|

市場調査レポート

商品コード

1408147

航空機用救命機器:市場シェア分析、産業動向と統計、2024~2029年の成長予測Aircraft Survival Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用救命機器:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

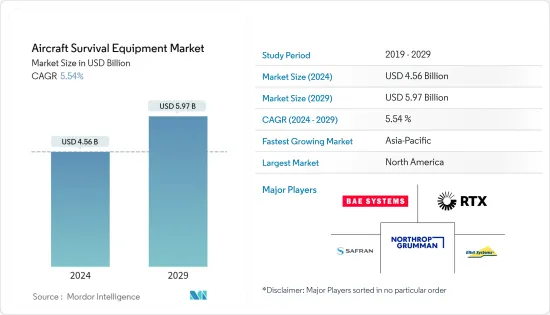

航空機用救命機器の市場規模は2024年に45億6,000万米ドルと推定され、2029年には59億7,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは5.54%で成長する見込みです。

COVID-19パンデミックは航空機生存装置市場に大きな影響を与えました。COVID-19の発生は、各国での封鎖や各国間の渡航制限につながり、それによって製造用部品の不足や最終最終製品の製造の遅れにつながった。現在のシナリオでは、規制が緩和されたことで各国間の貿易が自由になり、市場は生産量の増加を目の当たりにしています。これは近い将来、航空機用救命機器市場の着実な成長につながると思われます。

航空機用救命機器は、緊急時の救命に使用される基本的なツールやキットのパッケージで構成されています。すべてのタイプの航空機は、飛行時間中の安全性向上のために救命キットを装備しています。電子支援機器は、航空機の生存率を向上させるために航空機に設置されます。これには、飛行制御、アビオニクス、ナビゲーション、通信システムなどが含まれます。さらに、電子攻撃システムは、敵の攻撃や外部の脅威による損傷から航空機を守るために使用されます。このように、戦闘作戦用の戦闘機に対する需要の高まりが、市場成長の原動力となっています。

さらに、航空部門の急速な拡大、航空交通量の増加、航空機発注の増加は、航空機生存装置の需要を生み出しています。さらに、航空機周辺で発生する事故や災難の増加により、様々な管理機関が安全規範を厳格化しており、これが市場成長の原動力となっています。

航空機用救命機器の市場動向

市場セグメンテーションが市場シェアをリード

予測期間中、商業セグメントが航空機用救命機器市場をリードすると予想されます。乗客の安全確保は民間航空産業の主要目標です。乗客の移動の増加に伴い、民間航空機用救命機器の需要も増加しました。国際空港評議会(ACI)ワールドによると、2022年の世界航空旅客輸送量は66億人で、2021年から43.8%増加しました。旅客輸送量が最も多かった空港は、米国のアトランタ、ダラス、デンバー、シカゴで、ドバイ(アラブ首長国連邦)は世界第5位だった。

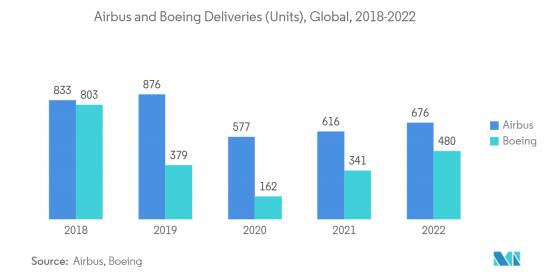

航空会社などの利害関係者は、増加する旅客輸送量を受け入れるにふさわしい、安全、安心、効率的な航空輸送システムの構築に引き続き注力しなければならないです。民間航空機の納入台数の増加もまた、市場の成長に拍車をかけています。例えば、2022年にエアバスは661機の民間航空機を84の顧客に納入し、1,078機の新規受注を記録しました。同様に、同年、Boeingは480機の航空機を納入し、774件の新規純受注を獲得しました。

2023年7月、モロッコの国営航空会社Royal Air Maroc(RAM)は、増加する旅客需要に対応するため、2037年までに保有機を4倍の200機に増やす計画を発表しました。2023年6月には、IndiGo AirlinesがエアバスA320型機を500機発注し、2030年から2035年にかけて納入する予定です。このような要因は、予測期間中の航空機生存装置市場の成長に寄与すると思われます。

アジア太平洋が予測期間中に最も高い成長を示すだろう

アジア太平洋は予測期間中に最も高いCAGRで推移すると予想されます。都市化の進展、航空交通量の増加、新しい航空機に対する需要の増加が、この地域の市場成長を後押しします。中国やインドなどの新興経済国による航空旅行者数の増加や航空分野への支出の増加は、近い将来の市場成長につながる可能性が高いです。

中国の航空機製造会社COMACが発表したデータによると、中国は2040年までに世界最大の航空市場に成長し、中国製航空機の保有機数は同時期に9,957機に達し、世界の旅客機保有機数の22%を占めるようになるといわれています。

国際航空運送協会(IATA)の報告書によると、インドは2024年までに英国を抜いて第3位の航空市場になります。航空産業への支出の増加と新空港の開発は、新型航空機の需要増につながります。インド政府は軍事力の強化に力を入れています。2021年の国防支出額は中国が第2位、インドが第3位でした。2021年9月、インドはAirbus Defence and SpaceとC-295輸送機56機の調達契約を締結しました。

この新機材は、インド空軍のアブロ748型機に取って代わることになります。このように、インド、中国、日本、韓国などの国々による航空機調達への支出の増加は、予測期間中に最も高い成長を遂げるアジア太平洋につながると思われます。

航空機用救命機器産業概要

航空機用救命機器市場は本質的に断片化されており、様々な種類の救命機器を提供する複数の事業者によって特徴付けられます。市場の著名な参入企業には、Northrop Grumman Corporation、Elbit Systems Ltd、BAE Systems plc、RTX Corporation、Safranなどがあります。先端技術のイントロダクションと戦闘作戦用の次世代戦闘機の開発が市場成長を促進しています。2022年、Northrop Grummanは米国海軍の電子攻撃機EA-18Gグラウラーを開発したが、これにはALQ-99妨害ポッド、ALQ-218受信機、衛星通信、通信対策などの攻撃装備が含まれています。こうした装備は、敵の脅威から軍用機を守る。したがって、このような進歩は予測期間中の市場の成長につながると思われます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 設備

- 救命いかだ

- 医療キット

- 電子支援

- 電子攻撃

- その他の装備

- アプリケーション

- 商用

- 防衛

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- BAE Systems plc

- Ellbit Systems Ltd.

- Northrop Grumman Corporation

- RUAG Ltd.

- THALES

- RTX Corporation

- Safran

- Saab AB

- Legend Aerospace

- Survitec Group Limited

- FCAH Aerospace

- TULMAR Safety Systems

第7章 市場機会と今後の動向

The Aircraft Survival Equipment Market size is estimated at USD 4.56 billion in 2024, and is expected to reach USD 5.97 billion by 2029, growing at a CAGR of 5.54% during the forecast period (2024-2029).

The COVID-19 pandemic significantly affected the Aircraft Survival Equipment Market. The onset of COVID-19 led to lockdowns in various countries and restrictions in terms of travel between countries, thereby leading to shortages in components for manufacturing and delays in terms of manufacturing the final end product. In the current scenario, the free flow in terms of trade between countries, owing to the ease of restrictions, has led to the market witnessing an increase in terms of production. This would lead to steady growth in the near future for the aircraft survival equipment market.

The aircraft survival equipment consists of a package of basic tools and kits used for survival in an emergency. All types of aircraft are equipped with survival kits for improved safety during flight hours. The electronic support equipment is installed in an aircraft to improve its survival. It includes flight control, avionics, navigation, and communication systems. Furthermore, electronic attack systems are used to protect aircraft from enemy attacks and damage from external threats. Thus, the growing demand for fighter aircraft for combat operations drives the market growth.

In addition, the rapid expansion of the aviation sector, growing air traffic, and rising aircraft orders create demand for aircraft survival equipment. Furthermore, various governing bodies tighten the safety norms due to an increase in the number of accidents and mishaps occurring around aircraft, which in turn drives the market growth.

Aircraft Survival Equipment Market Trends

Commercial Segment to Lead Market Share

The commercial segment is expected to lead the aircraft survival equipment market during the forecast year. Ensuring passenger safety is the primary goal of the commercial aviation industry. With the increase in passenger movement, the demand for commercial aircraft survival equipment also increased. According to the Airports Council International (ACI) World, in 2022, the global air passenger traffic stood at 6.6 billion, an increase of 43.8% from 2021. A few of the airports that handled the maximum passenger traffic were Atlanta, Dallas, Denver, and Chicago in the US, and Dubai (UAE) was in the fifth position globally.

Aviation stakeholders such as airline companies must continue to focus on building a safe, secure, efficient air transport system fit to welcome the rising passenger traffic. The rise in commercial aircraft deliveries also adds to market growth. For instance, in 2022, Airbus delivered 661 commercial aircraft to 84 customers and registered 1,078 gross new orders. Similarly, in the same year, Boeing delivered 480 airplanes and won 774 net new orders.

In July 2023, Moroccan state-owned airline Royal Air Maroc (RAM) announced its plans to quadruple its fleet to 200 aircraft by 2037 to meet increasing passenger demand. In June 2023, IndiGo Airlines placed an order for 500 Airbus A320 aircraft to be delivered between 2030 and 2035. Such factors will contribute to the growth of the aircraft survival equipment market during the forecast years.

Asia-Pacific Will Showcase the Highest Growth During the Forecast Period

Asia-Pacific is expected to register the highest CAGR during the forecast period. Growing urbanization, rising air traffic, and increasing demand for new aircraft would boost the market growth across the region. An increase in the number of air travelers and growing expenditure on the aviation sector from emerging economies such as China and India are likely to lead to market growth in the near future.

According to the data presented by COMAC, a Chinese aircraft manufacturing company, China will grow to become the largest aviation market globally by 2040, with the fleet size of Chinese aircraft increasing to reach 9,957 by the same time and shall account for 22% of the global passenger aircraft fleet.

According to the International Air Transport Association (IATA) report, India will surpass the United Kingdom to become the third-largest aviation market by 2024. Increasing spending on the aviation industry and the development of new airports will lead to increased demand for new aircraft. The Indian government holds a strong focus on strengthening military capabilities. China and India were the second and third largest defense spenders, respectively, in 2021. In September 2021, India signed a contract with Airbus Defence and Space for the procurement of 56 C-295 transport aircraft.

The new fleet will replace the Avro-748 planes of the Indian Air Force. Thus, growing spending on aircraft procurement from countries such as India, China, Japan, and South Korea would lead to the Asia-Pacific region with the highest growth during the forecast period.

Aircraft Survival Equipment Industry Overview

The aircraft survival equipment market is fragmented in nature and is characterized by several operators who provide various types of survival equipment. Some of the prominent players in the market include Northrop Grumman Corporation, Elbit Systems Ltd, BAE Systems plc, RTX Corporation, and Safran. The introduction of advanced technologies and the development of next-generation fighter aircraft for combat operations is driving the market growth. In 2022, Northrop Grumman developed the EA-18G Growler, the US Navy's electronic attack aircraft, that includes attack equipment such as the ALQ-99 jamming pods, ALQ-218 receiver, satellite communications, and communication countermeasures. Such equipment protects military aircraft from enemy threats. Thus, such advancements would lead to growth in the market during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Equipment

- 5.1.1 Life Rafts

- 5.1.2 Medical Kits

- 5.1.3 Electronic Support

- 5.1.4 Electronic Attack

- 5.1.5 Other Equipment

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Defense

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 Ellbit Systems Ltd.

- 6.2.3 Northrop Grumman Corporation

- 6.2.4 RUAG Ltd.

- 6.2.5 THALES

- 6.2.6 RTX Corporation

- 6.2.7 Safran

- 6.2.8 Saab AB

- 6.2.9 Legend Aerospace

- 6.2.10 Survitec Group Limited

- 6.2.11 FCAH Aerospace

- 6.2.12 TULMAR Safety Systems