|

|

市場調査レポート

商品コード

1406099

ポリウレア:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Polyurea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリウレア:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

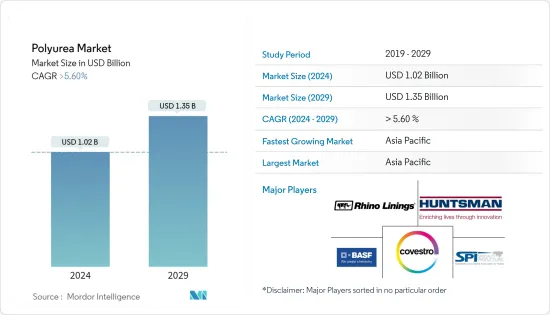

ポリウレアの市場規模は2024年に10億2,000万米ドルと推定され、2029年には13億5,000万米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは5.60%以上で成長する見込みです。

COVID-19の大流行により、自動車、建設などの業界が封じ込め対策と経済的混乱により生産の遅れを余儀なくされたため、市場は生産とモビリティの減速にマイナスの影響を受けました。現在、市場はパンデミックから回復しています。市場は2022年にはパンデミック以前の水準に達し、今後も安定した成長が見込まれます。

市場を牽引する主な要因のひとつは、建設業界からのポリウレア需要の拡大です。

しかし、ポリウレアの原料価格の変動が市場の成長を妨げると予想されます。

食品産業や飲料水用途でのポリウレアの使用増加は、今後数年間、市場にとって好機となる可能性が高いです。

アジア太平洋地域は、中国やインドなどの国々からの消費が最も多く、市場を独占すると予想されます。

ポリウレアの市場動向

建設業界からのポリウレア需要の高まり

- ポリウレアはエラストマーの一種で、イソシアネート成分と合成樹脂ブレンドの反応生成物から高度開発重合によって得られます。

- ポリウレアは、パイプやパイプラインを腐食や外的影響から保護するのに理想的であり、パイプラインの断熱材である鉄と発泡ポリウレタンの両方に適用できます。

- ポリウレアの鉄とコンクリート両方の断熱能力と高い耐久性により、長年にわたって改修の必要がない安全な構造物を実現できます。

- アジア太平洋地域の建設セクターは世界最大の規模を誇り、中国とインドにおける住宅建設市場の拡大により、住宅はアジア太平洋地域で最も高い成長が見込まれています。

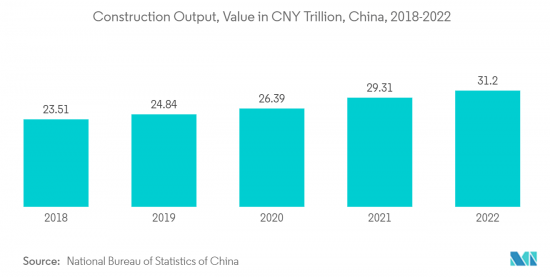

- また、中国国家統計局によると、中国の建設生産高は2022年にピークを迎え、その額は約31兆2,000億人民元(4兆6,100億米ドル)に達します。その結果、これらの要因が市場の需要を増加させる傾向にあります。

- インドは商業セクターを拡大しています。同国ではいくつかのプロジェクトが進行しています。例えば、2022年第1四半期には、9億米ドル相当のCommerzIII商業オフィス複合施設の建設が始まった。このプロジェクトでは、ムンバイのゴレガオンに43階建ての商業施設を建設します。このプロジェクトは2027年第4四半期に完成する予定で、予測期間中の市場成長に寄与します。

- さらに米国では、米国国勢調査局によると、2022年の民間建設額は1兆4,342億米ドルとなり、2021年の1兆2,795億米ドルを11.7%上回った。2022年の住宅建設支出は8,991億米ドルで、2021年の7,937億米ドルから13.3%増加し、市場の成長を支えています。

- また、ドイツは欧州最大の建設産業国です。同国の建設産業は緩やかな成長を続けており、その主な要因は新設住宅建設件数の増加です。同国には欧州大陸最大の建築ストックがあり、当面はこの傾向が続くと予想されます。ドイツは、持続可能なエネルギーシステムへの移行を進める一環として、2050年までに建築ストックをほぼ気候変動に左右されないものにすることを目指しています。

- したがって、上記の要因から、建設業界からのポリウレアの用途は予測期間中支配的となる可能性が高いです。

市場を独占するアジア太平洋地域

- 予測期間中、アジア太平洋地域がポリウレア市場を独占するとみられます。中国やインドのような発展途上国における人口増加、自動車部門、建設活動とともに、ポリウレアの需要が高まっていることが、この地域のポリウレア需要を牽引すると予想されます。

- ポリウレアの最大生産国はアジア太平洋地域です。ポリウレアの生産における大手企業には、BASF SE、Covestro AG、Huntsman International LLCなどがあります。

- インド政府は、自動車製造を「メイク・イン・インディア」構想の主要な原動力とすることを目指しており、これが市場の成長を促進すると予想されています。インド自動車工業会(SIAM)によると、2022年にインドで販売された乗用車は379万台で、2021年に販売された乗用車と比較して約23%の成長率を示しています。

- 2023-2024年度予算で、インド財務相は住宅建設促進のために27億インドルピー(約33億9,000万米ドル)の割り当てを発表しました。この配分は前年度に比べ10%近く増加しました。これは住宅建設に大きな弾みをつけると思われます。

- 同市場は、同地域の建設部門の成長によって大きく押し上げられます。中国政府は、経済成長全体を押し上げるため、国内の建設部門全体への投資強化に注力しています。例えば、インフラ建設への融資を増やすための最近の動きには、政策銀行の融資比率を1,200億米ドル引き上げることが含まれます。政府はまた、地方政府がインフラ建設資金を調達するための特別公債枠のうち、最大約2,200億米ドルを地方政府が使用できるようにすることも検討しています。

- 日本では、国土交通省によると、2022年に約85万9,500戸の住宅開発が開始され、前年比0.4%増となった。

- 上記の要因から、アジア太平洋地域のポリウレア市場は調査期間中に大きく成長すると予測されます。

ポリウレア産業の概要

ポリウレア市場は部分的に統合されています。調査市場の主要企業(順不同)には、BASF SE、Huntsman International LLC、Covestro AG、Rhino Linings Corporation、Speciality Products Inc.などが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設業界からのポリウレア需要の拡大

- 自動車産業からの需要拡大

- その他の促進要因

- 抑制要因

- 原料価格の変動

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模)

- 化学構造

- 芳香族

- 脂肪族

- タイプ

- ホットポリウレア

- コールドポリウレア

- 製品

- ライニング

- コーティング

- シーラント

- エンドユーザー産業

- 建設

- 塗料・コーティング

- 自動車

- 工業

- 海運

- その他のエンドユーザー産業(運輸など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Armorthane

- CITADEL FLOORS

- Covestro AG

- Dorf Ketal

- Elastothane

- Huntsman International LLC

- Lonza

- Rhino Linings Corporation

- SATYEN POLYMERS PVT. LTD.(TEVO)

- Speciality Products Inc.

- Teknos Group

第7章 市場機会と今後の動向

- 食品産業と飲料水用途におけるポリウレアの使用増加

- その他の機会

The Polyurea Market size is estimated at USD 1.02 billion in 2024, and is expected to reach USD 1.35 billion by 2029, growing at a CAGR of greater than 5.60% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as automotive, construction, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

One of the main factors driving the market is the growing demand for polyurea from the construction industry.

However, volatility in the raw material price of polyurea is expected to hinder the growth of the market studied.

The increasing use of polyurea in the food industry and drinking water application is likely to act as an opportunity for the market studied in the coming years.

The Asia-Pacific region is expected to dominate the market with the largest consumption from countries such as China and India.

Polyurea Market Trends

Growing Demand for Polyurea from the Construction Industry

- Polyurea is a kind of elastomer that results from the reaction product of an isocyanate component and synthetic resin blend through advanced development polymerization.

- Polyurea is ideal for protecting pipes and pipelines against corrosion and external influences and can be applied to both steel and polyurethane foam, which is the thermal insulation of the pipeline.

- The ability of polyurea to insulate both steel and concrete and high durability allows for secure structures without the need for renovation for many years.

- The construction sector in the Asia-Pacific region is the largest in the world, and the highest growth for housing is expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India.

- Also, according to the National Bureau of Statistics of China, China's construction output peaked in 2022 at a value of about CNY 31.20 (USD 4.61 trillion). As a result, these factors tend to increase the market demand.

- India is expanding its commercial sector. Several projects have been going on in the country. For instance, the CommerzIII Commercial Office Complex construction worth USD 900 million started in Q1 2022. The project involves the construction of a 43-story commercial office in Goregaon, Mumbai. The project is expected to be completed in Q4 2027, thus benefitting the market growth during the forecast period.

- Further, in the United States, according to the US Census Bureau, the value of private construction in 2022 stood at USD 1,434.2 billion, 11.7% higher than the USD 1,279.5 billion in 2021. Residential construction spending in 2022 was USD 899.1 billion, up 13.3% from USD 793.7 billion in 2021, thus supporting the market growth.

- In addition, Germany has the largest construction industry in Europe. The country's construction industry has been growing slowly, which is majorly driven by the increasing number of new residential construction activities. The country is home to the continent's largest building stock and is expected to continue in the foreseeable future. Germany aims to have an almost climate-neutral building stock by 2050 as part of its ongoing transition to a sustainable energy system.

- Hence, owing to the above-mentioned factors, the application of polyurea from the construction industry is likely to dominate during the forecast period.

The Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for polyurea during the forecast period. The rising demand for polyurea, along with the growing population, automotive sector, and construction activities in developing countries like China and India, is expected to drive the demand for polyurea in this region.

- The largest producers of polyurea are located in the Asia-Pacific region. Some of the leading companies in the production of polyurea are BASF SE, Covestro AG, Huntsman International LLC, and others.

- The Indian government aims to make automobile manufacturing the main driver of the 'Make in India' initiative, which is anticipated to enhance the growth of the market studied. According to the Society of Indian Automobile Manufacturers (SIAM), a total of 3.79 million passenger vehicles were sold in India in 2022, witnessing a growth rate of around 23% compared to the passenger vehicles sold in the year 2021.

- In the budget 2023-2024, the Indian finance minister announced an allocation of INR 2.7 lakh crore (~USD 3.39 billion) for boosting housing construction. This allocation increased by nearly 10% as compared to the previous year. This will provide a significant boost to housing construction.

- The market is significantly boosted by the growing construction sector in the region. The Chinese government is focusing on enhancing investments across the construction sector in the country to boost overall economic growth. For instance, recent moves to increase financing for infrastructure construction include a USD 120 billion increase in the lending ratio of policy banks. The government is also considering allowing local governments to spend up to about USD 220 billion of the special bond quota through which local governments fund infrastructure construction.

- In Japan, according to the Ministry of Land, Infrastructure, Transport, and Tourism (MLIT) Japan, in 2022, approximately 859.5 thousand housing developments were initiated in Japan, which represented an increase of 0.4% compared to the previous year.

- Owing to the above-mentioned factors, the market for polyurea in the Asia-Pacific region is projected to grow significantly during the study period.

Polyurea Industry Overview

The polyurea market is partially consolidated in nature. The major players in the studied market (not in any particular order) include BASF SE, Huntsman International LLC, Covestro AG, Rhino Linings Corporation, and Speciality Products Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand of Polyurea from Construction Industry

- 4.1.2 Growing Demand from Automotive Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatility in Raw Material Price

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Chemical Structure

- 5.1.1 Aromatic

- 5.1.2 Aliphatic

- 5.2 Type

- 5.2.1 Hot Polyurea

- 5.2.2 Cold Polyurea

- 5.3 Product

- 5.3.1 Lining

- 5.3.2 Coating

- 5.3.3 Sealants

- 5.4 End-user Industry

- 5.4.1 Construction

- 5.4.2 Paints and Coatings

- 5.4.3 Automotive

- 5.4.4 Industrial

- 5.4.5 Maritime

- 5.4.6 Other End-user Industries (Transportation, Etc.)

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Armorthane

- 6.4.2 CITADEL FLOORS

- 6.4.3 Covestro AG

- 6.4.4 Dorf Ketal

- 6.4.5 Elastothane

- 6.4.6 Huntsman International LLC

- 6.4.7 Lonza

- 6.4.8 Rhino Linings Corporation

- 6.4.9 SATYEN POLYMERS PVT. LTD. (TEVO)

- 6.4.10 Speciality Products Inc.

- 6.4.11 Teknos Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Use of Polyurea in Food Industry and Drinking Water Application

- 7.2 Other Opportunities