|

市場調査レポート

商品コード

1408254

ヘルスケアコンプライアンスソフトウェア:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Healthcare Compliance Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヘルスケアコンプライアンスソフトウェア:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

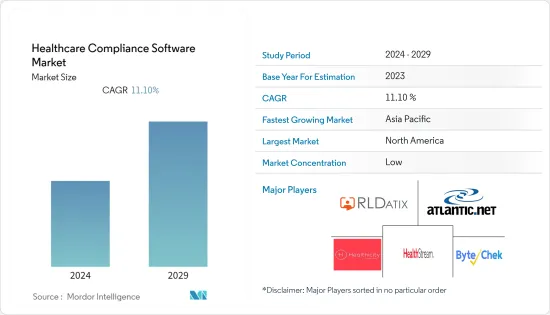

ヘルスケアコンプライアンスソフトウェア市場は、予測期間中にCAGR 11.1%という大幅な成長が見込まれています。

COVID-19パンデミックは、ヘルスケアコンプライアンスソフトウェア市場に大きな影響を与えました。多くの医療機関や病院では、社会的距離や遠隔地勤務のために、ヘルスケアコンプライアンスソフトウェアの採用が急増しました。また、パンデミックは医療のガイドラインや規制の更新や変更にもつながった。さらに、パンデミック中は物理的な交流が制限され、現地での監査や検査は困難でした。そのため、多くの組織が遠隔監査を取り入れました。例えば、イタリアの認定機関Accrediaは、緊急事態に対応するため、2020年3月7日付のテクニカルサーキュラーDC N 06/2020を発行し、その後2020年3月19日付のテクニカルサーキュラーDC N 08/2020で補足することで、遠隔審査を迅速に実施しました。このように、コンプライアンスソフトウェアは遠隔監査を容易にし、医療組織が常に情報を入手し、業務を見直すことを支援しました。したがって、COVID-19の流行が市場の成長を後押ししています。

手作業によるヘルスケアコンプライアンス手法から自動化されたコンプライアンスソフトウェアへの移行、医療データ量の増加は、ヘルスケアコンプライアンス市場の成長を促進する主要要因です。例えば、International Data Corporation(IDC)が更新したレポートによると、2018年には33ゼタバイトであったのに対し、医療業界では2025年まで世界中で約175ゼタバイトのデータが生成される見込みです。これは、バイオバンクの収集、公的・商業的医療提供者による電子カルテ、医療機器の製造、ソーシャルメディア・プラットフォームの運営、データ・プラットフォームの構築など、医療業界におけるデータ集積プロジェクトが後押ししています。従って、このような要因は、予測期間中にヘルスケアコンプライアンスソフトウェア市場の需要を増加させる可能性が高いです。

しかし、データ収集、分析、報告、スタッフのトレーニングなど、コンプライアンス・モニタリング・プロセスの多くの側面を自動化する技術の採用が拡大していることも、市場成長に大きく寄与しています。技術はコンプライアンス・モニタリングの精度と効率を高め、人為的ミスのリスクを低減します。また、組織が大量のデータを分析することで、コンプライアンス違反の領域を特定し、是正措置を講じるのにも役立ちます。以上のような要因から、ヘルスケアコンプライアンスソフトウェア市場は調査期間中に拡大すると予想されます。

しかし、専門クリニックの認識不足やITリソースの制限、導入コストの高さなどが、予測期間中の市場成長の妨げになると考えられます。

ヘルスケアコンプライアンスソフトウェア市場の動向

予測期間中、クラウドベースのセグメントが市場で大きなシェアを占める

クラウドベースのセグメントは、予測期間中にヘルスケアコンプライアンスソフトウェア市場で大きな成長を遂げると予測されます。同分野の成長に寄与している主要要因は、費用対効果やサブスクリプションベースの価格モデル、セキュリティと拡大性の向上です。また、政府による支援も市場の成長に寄与しています。例えば、米国の医療保険の相互運用性と説明責任に関する法律(HIPAA)、欧州の一般データ保護規則(GDPR)、業界標準のCSF HITRUST Allianceはいずれも、オンラインサービスにおける顧客の個人情報の保護を促進し、規制しています。SaaSソリューションやパブリッククラウドソフトウェアは、迅速な導入、ワークロードやアプリケーションの拡大性、手頃な価格設定により、オンプレミスのデータセンターの専門家やサーバーに依存することなく、HIPAAセキュリティプログラムを構築し、インフラを管理するためにますます使用されるようになっています。そのため、病院や医療組織によるクラウドベースのソフトウェアの採用は、同分野の成長を強化すると思われます。

さらに、このセグメントにおける新製品の発売は、市場の成長をさらに促進すると思われます。例えば、CenTrakは2023年1月、ワークフローとコミュニケーションを自動化し、臨床治療の各段階で不可欠な手作業による事務処理の負荷を軽減する、スケーラブルなクラウドベースのプラットフォーム、WorkflowRTの発売を発表しました。WorkflowRTは、ワークフローとコミュニケーションを自動化し、各診療段階で不可欠な手作業による事務処理の負担を軽減する、拡大性のあるクラウドベースのプラットフォームです。医療機関は、プロセス改善をサポートするために過去の測定値を活用することで、患者の待ち時間の減少、患者とのケア時間の増加、患者とスタッフの満足度の向上を示しています。このように、上記の要因は予測期間中の同分野の成長を促進すると予想されます。

北米がヘルスケアコンプライアンスソフトウェア市場で最大の市場シェアを占める

予測期間中、北米がヘルスケアコンプライアンスソフトウェア市場を独占すると予想されます。同地域の他の国々の中では、米国がサイバー攻撃やデータ漏えいのインシデントの増加、クラウドベースのソリューションの採用の増加、技術主導型ソリューションの採用の増加、デジタル化により市場をリードしています。

データ漏洩やサイバー攻撃の増加が市場成長に寄与しています。例えば、米国政府の公民権局(OCR)の報告によると、医療組織は2023年第1四半期に145件のデータ漏洩を報告しました。しかし、2022年には707件のデータ漏えいが報告され、5,190万件の記録が盗まれました。2022年に最も多かった医療データ漏えいの形態は、ハッキングとITインシデント(555件)、不正アクセスまたは開示(113件)、物理的盗難(35件)、不適切な記録廃棄(4件)でした。また、過去5年間にOCRは6,565万8,440米ドルのHIPAA制裁金を課しました。この中には2022年の217万140米ドルが含まれ、オクラホマ州立大学の保健サービスセンターが受けた罰金額が最も大きく、同センターはハッカーにサーバーに侵入された後、87万5,000米ドルを支払わなければならなかった。このようなサイバー攻撃やデータ漏洩の事例は、ヘルスケアコンプライアンスソフトウェアの需要を促進し、ひいては市場の成長を押し上げると予想されます。

さらに、医療におけるデジタルトランスフォーメーションやクラウドベースのソリューションの採用が拡大していることも、市場成長に寄与しています。例えば、2023年の記事では、DevOps自動化とコンプライアンス分野のパイオニアであるDuplo Cloudが、医療業界におけるクラウドコンピューティングソフトウェアの採用を理解するためにIT専門家を対象に調査を実施し、発表した調査結果を報告しています。それによると、クラウドインフラの採用率が最も高かったのは病院とメディケア/メディケイド機関で、それぞれ91%と90%でした。最も導入率が低かったのは歯科医院(23%)と医院(37%)でした。このように、医療企業による高い導入率が、予測期間中、同地域のヘルスケアコンプライアンスソフトウェア市場を牽引すると考えられます。

さらに、複数の主要企業が存在し、M&A、提携、製品発売、協業などさまざまな戦略に注力していることも、同地域の市場成長に寄与しています。例えば、Panacea Healthcare Solutionsは、2022年8月に米国の医療ソフトウェア会社Holliday &Associatesを買収しました。この買収により、同社は600以上の病院、クリニック、アカウンタブル・ケア・オーガニゼーション、医療システムを顧客とすることができます。また、買収企業の顧客は、単一のプロバイダーから広範なソフトウェア・ソリューションを利用できるため、この買収の恩恵を受ける。したがって、このような買収は、ソフトウェアサービスの需要を強化し、ひいてはヘルスケアコンプライアンスソフトウェア市場を押し上げると予想されます。

したがって、上記の要因により、ヘルスケアコンプライアンスソフトウェア市場は予測期間中にこの地域で成長すると予想されます。

ヘルスケアコンプライアンスソフトウェア産業概要

ヘルスケアコンプライアンスソフトウェア市場は適度に細分化されています。主要市場参入企業としては、Healthicity, LLC、RLDatix、Compliancy Group LLC、HealthStream、Atlantic.Netなどが挙げられます。これらの参入企業は、製品ポートフォリオや事業領域を拡大するために、M&A、パートナーシップ、技術提携などの戦略に注力しています。また、多くの企業がパートナーシップの構築や製品の拡大を通じて成長軌道を加速させるため、協定を結んだり資金調達に乗り出しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 医療プロバイダーによるデジタルデータ保存へのシフト

- 手動のヘルスケアコンプライアンス手法から自動コンプライアンスソフトウェアへのシフト

- 患者中心のケアの重視

- 市場抑制要因

- 専門クリニックの認識不足と限られたITリソース

- 高い導入コスト

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-100万米ドル)

- 製品タイプ別

- オンプレミス

- クラウドベース

- ウェブベース

- カテゴリー別

- 政策・手順管理

- 監査ツール

- トレーニング管理と追跡

- 医療請求とコーディング

- ライセンス、証明書、契約の追跡

- インシデント管理

- 認定管理

- その他のカテゴリー

- エンドユーザー別

- 病院

- 専門クリニック

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Healthicity, LLC

- RLDatix

- Compliancy Group LLC

- HealthStream

- Atlantic.Net

- ByteChek, Inc.

- Accountable HQ, Inc.

- Complinity Technologies Private Limited

- Radar Healthcare

- ConvergePoint Inc.

- Beacon Healthcare Systems

- Sprinto

第7章 市場機会と今後の動向

The healthcare compliance software market is expected to grow at a significant CAGR of 11.1% during the forecast period.

The COVID-19 pandemic had a significant impact on the healthcare compliance software market. There was a surge in the adoption of healthcare compliance software by many healthcare organizations and hospitals due to social distancing and remote work. The pandemic also led to updates and changes in healthcare guidelines and regulations. Besides, on-site audits and inspections were difficult during the pandemic with restrictions on physical interactions. Hence, many organizations incorporated remote auditing. For instance, in response to an emergency, the Italian Accreditation Body, Accredia, rapidly implemented remote auditing through the issuance of Technical Circular DC N 06/2020 of March 7, 2020, and the subsequent supplementation with Technical Circular DC N 08/2020 of March 19, 2020. Thus, the compliance software facilitated remote auditing and assisted healthcare organizations to stay informed and revise their practices. Hence, the COVID-19 pandemic has boosted the market growth.

The shift from manual healthcare compliance methods to automated compliance software, and the growing volume of healthcare data, are the key factors driving the growth of the healthcare compliance market. For instance, according to the report updated by International Data Corporation (IDC), around 175 Zettabytes of data is likely to be generated across the globe till 2025 by the healthcare industry as compared to 33 Zettabytes in 2018. This is fueled by data-aggregating projects in the healthcare industry, such as biobank collections, electronic health records made by public and commercial healthcare providers, and data from companies that manufacture medical devices, operate social media platforms, and construct data platforms. Hence, such factors are likely to increase the demand for the healthcare compliance software market over the forecast period.

However, the growing adoption of technology to automate many aspects of the compliance monitoring process, such as data collection, analysis, reporting, and training staff is also a major contributor to the market growth. Technology can enhance the precision and efficiency of compliance monitoring thereby reducing the risk of human errors. It can also help organizations analyze large amounts of data, which can help identify areas of non-compliance and take corrective actions. Thus, due to the above-mentioned factors, the healthcare compliance software market is expected to increase during the study period.

However, the lack of awareness and limited IT resources among specialty clinics, and high implementation costs are likely to hinder market growth over the forecast period.

Healthcare Compliance Software Market Trends

Cloud-Based Segment Holds Significant Share in the Market During the Forecast Period

The cloud-based segment is expected to witness significant growth in the healthcare compliance software market over the forecast period. The key factor contributing to the growth of the segment is cost-effectiveness or subscription-based pricing model, and increased security and scalability. Besides, favorable government support is also contributing to market growth. For instance, the US Health Insurance Portability and Accountability Act (HIPAA), the European General Data Protection Regulation (GDPR), and the industry-standard CSF HITRUST Alliance all promote and regulate the protection of customers' personal information in online services. SaaS solutions and public cloud software are increasingly used to build HIPAA security programs and manage infrastructure without relying on on-premises data center experts and servers owing to their rapid deployment, scalability of workloads, applications, and affordable pricing. Thus, the adoption of cloud-based software by hospitals, and healthcare organizations would strengthen segment growth.

Additionally, the launch of new products in the segment will further drive market growth. For instance, in January 2023, CenTrak announced the launch of WorkflowRT, a scalable, cloud-based platform that automates workflow and communications to reduce the load of manual paperwork essential throughout each stage of clinical care. It allows organizations to track key patient flow indicators through the platform's integrated reporting in order to identify abnormalities or bottlenecks. Healthcare institutions have shown a decrease in patient wait times, an increase in care time with patients, and higher levels of satisfaction among patients and staff by leveraging historical measurements to support process improvements. Thus, the factors mentioned above are expected to propel the segment's growth over the forecast period.

North America Holds the Largest Market Share of the Healthcare Compliance Software Market

North America is expected to dominate the healthcare compliance software market over the forecast period. Among the other countries in the region, the United States is leading the market due to the rising incidents of cyber-attacks and data breaches, growing adoption of cloud-based solutions, increasing adoption of technology-driven solutions, and digitalization.

The increasing incidents of data breaches and cyber-attacks are contributing to market growth. For instance, as per the Office for Civil Rights (OCR) of the United States government reports, healthcare organizations reported 145 data breaches in the first quarter of 2023. However, in 2022, there were 707 reported incidents of data breaches, resulting in the theft of 51.9 million records. The most prevalent forms of healthcare data breaches in 2022 were hacking and IT incidents (555), unauthorized access or disclosure (113), physical theft (35), and improper record disposal (4). In addition, over the previous five years, the OCR imposed USD 65,658,440 in HIPAA fines. This includes USD 2,170,140 in 2022, with the largest penalty issued to Oklahoma State University's Center for Health Services, which had to pay USD 875,000 after criminal hackers penetrated its server. Such cases of cyber-attacks & data breaches are likely to drive the demand for healthcare compliance software which in turn is expected to boost the market growth.

Furthermore, the growing adoption of digital transformation in healthcare and cloud-based solutions also contributes to market growth. For instance, a 2023 article reported a study published by Duplo Cloud, the pioneer in the field of DevOps automation and compliance which conducted a survey among IT professionals to understand the adoption of cloud computing software in the healthcare industry. It reported that hospitals and Medicare/Medicaid organizations had the highest adoption rates of cloud infrastructure, at 91% and 90%, respectively, among the many types of healthcare organizations. The lowest levels of adoption were observed in dental offices (23%), and doctor's offices (37%). Thus, the high adoption rate by healthcare firms is likely to drive the healthcare compliance software market in the region over the forecast period.

Additionally, the presence of several key players and their focus on various strategies such as mergers & acquisitions, partnerships, product launches, and collaboration are also contributing to the market growth in the region. For instance, Panacea Healthcare Solutions acquired US-based healthcare software firm Holliday & Associates in August 2022. With this acquisition, the company can reach 600+ hospitals, medical practices, accountable care organizations, and health systems as clients. Also, the clients of the acquirer benefit from this acquisition as they have access to an extensive range of software solutions from a single provider. Thus, such acquisitions would strengthen the demand for software services which, in turn, is anticipated to boost the healthcare compliance software market.

Therefore, due to the factors mentioned above, the healthcare compliance software market is expected to grow in the region over the forecast period.

Healthcare Compliance Software Industry Overview

The healthcare compliance software market is moderately fragmented. Some key market players are Healthicity, LLC, RLDatix, Compliancy Group LLC, HealthStream, and Atlantic.Net. These players are focusing on strategies such as mergers and acquisitions, partnerships, and technological collaboration to expand their product portfolio and business footprint. Besides, many companies are forming agreements and looking for funding to accelerate their growth trajectories through partnership development and product expansion.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 A Shift to Digital Data Storage By Healthcare Providers

- 4.2.2 Shift from Manual Healthcare Compliance Methods to Automated Compliance Software

- 4.2.3 Emphasis on Patient-Centered Care

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness & Limited IT Resources among Specialty Clinics

- 4.3.2 High Implementation Costs

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 On-Premise

- 5.1.2 Cloud-Based

- 5.1.3 Web-Based

- 5.2 By Category

- 5.2.1 Policy and Procedure Management

- 5.2.2 Auditing Tools

- 5.2.3 Training Management and Tracking

- 5.2.4 Medical Billing and Coding

- 5.2.5 License, Certificate, and Contract Tracking

- 5.2.6 Incident Management

- 5.2.7 Accreditation Management

- 5.2.8 Other Category

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Healthicity, LLC

- 6.1.2 RLDatix

- 6.1.3 Compliancy Group LLC

- 6.1.4 HealthStream

- 6.1.5 Atlantic.Net

- 6.1.6 ByteChek, Inc.

- 6.1.7 Accountable HQ, Inc.

- 6.1.8 Complinity Technologies Private Limited

- 6.1.9 Radar Healthcare

- 6.1.10 ConvergePoint Inc.

- 6.1.11 Beacon Healthcare Systems

- 6.1.12 Sprinto