|

市場調査レポート

商品コード

1408235

サーバーオペレーティングシステム:市場シェア分析、産業動向と統計、2024~2029年の成長予測Server Operating System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サーバーオペレーティングシステム:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

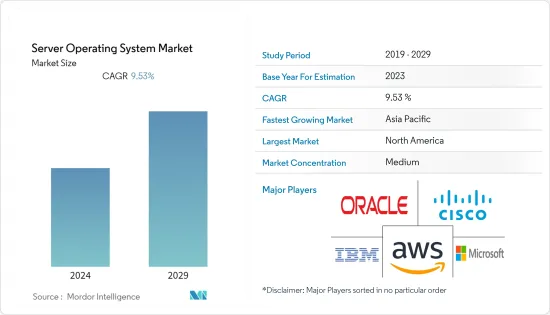

サーバーオペレーティングの世界市場規模は、今年度190億7,000万米ドルでした。

予測期間中のCAGRは9.53%で、予測年度末には306億9,000万米ドルに達すると予測されています。

主要ハイライト

- 同市場の成長は、堅牢なデータセンターインフラの構築に対する企業の支出に起因しています。また、ハイブリッドクラウド環境の採用増加や5Gネットワーク技術の導入が市場の成長を後押ししています。さらに、技術の進歩とインフラにおけるセキュリティ要件の増加は、予測期間中に市場に有利な拡大機会を提供すると予測されます。

- クラウドプラットフォームとインフラストラクチャの採用が増加し、著名な参入企業の多くによるデータセンターインフラストラクチャへの投資が増加していることが、市場の成長を後押ししています。現在の先進的なインフラ整備は、世界のクラウドサーバーユーザー数を押し上げると予想されます。主要なクラウドコンピューティングサービス企業は、世界中のクラウドインフラの拡大にかなりの金額を投資しています。例えば、2023年2月、Oracle Corporationは、クラウドサービスの需要増加を考慮し、サウジアラビアで15億米ドルを投資するパブリッククラウドの新計画を発表しました。

- サーバーは、ITS(高度道路交通システム)やV2X(Vehicle-to-Everything)通信向けの5GやAIアプリケーションなど、高性能で低遅延なサービスの提供など、スマートシティにおけるさまざまな用途に利用できます。また、公共輸送向けのクラウドベースのVoIP(Voice-over-IP)通信システムのホストや、IoTセンサーやデバイスからのデータの保存・管理にも利用できます。さらに、高可用性サーバーは、スマートシティ・サービスのセキュリティや認証プロセスでも役割を果たすことができます。例えば、世界的に多くのスマートシティプロジェクトや取り組みが実施されており、都市化に伴う世界の投資が促進されています。OECDは、2010年から2030年の間に、スマートシティ構想への国際投資は、都市インフラ・プロジェクト全体で約1兆8,000億米ドルに達すると推定しています。このことは、市場シェアを獲得するためにOSの新バージョンを開発する機会を各社にもたらすと思われます。

- 市場シェアを拡大するため、市場参入企業は新たな戦略を取り入れています。例えば、2023年7月、エンタープライズLinuxディストリビューション「ロッキーリナックス」上でワークロードを実行する企業向けソフトウェア・インフラを構築するCIQは、本日、CIQパートナー・プログラムの開始を発表しました。同社は、ITインフラやハイパフォーマンス・コンピューティングのニーズに対して、安定性、シームレスな互換性、コスト効率を求める世界中の組織に、同社の一連のソリューションとサービスを提供することを目的としており、今回の立ち上げは、CIQのパートナー第一のチャネル戦略を強化するものであると述べています。CIQパートナー・プログラムは、製品開発、科学研究、モデリング、機械学習、AIなどのデータ集約型ワークロードを大規模に展開・管理する企業や政府機関にインフラを販売する再販業者やインテグレーターに最適です。

- しかし、少数のアプリケーション向けにカスタマイズ型サーバーオペレーティングシステムへの関心の拡大や、合理的なサーバーの選択に関連する多くの困難は、市場開拓にマイナスの影響を与えると予想されます。また、高い設立費用とサポート費用は、予測期間中に製品を宣伝するための試練となります。いずれにせよ、BYOD(Bring Your Device Policy)や統合アドミタンス・フレームワークに対する要求の高まりは、予測期間中にサーバーに対する関心を維持するのに役立つと考えられています。

- COVID-19の大流行により、世界中のデジタル変革とインターネットサービスが大幅に後押しされ、企業やビジネスのかなりの部分が在宅勤務と連携を開始しました。COVID-19パンデミックの間、企業の運営を維持するために遠隔技術が要求されたため、データセンターの必要性が高まった。パンデミックの後、新たな企業環境が生まれ、クラウドサービスやデジタル化が促進され、企業はより良い働き方をサポートするためにデジタルインフラを近代化しました。

サーバーオペレーティングシステム市場の動向

クラウドセグメントが市場で大きなシェアを占める見込み

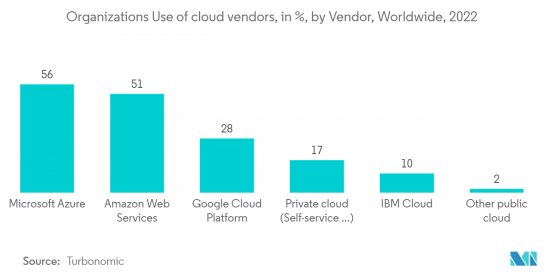

- クラウドコンピューティング技術を利用する企業が増えており、ITインフラを自社で構築・維持することなく、効率的なアプリケーションとデータ管理を提供できるようになっています。Flexera 2023 State of the Cloud Reportによると、企業の回答者の75%がパブリッククラウドの利用にMicrosoft Azureを採用していると回答しています。

- Amazon Web Services(AWS)、Microsoft Azure、Google Cloudは、世界的に主要なクラウドコンピューティング・プラットフォーム・プロバイダーです。このようなクラウド技術の急速な採用と、マルチクラウドサービスへのワンストップ・アクセスに対する需要の高まりは、クラウドサービス仲介の機会を生み出しています。このようなクラウドの大規模な導入は、サーバーの需要を増加させ、それに比例して調査市場の需要を促進します。

- さらに、フォーティネットのクラウドレポート2022によると、ほとんどの組織がハイブリッド(39%、2021年の36%から増加)またはマルチクラウド戦略(33%)を追求し、スケーラビリティや事業継続性の理由から複数のサービスを取り入れています。76%が2社以上のクラウドプロバイダーを利用しています。企業はワークロードをクラウドに急速に移行し続けています。調査対象企業の39%は、ワークロードの半分以上をクラウドに移行しており、58%は今後12~18ヶ月でこのレベルに達する予定です。クラウドユーザーは、クラウドが適応可能なキャパシティとスケーラビリティ(53%)、敏捷性の向上(50%)、可用性と事業継続性の向上(45%)という約束を実現していることを保証しています。

- 組織の近代化とクラウドへの移行が突然必要になったため、さまざまな金融機関がクラウドサービスプロバイダーと提携しました。HSBCがAmazon Web Services (AWS)とクラウド契約を計画したり、Deutsche BankがGoogle Cloudと10年間の戦略的パートナーシップを結んだり、Santanderが1日あたり200台以上のサーバーをクラウドに移行すると発表したりしたように、同社はこのプロジェクトの完了期限を2023年と宣言しています。

- Thales Groupによると、2022年現在、企業情報の約60%がクラウドに保存されているといわれています。企業がセキュリティ、信頼性、企業の俊敏性を高めるためにリソースをクラウド環境に移行する動きが進むにつれ、この割合は2015年に30%に達し、その後も増え続けています。これらの要因は、市場調査対象のベンダーにとって、今後数年間で提供サービスを拡大する大きな成長機会を生み出します。

- 企業の間でクラウドコンピューティングの採用が進んでいることも、市場の調査範囲を拡大しています。例えば、インドを拠点とする市場ベンダーであるDruva Inc.は、非構造化データが大量にあるため、多くの企業が主に企業データを対象としていると報告しています。同社はまた、エンタープライズ・ストレージシステムに保存されているデータの80%以上がこのデータであると報告しています。

- Turbonomicによると、2022年7月に発表されたデータによると、2021年には回答者の56%がクラウドサービスにMicrosoft Azureを利用していると回答しています。2020年にMicrosoftがその座を奪うまでは、Amazon Web Servicesがトップだった。さらに、どのクラウドも利用していないという回答者の割合は、2021年の4%から2022年には8%に増加しました。

- パンデミック時に実施されたCloudPathSurveyによると、89%の銀行がハイブリッドクラウドのストレージと展開で運用を計画しています。Nutanixの第3回金融サービス向けEnterprise Cloud Indexによると、ハイブリッドクラウドの導入は今後5年間で39%増加すると予想されています。このようなクラウド展開に向けた大規模な採用は、調査対象市場の需要を促進すると思われます。

北米が大きな成長を遂げる見込み

- 北米は市場で大きなシェアを占めると予想されます。サーバーオペレーティングシステムの需要増加とインターネットアプリケーションの開発により、アメリカ人が国際市場をリードすると予測されます。人工知能技術を利用したサーバーオペレーティングシステムは、ストレージやサーバー管理など多くのアプリケーションを管理します。同地域の市場は、多くの企業でクラウドコンピューティング・ソリューションの採用が拡大していることが要因となっています。その結果、地方の市場参入企業数社がクラウドコンピューティング・サービスへの投資を拡大しています。いくつかの参入企業は、サーバーオペレーティングシステム・サービスの提供にも注力しています。

- この地域の参入企業は、市場シェアを獲得するために、サーバー用の新しいオペレーティングシステム(OS)を開拓しています。例えば、Red Hat Enterprise Linux(RHEL)9 Betaが利用可能で、エキサイティングな新機能と多くの修正を提供しています。RHEL 9 Betaはアップストリームカーネルバージョン5.14で確立されており、RHELの次のメジャーアップデートのプレビューを提供します。このリリースは、オンプレミスやパブリック・クラウドからエッジまで、ハイブリッドなマルチクラウドの展開を必要とするように設計されています。ビルトインのビジネスシングルサインオンフレームワークであるSystem Security Services Daemon(SSSD)には、タスク完了までの時間、エラー、認証フローなどの可能性について、より詳細な情報が追加されました。新しい検索機能により、管理者はパフォーマンスや設定の問題を分析できます。

- United States Small Business Administration Office of Advocacyによると、2022年、米国の中小企業数は3,320万社に達し、国内のほぼすべての企業(99.9%)を占めました。2022年の米国における中小企業数の増加は継続的な成長を反映しており、前年(2021年)から2.2%増、2017~2022年にかけては12.2%増となっています。様々な地域における中小企業のこのような大規模な増加は、市場参入企業が市場シェアを獲得するために新しいソリューションを開発する機会を創出すると思われます。このような膨大な数の中小企業は、調査対象市場の成長を可能にすると思われます。

- さらに、クラウドコンピューティングの台頭により、仮想化技術も市場の牽引役となっています。クラウド環境では、仮想化を利用して複数の仮想マシン(VM)を作成・管理します。例えば、KVM(Kernael-based Virtual Machine)を搭載したLinuxや、Hyper-Vを搭載したMicrosoft Windowsなど、堅牢な仮想化機能を提供するオペレーティングシステムは、クラウドプロバイダーやユーザーにとって不可欠なものとなっています。こうした技術は、リソースの効率的な割り当てとVMの管理を可能にし、クラウド展開における特定のサーバーオペレーティングシステムの魅力をさらに高めています。

- さらに、国内では5Gの導入が急増しており、展開される5Gの機能やサービスをサポートするサーバーオペレーティングシステムの需要が高まると思われます。例えば、エリクソンによると、5Gの契約数は2026年までに1億9,500万を超え、米国では2029年までに5Gが米国モバイル市場全体の約71.5%を占めるようになるといわれています。CTIAによると、急速な成長は米国の5G経済の基盤を作る。

サーバーオペレーティングシステム業界概要

世界のサーバーオペレーティングシステム市場は、Oracle、Cisco System、IBM、Amazon Web Services、Microsoft Corporationなど複数の参入企業が存在し、適度に統合されています。各社は戦略的パートナーシップや製品開拓に継続的に投資し、市場シェアを大きく伸ばしています。最近の市場開拓をいくつか紹介しよう:

2023年6月、アプリケーションに特化したコンピューティングソリューションを専門とするHIPER Globalは、Ubuntu Linuxディストリビューションとオープンソース製品を提供するCanonicalとの新たな提携を発表しました。この提携は、HIPER Globalの世界中の顧客に対し、Ubuntu Linuxのセキュリティ修正と長期サポートのサブスクリプションを含む付加価値サービスを提供することを目的としています。さらに顧客は、プライベートクラウド基盤、仮想化コンポーネント、集中管理システム、Kubernetesのサポートバージョンなど、HIPER Globalのソリューションに統合された先進的なキヤノニカル製品を利用できるようになります。さらに、このパートナーシップは、世界中の顧客に高度なサービスを提供するというHIPER Globalのコミットメントを強化するものです。

2023年1月、オープンソースソリューションの世界的プロバイダーであるRed Hat, Inc.とOracleは、複数州にわたる契約を締結しました。この協業は、Oracle Cloud Infrastructure向けのオペレーティングシステムの選択肢を顧客に追加提供することを目的としています。この提携は、QCIがサポートするオペレーティングシステムのリストにRed Hat Enterprise Linuxを追加することから始まる。さらに、このアップグレードは、デジタルトランスフォーメーションと必須アプリケーションのクラウド移行にOCIとRed Hat Enterprise Linuxに依存している企業を支援します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- ハイブリッドプラットフォームとクラウドプラットフォームの利用増加によるサーバーオペレーティングシステムの需要拡大

- ハイパースケールデータセンター構築への投資の増加が市場拡大を大きく促進

- 市場抑制要因

- 高いサーバーダウンタイムと導入コストが市場拡大を阻害する可能性

- セキュリティ上の欠陥の増加が市場の成長を妨げる可能性

第6章 市場セグメンテーション

- コンポーネント別

- ソフトウェア

- サービス

- タイプ別

- Windows

- Linux

- UNIX

- その他のタイプ

- 仮想化別

- 仮想サーバー

- 物理サーバー

- 導入形態別

- クラウド

- オンプレミス

- 企業規模別

- 大企業

- 中小企業(SME)

- 業界別

- IT・通信

- BFSI

- 製造業

- 小売・eコマース

- 政府機関

- 医療

- その他業界別

- 地域

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Oracle System Corporation

- Cisco Systems, Inc.

- IBM Corporation

- Amazon Web Services(AWS)

- Microsoft Corporation

- NEC Corporation

- Google LLC

- Fujitsu Ltd.

- Delll Technologies Inc.

- Hewlett PAckward Enterprises

- Apple Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The global server operating market was valued at USD 19.07 billion in the current year. It is expected to reach USD 30.69 billion by the end of the forecasted year, registering a CAGR of 9.53% during the forecast period.

Key Highlights

- The market's growth is attributed to enterprise spending on creating a robust data center infrastructure. In addition, the increasing adoption of hybrid cloud environments and deployment of 5G networking technologies fuel the market's growth. Further, technological advancements and increasing security requirements in infrastructure are anticipated to provide lucrative expansion opportunities for the market during the forecast period.

- Increasing adoption of cloud platforms & infrastructure and rising data center infrastructure investments by most of the prominent players are assisting the market growth. The development of current advanced infrastructure is anticipated to boost the number of cloud server users worldwide. The key cloud computing service firms are investing a considerable portion of money in expanding cloud infrastructure around the globe. For instance, In February 2023, Oracle Corporation announced a new plan for public cloud in Saudi Arabia with an investment of USD 1.5 billion, considering the increasing demand for cloud services.

- Servers can be used in various applications in smart cities, including delivering high-performance, low-latency services such as 5G and AI applications for intelligent transportation systems (ITS) and vehicle-to-everything (V2X) communication. They can also be used to host cloud-based voice-over-IP (VoIP) communication systems for public transportation and storing and managing data from IoT sensors and devices. Additionally, high-availability servers can play a role in smart city services' security and authentication processes. For example, Globally, many smart city projects and efforts are being implemented, encouraging global investments owing to urbanization. The OECD estimates that between 2010 and 2030, international investments in smart city initiatives would total around USD 1.8 trillion for all urban city infrastructure projects. This would create an opportunity for the players to develop a new version of OS to capture the market share.

- To expand their market share, the market players are incorporating new strategies; for instance, In July 2023, CIQ, which builds software infrastructure for enterprises running workloads atop the Rocky Linux enterprise Linux distribution, announced today the launch of its CIQ Partner Program. The company said the launch reinforces CIQ's partner-first channel strategy as it aims to deliver its suite of solutions and services to organizations worldwide that desire stability, seamless compatibility, and cost-effectiveness for their IT infrastructure and high-performance computing needs. The CIQ Partner Program is ideal for resellers and integrators selling to enterprises and government organizations deploying and managing infrastructure at scale, data-intensive workloads for product development, scientific research, modeling, machine learning, and AI.

- However, the expanded interest in server operating systems with customized arrangements for a few applications & the many difficulties related to choosing a reasonable server is expected to affect the market development negatively. Besides, high establishment & support expenses represent a test to advertise product during the forecast period. In any case, the Bring Your Device Policy (BYOD) & the rising requirement for unified admittance frameworks are considered to assist with keeping the interest up for servers over the forecast period.

- The Covid-19 pandemic significantly boosted digital transformation and Internet services worldwide, with a significant part of businesses and enterprises that have started cooperating and working from home. The need for data centers has grown since remote technologies are demanded to keep companies operating during the Covid-19 pandemic. Following the pandemic, a new company environment has materialized, boosting cloud services and digitization as corporations modernize their digital infrastructure to support better working practices.

Server Operating System Market Trends

Cloud Segment is Expected to Hold a Significant Share of the Market

- A growing number of companies are increasingly using cloud computing technologies to provide efficient application and data management with no need for constructing or maintaining IT infrastructures on site. As per Flexera 2023 State of the Cloud Report, 75% of enterprise respondents indicated adopting Microsoft Azure for public cloud usage.

- Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are the leading cloud computing platform providers globally. This rapid adoption of cloud technologies and the rising demand for one-stop access to multi-cloud services have created opportunities for cloud services brokerage. Such huge adoption of the cloud would increase the demand for servers, proportionately driving the demand for the studied market.

- Further, according to the Fortinet cloud report 2022, Most organizations pursue a hybrid (39%, up from 36% in 2021) or multi-cloud strategy (33%) to incorporate multiple services for scalability or business continuity reasons. 76% percent are utilizing two or more cloud providers. Firms continue to move workloads to the cloud at a rapid pace. 39% of surveyed members have more than half of their workloads in the cloud, while 58 percent plan to get to this level in the next 12-18 months. Cloud users guarantee that the cloud is delivering on the promise of adaptable capacity and scalability (53%), increased agility (50 percent), and improved availability and business continuity (45%).

- As organizations had to modernize and migrate to the cloud abruptly, various financial organizations partnered with cloud service providers. Such as HSBC's planned cloud contract with Amazon Web Services (AWS), Deutsche Bank striking a 10-year strategic partnership with Google Cloud, and Santander's made announcement that it is shifting its over 200 servers to the cloud per day, the company has declared the deadline to complete this project is the year 2023.

- According to Thales Group, as of 2022, around 60% of all corporate information is stored in the cloud. As companies progressively move their resources into cloud environments to enhance security, dependability, and enterprise agility, this proportion hit 30% in 2015 and has since continued to grow. These factors create a massive growth opportunity for the market-studied vendors to expand their offerings in the coming years.

- The growing adoption of cloud computing among enterprises also expands the market studied scope. For instance, India-based market vendor, Druva Inc., reported that many companies primarily target enterprise data due to a large amount of unstructured data. The company also reported that this data claim accounts for over 80% of the data stored in enterprise storage systems.

- According to Turbonomic, they released data in July 2022 stating that, in 2021, 56% of respondents stated that they are utilizing Microsoft Azure for their cloud services. Amazon Web Services was on top of the list until 2020 Microsoft took its place. Additionally, the percentage of respondents not utilizing any cloud increased to eight percent in 2022 from four percent in 2021.

- As per CloudPathSurvey conducted during a pandemic, 89% of banks plan to operate with hybrid cloud storage and deployment. As per Nutanix's third annual Enterprise Cloud Index report for financial services, hybrid cloud adoption is expected to grow 39% in the coming five years. Such huge adoption towards cloud deployment would drive the demand for the studied market.

North America Expected to Witness Significant Growth

- North America is expected to hold a significant share of the market. Americans are anticipated to lead the international market due to the increasing demand for server operating systems and the development of Internet applications. Using artificial intelligence technology, the server operating system manages many applications, such as storage and server management. The market in the region is being driven by the growing adoption of cloud computing solutions across numerous corporations. As a result, several provincial market participants are expanding their investments in cloud computing services. Several players are even focused on providing server operating system services.

- The players in the region are developing new operating systems (OS) for servers to capture the market share. For example, Red Hat Enterprise Linux (RHEL) 9 Beta is available and delivers exciting new features and many more modifications. RHEL 9 Beta is established on upstream kernel version 5.14 and delivers a preview of the following major update of RHEL. This release is designed to require hybrid multi-cloud deployments that range from on-premises and public cloud to edge. The System Security Services Daemon (SSSD), the built-in business single-sign-on framework, now adds more detail for possibilities such as time to complete tasks, errors, the authentication flow, and more. New search capabilities allow admins to analyze performance and configuration issues.

- According to the United States Small Business Administration Office of Advocacy, in 2022, the number of small businesses in the United States reached 33.2 million, accounting for nearly all (99.9 percent) firms in the country. The growth in the number of small businesses in the United States in 2022 reflects continuous growth, with a 2.2% increase from the previous year(2021) and a 12.2% increase from 2017 to 2022. Such a massive rise in the SMEs in the various region would create an opportunity for the market players to develop new solutions to capture the market share. Such a huge number of SMEs would allow the studied market to grow.

- Furthermore, virtualization technologies have also been instrumental in driving the market with the rise of cloud computing. Cloud environments use virtualization to create and manage multiple virtual machines (VMs). Operating systems that offer robust virtualization capabilities, for example, Linux with KVM (Kernael-based Virtual Machine) or Microsoft Windows with Hyper-V, become essential for cloud providers and users. Such technologies enable the efficient allocation of resources and managing VMs, further growing the appeal of specific server operating systems in cloud deployments.

- Further, the booming 5G deployments in the country will increase the demand for server operating systems to support the 5G features and services being rolled out. For instance, according to Ericsson, there will be more than 195 million 5G subscriptions by 2026, and by 2029, in the United States, 5G will account for about 71.5% of the entire U.S. mobile market. According to CTIA, rapid growth creates a platform for the US 5G economy.

Server Operating System Industry Overview

The Global Server Operating System market is moderately consolidated with the presence of several players like Oracle, Cisco System, IBM, Amazon Web Services, Microsoft Corporation, etc. The companies continuously invest in strategic partnerships and product developments to gain substantial market share. Some of the recent developments in the market are:

In June 2023, HIPER Global, a company specializing in application-specific computing solutions, announced a new partnership with Canonical, the provider of Ubuntu Linux distribution and open-source products. The collaboration aims to offer HIPER Global's worldwide customers value-added services, including a subscription to security fixes and long-term support for Ubuntu Linux. Additionally, customers will have access to advanced Canonical products integrated into HIPER Global solutions, such as private cloud infrastructures, virtualization components, centralized management systems, and supported versions of Kubernetes. Furthermore, the partnership strengthens HIPER Global's commitment to delivering advanced service to its customer worldwide.

In January 2023, Red Hat, Inc., the global provider of open-source solutions, and Oracle formed a multi-state agreement. The collaboration aims to provide clients with additional operating system options for Oracle Cloud Infrastructure. The partnership begins with adding Red Hat Enterprise Linux to QCI's supported operating systems list. Furthermore, this upgrade will assist enterprises that rely on OCI and Red Hat Enterprise Linux for digital transformation and cloud migration of essential applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing hybrid and cloud platform usage will increase demand for server operating systems

- 5.1.2 Rising investments in the building of hyperscale data centers are significantly driving the market expansion

- 5.2 Market Restraints

- 5.2.1 High server downtime and implementation costs could impede market expansion

- 5.2.2 The growing number of security flaws could hamper the growth of the market

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Service

- 6.2 By Type

- 6.2.1 Windows

- 6.2.2 Linux

- 6.2.3 UNIX

- 6.2.4 Other Types

- 6.3 By Virtualization

- 6.3.1 Virtual Server

- 6.3.2 Physical Server

- 6.4 By Deployment Mode

- 6.4.1 Cloud

- 6.4.2 On-premise

- 6.5 By Enterprise Size

- 6.5.1 Large Enterprises

- 6.5.2 Small and Medium-sized Enterprises (SMEs)

- 6.6 By Industry Vertical

- 6.6.1 IT and Telecom

- 6.6.2 BFSI

- 6.6.3 Manufacturing

- 6.6.4 Retail and E-Commerce

- 6.6.5 Government

- 6.6.6 Healthcare

- 6.6.7 Other Industry Verticals

- 6.7 Geography

- 6.7.1 North America

- 6.7.2 Europe

- 6.7.3 Asia-Pacific

- 6.7.4 Latin America

- 6.7.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Oracle System Corporation

- 7.1.2 Cisco Systems, Inc.

- 7.1.3 IBM Corporation

- 7.1.4 Amazon Web Services (AWS)

- 7.1.5 Microsoft Corporation

- 7.1.6 NEC Corporation

- 7.1.7 Google LLC

- 7.1.8 Fujitsu Ltd.

- 7.1.9 Delll Technologies Inc.

- 7.1.10 Hewlett PAckward Enterprises

- 7.1.11 Apple Inc.