|

市場調査レポート

商品コード

1406206

対潜水艦戦(対潜戦):市場シェア分析、産業動向・統計、成長予測、2024年~2029年Anti-Submarine Warfare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 対潜水艦戦(対潜戦):市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

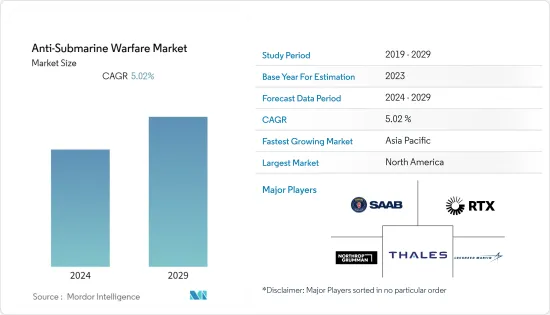

対潜水艦戦(対潜戦)市場は2024年に179億8,000万米ドルと評価され、2029年には229億8,000万米ドルに成長し、予測期間中のCAGRは5.02%を記録すると予測されています。

対潜水艦戦は、世界中の海軍部隊の戦略的速度と作戦の機敏性を守るために不可欠です。新技術の普及が、友軍と敵軍の双方の作戦計画と任務遂行に劇的な影響を与えているからです。対潜水艦戦は、水面下で活動する敵対勢力からの迅速かつステルス的な攻撃から海上資産を守るために不可欠となっています。ステルス潜水艦や無人海洋システムなど、先進的な海洋技術の開発に向けて進行中の研究開発は、ステルス潜水艦やその他の水中に潜った敵対的な船舶を探知することができる、強化されたレンジソナー・システムなどの対抗手段の開発への潜在的な投資を鼓舞するものと想定されています。しかし、対潜水艦戦システムの開発に伴う運用の複雑さと高コストが、市場成長の課題となる可能性があります。

対潜水艦戦市場の動向

潜水艦が予測期間中に最も高い成長を遂げる

潜水艦セグメントは、深度を変える能力と探知を助ける静粛性により、高いCAGRで成長すると予想されます。米国、英国、中国、インドなどの軍事大国は、海軍火力の増強に注力しており、国家安全保障に対する進化する脅威に対処するために、いくつかの艦隊の近代化と調達契約が進行中です。例えば、米国海軍は2022年12月、ジェネラル・ダイナミクス社に51億米ドルの契約を発注し、米国海軍の将来のコロンビア級潜水艦の重要部品の先行建造を実施しました。米国海軍は、耐用年数の延長と新規建造を組み合わせることで、2034年度までに355隻の目標を達成することを目指し、戦力構造拡大計画を積極的に実施しています。これに関連して、米国海軍は2021年にロサンゼルス級攻撃型潜水艦を受領しました。最近では、2023年3月にオーストラリアが米国と英国の協力を得て原子力潜水艦を建造する計画を発表し、「オークス」と呼ばれる協定に調印しました。プログラム全体の費用は2680億~3,680億米ドルと予測されています。同様の誘導プログラムは、予測期間中に潜水艦セグメントを推進すると想定されています。

予測期間中、アジア太平洋が最も高い成長を遂げる

米国とアジア太平洋の主権国家間の戦略的軍事同盟の強化、およびそれに続く軍事展開と軍事介入の強化は、複雑なシナリオをもたらし、既得権益を守るために中国などの地域諸国の防衛能力の急速な近代化を促しています。中国は、陸・空・海という3つのプラットフォームすべてにおいて軍事力を高めるため、その膨大な技術力をいくつかの兵器システムの独自開発に向けて投資してきました。中国はまた、偵察から機雷掃海、さらには敵艦への特攻に至るまで、幅広い任務を遂行できる長い耐久力を持ち、大型で賢く、比較的低コストのクルーレス潜水艦を開発しています。2023年8月、中国は南シナ海で対潜水艦演習を実施したが、これは近隣諸国やその同盟国との海洋における緊張が高まる中、その能力を磨く努力の一環です。

逆に、インド洋地域における中国人民解放軍海軍の関心の高まりを受けて、インド海軍はカモルタ級コルベットなどの対潜艦艇、ボーイングP-8ポセイドンなどの長距離海上偵察機、サーリュウ級哨戒艦などの艦船に急速に投資しています。オーストラリアはまた、スコルペン級をベースにしたバラクーダ級潜水艦6隻の導入により、潜水艦艦隊の増強も構想しています。このほかにもいくつかの計画がこの地域で進行中であり、予測期間中に注目される市場の成長見通しを強化しています。

対潜水艦戦産業の概要

対潜水艦戦市場は断片化されており、多くの世界的プレーヤーが市場に存在しています。市場の著名なプレーヤーとしては、Lockheed Martin Corporation、RTX Corporation、Northrop Grumman Corporation、Saab AB、THALESなどが挙げられます。長期契約を獲得し、世界のプレゼンスを拡大するため、プレーヤーは新しい海軍資産の調達に多額の投資を行っています。さらに、継続的な研究開発、パートナーシップ、事業拡大が、対潜水艦戦能力を備えた海軍戦闘システムの統合兵器技術や関連製品・ソリューションの精度と効率の向上を促進しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- システム

- センサー

- 電子支援手段

- 兵装

- プラットフォーム

- 潜水艦

- 水上艦

- ヘリコプター

- 海上哨戒機

- 無人システム

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- その他の地域

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- BAE Systems plc

- Lockheed Martin Corporation

- RTX Corporation

- THALES

- General Dynamics Corporation

- Saab AB

- L3Harris Technologies Inc.

- Northrop Grumman

- Safran

- Elbit Systems Ltd.

- Kongsberg Defense & Aerospace(Kongsberg Gruppen ASA)

- TERMA

第7章 市場機会と今後の動向

The anti-submarine warfare market was valued at USD 17.98 billion in 2024 and is projected to grow to USD 22.98 billion by 2029, registering a CAGR of 5.02% during the forecast period.

Anti-submarine warfare is critical for protecting the strategic speed and operational agility of naval forces around the world, as the proliferation of new technologies is dramatically affecting the operational planning and execution of missions of both friendly and hostile forces. With counter- and anti-denial strategies evolving as a crucial part of implemented maritime strategies of key naval forces, anti-submarine warfare has become vital in protecting maritime assets against a swift, stealthy attack from hostile forces operating below the surface of the water. The ongoing R&D toward the development of advanced maritime technologies, such as stealth submarines and unmanned marine systems, is envisioned to inspire potential investments in developing countermeasures, such as enhanced range-sonar systems, that can detect stealth submarines and other immersed hostile craft. However, operational complexities and high costs involved in the development of anti-submarine warfare systems may pose a challenge to market growth.

Anti-Submarine Warfare Market Trends

Submarines to WItness Highest Growth During the Forecast Period

The submarines segment is expected to grow at a high CAGR owing to their ability to change depth and their quietness, which aids detection. Military powerhouses, such as the United States, the United Kingdom, China, and India, are focused on augmenting their naval firepower, and several fleet modernization and procurement contracts are underway to address the evolving threats to their national security. For instance, in December 2022, the US Navy awarded a USD 5.1 billion contract to General Dynamics to conduct advanced construction of critical components for the US Navy's future Columbia-class submarines. The US Navy has been actively implementing force structure expansion plans, aiming to reach its 355-ship goal by FY 2034 through a mix of service life extensions and new construction. In this regard, in 2021, the US Navy received a Los Angeles-class attack submarine. Recently, in March 2023, Australia announced its plan to build a nuclear-powered submarine with the help of the US and UK and signed an agreement called the Aukus. The entire program is projected to cost between USD 268-368 billion. Similar induction programs are envisioned to drive the submarine segment during the forecast period.

Asia-Pacific to Witness Highest Growth During the Forecast Period

The strengthening of the strategic military alliances between the United States and several Asia-Pacific sovereign nations and subsequent reinforcement of military deployment and intervention has resulted in a complex scenario, urging rapid modernization of defense capabilities of regional countries, such as China, to safeguard their vested interests. China has invested its vast technological prowess toward the indigenous development of several weapon systems to foster its military prowess over all three platforms- land, air, and water. China is also developing large, smart, and relatively low-cost crewless submarines with long endurance capacity to perform a wide range of missions, from reconnaissance to mine placement to even suicide attacks against enemy vessels. In August 2023, China conducted anti-submarine exercises in the South China Sea as part of efforts to hone its capabilities amid rising maritime tensions with its neighbors and their allies.

On the contrary, the increasing interest of the Chinese People's Liberation Army Navy in the Indian Ocean region has led the Indian Navy to rapidly invest in anti-submarine ships, such as the Kamorta-class corvette, long-range maritime reconnaissance aircraft such as Boeing P-8 Poseidon and ships such as the Saryu-class patrol vessel, among others. Australia also envisions boosting its submarine fleet with the induction of six Barracuda class submarines based on the Scorpene-class. Several other programs are underway in the region, bolstering the growth prospects of the market in focus during the forecast period.

Anti-Submarine Warfare Industry Overview

The anti-submarine warfare market is fragmented, with many global players present in the market. Some of the prominent players in the market are Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, Saab AB, and THALES. In order to gain long-term contracts and expand their global presence, players are investing significantly in the procurement of new naval assets. Furthermore, continuous R&D, partnerships, and expansions are fostering the advancements in accuracy and efficiency of integrated weapon technologies and associated products and solutions of naval combat systems with anti-submarine warfare capabilities. For instance, in April 2021, THALES signed a contract with Lockheed Martin as a tier-one supplier for the delivery of up to 55 airborne anti-submarine warfare sonars. Likewise, in April 2022, Saab announced a new 10,000 sq. ft. Anti-Submarine Warfare (ASW) production facility in Rhode Island, the US. The facility will also house the Autonomous and Undersea Systems Division of Saab AB.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 System

- 5.1.1 Sensors

- 5.1.2 Electronic Support Measures

- 5.1.3 Armament

- 5.2 Platform

- 5.2.1 Submarines

- 5.2.2 Surface Ships

- 5.2.3 Helicopters

- 5.2.4 Maritime Patrol Aircraft

- 5.2.5 Unmanned Systems

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 Lockheed Martin Corporation

- 6.2.3 RTX Corporation

- 6.2.4 THALES

- 6.2.5 General Dynamics Corporation

- 6.2.6 Saab AB

- 6.2.7 L3Harris Technologies Inc.

- 6.2.8 Northrop Grumman

- 6.2.9 Safran

- 6.2.10 Elbit Systems Ltd.

- 6.2.11 Kongsberg Defense & Aerospace (Kongsberg Gruppen ASA)

- 6.2.12 TERMA