|

市場調査レポート

商品コード

1408188

慢性腰痛(CLBP)-市場シェア分析、産業動向・統計、2024~2029年の成長予測Chronic Lower Back Pain (CLBP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 慢性腰痛(CLBP)-市場シェア分析、産業動向・統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

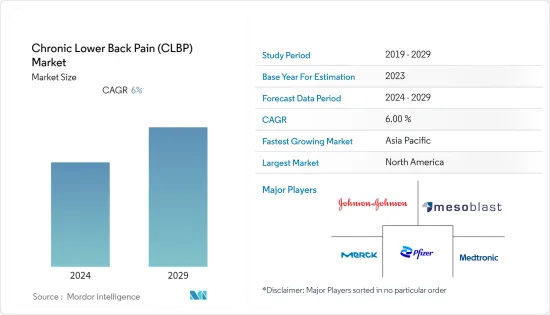

慢性腰痛(CLBP)市場は予測期間中にCAGR 6.0%を記録すると予測されます。

主要ハイライト

- COVID-19の大流行時、対象市場の成長は初期段階でかなり影響を受けたが、政府の厳格な対策により治療は再開されました。ストレスレベルの上昇や精神的苦痛は、筋肉の緊張を引き起こし、腰痛に対する感受性を高める可能性があります。2022年9月にMedical News Todayが発表した記事によると、腰の不快感は急性と慢性のCOVID-19の徴候である可能性があります。

- ウイルス感染は筋肉痛を直接引き起こす可能性があり、発熱による不動は筋肉疲労を悪化させる可能性があります。同様に、2021年11月に発行されたJournal of Medical Science誌が発表した論文によると、COVID-19の入院患者のうち69.3%が痛みを訴え、43.6%が背部痛、33.1%が腰痛を訴えたといいます。

- さらに、国際疼痛学会が2023年1月に発表した別の論文によると、慢性疼痛は世界の成人の5人に1人が罹患しているといいます。慢性疼痛による疾病負担と効果的な疼痛管理に対する需要は、COVID-19の流行期間中に増加し、関節痛と筋肉痛が急性期とCOVID長期感染者の両方で報告されました。

- COVID後は、身体活動の減少により慢性腰痛への影響が増大しました。例えば、2023年3月にOsong Public Health Research Perspectivesが発表した論文によると、COVID-19に罹患した患者の46.6%が痛みを訴え、筋骨格系の痛みを経験したCOVID-19と診断された患者の92.6%がCOVID-19に罹患する前は痛みがなかったと答えています。このようなCOVID後の慢性腰痛の増加は、予測期間中に市場に大きな影響を与えると予想されます。

- 神経痛や腰背部筋肉痛の症例数の増加は、市場の成長を押し上げると予想されます。例えば、StatPearls Publishingが2022年10月に発表した記事によると、末梢神経の問題は世界人口の約2.4%に影響を与え、高齢者では8.0%に増加します。同様に、2023年2月に同じ情報源から発表された別の論文によると、慢性腰痛は世界中の成人の23%が罹患しており、生涯における再発率は24%から80%です。このように、慢性腰痛の有病率の増加は、診断率と治療法の採用を高め、予測期間中の市場の成長を導くと予想されます。

- 高齢者人口の増加は、市場成長を促進する主要理由の一つです。例えば、WHOがWorld Social Report 2023で発表したデータによると、65歳以上の世界人口は4倍を超え、2021年の7億6,100万人から2050年には16億人に増加すると予想されています。80歳以上の高齢者数は、さらに急速に増加しています。

- 同市場における製品承認は、市場成長の原動力になると予想されます。例えば、2023年2月、メソブラスト社は、FDAのOffice of Tissues and Advanced Therapies(OTAT)が、腰椎椎間板への注入用デリバリー剤としてヒアルロン酸(HA)と併用することで、椎間板変性に伴う慢性腰痛(CLBP)の治療薬としてrexlemestrocel-L再生医療先進療法(RMAT)の指定を与えたと発表しました。同様に、2022年12月、食品医薬品局(FDA)は、慢性疼痛の治療に用いるアボット社のマイナー脊髄刺激(SCS)インプラントEternaを承認しました。このような承認は、予測期間中の市場成長を押し上げると予想されます。

- 様々な組織による腰痛治療の研究開発も市場成長を促進します。例えば、2023年3月にSIR(Society for Interventional Radiology)が実施した研究によると、VIA Disc注射(VIVEX Biologics)の治療後3年間で、60%の患者の痛みが50%以上改善し、70%以上の患者の動きや機能が20ポイント以上向上したと述べています。

- しかし、治療による副作用や偽造薬の入手が可能であることが、市場成長の妨げになると予想されます。

慢性腰痛(CLBP)市場動向

慢性腰痛(CLBP)市場の疼痛タイプでは、慢性腰痛セグメントが大きなシェアを占めると予想されます。

- 慢性腰痛例の有病率の上昇と全体的な診断導入率により、慢性腰痛セグメントは予測期間中に大幅に増加すると予想されます。例えば、StatPearlsが2023年2月に発表した記事では、腰の不快感は成人の共同であり、成人の23%が慢性腰痛に苦しんでいます。この再発率は生涯で24%から80%です。このように、腰痛の再発率の高さは、セグメントの成長を促進すると予想されます。

- 同様に、Lancet Rheumatology誌が2023年6月に発表した論文によると、2020年には世界で6億1,900万人が腰痛に苦しんでおり、2050年にはその数は8億4,300万人に達すると予想されています。このように、世界の腰痛の流行はエスカレートしており、市場セグメントを牽引すると予想されています。

- さらに、2022年10月にPubMedが発表した論文によると、慢性腰痛の多くは24歳から39歳で4.2%、20歳から59歳で19.6%でした。歳以上を対象とした6つの研究では、慢性腰痛の有病率は3.9%から10.2%、3つの研究では13.1%から20.3%と報告されています。

- 同じ出典によると、ブラジルの高齢者人口における慢性腰痛の大部分は25.4%でした。腰の不快感は今後増加すると予想され、この分野の市場成長を後押しします。

北米が市場で大きなシェアを占めると予想され、予測期間中も同様と予想される

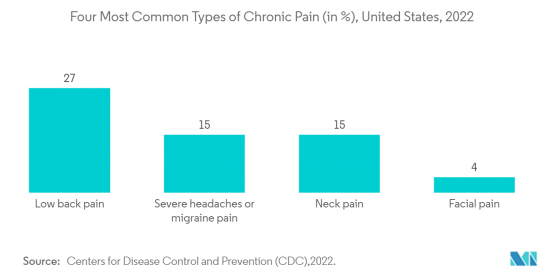

- 北米では慢性腰痛患者が増加しており、市場の牽引役となることが期待されます。例えば、2022年10月に発表されたCenter on an Aging Society(CAS)の記事によると、全個人の8%に当たる約1,600万人の成人が持続的な慢性腰痛に悩まされており、日常業務をこなす能力が制限され、米国で6番目に高額な医療費となっています。

- 同様に、Red Cross Therapy(RCT)が2022年12月に発表した論文によると、アメリカ人の約80%が少なくとも年に一度は腰痛を経験し、18歳以上の約8%が活動が著しく制限されるほどの慢性腰痛に苦しんでいるといわれています。このため、同地域では様々な治療法の導入が進み、市場の成長を後押しすることが期待されます。

- 製品承認は同地域の市場成長を後押しすると予想されます。例えば、2022年10月、Nevro Corp.は、Senza HFX iQ脊髄刺激(SCS)システムについて米国食品医薬品局(FDA)から承認を取得したと発表しました。従って、このような様々な地域製品の承認が市場を牽引すると予想されます。

慢性腰痛(CLBP)産業概要

慢性腰痛(CLBP)市場は細分化され、競合が激しく、複数の大手企業が存在します。現在、数社の大手企業が市場シェアで市場を独占しています。現在市場を独占している企業には、Johnson &Johnson Services Inc.、Pfizer Inc.、Mesoblast Limited、Merck &Co.、Medtronicなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 腰痛に対する幹細胞治療の増加

- 神経痛疾患の増加

- 高齢者人口の増加

- 市場抑制要因

- 治療による副作用と偽造薬の入手可能性

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-100万米ドル)

- 疼痛タイプ別

- 急性疼痛

- 亜急性腰痛

- 慢性腰痛

- その他の疼痛タイプ(機械的疼痛、橈骨神経痛、橈骨神経炎)

- 診断名別

- 痛みの評価

- 病歴

- 身体所見

- 画像診断ガイドライン

- エンドユーザー別

- 病院

- 整形外科クリニック

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Johnson & Johnson Services Inc.

- Pfizer Inc

- Vertebral Technologies, Inc.

- Merck & Co.

- Medtronic

- Boston Scientific Corporation

- Mesoblast Limited

- SpineThera

- Stayble Therapeutics

- Eli Lilly and Company

- Persica Pharmaceuticals

第7章 市場機会と今後の動向

目次

Product Code: 5000306

The chronic lower back pain (CLBP) market is projected to register a CAGR of 6.0% during the forecast period.

Key Highlights

- During the COVID-19 pandemic, the target market growth was considerably influenced in the early stages; treatments resumed due to strict government measures. Elevated stress levels and emotional distress may cause muscle tightness and heightened sensitivity to lower back pain. According to an article published by Medical News Today in September 2022, lower back discomfort can be a sign of acute and chronic COVID-19.

- Viral infections can directly cause muscle pain, and fever-induced immobility can exacerbate muscle strain. Similarly, an article published by the Journal of Medical Science published in November 2021 stated that, among hospitalized people with COVID-19, 69.3% reported pain, with 43.6% reporting back pain and 33.1% reporting lower back pain.

- Moreover, another article published by the International Association for the Study of Pain in January 2023 stated that chronic pain affects 1 in 5 adults globally. The burden of disease due to chronic pain and the demand for effective pain management increased during the COVID-19 pandemic, with joint and muscle pain being reported both in the acute phase and by those with long COVID.

- Post-COVID, the impact on chronic lower back pain increased due to reduced physical activities. For instance, an article published by Osong Public Health Research Perspectives in March 2023 stated that 46.6% of patients who contracted COVID-19 complained of pain, and 92.6% of patients diagnosed with COVID-19 who experienced musculoskeletal pain said no pain before getting COVID-19. Such an increase in chronic lower back pain post-COVID is expected to significantly impact the market during the forecast period.

- The increasing number of nerve and lower back muscle pain cases is expected to boost the market growth. For instance, an article published by StatPearls Publishing in October 2022 stated that peripheral nerve problems impact approximately 2.4% of the global population, with an increase to 8.0% in older people. Similarly, another article published by the same source mentioned in February 2023 stated that chronic low back pain affects 23% of adults worldwide, with a recurrence rate of 24% to 80% in their lifetime. Thus, the increasing prevalence of chronic lower back pain is expected to raise the diagnosis rate and adoption of treatment, leading the market to grow in the forecast period.

- The increasing geriatric population is one of the main reasons to promote market growth. For instance, according to WHO data published in the World Social Report 2023, the global population of individuals aged 65 and over is expected to surpass quadruple, rising from 761 million in 2021 to 1.6 billion in 2050. The number of people aged 80 and above is increasing considerably faster.

- The product approvals in the market are expected to drive the market growth. For instance, in February 2023, Mesoblast Limited announced that the FDA's Office of Tissues and Advanced Therapies (OTAT) granted rexlemestrocel-L regenerative medicine advanced therapy (RMAT) designation for the treatment of chronic low back pain (CLBP) associated with disc degeneration, in combination with hyaluronic acid (HA) as a delivery agent for injection into the lumbar disc. Similarly, in December 2022, the Food and drug administration (FDA) approved the minor spinal cord stimulation (SCS) implant Abbott's Eterna from Abbott to treat chronic pain. Such approvals are expected to boost the market growth during the forecast period.

- Research and development in treating lower back pain by various organizations also promote market growth. For instance in March 2023, a study carried out by Society for Interventional Radiology (SIR) stated that 60% of patients had a 50% or better improvement in pain three years following therapy of VIA Disc injection (VIVEX Biologics), and more than 70% had a larger than the 20-point increase in movement and function.

- However, the side effects of treatments and the availability of counterfeit drugs are expected to hamper the market growth.

Chronic Lower Back Pain (CLBP) Market Trends

The Chronic back pain Segment is Expected to Hold a Major Share in Pain Type of the Chronic Lower Back Pain (CLBP) Market.

- The chronic back pain segment is expected to increase significantly during the forecast period due to the rising prevalence of chronic back pain cases and the overall diagnostic adoption rate. For instance, in an article published by StatPearls in February 2023, back discomfort is joint in adults, and 23% of adults suffer from chronic low back discomfort. This recurrence rate was 24% to 80% in their lifetime. Thus, the high recurrence rate of lower back pain is expected to drive segmental growth.

- Similarly, an article published by the Lancet Rheumatology in June 2023 stated that 619 million people worldwide suffered from low back pain in 2020, and by 2050, that number is expected to reach 843 million. Thus, the global low back pain epidemic is escalating and expected to drive the market segment.

- Moreover, an article published by PubMed in October 2022 stated that most chronic low back pain was 4.2% in people aged 24 to 39 and 19.6% in people aged 20 to 59. Six studies with people aged 18 and up indicated chronic low back pain prevalence ranging from 3.9% to 10.2%, while three reported prevalence ranging from 13.1% to 20.3%.

- As per the same source, the majority of chronic low back pain in the Brazilian elderly population was 25.4%. Lower back discomfort is anticipated to rise in future years, boosting the segmental market growth.

North America is Expected to Hold a Significant Share in the Market and Expected to do the Same in the Forecast Period

- North America has an increasing number of chronic back pain is expected to drive the market. For instance, according to the Center on an Aging Society (CAS) article published in October 2022, approximately 16 million adults that are 8% of all individuals, suffered from persistent chronic back pain, limiting their ability to do daily tasks, making that sixth most expensive medical problem in the United States.

- Similarly, an article published by Red Cross Therapy (RCT) in December 2022 stated that approximately 80% of Americans experience back pain at least once a year around 8% of people aged 18 and up suffer from chronic back pain to the point where their activities are severely limited. This is expected to increase various treatment adoption in the region and expected to boost the growth in the market.

- Product approvals are expected to boost the market growth in the region. For instance, in October 2022, Nevro Corp. announced that it had received approval from the United States Food and Drug Administration (FDA) for the Senza HFX iQ spinal cord stimulation (SCS) system. Therefore, such approvals of various regional products are expected to drive the market.

Chronic Lower Back Pain (CLBP) Industry Overview

The chronic lower back pain (CLBP) market is fragmented, competitive, and has several major players. A few of the major players are currently dominating the market in terms of market share. Some companies currently dominating the market are Johnson & Johnson Services Inc., Pfizer Inc, Mesoblast Limited, Merck & Co., and Medtronic.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Stem Cell therapy for Lower Back Pain

- 4.2.2 Increasing Prevelence of Nerve Pain Disorders

- 4.2.3 Growing geriatric population

- 4.3 Market Restraints

- 4.3.1 Side Effects of Treatments and Availability of Counterfeit Drugs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Pain Type

- 5.1.1 Acute Pain

- 5.1.2 Subacute Low Back Pain

- 5.1.3 Chronic Back Pain

- 5.1.4 Other Pain Types (Mechanical pain, Radicular pain, Radiculitis)

- 5.2 By Diagnosis

- 5.2.1 Assessment of Pain

- 5.2.2 Clinical History

- 5.2.3 Physical Examination

- 5.2.4 Imaging Guidelines

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Orthopedic Clinics

- 5.3.3 Other End -Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Johnson & Johnson Services Inc.

- 6.1.2 Pfizer Inc

- 6.1.3 Vertebral Technologies, Inc.

- 6.1.4 Merck & Co.

- 6.1.5 Medtronic

- 6.1.6 Boston Scientific Corporation

- 6.1.7 Mesoblast Limited

- 6.1.8 SpineThera

- 6.1.9 Stayble Therapeutics

- 6.1.10 Eli Lilly and Company

- 6.1.11 Persica Pharmaceuticals