|

市場調査レポート

商品コード

1408008

ヘルスケア流通-市場シェア分析、業界動向・統計、2024~2029年成長予測Healthcare Distribution - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヘルスケア流通-市場シェア分析、業界動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

ヘルスケア流通市場は、予測期間中にCAGR 6.5%を記録する見込みです。

COVID-19パンデミックは、他に類を見ない世界の公衆衛生上の緊急事態でした。主にヘルスケアサプライチェーンの混乱により、ヘルスケア流通を含むほぼすべての産業分野に影響を与えました。しかし、企業は戦略的パートナーやメーカーのサプライヤーを通じて、サプライチェーンにおけるこれらの混乱を管理するために様々な行動を取った。例えば、Cardinal Healthが2021年12月に発表した報告書によると、同社はメーカー・サプライヤーと緊密に連携し、製品の健全な供給を支援しました。また、同出典によると、同社はヘルスケアのサプライチェーンにおける課題を管理するため、多くの物流センターに新しい倉庫管理システムを導入しました。その結果、市場は元々緩やかなマイナス影響を受けていたが、今後数年間はサプライチェーンの難題に対処するための企業戦略により発展が見込まれます。

慢性疾患の経済的負担が大きい中、流通における技術進歩、有利な研究開発投資シナリオ、その後の医薬品上市の増加が、ヘルスケア流通市場の主要促進要因となっています。例えば、2022年にNational Institution of Chronic Disease and Dataが報告したところによると、米国成人の60%近くが少なくとも1つの慢性疾患に罹患しており、成人の約40%が複数の慢性疾患(MCC)を抱えています。糖尿病、がん、心血管疾患などの慢性疾患は、米国における罹患率の主要原因です。したがって、これらの疾患の適切な管理と診断には、効果的なヘルスケア流通サービスに必要な様々なヘルスケア製品が必要です。このように、慢性疾患患者の増加がヘルスケア流通市場を牽引しています。

技術の進歩や市場参入企業の新たな流通戦略は、ヘルスケア流通市場を押し上げると予想されます。例えば、Nippon Expressは2022年5月、医薬品業界向けに超低温(~20℃~-85℃)を必要とする商品を取り扱える物流サービスを開始しました。これにより、同社は厳しい温度管理が可能な医薬品物流プラットフォームを提供しました。したがって、ヘルスケア物流におけるこうした新しいプラットフォームは、予測期間中、市場で大きな成長を維持すると予想されます。

しかし、ヘルスケア流通サービスに関連する高コストと投資が、この市場全体の成長を妨げると予想されます。

ヘルスケア流通市場の動向

小売薬局は予測期間中に大幅な成長が見込まれる

小売薬局(しばしば地域薬局として知られる)は、一般市民や開業医向けに医薬品やヘルスケア関連製品を供給・販売するほか、トイレタリー、化粧品、小型ヘルスケア機器、動物用医薬品などのその他の商品も供給・販売しています。小売薬局は多くの処方箋を扱うため、この市場を牽引すると予想されます。先進諸国では、ヘルスケア制度やプログラムが充実しているため、処方箋枚数が大幅に増加しています。

さらに、小売薬局でのヘルスケア製品の流通に関する市場参入企業間の新たな合意は、市場の成長を促進する可能性が高いです。例えば、2022年9月、McKesson CorporationはCVS Healthとのパートナーシップを延長し、2027年6月まで小売店やその他の薬局、流通センターに医薬品を流通させることで基本合意しました。同様に、2022年6月、BD(Becton, Dickinson, and Company)とFrazier Healthcare Partnersは、BDがParata Systemsを買収することで最終合意に達しました。Parata Systemsは、病院、小売薬局、その他のヘルスケア環境向けに薬局自動化ソリューションを提供する革新的なプロバイダーです。このように、これらの契約はヘルスケア製品の効率的な供給に役立ち、市場の成長を後押しすると期待されています。

さらに、高血圧、糖尿病、心血管疾患、がんなど、長期にわたる投薬が必要な慢性疾患の罹患率の増加は、処方箋の増加に直結しています。これは、予測期間中の小売薬局市場の成長をさらに促進する可能性があります。例えば、DiabetesAtlas.org 2021は、2021年に約5億3,660万人が糖尿病に罹患していると推定され、この数は2030年までに6億4,270万人に増加すると報告しています。したがって、糖尿病のような慢性疾患の高い有病率は、小売薬局から調達できる様々な医薬品の必要性を増加させ、予測期間中にセグメントで成長することが期待されています。

予測期間中、北米が市場で大きなシェアを占める見込み

北米は、製薬・バイオ医薬品産業の急速な拡大、特殊医薬品やジェネリック医薬品に対する需要の高まり、ヘルスケア分野における人工知能やブロックチェーンなどの先端技術の大規模な導入などの要因により、大きな市場シェアを占めると予想されます。

人工知能技術の利用は、世界の流通慣行を後押ししました。例えば、2021年9月にSAGEが発表した論文では、人工知能技術を利用することで、企業は顧客に出荷の最新情報を提供できると要約しています。追跡技術に障害が発生した場合、(人工知能)AIシステムは配送の遅れを追跡できるため、企業は顧客への配送時間を簡単に見積もることができます。AIによる製品配送に関するこうした最新情報は、流通サービスを向上させ、市場の成長を後押しする可能性が高いです。

さらに、この地域では処方箋の数が多いため、さまざまなヘルスケア製品と流通サービスの需要が高まっています。例えば、AssureCare LLCが2022年11月に発表したレポートによると、米国では2021年に約64億7,000万件の処方箋が調剤されたが、これは高水準であり、今後数年間でさらに増加すると予想されます。加えて、新たな地域販売契約はサービスを増加させ、市場を押し上げる可能性が高いです。例えば、2023年3月、Endonovo Therapeutics, Inc.は、退役軍人健康管理局(VHA)と国防総省(DoD)の契約への利用可能性を確保するために、フロリダ州ウェストパームビーチのAcademy Medical, Inc.とソフパルスヘルスケア機器を販売するために、Service-Disabled Veteran-Owned Small Business(SDVOSB)政府再販業者契約を締結しました。このように、処方箋の増加やヘルスケア製品の流通に関する新たな契約は、ヘルスケア流通サービスに対する需要を高め、予測期間中の市場成長を押し上げる可能性が高いです。

ヘルスケア流通業界概要

ヘルスケア流通市場は、世界に事業を展開する企業だけでなく、地域的に事業を展開する企業も存在するため、その性質上、断片化されています。競合情勢には、McKesson Corporation、Cardinal Health、Morris and Dickson Company、Smith Drug Company、Owens and Minor Inc.、Patterson Companies、PHOENIX Group、Owens、Medline Industries、とその他の企業としてよく知られている、市場シェアを保有するいくつかの国際企業や地元企業の分析が含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の高い発生率と大きな経済的負担

- 流通における技術の進歩

- 有利な研究開発投資シナリオとそれに伴う医薬品上市の増加

- 市場抑制要因

- ヘルスケア流通の高コスト

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 製品タイプ別

- 医薬品流通サービス

- 市販薬

- ジェネリック医薬品

- ブランド医薬品

- バイオ医薬品流通サービス

- 組み換えタンパク質

- モノクローナル抗体

- ワクチン

- ヘルスケア機器流通サービス

- 医薬品流通サービス

- エンドユーザー別

- 小売薬局

- 病院薬局

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- McKesson Corporation

- Cardinal Health

- Morris and Dickson Company

- Smith Drug Company

- Owens and Minor Inc

- Patterson Companies

- PHOENIX Group

- Shanghai Pharmaceutical Group

- Medline Industries

- CuraScript SD

- Mutual Drug

第7章 市場機会と今後の動向

The healthcare distribution market is expected to register a CAGR of 6.5 % over the forecast period.

The COVID-19 pandemic was an incomparable global public health emergency. It impacted almost every industry sector, including healthcare distribution, mainly due to disruptions to the healthcare supply chain. However, the companies took various actions to manage these disruptions in the supply chain through their strategic partners and manufacturer suppliers. For instance, as per the report published by Cardinal Health in December 2021, the company worked closely with its manufacturer suppliers to help ensure a healthy supply of products. In addition, as per the same source, the company installed a new warehouse management system in many distribution centers to manage the challenges in the healthcare supply chain. As a result, the market originally had a modest negative impact but is anticipated to develop due to corporate strategies for addressing supply chain difficulties over the coming years.

With the large economic burden of chronic diseases, technological advancement in distribution, favorable R&D investment scenario, and subsequent increase in drug launches are the main driving factors of the healthcare distribution market. For instance, in 2022, the National Institution of Chronic Disease and Data reported that nearly 60% of American adults suffer from at least one chronic disease, and about 40% of adults include multiple chronic conditions (MCC). Chronic conditions like diabetes, cancer, and cardiovascular disease are the leading causes of morbidity in the United States. Hence, proper management and diagnosis of these diseases are needed with various healthcare products necessary for effective healthcare distribution services. Thus, increasing cases of chronic disease are driving the healthcare distribution market.

Technological advancements and new distribution strategies of market players are expected to boost the healthcare distribution market. For instance, in May 2022, Nippon Express Co., Ltd. launched a logistics service capable of handling goods requiring ultra-low temperatures (-20 C to -85 C) for the pharmaceutical industry. With this, the company provided a pharmaceutical distribution platform with strict temperatures. Hence, these new platforms in healthcare distribution are expected to hold significant growth in the market over the forecast period.

However, the high cost and investment associated with healthcare distribution services are expected to hamper the overall growth of this market.

Healthcare Distribution Market Trends

Retail Pharmacy is Expected to Witness a Significant Growth Over the Forecast Period

Retail pharmacies (often known as community pharmacies) supply and sell medicine and medical-related products to the general public and medical practitioners, as well as other goods such as toiletries, cosmetics, small medical devices, and veterinary products. The retail pharmacy deals with many prescriptions and is thus expected to drive this market. In developed countries, the high availability of healthcare schemes and programs led to a significant increase in the number of prescriptions.

Furthermore, the new agreements among the market players for distributing healthcare products in retail pharmacies likely propel the market to grow. For instance, in September 2022, McKesson Corporation signed an agreement in principle to extend its partnership with CVS Health to distribute pharmaceuticals to retail and other pharmacies and distribution centers through June 2027. Similarly, in June 2022, BD (Becton, Dickinson, and Company) and Frazier Healthcare Partners entered a definitive agreement for BD to acquire Parata Systems. It is an innovative provider of pharmacy automation solutions for hospitals, retail pharmacies, and other healthcare settings. Thus, these agreements help supply healthcare products efficiently, which is expected to boost market growth.

Moreover, the growing incidence of chronic diseases like hypertension, diabetes, cardiovascular diseases, and cancer, which require prolonged medication, is directly related to increased prescriptions. It can further drive the growth of the retail pharmacy market during the forecast period. For instance, DiabetesAtlas.org 2021 reported that about 536.6 million people were estimated to suffer from diabetes in 2021, and this number will increase to 642.7 million by 2030. Thus, the high prevalence rate of chronic diseases like diabetes increases the need for various pharmaceuticals that can be procured from retail pharmacies and is expected to grow in the segment over the forecast period.

North America is Expected to hold Significant Share in the Market Over the Forecast Period

North America is expected to hold a significant market share owing to factors such as the rapid expansion of the pharmaceutical and biopharmaceutical industry, rising demand for specialty drugs and generics, and large-scale adoption of advanced technologies such as Artificial Intelligence and blockchain in the healthcare sector.

The use of artificial intelligence technology boosted distribution practices globally. For instance, the article published by the journal SAGE in September 2021 summarizes that by using Artificial intelligence technology, businesses can offer shipment updates to customers. When tracking technology fails, an (Artificial Intelligence) AI system can track the delay in the delivery so companies can easily estimate delivery time to their customers. These updates on product delivery through AI increase the distribution services and likely boost the market to growth.

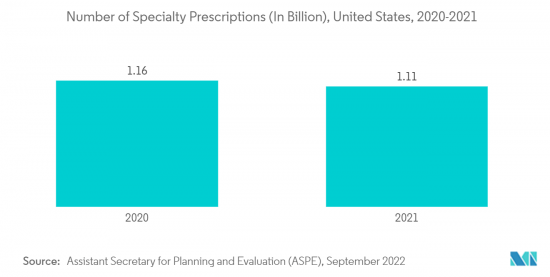

Furthermore, the significant number of prescriptions in the region increases the demand for various healthcare products and distribution services. For instance, as per the report published by AssureCare LLC in November 2022, in the United States, around 6.47 billion prescriptions were dispensed in 2021, which is high and is expected to increase more over the coming years. In addition, the new regional distribution agreements increase the services and likely boost the market. For instance, in March 2023, Endonovo Therapeutics, Inc. signed a Service-Disabled Veteran-Owned Small Business (SDVOSB) Government Reseller Agreement (Agreement or Contract) with Academy Medical, Inc. of West Palm Beach, FL, to distribute SofPulse medical devices to ensure its availability to the Veterans Health Administration (VHA) and Department of Defense (DoD) contracts. Thus, increasing prescriptions and new agreements to distribute healthcare products will likely raise the demand for healthcare distribution services and boost the market growth over the forecast period.

Healthcare Distribution Industry Overview

The healthcare distribution market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies that hold the market shares and are well known as McKesson Corporation, Cardinal Health, Morris and Dickson Company, Smith Drug Company, Owens and Minor Inc., Patterson Companies, PHOENIX Group, Owens, Medline Industries, and other Companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Incidence and Large Economic Burden of Chronic Diseases

- 4.2.2 Technological Advancement in Distribution

- 4.2.3 Favorable R&D Investment Scenario, and Subsequent Increase in Drug Launches

- 4.3 Market Restraints

- 4.3.1 High Cost of Healthcare Distribution

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product Type

- 5.1.1 Pharmaceutical Product Distribution Services

- 5.1.1.1 Over The Counter Drugs

- 5.1.1.2 Generic Drugs

- 5.1.1.3 Branded Drugs

- 5.1.2 Biopharmaceutical Product Distribution Service

- 5.1.2.1 Recombinant Proteins

- 5.1.2.2 Monoclonal Antibodies

- 5.1.2.3 Vaccines

- 5.1.3 Medical Devices Distribution Services

- 5.1.1 Pharmaceutical Product Distribution Services

- 5.2 By End-User

- 5.2.1 Retail Pharmacies

- 5.2.2 Hospital Pharmacies

- 5.2.3 Other End-Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 McKesson Corporation

- 6.1.2 Cardinal Health

- 6.1.3 Morris and Dickson Company

- 6.1.4 Smith Drug Company

- 6.1.5 Owens and Minor Inc

- 6.1.6 Patterson Companies

- 6.1.7 PHOENIX Group

- 6.1.8 Shanghai Pharmaceutical Group

- 6.1.9 Medline Industries

- 6.1.10 CuraScript SD

- 6.1.11 Mutual Drug