|

市場調査レポート

商品コード

1408268

救急医療サービス製品-市場シェア分析、産業動向・統計、2024~2029年成長予測Emergency Medical Services Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 救急医療サービス製品-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

救急医療サービス製品市場は予測期間でCAGR 6.2%を記録する見込み

主要ハイライト

- COVID-19パンデミックは、パンデミックの初期段階において救急医療サービス(救急医療サービス)製品市場に大きな影響を与えました。例えば、2022年3月にPLOS One Journalが発表した論文によると、COVID-19に関連した呼吸不全の多発により、世界中で機械式人工呼吸器の供給が不足しました。したがって、パンデミック時の人工呼吸器の不足は、COVID-19パンデミックが救急医療サービス製品市場に大きな影響を与えたことを示しています。

- しかし、その頃には、備えの重要性と強固な医療インフラの必要性に対する認識が高まり、市場はペースを取り戻していました。さらに、パンデミック後の緊急対応能力を強化し、適切な医療を提供するために、高度な呼吸補助装置やその他の救急医療製品への需要が持続するとみられます。

- 市場成長を牽引する主要要因としては、慢性疾患や外傷の発生率の上昇、医療技術の進歩、有力企業による製品発売の急増などが挙げられます。

- 交通事故や外傷の増加により、効果的な救急医療と管理のための高度な救急医療サービス製品の利用が必要となり、それによって市場の成長が増大します。例えば、インド道路交通高速道路省(MoRTH)が2022年12月に発表した報告書によると、インドでは2021年に約41万2,432件の交通事故が報告され、384,448人が負傷しました。したがって、インドでは交通事故の頻度が高いため、迅速かつ効果的な緊急対応に必要な外傷キット、医療用品、専門機器などの救急医療サービス製品の需要が高まると予測されます。

- さらに、各国における救急部(ED)の受診者数の増加も、予測期間中に生命維持・救急蘇生患者対応システムの需要を押し上げると予測されています。例えば、オーストラリア保健福祉研究所が2022年10月に発表したデータによると、2021年から2022年にかけてオーストラリアの公立病院では約879万人がEDを訪れました。同じ情報源によると、2021~2022年におけるオーストラリアのED受診者数は人口1,000人当たり約339人でした。

- さらに、著名な参入企業は、高度な救急医療サービス製品を市場に投入するために、さまざまな戦略的提携やパートナーシップを結んでいます。例えば、2022年8月、英国を拠点とする車椅子メーカーRGKと北米Sunrise Medicalは、RGKの新しいウィンドウOctane Sub4、硬質チタン製車椅子を発売するために協力しました。

- したがって、交通事故件数の増加、各国におけるED受診件数の増加、先進的な救急医療サービス製品を発売するための有力企業間の提携件数の急増が、予測期間中の市場成長を促進すると予測されます。しかし、救急医療サービス製品の高コストと厳しい規制要件が、予測期間中の市場成長を抑制すると予測されています。

救急医療製品の市場動向

人工呼吸器セグメントは予測期間中に大幅な成長が見込まれる

- 人工呼吸器は、救急医療部門において、重篤な状態の患者に救命のための生命維持を提供することで重要な役割を果たしています。同分野の成長を促進する主要要因としては、急性呼吸窮迫症候群(ARDS)、慢性閉塞性肺疾患(COPD)、肺炎などの重篤な呼吸器疾患の増加、政府のイニシアティブや投資の急増、有力企業による製品発売の増加などが挙げられます。例えば、2021年4月に英国政府が発表したデータによると、2021年にはイングランドで約115万2,272人がCOPDを患っています。したがって、COPDを患う人の増加は、予測期間中に人工呼吸器の需要を加速させると予測されています。

- さらに、世界的に医療インフラを改善するための政府資金が増加していることも市場成長に寄与しています。例えば、2022年3月、オーストラリア政府は2022~2023年に1,320億米ドルを投資し、2025-26年には約1,400億米ドルを投資する見込みであり、2021~2022年予算と比較して、メディケア資金73億米ドル増、病院資金98億米ドル増、高齢者医療資金101億米ドル増など、今後4年間で総額5,370億米ドルのコミットメントが見込まれています。このようなイニシアチブは、高度な救急医療サービス製品の生産を促進し、市場成長を促進すると予想されます。

- さらに、有力企業の製品開拓の増加も市場成長を高めています。例えば、2023年1月、Getinge ABは、小児と成人患者に肺保護治療ツールを提供する新しいServo-c機械式人工呼吸器を発売しました。

- したがって、COPDの高い有病率、政府資金の増加、製品開発の急増により、このセグメントは予測期間中に大きく成長すると予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

- 北米は、救急外来(ED)受診者数の増加、高い医療支出、同地域における様々な有力企業の存在により、予測期間中に大きな市場シェアを占めると予想されます。

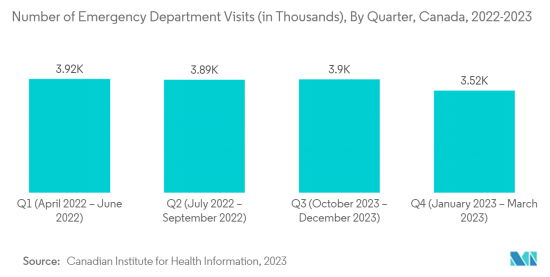

- 同地域では、様々な緊急事態による救急外来受診件数の増加が、予測期間中の救急医療サービス製品に対する需要を促進すると予測されています。例えば、カナダ健康情報研究所が2023年2月に発表したデータによると、2021~2022年の間にカナダで報告されたED訪問の総数は、前年の1,170万件から約1,400万件に増加しました。

- さらに、同地域における死亡事故件数の急増もED受診件数の増加につながり、市場成長を牽引しています。例えば、米国労働統計局が2022年12月に発表したデータによると、米国における死亡労働災害は前年の4,764件に対し、2021年には5,190件に達しました。従って、このような統計は、同国におけるED受診件数の増加を示しており、地域市場の成長を急成長させています。

- さらに、この地域の有力参入企業の存在と先進的な救急医療サービス製品の発売への積極的な参加も市場成長を高めています。例えば、2022年5月、Invacare Corporationは米国でBirdie Evo XPLUSリフトを発売しました。

- したがって、北米の救急医療サービス市場は、ED受診者数の急増、致命的な労働災害の発生率の増加、製品発売数の増加により、大きく成長すると予想されます。

救急医療サービス製品産業概要

救急医療製品市場は、救急医療サービス製品を製造・販売する企業の数が限られているため、競争は緩やかです。Bound Tree Medical、McKesson Corporation、Stryker Corporation、ICU Medical, Inc. (Smith Medical)、Cardinal Healthなど、市場参入企業は製品の発売、提携、買収に積極的に取り組み、その地位を維持しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患と傷害の発生率の増加

- 医療技術の進歩

- 市場抑制要因

- 救急医療サービス製品の高コストと厳しい規制要件

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- タイプ別

- 生命維持・救急蘇生

- 除細動器

- 人工呼吸器

- 喉頭鏡

- その他の生命維持・救急蘇生

- 患者モニタリングシステム

- 創傷ケア用品

- ドレッシング材と包帯

- 縫合糸・ステープル

- その他の創傷治療消耗品

- 患者ハンドリング機器

- 医療用ベッド

- 車椅子・スクーター

- その他の機器

- 感染管理用品

- 消毒剤・洗浄剤

- 個人用保護具

- その他感染管理用品

- その他の救急医療サービス製品

- 生命維持・救急蘇生

- エンドユーザー別

- 病院と外傷センター

- 外来手術センター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Bound Tree Medical

- McKesson Corporation

- Medline Industries, Inc.

- Stryker Corporation

- ICU Medical, Inc.(Smith Medical)

- Cardinal Health

- Becton, Dickinson and Company

- GE Healthcare

- Medtronic

- 3M

- B. Braun SE

第7章 市場機会と今後の動向

The emergency medical services products market is expected to register a CAGR of 6.2% over the forecast period.

Key Highlights

- The COVID-19 pandemic significantly impacted the emergency medical services (EMS) products market during the early phase of the pandemic. For instance, as per the article published by the PLOS One Journal in March 2022, the high incidence of COVID-19-related respiratory failure led to shortages in the supply of mechanical ventilators worldwide. Therefore, the shortages of ventilators during the pandemic showed the significant impact of the COVID-19 pandemic on the emergency medical services products market.

- However, by that time, the market had picked up its pace due to the increased awareness of the importance of preparedness and the need for robust medical infrastructure. Additionally, the market will likely experience sustained demand for advanced respiratory support devices and other emergency medical products to enhance emergency response capabilities and ensure adequate healthcare delivery during the post-pandemic period.

- The major factors driving the market growth include the rising incidence of chronic diseases and injuries, advancements in medical technology, and a surging number of product launches by prominent players.

- The rise in road accidents and trauma cases necessitates the availability of advanced EMS products for effective emergency care and management, thereby augmenting market growth. For instance, as per the report published by the Ministry of Road Transport and Highways of India (MoRTH) in December 2022, approximately 412,432 road accidents were reported in India in 2021, with injuries to 384,448 persons. Hence, the high frequency of road accidents in India is projected to drive the demand for emergency medical services products such as trauma kits, medical supplies, and specialized equipment needed for prompt and effective emergency response.

- In addition, the rising number of Emergency Department (ED) visits in various countries is also projected to drive the demand for life support & emergency resuscitation patient handling systems during the forecast period. For instance, according to the data published by the Australian Institute of Health and Welfare in October 2022, there were around 8.79 million visits to EDs in Australian public hospitals during 2021-2022. The same source mentioned that the ED visits in Australia were approximately 339 visits per 1,000 population during 2021-2022.

- Moreover, the prominent players are doing various strategic collaborations or partnerships to bring advanced emergency medical services products to the market. For instance, in August 2022, United Kingdom-based wheelchair manufacturer RGK and Sunrise Medical North America collaborated to launch RGK's new window Octane Sub4, a rigid titanium wheelchair.

- Therefore, the rising number of road accidents, increase in ED visits in various countries, and spur in the number of collaborations amongst prominent players to launch advanced EMS products are projected to drive market growth during the forecast period. However, the high cost of EMS products and stringent regulatory requirements are projected to restrain market growth during the forecast period.

Emergency Medical Services Products Market Trends

Ventilators Segment is Expected to Show Significant Growth Over the Forecast Period

- Ventilators play a vital role in emergency medical departments by providing life-saving life support to patients in critical conditions. The major factors driving the segment growth include the increase in critical respiratory conditions such as acute respiratory distress syndrome (ARDS), chronic obstructive pulmonary disease (COPD), pneumonia, surging government initiatives and investments, and a rising number of product launches by prominent players. For instance, as per the data released by the Government of the UK in April 2021, approximately 1,152,272 people were suffering from COPD in England in 2021. Hence, the rising number of people suffering from COPD is projected to accelerate the demand for ventilators during the forecast period.

- Furthermore, the rising government funding to improve healthcare infrastructure worldwide contributes to market growth. For instance, in March 2022, the Australian government invested USD 132 billion in 2022-2023 and is expected to invest about USD 140 billion in 2025-26, with a total commitment of USD 537 billion over the next four years, including USD 7.3 billion increase in Medicare funding, USD 9.8 billion increase in Hospital funding and USD 10.1 billion increase in Aged Care funding as compared to 2021-2022 budget. Such initiatives are anticipated to fuel the production of advanced EMS products, propelling the market growth.

- Moreover, prominent players' rising number of product developments is also increasing the market growth. For instance, in January 2023, Getinge AB launched its new Servo-c mechanical ventilator that offers lung-protective therapeutic tools for pediatric and adult patients.

- Therefore, due to the high prevalence of COPD, rising government funding, and surging number of product developments, the segment is expected to grow significantly during the forecast period.

North America is Expected to Hold the Significant Share of the Market Over the Forecast Period

- North America is expected to hold a significant market share over the forecast period due to the increasing number of emergency department (ED) visits, high healthcare expenditure, and the presence of various prominent players in the region.

- The rising number of ED visits in the region due to various emergency situations is projected to drive the demand for EMS products during the forecast period. For instance, as per the data published by the Canadian Institute for Health Information in February 2023, the total number of reported ED visits rose to around 14.0 million in Canada during 2021-2022, compared to 11.7 million in the previous year.

- Furthermore, the surge in the number of fatal injuries in the region also led to an increase in ED visits, thereby driving the market growth. For instance, according to the data released by the United States Bureau of Labor Statistics in December 2022, fatal work injuries in the United States reached 5,190 in 2021 compared to 4,764 in the previous year. Thus, such statistics indicate the increasing number of ED visits in the country, which is burgeoning the regional market growth.

- Furthermore, the presence of prominent players in the region and their active participation in launching advanced EMS products is also increasing the market growth. For instance, in May 2022, Invacare Corporation launched the Birdie Evo XPLUS lift in the United States.

- Therefore, the North American EMS market is expected to grow significantly due to the spur in the number of ED visits, increase in the incidence of fatal work injuries, and rising number of product launches.

Emergency Medical Services Products Industry Overview

The Emergency Medical Services Products market is moderately competitive due to a limited number of companies that manufacture and distribute EMS products. The market players are actively involved in product launches, collaborations, and acquisitions to uphold their position, including Bound Tree Medical, McKesson Corporation, Stryker Corporation, ICU Medical, Inc. (Smith Medical), and Cardinal Health, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Chronic Diseases and Injuries

- 4.2.2 Advancements in Medical Technology

- 4.3 Market Restraints

- 4.3.1 High Cost of EMS Products and Stringent Regulatory Requirements

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value-USD)

- 5.1 By Type

- 5.1.1 Life Support & Emergency Resuscitation

- 5.1.1.1 Defibrillators

- 5.1.1.2 Ventilators

- 5.1.1.3 Laryngoscopes

- 5.1.1.4 Other Life Support & Emergency Resuscitations

- 5.1.2 Patient Monitoring Systems

- 5.1.3 Wound Care Consumables

- 5.1.3.1 Dressings & Bandages

- 5.1.3.2 Sutures & Staples

- 5.1.3.3 Other Wound Care Consumables

- 5.1.4 Patient Handling Equipment

- 5.1.4.1 Medical Beds

- 5.1.4.2 Wheelchairs & Scooters

- 5.1.4.3 Other Equipment

- 5.1.5 Infection Control Supplies

- 5.1.5.1 Disinfectant & Cleaning Agents

- 5.1.5.2 Personal Protection Equipment

- 5.1.5.3 Other Infection Control Supplies

- 5.1.6 Other EMS Products

- 5.1.1 Life Support & Emergency Resuscitation

- 5.2 By End-User

- 5.2.1 Hospitals & Trauma Centers

- 5.2.2 Ambulatory Surgical Centers

- 5.2.3 Other End-Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bound Tree Medical

- 6.1.2 McKesson Corporation

- 6.1.3 Medline Industries, Inc.

- 6.1.4 Stryker Corporation

- 6.1.5 ICU Medical, Inc. (Smith Medical)

- 6.1.6 Cardinal Health

- 6.1.7 Becton, Dickinson and Company

- 6.1.8 GE Healthcare

- 6.1.9 Medtronic

- 6.1.10 3M

- 6.1.11 B. Braun SE