|

市場調査レポート

商品コード

1408266

抗ヒスタミン薬:市場シェア分析、産業動向と統計、2024~2029年の成長予測Antihistamine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 抗ヒスタミン薬:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

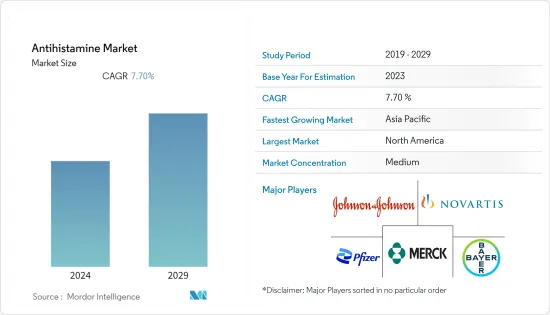

抗ヒスタミン薬市場は予測期間中にCAGR 7.7%を記録すると予想されています。

COVID-19は抗ヒスタミン薬市場に大きな影響を与えています。多くの臨床試験や試験管内試験で、肺の症状を緩和することによってCOVID-19の管理にいくつかの抗ヒスタミン薬が有望であることが示されているからです。例えば、2023年2月にHealth Science Reports誌に掲載された研究によると、COVID-19に特異的な抗ヒスタミン薬を特定し、他の手法とともにCOVID-19のケアプランに基本的な治療法として加える必要があります。抗ヒスタミン薬はCOVID-19の治療に効果的であると同時に、症状を速やかに除去し、身体の防御機構をリセットするのに十分な時間を与え、結果として早期回復をもたらすようです。パンデミック初期には、サプライチェーンの制限や製造の停止により、市場は若干の落ち込みを見せた。しかし、パンデミック後期には、COVID-19の治療プロトコールに抗ヒスタミン薬が含まれるようになったため、市場は大きな伸びを示しました。さらに、市場はパンデミック後に有利な成長を遂げ、予測期間中も同様の動向を示すと予測されています。

市場の成長を促進する要因としては、アレルギーや胃障害の増加、新規剤形開発のための研究開発活動の活発化などが挙げられます。

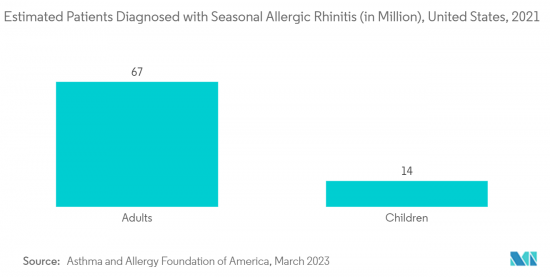

アレルギーや胃酸過多の問題の高まりは、予測期間中の市場成長の原動力になると予想されます。例えば、Asthma and Allergy Foundation 2023によると、2021年の米国では約8,100万人が季節性アレルギー性鼻炎(花粉症)と診断され、その中には成人の約26%(6,700万人)と小児の約19%(1,400万人)が含まれています。また、2022年9月にRawal Medical Journalに掲載された研究によると、胃食道反射疾患(GERD)の有病率は、北米で18.1~27.8%、欧州で8.8~25.9%、東アジアで2.5~7.8%、中東で8.7~33.1%、オーストラリアで11.6%、南米で23%でした。したがって、このようなアレルギーと胃障害の膨大な有病率は、抗ヒスタミン薬の需要を増加させ、市場の成長を促進すると予想されます。

さらに、抗ヒスタミン薬の新規剤形の開発における進歩の高まりや、国際的な規制機関からの承認が、予測期間中の市場成長を後押しすると予想されます。例えば、2021年6月、米国食品医薬品局は、季節性と通年性アレルギー性鼻炎のための部分処方から非処方への移行として知られる手順を通じて、Bayerによって開発された点鼻抗ヒスタミン薬(アゼラスチンHCI .15%)を承認しました。そのため、抗ヒスタミン薬が非処方薬として承認されれば、人々の間で採用が進み、市場成長の原動力になると予想されます。

さらに、抗ヒスタミン薬の価格統制と償還は、市場の成長をさらに促進すると予想されます。例えば、日本では2021年11月にTaiho PharmaceuticalとMeiji Seika Pharmaの経口抗アレルギー薬「ビラノアOD錠20mg」(一般名:ビラスチン)が薬価収載されました。薬価収載により、抗ヒスタミン薬の薬価が引き下げられ、市場拡大が期待されます。

したがって、アレルギーや胃障害の問題の高まり、有利な償還政策、規制機関からの承認の高まりは、市場成長を促進すると予想される要因です。しかし、ブランド薬の特許切れ、ジェネリック医薬品のイントロダクション、抗ヒスタミン薬に関連する副作用が市場成長を阻害しています。

抗ヒスタミン薬市場の動向

アレルギー性疾患が市場調査において大きなシェアを占めると予測

アレルギー性疾患における抗ヒスタミン薬の採用が増加していることから、アレルギー性疾患分野が市場で大きなシェアを占めると予測されています。アレルギー体質の人は、花粉、ペットの毛、家庭のほこりなどのアレルゲンを脅威と解釈し、ヒスタミンを放出します。ヒスタミンは、かゆみ、涙目、鼻水や鼻づまり、くしゃみ、皮膚の発疹として現れるアレルギー反応を引き起こします。

アレルギー性抗ヒスタミン剤の発売など、主要市場参入企業のイニシアティブの高まりが、このセグメントの成長を促進すると予想されます。例えば、2021年2月、ボシュロムは米国でAlaway Preservative Free(ケトチフェンフマル酸塩点眼液0.035%)抗ヒスタミン点眼薬を発売しました。これは、米国食品医薬品局が承認した防腐剤フリーの一般用抗ヒスタミン点眼薬です。したがって、アレルギー用のOTC抗ヒスタミン薬の発売は、このセグメントの成長を促進する採用の増加につながります。

さらに、アレルギーの治療における抗ヒスタミン薬の有効性は、セグメントの成長をさらに促進すると予想されます。例えば、2023年6月にBrazilian Journal of Otorhinolaryngologyに掲載された研究によると、経口H1抗ヒスタミン薬はアレルギー性鼻炎患者の第一選択薬であり、抗ヒスタミン薬であるルパタジンはアレルギー性鼻炎患者の症状緩和に最も効果的です。したがって、アレルギーの治療における抗ヒスタミン薬の重要性は、調査対象セグメントの需要を高め、それによって成長を促進します。

したがって、主要市場参入企業のイニシアチブの高まりと、アレルギー治療における抗ヒスタミン薬の重要性の高さが、このセグメントで有利な成長を示すと予想される要因です。

予測期間中、北米が市場で大きなシェアを占める見込み

北米は、アレルギーの罹患率の上昇、主要市場参入企業の強固な足場、医療インフラの改善、医療政策、アレルギー疾患の研究開発に対する政府からの資金提供などにより、市場調査において大きなシェアを占めると予測されます。

アレルギーの有病率の上昇は、同地域における抗ヒスタミン薬市場の成長を促進すると予測されています。例えば、2023年1月の米国疾病予防管理センター(CDC)によると、2021年には個人の6.2%が食物アレルギー、7.3%が湿疹、成人の25.7%が季節性アレルギーを持っています。さらに、2021年8月のカナダ政府によると、ケベック州では成人の17%がアレルギー性鼻炎に罹患しています。同地域におけるこのような膨大なアレルギー有病率は、アレルギー治療のための抗ヒスタミン剤の需要を増加させ、市場成長を促進すると予想されます。

さらに、主要市場参入企業のイニシアチブの高まりと、この地域の各国政府による抗ヒスタミン薬の承認が、市場成長を後押しすると予想されます。例えば、2022年9月、カナダ保健省は、中等度から重度の季節性アレルギー性鼻炎(SAR)の対症療法として、Glenmark Pharmaceuticalsの子会社であるGlenmark Specialtyが製造するリヤルトリス(オロパタジン塩酸塩とモメタゾンフロエート点鼻薬)を承認しました。

さらに、アレルギー治療薬の研究開発に対する多額の資金援助が市場の成長を促進すると予想されています。例えば、米国国立衛生研究所(National Institute of Health)は、アレルギー性鼻炎(花粉症)に600万米ドル、食物アレルギーに7,700万米ドルの薬物療法開発資金を提供しています。これにより、抗ヒスタミン薬の研究開発と承認が増加し、予測期間中の市場成長が促進されると予想されます。

したがって、アレルギー症状の増加、主要市場参入企業のイニシアティブの高まりなどの上記の要因は、この地域で調査された市場の成長を促進すると予想されます。

抗ヒスタミン剤産業概要

抗ヒスタミン薬市場は適度な競争状態にあり、大手企業が世界市場で大きなシェアを占めています。競合要因としては、市場参入企業による発売や提携などのイニシアチブの高まり、抗ヒスタミン薬の認可の高まりなどが挙げられます。市場に参入している企業には、Johnson and Johnson、Novartis AG、Pfizer Inc.、Merck and Co.、Bayer AG、GlaxoSmithKline、Almirall、Akornなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- アレルギーと胃障害の問題の増加

- 新規剤形開発につながる研究開発活動の増加

- 市場抑制要因

- 特許切れとジェネリック医薬品のイントロダクション

- 抗ヒスタミン薬に伴う副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-100万米ドル)

- 薬剤クラス別

- H1抗ヒスタミン薬

- 第一世代

- 第二世代

- H2抗ヒスタミン薬

- H3抗ヒスタミン薬

- H1抗ヒスタミン薬

- 剤形別

- 経口剤

- 非経口剤

- その他

- タイプ別

- 市販薬

- 処方薬

- 疾患別

- アレルギー性疾患

- 胃腸障害

- 中枢神経系疾患

- その他

- 流通別

- 病院薬局

- 小売薬局

- オンライン薬局

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Bayer

- Almirall

- GlaxoSmithKline

- AstraZeneca

- Johnson and Johnson

- Novartis

- Sanofi

- Pfizer

- Sun Pharmaceutical Industries Limited

- Akorn

- Merck and Co.

- Teva Pharmaceutical

第7章 市場機会と今後の動向

The antihistamine market is expected to register a CAGR of 7.7% over the forecast period.

COVID-19 has significantly impacted the antihistamines market as many clinical trials and in vitro, studies have shown several antihistamines to be promising in the management of Covid19 by easing pulmonary symptoms. For instance, according to a study published in Health Science Reports in February 2023, antihistamines specific to Covid-19 have to be identified and added as a fundamental treatment method to the care plan for Covid-19, along with other techniques. They appear to be effective in treating Covid-19 while removing symptoms quickly and giving the body enough time to reset its defense mechanisms, resulting in a speedy recovery. The market has seen a slight decline during the early pandemic, due to supply chain restrictions and manufacturing halts. However, during the late pandemic, the market has attained a significant pace due to the inclusion of antihistamines in COVID-19 treatment protocols. Furthermore, the market has seen lucrative growth post-pandemic and is anticipated to show the same trend over the forecast period.

The factors driving the market growth include rising issues of allergies and stomach disorders, rising in the research and development activities for the development of novel dosage forms.

The rising issues of allergies and acid reflex are anticipated to drive the growth of the market studied over the forecast period. For instance, according to the Asthma and Allergy Foundation 2023, approximately 81 million people in the United States in 2021 were diagnosed with seasonal allergic rhinitis (hay fever) including around 26% (67 million) of adults and 19% (14 million) of children. In addition, according to the study published in Rawal Medical Journal in September 2022, the prevalence of gastroesophageal reflex disease (GERD) was found to be 18.1 to 27.8% in NorthAmerica, 8.8 to 25.9% in Europe, 2.5 to 7.8% in East Asia, 8.7 to 33.1% in MiddleEast, 11.6% in Australia and 23% in South-America. Therefore, such a huge prevalence of allergies and stomach disorders is anticipated to increase the demand for antihistamines, driving the market growth.

Furthermore, rising advancements in development of novel dosage forms of antihistamine medications and approvals from the international regulatory agencies are anticipated to bolster the market growth over the forecast period. For instance, in June 2021, The United States Food and Drug Administration approved a nasal antihistamine (Azelastine HCI .15%) developed by Bayer through a procedure known as a partial prescription to nonprescription transition for seasonal and perennial allergic rhinitis. Therefore, the approvals of antihistamines as a nonprescription medication is anticipated to increase the adoption among people, driving the market growth.

Moreover, the price control and reimbursement of antihistamine drugs are anticipated to propel the market growth further. For intance, in November 2021, Taiho Pharmaceutical Co., Ltd. and Meiji Seika Pharma Co., Ltd's Bilanoa OD Tablets 20 mg (generic name: bilastine), an oral anti-allergy drug, in Japan has been listed on National Health Insurance reimbursement price list. The listing of drugs on reimbursement price list is anticipated to rise the adoption due to reduction in prices of antihistamine drugs, thereby driving the market growth.

Therefore, the rising issues of allergies and stomach disorders, favourable reimbursement policies and rising approvals from regulatory agencies are the factors anticipated to drive the market growth. However, the patent expiry of branded drugs, introduction of generic drugs and adverse affects associated with antihistamine drugs are impeding the market growth.

Antihistamine Market Trends

Allergic Disorders in Anticipated to Hold a Significant Share in the Market Studied

The allergic disorders segment is anticipated to hold a significant share of the market due to the rising adoption of antihistaminics in allergic conditions. In people with allergies, the body interprets allergens such as pollen, pet hair, or household dust as a threat and releases histamine. Histamine triggers an allergic reaction that manifests as itchy, watery eyes, runny or stuffy nose, sneezing, and skin rashes.

The rising initiatives from the key market players such as the launch of allergic antihistamine products are anticipated to drive the segment growth. For instance, in February 2021, Bausch + Lomb launched Alaway Preservative Free (ketotifen fumarate ophthalmic solution 0.035%) antihistamine eye drops in the United States. It is the over-the-counter (OTC) preservative-free antihistamine eye itch relief drop approved by the United States Food and Drug Administration. Therefore, the launch of OTC antihistamine drugs for allergies will lead to increase adoption driving the segment growth.

Furthermore, the efficacy of antihistamines in the treatment of allergies is anticipated to drive the segment growth further. For instance, according to the study published in the Brazilian Journal of Otorhinolaryngology in June 2023, oral H1 antihistamines are the first-line therapy for patients with allergic rhinitis, and rupatadine, an antihistamine is the most effective in alleviating symptoms of patients with allergic rhinitis. Therefore, the importance of antihistamine drugs in treating allergies will raise the demand for the segment studied, thereby propelling its growth.

Therefore, the rising initiatives from the key market players along with the high importance of antihistaminic drugs in treating allergies are the factors anticipated to show lucrative growth in this segment.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is anticipated to hold a significant share of the market studied due to the rising incidence of allergies, the strong foothold of key market players, improved healthcare infrastructure, medicare policies, and funding from the government on research and development of allergic disorders, among others.

The rising prevalence of allergies is anticipated to drive the growth of the antihistamine market in the region. For instance, according to the Centers for Disease Control and Prevention (CDC) in January 2023, in the United States, 6.2% of individuals had food allergies, 7.3% had eczema, and 25.7% of adults had seasonal allergies in 2021. Furthermore, according to the Government of Canada in August 2021, allergic rhinitis affects 17% of adults in Quebec. Such a huge prevalence of allergies in the region is anticipated to increase the demand for antihistamines for the treatment of allergies, driving market growth.

In addition, the rising initiatives from the key market players and approvals of antihistamine medications by the national governments in the region are anticipated to boost market growth. For instance, in September 2022, Health Canada approved Ryaltris (olopatadine hydrochloride and mometasone furoate nasal spray) manufactured by Glenmark Pharmaceuticals subsidiary Glenmark Specialty's as a symptomatic therapy for moderate to severe seasonal allergic rhinitis (SAR).

Furthermore, the high funding for the research and development of allergic therapies is anticipated to propel the market growth. For instance, the National Institute of Health of United States has granted a funding of USD 6 million for allergic rhinitis (Hay Fever) and USD 77 million for food allergies for the development of drug therapies. This will lead to increased research and development and approvals of antihistamines, thereby anticipated to drive the market growth over the forecast period.

Therefore, the above factors such as rising allergic condition, rising initiatives from the key market players, among others are anticipated to drive the growth of the market studied in the region.

Antihistamine Industry Overview

The antihistamine market is moderately competitive, with major players holding a significant share in the global market. The factors owing to the competition include the rising initiatives from the market players, such as launches and partnerships, and rising approvals of antihistamines, among others. Some of the players operating in the market include Johnson and Johnson, Novartis AG, Pfizer Inc., Merck and Co., Bayer AG, GlaxoSmithKline, Almirall, and Akorn.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Issues of Allergies and Stomach Disorders

- 4.2.2 Increase in R&D Activities Leading to Development of Novel Dosage Forms

- 4.3 Market Restraints

- 4.3.1 Patent Expiry and Introduction of Generic Drugs

- 4.3.2 Adverse Effects Associated with Antihistamine Drugs

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Drug Class

- 5.1.1 H1 Antihistamanics

- 5.1.1.1 First Generation

- 5.1.1.2 Second Generation

- 5.1.2 H2 Anti histamanics

- 5.1.3 H3 Anti histamanics

- 5.1.1 H1 Antihistamanics

- 5.2 By Dosage Form

- 5.2.1 Oral route

- 5.2.2 Parenteral

- 5.2.3 Others

- 5.3 By Type

- 5.3.1 OTC

- 5.3.2 Prescription-Based

- 5.4 By Disease

- 5.4.1 Allergic Disorders

- 5.4.2 Stomach Disorders

- 5.4.3 Central Nervous System Disorders

- 5.4.4 Others

- 5.5 By Distribution

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bayer

- 6.1.2 Almirall

- 6.1.3 GlaxoSmithKline

- 6.1.4 AstraZeneca

- 6.1.5 Johnson and Johnson

- 6.1.6 Novartis

- 6.1.7 Sanofi

- 6.1.8 Pfizer

- 6.1.9 Sun Pharmaceutical Industries Limited

- 6.1.10 Akorn

- 6.1.11 Merck and Co.

- 6.1.12 Teva Pharmaceutical