|

|

市場調査レポート

商品コード

1408069

日本の超音波装置:市場シェア分析、産業動向・統計、2024~2029年の成長予測Japan Ultrasound Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本の超音波装置:市場シェア分析、産業動向・統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 85 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

日本の超音波装置市場規模は、2024年の4億7,418万米ドルから2029年には6億75万米ドルに成長し、予測期間(2024~2029年)のCAGRは6.08%と予測されます。

COVID-19パンデミックは、日本の超音波装置市場に大きな影響を与えました。パンデミックの間、さまざまな心臓血管や婦人科処置のための超音波処置を含む診断処置が大きな影響を受けたからです。また、パンデミック中は、初期診断ツールとして超音波を必要とする選択的手術が減少しました。例えば、2021年11月にPubMed Centralで発表された論文によると、日本ではCOVID-19のパンデミック当初、外科患者に対する標準的な医療の提供が制限されました。このように、パンデミックは当初、市場に大きな影響を与えました。しかし、パンデミック後の期間も超音波装置の需要は安定しており、予測期間中の市場の成長を後押しすると予想されます。

超音波装置は、心血管疾患、婦人科疾患、筋骨格系疾患、がんなどの診断に広く使用されているため、日本の慢性疾患負担の増加に伴い、超音波装置の需要は予測期間中に拡大すると予想されます。例えば、THE LANCET Regional Healthが2022年11月に発表した記事によると、日本では2021年に脳卒中などの心血管疾患の負担が高いという調査が行われました。さらに、SpringerLinkが2023年1月に発表した論文によると、ある研究が日本で実施され、調査対象集団における心血管疾患と動脈硬化の加重有病率は、それぞれ37.3%と33.5%でした。また、頸動脈疾患、冠動脈疾患、脳血管疾患は、心血管疾患の最も一般的なサブタイプでした。

さらに、BMC Musculoskeletal Disordersが2022年8月に発表した論文によると、日本で行われた研究によると、慢性筋骨格痛のプール有病率は39.0%で、そのうち男性が36.3%、女性が41.8%と多く、有病率は年齢とともに増加しました。このような慢性疾患の有病率の高さは、日本における高齢者人口の増加とともに、診断のための超音波装置の使用率を高め、市場成長を促進すると予想されます。

さらに、契約、提携、製品発売、買収など、主要参入企業やさまざまな組織による新興国市場の発展も、日本における技術的に高度な製品へのアクセスを増加させると予想されるため、市場成長を促進すると期待されます。例えば、2021年1月、Olympus CorporationとHitachi, Ltd.は、内視鏡超音波システム(EUS)を共同開発する5年間の契約を東京で締結しました。また、Hitachi, Ltd.はこの契約に基づき、EUSに使用される診断用超音波システムと関連部品をOlympusに供給し続けることになります。

このように、日本では慢性疾患の有病率が高く、発展が進んでいるなど、上記のような要因が市場の成長を後押しすると予想されます。しかし、厳しい規制が市場の成長を阻害すると予想されます。

日本の超音波装置市場動向

予測期間中、ポータブル超音波装置セグメントが大きな市場シェアを占める見込み

ポータブル超音波装置は、モバイル超音波システムとも呼ばれ、狭いスペース、患者のベッドサイド、または診断現場で直接使用するように設計されています。ポータブル超音波装置は、可動性と手頃な価格、正確で迅速な診断、患者の処理能力の向上、据え置き型超音波装置よりもアクセスが容易であるなどの利点があり、あらゆる医療プロバイダーにとってより良い選択肢となります。

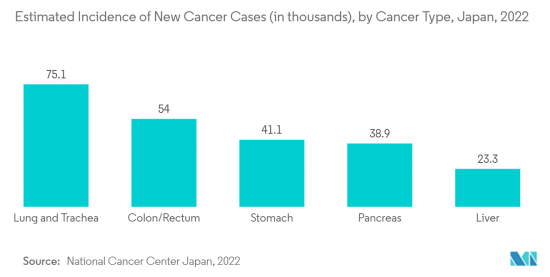

携帯型超音波検査分野の成長を促進する主要要因には、これらの機器で使用される高度な技術、ポイントオブケア診断を必要とするがんや心血管疾患の有病率の上昇、携帯型超音波検査の利用可能性に関する意識の高まりなどがあります。例えば、国立がん研究センターが2022年6月に発表したデータによると、日本では2022年に101万9,000件の新規がん罹患が予測され、そのうち結腸/直腸がんが15万8,000件、胃がんが13万2,000件、肺/気管がんが12万8,000件と予測されています。

さらに、技術的に高度な製品の開発における重要な参入企業による活動の活発化も、セグメントの成長を高めると予想されます。例えば、2021年11月、Canon Medicalは日本のiLEAD(革新的な肝臓、弾性、減衰、分散)研究を支援しました。これは、肝生検に対する定量的超音波イメージングツールを評価する多施設共同研究です。iLEADは、ポータブル超音波装置Aplio Iシリーズの肝臓パッケージで利用でき、臨床環境で脂肪症、線維症、炎症を評価することができます。したがって、このような研究はポータブル超音波システムの使用範囲を拡大し、市場成長を押し上げると予想されます。

このように、日本におけるがんや心血管疾患の有病率の高さ、技術的に先進的な製品を開発するための主要参入企業による活動の活発化など、上記の要因は、ポータブル超音波システムの利用を増加させ、その結果、セグメントの成長を押し上げると予想されます。

市場セグメンテーションでは、循環器領域が予測期間中に大きなシェアを占めると予想されます。

心不全、心雑音、虚血性心疾患、急性肺動脈血栓塞栓症などの心血管疾患は、超音波装置によって診断されることが多いです。日本では、このような疾患の有病率が増加しており、高齢者人口が増加していることから、同分野の成長が期待されています。例えば、Journal of American Heart Associationが2021年11月に発表した論文によると、日本人は生涯で心血管疾患を発症するリスクが高いです。このように、同国では心血管疾患の負担が大きいため、超音波装置の利用が促進されると予想されます。

さらに、同国では高齢者人口が多く、心血管疾患は高齢者と関連することが多いため、超音波装置の使用量が増加し、市場成長を押し上げると予想されます。例えば、2022年に発表された「2022年版高齢社会白書」によると、2022年の日本の65歳以上人口は3,621万人強で、総人口の28.9%を占める。この数は2024年には3,935万人とピークに達すると予想されています。したがって、同国では高齢者人口が多いため、心血管疾患の有病率も増加すると考えられ、超音波装置の使用量が増加すると予想されます。

このように、日本における心血管疾患の有病率の高さや高齢者人口の増加といった上述の要因は、セグメントの成長を後押しすると予想されます。これらの要因によって、日本での超音波装置の使用量が増加すると推定されます。

日本の超音波装置産業概要

日本の超音波装置市場は競争が激しく、複数の大手企業が参入しています。同市場の主要企業には、Canon Medical Systems Corporation、Siemens Healthineers AG、GE Healthcare、Fujifilm Holdings Corporation、Koninklijke Philips NVなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の負担増

- 超音波装置の技術進歩

- 市場抑制要因

- 厳しい規制

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模(100万米ドル))

- 用途別

- 麻酔科学

- 循環器科

- 婦人科/産科

- 筋骨格系

- 放射線学

- クリティカルケア

- その他

- 技術別

- 2D超音波イメージング

- 3Dと4D超音波イメージング

- ドップラーイメージング

- 高密度焦点式超音波

- タイプ別

- 据え置き型

- ポータブル

第6章 競合情勢

- 企業プロファイル

- Canon Medical Systems Corporation

- Fujifilm Holdings Corporation

- GE Healthcare

- Hologic Inc.

- Koninklijke Philips NV

- Konica Minolta, Inc.

- Neusoft Medical Systems Co. Ltd

- Esaote SPA

- Siemens Healthineers AG

- Carestream Health

- Becton, Dickinson and Company

第7章 市場機会と今後の動向

The Japan Ultrasound Devices Market size is expected to grow from USD 474.18 million in 2024 to USD 600.75 million by 2029, at a CAGR of 6.08% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the ultrasound devices market in Japan, as the diagnostic procedures, including ultrasound procedures for various cardiovascular and gynecological procedures, were greatly affected during the pandemic. Also, fewer elective surgeries occurred during the pandemic, which required ultrasound as an initial diagnostic tool. For instance, according to an article published by PubMed Central in November 2021, the initial COVID-19 pandemic restricted the delivery of standard medical care to surgical patients in Japan. Thus, the pandemic had a significant effect on the market initially. However, the demand for ultrasound devices is expected to remain consistent during the post-pandemic period, thereby boosting the market's growth over the forecast period.

Ultrasound devices are widely used to diagnose cardiovascular diseases, gynecological diseases, musculoskeletal diseases, and cancer, among others; thus, with Japan's rising chronic disease burden, the demand for ultrasound devices is expected to grow over the forecast period. For instance, according to an article published by THE LANCET Regional Health in November 2022, a study was conducted in Japan in 2021, which showed that the country has a high burden of cardiovascular diseases such as stroke, among others. Moreover, according to an article published by SpringerLink in January 2023, a study was conducted in Japan, which showed that the weighted prevalence of cardiovascular diseases and atherosclerosis in the study population was 37.3% and 33.5%, respectively. The source also stated that carotid artery disease, coronary heart disease, and cerebrovascular diseases were among the most common subtypes of cardiovascular diseases.

Moreover, according to an article published by BMC Musculoskeletal Disorders in August 2022, a study was conducted in Japan which showed that the pooled prevalence of chronic musculoskeletal pain was 39.0% in Japan, among which the majority in men was 36.3% and women 41.8%, and the prevalence increased with age. Thus, the high prevalence of such chronic diseases, along with the rising geriatric population in Japan, is expected to enhance the usage of an ultrasound devices for diagnosis, thus driving the market growth.

Additionally, the rising developments by key players and various organizations, such as agreements, partnerships, product launches, and acquisitions, are also expected to enhance the market growth, as they are expected to increase access to technologically advanced products in Japan. For instance, in January 2021, Olympus Corporation and Hitachi, Ltd. signed a five-year contract in Tokyo to develop endoscopic ultrasound systems (EUS) jointly. Hitachi would also continue to supply diagnostic ultrasound systems and related parts used in EUS to Olympus under this contract.

Thus, the factors mentioned above, such as the high prevalence of chronic diseases in Japan and the rising developments, are expected to boost market growth. However, stringent regulations are expected to impede the growth of the market.

Japan Ultrasound Devices Market Trends

Portable Ultrasounds Segment is Expected to Hold a Significant Market Share Over the Forecast Period

Portable ultrasound machines are also known as mobile ultrasound systems, and they are designed to be used in small spaces, at a patient's bedside, or directly in the diagnostic field. They provide the advantages of mobility and affordability, accurate and instant diagnosis, improved patient throughput, and ease of access over stationary ultrasound devices, which makes them a better choice for any healthcare provider.

The major factors driving the growth of the portable ultrasounds segment include advanced technology used in these devices, the rising prevalence of cancer and cardiovascular diseases that require point-of-care diagnosis, and rising awareness regarding the availability of portable ultrasounds. For instance, according to the data published by National Cancer Center Japan in June 2022, it was estimated that 1,019 thousand new cases of cancer were expected in Japan in 2022, out of which 158 thousand new cases of colon/rectum cancer, 132 thousand cases of stomach cancer, and 128 thousand cases of lung/trachea cancer were expected.

Moreover, the increased activity by crucial players in developing technologically advanced products is also expected to enhance segment growth. For instance, in November 2021, Canon Medical supported Japan's iLEAD (innovative Liver, Elasticity, Attenuation, and Dispersion) study. It is a multicenter study to evaluate quantitative ultrasound imaging tools against liver biopsy. It is available on the Aplio I series portable ultrasound system's Liver Package for assessing steatosis, fibrosis, and inflammation in the clinical environment. Hence, such studies are expected to increase the scope of usage of portable ultrasound systems, thus boosting market growth.

Thus, the factors mentioned above, such as the high prevalence of cancer and cardiovascular diseases in Japan and the increased activity by key players for developing technologically advanced products, are expected to increase the usage of the portable ultrasound system, thus boosting segment growth.

Cardiology Segment is Expected to Hold a Significant Share in the Market Over the Forecast Period

Cardiovascular diseases such as heart failure, cardiac murmur, ischemic heart disease, and acute pulmonary artery thromboembolism are often diagnosed by ultrasound devices. The increasing prevalence of such diseases in Japan and the rising geriatric population in the country is expected to boost the segment growth. For instance, according to an article published by the Journal of American Heart Association in November 2021, the Japanese population has a high risk of developing cardiovascular diseases in their lifetime. Thus, the high burden of cardiovascular diseases in the country is expected to boost the usage of ultrasound devices.

Moreover, the high geriatric population in the country is also expected to boost market growth as cardiovascular diseases are often associated with older people, which is expected to increase the usage of ultrasound devices. For instance, according to the 2022 White Paper on Ageing Society, published in 2022, Japan's population aged 65 and over stood at just over 36.21 million in 2022, accounting for 28.9% of the total population. This number is expected to peak at 39.35 million by 2024. Hence, with the high geriatric population in the country, the prevalence of cardiovascular diseases is also likely to increase, which is expected to increase the usage of ultrasound devices.

Thus, the factors mentioned above, such as the high prevalence of cardiovascular diseases in Japan and the rising geriatric population, are expected to boost segment growth. These factors are estimated to increase the usage of ultrasound devices in the country.

Japan Ultrasound Devices Industry Overview

Japan's ultrasound devices market is highly competitive and consists of several major players. Some of the key companies in the market are Canon Medical Systems Corporation, Siemens Healthineers AG, GE Healthcare, Fujifilm Holdings Corporation, and Koninklijke Philips NV, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Burden of Chronic Diseases

- 4.2.2 Technological Advancements in Ultrasound Devices

- 4.3 Market Restraints

- 4.3.1 Stringent Regulations

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Application

- 5.1.1 Anesthesiology

- 5.1.2 Cardiology

- 5.1.3 Gynecology/Obstetrics

- 5.1.4 Musculoskeletal

- 5.1.5 Radiology

- 5.1.6 Critical Care

- 5.1.7 Other Applications

- 5.2 By Technology

- 5.2.1 2D Ultrasound Imaging

- 5.2.2 3D and 4D Ultrasound Imaging

- 5.2.3 Doppler Imaging

- 5.2.4 High-intensity Focused Ultrasound

- 5.3 By Type

- 5.3.1 Stationary Ultrasound

- 5.3.2 Portable Ultrasound

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Canon Medical Systems Corporation

- 6.1.2 Fujifilm Holdings Corporation

- 6.1.3 GE Healthcare

- 6.1.4 Hologic Inc.

- 6.1.5 Koninklijke Philips NV

- 6.1.6 Konica Minolta, Inc.

- 6.1.7 Neusoft Medical Systems Co. Ltd

- 6.1.8 Esaote SPA

- 6.1.9 Siemens Healthineers AG

- 6.1.10 Carestream Health

- 6.1.11 Becton, Dickinson and Company