class of antimicrobials used for treating hepatitis C. These medications usually work by prohibiting the multiplication of the HCV virus. The segment's growth is attributed to the high burden of hepatitis C infection and the growing adoption and advantages of antiviral drugs over other treatment modalities.

- For instance, according to an article published by the American Association for the Study of Liver Diseases in September 2022, the estimated national prevalence rate of HCV infection in India was 0.32%, with 44.2 million HCV-positive individuals making up a significant portion of the worldwide HCV burden. Thus, with the high burden of hepatitis C, the demand for antiviral drugs is expected to increase, leading to segmental growth.

- Furthermore, according to the World Health Organization (WHO) update in June 2022, antiviral medicines cure more than 95% of hepatitis C infections. WHO recommends therapy with pan-genotypic direct-acting antivirals (DAAs) for all adults, adolescents, and children down to 3 years of age with chronic hepatitis C infection. In 2022, WHO included new recommendations for treating adolescents and children using the same pan-genotypic treatments for adults. Thus, with the increased adoption of antiviral therapies over other treatment modalities, the segment is anticipated to grow over the coming years.

- Thus, owing to the factors above, the usage of antiviral drugs is expected to grow significantly during the forecast period.

North America is Expected to Hold a Significant Share in the Hepatitis C Market

- Due to an increase in hepatitis C infections and the commercial availability of hepatitis drugs in the region, North America is expected to hold a significant market share in the hepatitis C market. For instance, according to an article published by the American Hospital Association, in August 2022, over 2 million United States adults have hepatitis C virus infection each year. Infections are increasing by about 60,000 annually due to the opioid epidemic. Thus, with an increase in hepatitis C infection, the demand for its diagnosis and treatment is likely to increase, ultimately boosting the market growth in the region.

- Furthermore, the presence of key market players, growing awareness programs, and the introduction of newer drugs and tests in the region bolster the market's growth in the North American region. For instance, in February 2022, the Task Force for Global Health sponsored a clinical trial to assess the outcomes of hepatitis C-affected mother-infant pairs exposed to direct-acting antivirals (DAAs) during pregnancy within a global clinical case registry. Additionally, in October 2021, AbbVie Inc. initiated a clinical trial in the United States to assess the adversative events and modifications in disease activity in adolescent and adult participants with acute hepatitis C virus (HCV) infection on treatment with oral tablets of Glecaprevir (GLE)/Pibrentasvir (PIB). Such instances are likely to favor the market growth in the region.

- Thus, due to the abovementioned factors, North America is anticipated to witness notable growth over the forecast period.

Hepatitis C Industry Overview

The hepatitis C market is moderately concentrated in nature due to the presence of companies operating globally and regionally. The competitive landscape includes analyzing companies, including Gilead Sciences, Inc., AbbVie Inc., Bristol-Myers Squibb Company, Merck & Co., Inc., and Novartis AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Disease Burden of Hepatitis C

- 4.2.2 Increasing Awareness and Advances in Diagnosis

- 4.2.3 Surge In Availability of Advanced Therapeutic Products

- 4.3 Market Restraints

- 4.3.1 High Cost of Treatment

- 4.3.2 Social Stigma and Undiagnosed Cases

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Diagnosis

- 5.1.1.1 Liver Biopsy

- 5.1.1.2 Blood Tests

- 5.1.1.3 Other Diagnoses

- 5.1.2 Treatment

- 5.1.2.1 Antiviral Drugs

- 5.1.2.2 Immune Modulator Drugs

- 5.1.2.3 Other Treatments

- 5.1.1 Diagnosis

- 5.2 By End-User

- 5.2.1 Hospitals and Clinics

- 5.2.2 Diagnostic Laboratory

- 5.2.3 Other End-Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Gilead Sciences, Inc.

- 6.1.2 AbbVie Inc.

- 6.1.3 Bristol-Myers Squibb Company

- 6.1.4 Merck & Co., Inc.

- 6.1.5 Novartis AG

- 6.1.6 Johnson & Johnson

- 6.1.7 GlaxoSmithKline plc

- 6.1.8 F. Hoffmann-La Roche Ltd

- 6.1.9 Eli Lilly and Company

- 6.1.10 Takeda Pharmaceutical Company Limited

- 6.1.11 Cipla Inc.

- 6.1.12 Daiichi Sankyo Company, Limited

- 6.1.13 Astellas Pharma Inc.