|

市場調査レポート

商品コード

1406998

非小細胞肺がん(NSCLC)-市場シェア分析、産業動向・統計、成長予測、2024年~2029年Non-Small Cell Lung Cancer (NSCLC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 非小細胞肺がん(NSCLC)-市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

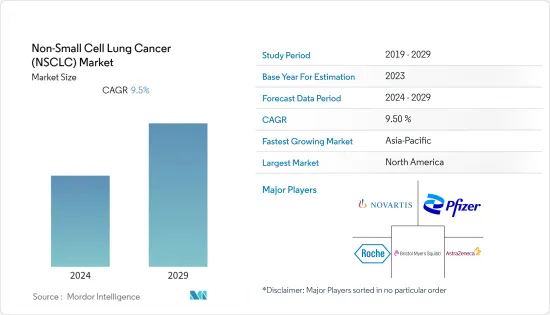

非小細胞肺がん(NSCLC)市場は、予測期間中にCAGR 9.5%を記録すると予想されます。

COVID-19は非小細胞肺がん市場の成長に大きく影響しています。例えば、clinicaltrials.govによると、2021年7月現在、200以上の介入研究がパンデミック中に中止されました。このため、パンデミック期間中の市場成長は鈍化しました。しかし、規制が解除されサービスが再開されたことで、同社は非小細胞肺がん治療のための臨床試験の実施に力を入れるようになりました。例えば、2022年10月、Daiichi Sankyo, Inc.はAstraZenecaと提携し、HER2変異転移性非小細胞肺がん(NSCLC)に対するトラスツズマブ・デルクステカンの安全性と有効性を評価する第II相臨床試験を実施しています。このような活動により、研究対象市場は予測期間中に成長すると予想されます。

非小細胞肺がんに罹患する患者数の増加や、喫煙、タバコやアルコールの摂取、サプリメントの大量摂取、座りっぱなしの生活といった不健康な習慣を持つ人々の増加が、世界中で市場の成長を牽引しています。例えば、2022年12月に発表されたニュースによると、世界全体で約220万人の新規症例が全胸部腫瘍症例の11.4%に含まれ、この数は2025年までに倍増すると予測されています。また、国立がん登録計画(ICMR-NCRP)が2022年12月に発表したデータによると、肺がん症例数は2020年の98,278例から2022年には103,371例へとなり、5%の増加となっています。このように、人口の間で肺がんの負担が大きいため、効果的な治療オプションに対する需要が高まっており、これが市場の成長を促進すると予想されます。

さらに、NSCLCの治療に有効な薬剤の研究開発に注力する企業の増加や、製品承認の増加、さまざまな治療法の指定が市場成長に寄与しています。例えば、2022年10月、GSK plcは転移性非扁平上皮非小細胞肺がん患者を対象としたJemperli(dostarlimab)+化学療法の第II相試験であるPERLAの良好な結果を報告しました。また、欧州委員会は2022年6月、Novartisのタブレクタ(一般名:カプマチニブ)を、免疫療法および/またはプラチナ製剤ベースの化学療法による治療前に全身療法を必要とする進行非小細胞肺がん(NSCLC)の成人患者に対する単剤療法として承認しました。同様に、2022年2月、医薬品・ヘルスケア製品規制庁(MHRA)は、Genentechのテセントリクを早期非小細胞肺がんの治療薬として承認しました。

さらに、肺がん患者を治療するための効果的な治療法を開発するための企業による投資の増加も、市場の成長を促進すると予想されます。例えば、臨床段階の医薬品開発企業であるDeuterOncologyは、2023年1月に565万ユーロ(610万米ドル)のシリーズA資金調達ラウンドを完了しました。この資金調達により、同社は主力製品である改良型METキナーゼ阻害剤DO-2の第I相臨床試験を開始することができ、肺がんに対するクラス最高の標的治療薬となる可能性があるとして開発が進められています。MET阻害剤は最近、METエクソン14スキップ変異を有する非小細胞肺がん(NSCLC)患者に対して承認されました。

従って、非小細胞肺がんの高負担、研究開発活動の活発化、製品承認などの要因により、研究市場は予測期間中に成長すると予想されます。しかし、治療や薬剤のコストが高く、新興諸国における診断率が低いことが、予測期間中の非小細胞肺がんの成長を阻害する可能性が高いです。

非小細胞肺がん(NSCLC)市場動向

標的薬物療法セグメントが予測期間中に大きな市場シェアを占める見込み

非小細胞肺がんの罹患率の上昇や、新規治療法の市場開拓に向けた企業活動の活発化などの要因により、標的治療薬セグメントは予測期間中に市場で大きな成長を遂げると予測されます。

標的治療薬は進行した肺がんの治療に用いられることが多く、化学療法と併用されるか、単独で使用されます。非小細胞肺がんを治療する主な標的治療薬には、エルロチニブ(タルセバ)、ゲフィチニブ(イレッサ)、アファチニブ(ギロトリフ)、モボセルチニブ(エクスキティビティ)、オシメルチニブ(タグリッソ)、ダコミチニブ(ビジムプロ)などがあります。これらの薬剤は、体内の変異遺伝子を標的とすることで、健康な細胞への悪影響を回避します。標準的な化学療法に対する優位性から市場各社が標的治療薬の開発に投資していることや、これらの薬剤が世界各国で発売されていることが、市場成長の促進力となっています。例えば、2021年10月、AUM BiosciencesはシリーズA資金調達ラウンドで2,700万米ドルを調達しました。これらの資金は、同社の精密がん治療および標的がん治療の臨床段階のパイプラインを前進させるために使用されます。

MDPIが2022年12月に発表した記事によると、精密医療の出現は非小細胞肺がんの治療に光を当て、遺伝的・エピジェネティックマーカーを標的とした治療により、進行NSCLC患者が利用できる選択肢を増やしました。さらに、2021年6月にJournal of Hematology and Oncologyに掲載された論文によると、標的治療を受けた患者は化学療法を受けた患者と比較して、無増悪生存期間が有意に改善したことが観察されています。また、同出典によると、標的治療を受けた患者でEGFR、ALK、ROS1、BRAF遺伝子変異を有する患者の奏効率は50%から80%でした。このように、分子標的治療薬の有効性は、NSCLC患者の治療への需要と同様にその採用を増加させ、それゆえこのセグメントの成長を促進しています。

さらに、標的治療薬の承認が増加することで、市場における新規治療薬の利用可能性が高まり、予測期間中の同分野の成長を促進すると予想されています。例えば、2022年8月、AstraZenecaとDaiichi Sankyoの標的治療薬Enhertuは、腫瘍に活性化HER2(ERBB2)変異を有する切除不能または転移性の非小細胞肺がん成人患者の治療薬として米国で承認されました。また、2021年5月、米国FDAは、上皮成長因子受容体(EGFR)エクソン20挿入変異など特定の遺伝子変異を有する成人非小細胞肺がん患者に対する初の標的治療薬として、ライブレバント(amivantamab-vmjw)を承認しました。

したがって、企業や研究機関による研究活動の活発化、標的薬物療法治療の採用拡大、製品承認の増加などの要因により、調査対象セグメントは予測期間中に成長すると予想されます。

北米が予測期間中に大きな市場シェアを占める見込み

北米は、人口の間で非小細胞肺がん患者数が増加していること、同地域の主要企業が上市と当局からの承認取得に注力していることなどの要因から、予測期間中に市場が大きく成長すると見込まれます。加えて、各社による研究開発投資の増加や、同地域における莫大なヘルスケア支出も市場成長に寄与しています。

人口の間でNSCLCの負担が増加していることが、同地域の市場成長を促進する主な要因です。例えば、ACSが発表した2023年の統計によると、米国では2023年に約23万8,340人の肺がん患者が新たに診断されると予想されています。さらに、カナダがん協会が発表した2022年の統計によると、カナダでは約30,000人のカナダ人が肺がんおよび気管支がんと診断され、2022年の新規がん症例の13%を占めました。このように、肺がんに罹患する人の多さは、化学療法、標的療法、その他のような効果的な治療療法への需要を煽っています。このことは、予測期間中の市場成長を促進すると予想されます。

さらに、カナダ統計局が発表したデータによると、2022年1月、肺がんはカナダで最も頻繁に診断されるがんであり、がん関連死亡の主な原因となっています。肺がん患者の約50%は、生存の可能性が信じられないほど低いステージIVで発見されます(5年間で4%)。このように、主に最終ステージで発見される肺がんの負担が大きいため、効果的な薬剤とともに化学療法セッションの需要が高まり、予測期間中の市場成長を後押しすると期待されています。

さらに、企業活動の活発化と製品認可の増加も、予測期間中の市場成長を高めると予想されます。例えば、カナダ保健省は2022年8月、切除可能な非小細胞肺がん(NSCLC)の成人患者を対象としたネオアジュバント療法において、Bristol Myers Squibbのオプジーボ360mg(静注用注射剤)をプラチナ製剤との併用で3週間ごとに3サイクル投与することを承認しました。また、2022年1月、米国FDAはAbbVieの治験薬であるテリソツズマブ・ベドチン(Teliso-V)を、プラチナ製剤による治療中または治療後に病勢が進行した、c-Met過剰発現が高値の上皮成長因子受容体(EGFR)野生型の進行性/転移性非扁平上皮非小細胞肺がん(NSCLC)患者の治療薬として、画期的治療薬指定(Breakthrough Therapy Designation:BTD)を承認しました。

したがって、製品承認や製品上市の増加、非小細胞肺がん症例数の増加といった前述の要因により、調査対象市場は予測期間中に成長すると予想されます。

非小細胞肺がん(NSCLC)産業概要

非小細胞肺がん市場は細分化された競合市場であり、複数の大手企業で構成されています。各社は市場での地位を維持するため、提携、パートナーシップ、新製品の発売、その他の取り組みなど、さまざまな主要事業戦略を採用しています。同市場の主要企業としては、F. Hoffmann-La Roche、AstraZeneca、Bristol-Myers Squibb、Merck、Novartis、Pfizer、Takeda Pharmaceuticals、Bayer Healthcare、Eli Lilly and Company、GlaxoSmithKlineなどが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 新規治療開発への投資の増加

- NSCLCの有病率の増加

- 市場抑制要因

- 新興諸国における治療/薬剤の高コストと診断率の低さ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- がんタイプ別

- 扁平上皮がん

- 腺がん

- 大細胞がん

- 治療法別

- 化学療法

- 標的療法

- 免疫療法

- その他の治療法

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- F. Hoffmann-La Roche Ltd.

- AstraZeneca

- Bristol-Myers Squibb Company

- Merck & Co., Inc.

- Novartis AG

- Pfizer Inc.

- Takeda Pharmaceutical Company Limited

- Bayer AG

- Eli Lilly and Company

- GlaxoSmithKline plc.

- Sanofi

- Agennix AG

第7章 市場機会と今後の動向

The non-small cell lung cancer (NSCLC) market is expected to register a CAGR of 9.5% during the forecast period.

COVID-19 has significantly affected the growth of the non-small cell lung cancer market. For instance, as per clinicaltrials.gov, as of July 2021, more than 200 interventional studies were halted during the pandemic. This has slowed down the market growth during the pandemic. However, with the released restrictions and resumed services, the company has increased its focus on conducting clinical trials for the treatment of non-small cell lung cancer. For instance, in October 2022, Daiichi Sankyo, Inc. in partnership with AstraZeneca is conducting a Phase II clinical trial to evaluate the safety and efficacy of trastuzumab deruxtecan in HER2-mutated metastatic non-small cell lung cancer (NSCLC). Thus, with such activities, the studied market is expected to grow over the forecast period.

The growing number of patients suffering from non-small cell lung cancer and the increasing number of people with unhealthy habits such as smoking, tobacco and alcohol consumption, high dose of supplements, and sedentary lifestyle across the world are driving the market growth. For instance, according to the news published in December 2022, globally about 2.20 million new cases are among 11.4% of total thoracic tumor cases and this number is projected to double by 2025. Also, as per the data published by National Cancer Registry Programme (ICMR-NCRP), in December 2022, the number of lung cancer cases increased from 98,278 in 2020 to 1,03,371 in 2022, representing an increase of 5%. Thus, the high burden of lung cancer among the population has increased the demand for effective treatment options, which in turn is anticipated to fuel market growth.

Furthermore, the increasing company's focus on conducting R&D of effective drugs for the treatment of NSCLC and the increasing product approvals and various therapy designations are contributing to the market growth. For instance, in October 2022, GSK plc reported positive results from PERLA, the phase II trial of Jemperli (dostarlimab) plus chemotherapy in patients with metastatic non-squamous non-small cell lung cancer. Also, in June 2022, the European Commission approved Novartis's Tabrecta (capmatinib) as a monotherapy for the treatment of adults with advanced non-small cell lung cancer (NSCLC) who require systemic therapy following before treatment with immunotherapy and/or platinum-based chemotherapy. Similarly, in February 2022, the Medicines and Healthcare Products Regulatory Agency (MHRA) approved Genentech's Tecentriq to treat early-stage non-small cell lung cancer.

Moreover, the increasing investment by companies in developing effective therapies for treating patients with lung cancer is also expected to fuel market growth. For instance, in January 2023, DeuterOncology, a clinical-stage drug development company, closed EUR 5.65 million (USD 6.1 million) Series A financing round. This funding enables the company to initiate the phase I clinical study for its lead product DO-2, an improved MET kinase inhibitor that is being developed as a potential best-in-class targeted therapy for lung cancer. MET inhibitors have recently been approved for patients with Non-Small Cell Lung Cancer (NSCLC) harbouring the MET exon 14 skipping mutant.

Therefore, owing to the factors such as the high burden of non-small cell lung cancer, growing R&D activities, and product approvals, the studied market is anticipated to grow over the forecast period. However, the high cost of therapy or drugs and low diagnosis rate in developing countries is likely to impede the growth of non-small cell lung cancer over the forecast period.

Non-Small Cell Lung Cancer (NSCLC) Market Trends

Targeted Therapy Segment is Expected to Hold Significant Market Share Over the Forecast Period

The targeted drug therapy segment is anticipated to witness significant growth in the market over the forecast period owing to the factors such as the rising incidence of non-small cell lung cancer, and increasing company activities for developing novel treatments.

Targeted therapy drugs are often used to treat advanced lung cancers and are either used along with chemotherapy or used individually. Some of the major targeted therapy drugs to treat non-small cell lung cancer are Erlotinib (Tarceva), Gefitinib (Iressa), Afatinib (Gilotrif), Mobocertinib (Exkivity), Osimertinib (Tagrisso), and Dacomitinib (Vizimpro). These drugs targets mutated genes in the body and thereby avoid adverse effect on healthy cells. Investment by market players in the development of targeted therapy due to its advantages over standard chemotherapy and entry of these drugs in multiple countries across the world are likely to drive market growth. For instance, in October 2021, AUM Biosciences completed USD 27 million in a Series A funding round. These funds are used to advance the company's clinical-stage pipeline of precision and targeted cancer therapies.

According to an article published by MDPI, in December 2022, precision medicine's emergence has shed light on the treatment of non-small cell lung cancer, increasing the options available to patients with advanced NSCLC by targeting therapy on genetic and epigenetic markers. Additionally, as per an article published in the Journal of Hematology and Oncology, in June 2021, it has been observed that patients receiving targeted therapy showed a significant improvement in progression-free survival as compared to patients receiving chemotherapy. Also, as per the same source, for patients who underwent targeted therapy and had EGFR, ALK, ROS1, and BRAF mutations, the response rate ranged from 50% to 80%. Thus, the effectiveness of targeted drug therapy increases their adoption as well as demand for treating patients with NSCLC, hence propelling the segment growth.

Furthermore, the rising targeted therapy product approvals increase the availability of novel therapeutic drugs in the market which is also anticipated to augment the segment growth over the forecast period. For instance, in August 2022, AstraZeneca and Daiichi Sankyo's Enhertu, a targeted therapy, was approved in the United States for the treatment of adult patients with unresectable or metastatic non-small cell lung cancer whose tumors have activating HER2 (ERBB2) mutations. Also, in May 2021, the US FDA approved Rybrevant (amivantamab-vmjw) as the first targeted therapy treatment for adult patients with non-small cell lung cancer whose tumors have specific types of genetic mutations such as epidermal growth factor receptor (EGFR) exon 20 insertion mutations.

Therefore, owing to the factors such as the rising research activities by companies and institutions, growing adoption of targeted drug therapy treatment, and increasing product approvals, the studied segment is anticipated to grow over the forecast period.

North America is Expected to Have the Significant Market Share Over the Forecast Period

North America is expected to witness significant growth in the market over the forecast period owing to the factors such as the rising number of non-small cell lung cancer among the population and the presence of key players in the region focusing on launching and gaining approvals from the authorities. In addition, the increasing R&D investment by the players and huge healthcare spending in the region is also contributing to the market growth.

The increasing burden of NSCLC among the population is the key factor driving the market growth in the region. For instance, according to the 2023 statistics published by ACS, about 238,340 new cases of lung cancer are expected to be diagnosed in the United States in 2023. Additionally, as per 2022 statistics published by the Canadian Cancer Society, approximately 30,000 Canadians were diagnosed with lung and bronchus cancer, accounted for 13% of all new cancer cases, in Canada, in 2022. Thus, the high number of people suffering from lung cancer fuels the demand for effective treatment therapies such as chemotherapy, targeted therapy, and others. This is anticipated to propel the market growth over the forecast period.

Additionally, as per the data published by Statistics Canada, in January 2022, lung cancer is the most often diagnosed cancer and the leading cause of cancer-related deaths in Canada. About 50% of lung cancer cases are discovered at stage IV when the chance of survival is incredibly low (4% over five years). Thus, the high burden of lung cancer mainly discovered at the last stage increases the demand for chemotherapy sessions along with effective drugs, which in turn is expected to boost the market growth over the forecast period.

Furthermore, the growing company activities and increasing product approvals are also expected to increase the market growth over the forecast period. For instance, in August 2022, Health Canada approved Bristol Myers Squibb's OPDIVO 360 mg (injection for intravenous use) in combination with platinum-doublet chemotherapy every three weeks for three cycles for adult patients with resectable non-small cell lung cancer (NSCLC) in the neoadjuvant setting. Also, in January 2022, the US FDA granted Breakthrough Therapy Designation (BTD) to AbbVie's investigational telisotuzumab vedotin (Teliso-V) for the treatment of patients with advanced/metastatic epidermal growth factor receptor (EGFR) wild-type, nonsquamous non-small cell lung cancer (NSCLC) with high levels of c-Met overexpression whose disease has progressed on or after platinum-based therapy.

Therefore, due to the aforementioned factors, such as growing product approvals and product launches as well as the increasing number of non-small cell lung cancer cases, the studied market is expected to grow over the forecast period.

Non-Small Cell Lung Cancer (NSCLC) Industry Overview

The non-small cell lung cancer market is fragmented and competitive and consists of several major players. The companies are adopting various key business strategies such as collaborations, partnerships, new product launches and other initiatives to withhold their market position. Some of the key companies in the market are F. Hoffmann-La Roche, AstraZeneca, Bristol-Myers Squibb, Merck, Novartis, Pfizer, Takeda Pharmaceuticals, Bayer Healthcare, Eli Lilly and Company, and GlaxoSmithKline among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Investment for the Development of New Therapy

- 4.2.2 Increasing Prevalence of NSCLC

- 4.3 Market Restraints

- 4.3.1 High Cost of Therapy/Drugs and Low Diagnosis Rate in Developing Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Cancer Type

- 5.1.1 Squamous Cell Carcinoma

- 5.1.2 Adenocarcinoma

- 5.1.3 Large-cell Carcinoma

- 5.2 By Treatment

- 5.2.1 Chemotherapy

- 5.2.2 Targeted Therapy

- 5.2.3 Immunotherapy

- 5.2.4 Other Treatment Therapy

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 F. Hoffmann-La Roche Ltd.

- 6.1.2 AstraZeneca

- 6.1.3 Bristol-Myers Squibb Company

- 6.1.4 Merck & Co., Inc.

- 6.1.5 Novartis AG

- 6.1.6 Pfizer Inc.

- 6.1.7 Takeda Pharmaceutical Company Limited

- 6.1.8 Bayer AG

- 6.1.9 Eli Lilly and Company

- 6.1.10 GlaxoSmithKline plc.

- 6.1.11 Sanofi

- 6.1.12 Agennix AG