|

市場調査レポート

商品コード

1406196

照準ポッド(TGP):市場シェア分析、産業動向・統計、2024~2029年成長予測Targeting Pods - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 照準ポッド(TGP):市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 85 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

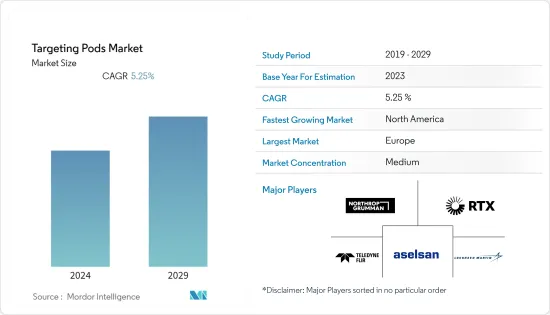

照準ポッド市場は、2024年に46億1,000万米ドルと評価され、2029年には59億5,000万米ドルに成長し、予測期間中のCAGRは5.25%を記録すると予測されています。

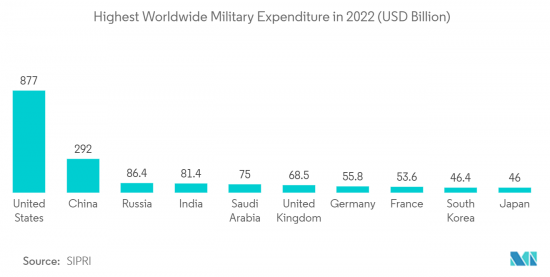

世界の軍事費支出額は過去数年間着実に増加しており、2022年には2兆2,400億米ドルに達しました。強化された国防支出の大部分は、新世代の軍用戦闘機やその他の航空資産の調達に向けられており、それによって長距離精密交戦を可能にすることによって敵対勢力に対する戦術的優位性を獲得するための統合照準ポッドの現在の能力を強化するための研究開発(R&D)が促進されています。予期せぬ景気変動により、防衛予算の抑制が予想されます。こうした混乱は市場の成長を制限する可能性があります。さらに、ステルス対応の第5世代航空機さえも探知できる長距離レーダーの開発は、その適用範囲を効果的に制限する可能性があります。

照準ポッド市場動向

戦闘機セグメントが予測期間中に市場を独占する

戦闘機は、空中戦と地上支援任務の両方に従事できるため、空中からの脅威に対する防御に不可欠です。米国、英国、中国、フランス、日本などの世界の軍事大国は、第5世代戦闘機と想定される第6世代戦闘機の独自開発を促進することで、現代の空中戦技術の大幅な再認識を達成しようと競い合っています。世界各国間の緊張が高まるにつれ、各国は空中戦能力の強化に努めてきました。いくつかの国は、既存の戦闘機をアップグレードしたり、老朽化した機体を先進機能を備えた新世代の航空機に置き換えたりしています。世界のいくつかの国による防衛費の増加に伴い、業界ではここ数年、戦闘機の大規模な調達と開発活動が示されています。

例えば、フランス政府は2022年2月、インドネシアがフランスのメーカー、ダッソー・アビエーションが製造するラファール戦闘機6機を購入することで合意したと発表しました。インドネシアは総額81億米ドルで42機のラファール戦闘機を発注する可能性が高いです。2021年3月、米国空軍は最初のF-15EXイーグルII戦闘機を引き渡しました。イーグルII計画は、老朽化したF-15Cの後継機として144機を納入することを目的としており、そのほとんどが航空州兵に配備されています。2021年度国防予算案によると、F-15EXの調達資金は12機で12億3,000万米ドルになります。米国国防総省は、2024年度には年間19機に達する生産スケジュールを予測しています。全144機の契約は229億米ドルと見積もられています。同様の長期契約は最近も締結されており、予測期間中に完了する予定であり、予測期間中に注目される市場の牽引役となることが想定されます。

北米が市場の優位性を維持

北米は、世界有数の国防支出国である米国の複数の開発により、予測期間中に最も高いCAGRを示すと予想されます。ストックホルム国際平和研究所(SIPRI)が発表したデータによると、米国は世界最大の国防支出国であり、2022年の国防予算は8,770億米ドルでした。これには、115機の回転翼航空機、85機のF-35A/B/C戦闘機、12機のF-15EX戦闘機、73機の兵站・支援機の調達予算が含まれています。これまでの 2022 会計年度の国防予算では、524億米ドルでした。さらに米国政府は2023年3月、国防総省(DoD)の2024年度予算要求案として、2023年度比260億米ドル増の8,420億米ドルを米国議会に提出しました。F-35、C-130Jハーキュリーズ、E-2Dアドバンスド・ホークアイ、KC-46ペガサス・タンカーといった戦闘機の大型受注に加え、軍用ヘリコプターの受注も増加しています。2022年5月、米国陸軍は次世代ヘリコプターの契約をテキストロンのベル部門に発注しました。米国国防軍は、空中戦の優位性を維持するため、高度な照準ポッドを装備し、要求される任務仕様に従って運用能力を維持する契約をいくつか結びました。

例えば、2022年12月、ロッキード・マーティンは、スナイパー包括的高度照準ポッド維持プログラムの一環として、米国空軍が軍用機で使用される電気光学照準システムを維持するのを支援するために、7年間、2億2,580万米ドルの契約を獲得しました。スナイパーは、航空兵が空対空および空対地目標を探知し、情報、監視、偵察データを収集するのに役立つセンサーで設計されています。同様の開拓が北米市場の成長を促進するものと思われます。

照準ポッド産業概要

照準ポッド市場は半固体化しており、Lockheed Martin Corporation、ASELSAN A.S.、RTX Corporation、Northrop Grumman Corporation、Teledyne FLIR LLCなど多くの著名な企業が存在することが特徴です。レーダー探知技術の進歩は長距離交戦を必要とするため、赤外線技術、熱冷却赤外線装置、前方指向赤外線(FLIR)技術などの未来型技術を統合する必要性を高めています。製品革新は市場プレーヤーに新たな成長機会を提供するものと思われます。しかし、防衛分野における厳しい安全政策や規制政策は、新規参入を制限すると予想されます。さらに、同市場は主に米国のような主要市場の経済状況の影響を受けます。したがって、景気後退局面では、契約が延期またはキャンセルされ、成長率が相対的に低下する可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム

- 戦闘機

- 無人戦闘空中システム

- 攻撃ヘリコプター

- 爆撃機

- フィット

- OEM

- レトロフィット

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- ASELSAN A.S.

- Teledyne FLIR LLC

- IAI

- L3Harris Technologies, Inc.

- Lockheed Martin Corporation

- MOOG Inc.

- Northrop Grumman Corporation

- Rafael Advanced Defense Systems Ltd.

- RTX Corporation

- THALES

- Ultra

第7章 市場機会と今後の動向

The targeting pods market was valued at USD 4.61 billion in 2024 and is projected to grow to USD 5.95 billion by 2029, registering a CAGR of 5.25% during the forecast period.

The value of military spending globally has grown steadily in the past years and reached USD 2.24 trillion in 2022. A large portion of the enhanced defense expenditure is directed toward the procurement of new-generation military combat aircraft and other aerial assets, thereby encouraging research and development (R&D) to enhance the current capabilities of the integrated targeting pods to attain tactical superiority over hostile forces by enabling long-range precision engagement. Unanticipated economic fluctuations are anticipated to deter defense budget sanctions during the upcoming period to divert resources for other vital needs. Such disruptions may restrict the growth of the market. Furthermore, the development of long-range radars that can even detect stealth-enabled fifth-generation aircraft can effectively limit the scope of their application.

Targeting Pods Market Trends

Combat Aircraft Segment to Dominate the Market During the Forecast Period

Combat aircraft are vital for protection against aerial threats as they can engage in both aerial warfare and ground-support missions. Global military powerhouses, such as the US, the UK, China, France, and Japan, are vying to achieve a profound reconceptualization of modern aerial warfare techniques by fostering the indigenous development of fifth-generation and the envisioned sixth-generation combat aircraft. As tensions between various global nations have increased, countries have been striving to enhance their aerial combat capabilities. Several nations have upgraded their existing fighter jets or replaced their aging fleet with newer-generation aircraft with advanced features. With the growth in defense spending by several nations around the world, the industry has witnessed large-scale procurement and development activities for fighter jets in the last few years. For instance, in February 2022, the French government announced that Indonesia had agreed to buy six Rafale fighter jets produced by the French manufacturer Dassault Aviation. In total, Indonesia will likely order 42 Rafale fighter jets in a USD 8.1 billion deal. In March 2021, the US Air Force took delivery of its first F-15EX Eagle II fighter. The Eagle II program is intended to deliver 144 aircraft to replace aging F-15Cs, most of which are in the Air National Guard. According to the FY2021 defense appropriations bill, the budget bill funded F-15EX procurement at USD 1.23 billion for 12 aircraft. US DoD projects a production schedule that would reach 19 per year in FY2024. The contract for all 144 jets is estimated at USD 22.9 billion. Similar long-term contracts have been awarded recently, which are scheduled to be completed during the forecast period and are envisioned to drive the market in focus during the forecast period.

North America to Continue its Dominance in the Market

North America is expected to showcase the highest CAGR during the forecast period owing to multiple developments in the US, which is one of the leading defense spenders globally. According to the data published by the Stockholm International Peace Research Institute (SIPRI), the US was the largest defense spender in the world, with a defense budget of USD 877 billion in 2022. Earlier, in the FY2022 defense budget, USD 52.4 billion was requested for aircraft and related systems, which includes the budget for the procurement of 115 rotary-wing aircraft, 85 F-35A/B/C fighter jets, 12 F-15EX jets, 73 logistics and support aircraft. Furthermore, in March 2023, the US government submitted to US Congress a proposed FY 2024 Budget request of USD 842 billion for the Department of Defense (DoD), an increase of USD 26 billion over FY 2023. In addition to the large-scale orders for fighter jets like F-35, C-130J Hercules, E-2D Advanced Hawkeye, and KC-46 Pegasus Tanker, the orders for military helicopters have also increased. In May 2022, the US Army awarded a contract for its next-generation helicopter to Textron's Bell unit, which will likely replace the Black Hawk utility helicopter. To retain its aerial dominance, the US defense forces awarded several contracts to equip its aerial combat fleet with sophisticated targeting pods and maintain their operational capabilities as per required mission specifications. For instance, in December 2022, Lockheed Martin received a seven-year, USD 225.8 million contract to help the US Air Force maintain an electro-optical targeting system used by military aircraft as a part of the Sniper Comprehensive Advanced Targeting Pod sustainment program. The Sniper is designed with sensors that work to help airmen detect air-to-air and air-to-surface targets as well as to collect intelligence, surveillance, and reconnaissance data. Similar developments are envisioned to drive market growth in North America.

Targeting Pods Industry Overview

The targeting pods market is semi-consolidated and is marked by the presence of many prominent players, such as Lockheed Martin Corporation, ASELSAN A.S., RTX Corporation, Northrop Grumman Corporation, and Teledyne FLIR LLC. The advancement in radar detection technologies has necessitated long-range engagement, hence bolstering the need to integrate futuristic technologies, such as infrared technologies, thermally cooled infrared devices, and forward-looking infrared (FLIR) technology. Product innovation is envisioned to offer new growth opportunities for market players. However, stringent safety and regulatory policies in the defense sector are expected to restrict the entry of new players. Furthermore, the market is primarily influenced by the prevalent economic conditions in dominant markets like the United States. Hence, during an economic downturn, contracts may be subjected to deferral or cancelation and lead to a relatively slower growth rate, which, in turn, can adversely affect the market dynamics and expose the players to financial duress.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Combat Aircraft

- 5.1.2 Unmanned Combat Aerial Systems

- 5.1.3 Attack Helicopters

- 5.1.4 Bombers

- 5.2 Fit

- 5.2.1 OEM

- 5.2.2 Retrofit

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 ASELSAN A.S.

- 6.2.2 Teledyne FLIR LLC

- 6.2.3 IAI

- 6.2.4 L3Harris Technologies, Inc.

- 6.2.5 Lockheed Martin Corporation

- 6.2.6 MOOG Inc.

- 6.2.7 Northrop Grumman Corporation

- 6.2.8 Rafael Advanced Defense Systems Ltd.

- 6.2.9 RTX Corporation

- 6.2.10 THALES

- 6.2.11 Ultra