|

|

市場調査レポート

商品コード

1689923

エンコーダ:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Encoder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エンコーダ:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 171 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

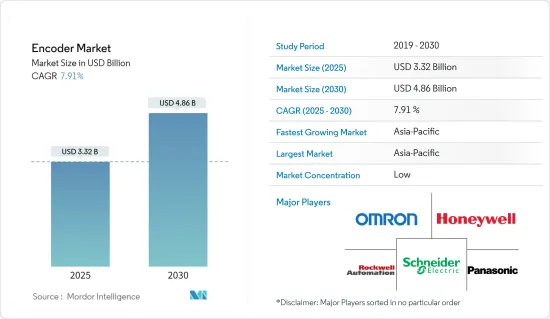

エンコーダの市場規模は2025年に33億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.91%で、2030年には48億6,000万米ドルに達すると予測されます。

同市場は、データセンターから通信まで、さまざまな用途でエンコーダ需要が増加しているため、急成長を遂げています。

主なハイライト

- ハイエンド自動化のニーズとインダストリー4.0が市場成長の主な要因です。インダストリー4.0とは、第4次産業革命のことで、工場の自動化が従来の情報技術システムによって制御される製造工場から、ビッグデータ解析と生産プロセスの仮想化を可能にするクラウドベースのインフラへと移行する新しい世界のことです。

- 世界の多くの国々が、インダストリー4.0の導入を強化する戦略的イニシアチブを開発することで、インダストリー4.0に積極的に対応しています。例えば、SAMARTH Udyog Bharat 4.0は、インド政府重工業・公営企業省によるインダストリー4.0イニシアチブであり、インド資本財セクターの競争力強化に関するスキームの下にあります。UNCTADによると、中国と米国はインダストリー4.0技術への投資と能力においてリーダー的存在です。中国と米国は最大のデジタルプラットフォームの本拠地であり、時価総額の90%を占めています。

- さらに、エンコーダはモーションコントロールアプリケーションの中心的存在です。エンコーダは、位置、速度、方向をコントローラやドライブにフィードバックし、ドライブシステムの精度と信頼性を向上させます。技術が進歩するにつれて、エンコーダも進歩し、通信とネットワークにおける最新の開発を取り入れ、多様なモーションコントロールアプリケーションでエンジニアが直面する課題を解決するツールを提供しています。

- エンコーダの最も大きな制限の1つは、エンコーダがそれなりに複雑で、デリケートな部品で構成されていることです。そのため、機械的な酷使に対する耐性が低く、許容温度も制限されます。1200℃を超えても使用できる光学式エンコーダを見つけるのは難しいと思われます。これに加えて、機能安全認証の取得は困難であり、モーションコントロールエンコーダの機能に関連するエラーが発生する可能性があるため、モーションコントロールの設計において重要な機能安全問題に対する関心が高まっていることも、市場の成長にとって顕著な制限となっています。このような制約は、市場の成長にとって課題となります。

- さらに、パンデミックは自動化の重要性を浮き彫りにし、製造業における遠隔用途は自動化への投資を増加させ、様々なタイプのエンコーダの需要を押し上げる可能性があります。eコマースの台頭と倉庫や物流などの分野における自動化は、これらの用途におけるエンコーダの需要を促進すると予想されます。

エンコーダ市場の動向

産業分野が市場の主要シェアを占めると予測

- エンコーダの使用は、リニア測定、レジストレーションマークタイミング、ウェブテンション、バックストップゲージング、搬送、充填などの複数の産業用途で急速に拡大しています。最も標準的な用途は、電気モーターのモーションコントロールにフィードバックを提供することです。産業部門では、かなりの電力が電動モーターに使われており、そのほとんどにエンコーダが組み込まれています。

- ロボットは、特に溶接、マテリアルハンドリング、組立、研削などの作業において、応用分野が拡大しています。通常、人間が監視したり監督したりすることは限られているため、これらのロボットには動きをガイドする信頼性の高いエンコーダが必要です。ロボット工学では、エンコーダはロボットアームや移動ロボットの位置や動きを制御するために不可欠です。

- IFRのWorld Robotics 2023レポートによると、世界の工場には約55万3,052台の産業用ロボットが設置されています。設置された産業用ロボット全体のうち、新たに導入されたロボットの73%がアジア、15%が欧州、10%が南北アメリカに設置されました。中国、日本、米国、韓国、ドイツは、電気・電子、自動車、金属・機械などの主要産業において、産業用ロボットの年間導入台数が多い上位国のひとつです。このような産業における自動化導入の増加は、市場におけるエンコーダの需要をさらに促進すると予想されます。

- 産業自動化が急速に勢いを増すにつれ、様々な産業用途におけるエンコーダの需要が高まっています。そのため、この需要に対応するため、市場で事業を展開するベンダーは、産業用途向けの新しいエンコーダを投入しています。例えば、SICKは2023年6月、油圧シリンダーのピストン位置の高精度検出や機械の直線運動の監視に使用される新しいリニアエンコーダ製品ラインを発表しました。この新しいリニアエンコーダ製品ラインは、数え切れないほどの産業用途に柔軟性を提供します。

アジア太平洋地域が最速の成長を記録する見込み

- 中国、インド、その他の東南アジア諸国などの国々では、急速な工業化と製造基盤の拡大が進んでおり、ロボット、CNC機械、コンベアや包装機械などの様々な産業機器の生産性を向上させるために使用される組立ラインや工場機械において、正確な位置決めと制御を行う産業用途に使用されるエンコーダの需要が急増しています。

- アジア太平洋全域の政府は、自動化とインダストリー4.0イニシアチブを積極的に推進しています。これには、外国からの技術輸入への依存を減らし、イノベーションに投資する中国のメイド・イン・チャイナ2025や、生産パラダイムの技術的変革を通じて自立を提唱するインドの製造業のための国家戦略が含まれます。このような取り組みにより、自動化が進み産業活動が活性化し、様々な用途でエンコーダのニーズが高まると予想されます。

- さらに、自動車産業の急速な拡大は、予測期間中にエンコーダの需要を促進すると思われます。この地域には、世界の主要な自動車メーカーが進出しています。エンコーダは、自動車部品や組立ラインの製造工程でますます使用されるようになっています。同地域では電気自動車の生産台数が増加しており、先進的なモーター制御システムやバッテリー管理システムにエンコーダが不可欠であるため、エンコーダの需要を牽引すると予想されます。

- 2024年1月、Suzuki Motor Corp.はインドのグジャラート州での事業を拡大し、自動車生産能力をほぼ倍増させる計画を発表しました。同工場は2028年度に操業を開始する予定で、生産能力は年間400万台に拡大する見込みです。このような自動車製造工場の拡大は、自動化の促進、生産ラインの精密制御、品質管理システムの強化、サプライチェーン管理の最適化を必要とし、エンコーダの需要を促進します。

エンコーダ産業の概要

エンコーダ市場には、Omron Corporation、Honeywell、Heidenhain GmbH、Baumer Group、Posital Fraba Inc.など様々な企業が参入しています。各社は大規模な顧客基盤を有しているため、エンコーダの大量生産が可能であり、センサー市場においてより良い利益と規模の経済を確保するための重要な要因となっています。強力なブランドは優れた性能の代名詞であるため、老舗企業が優位に立つと予想されます。市場に浸透し、先進的な製品を提供できることから、競争企業間の敵対関係は今後も続くと予想されます。

2023年11月、世界のセンサーとエンコーダのソリューションメーカーであるBaumerは、移動機械や屋外環境などの過酷な用途で安全性と性能を発揮するように設計されたアブソリュートエンコーダEAM580RSを発売しました。さらに、この安全認証エンコーダは、費用対効果が高く、実装が容易な安全な自動化を提供します。この磁気式セーフティエンコーダは、厳しい屋外環境から保護するためにステンレススチールケースを備え、振動や衝撃などの産業要因に耐えることができます。

エンコーダメーカーのDynaparは2023年8月、新しいプログラマブル中空軸エンコーダであるPulseIQテクノロジー搭載のHS35iQエンコーダを発表しました。これは、色分けされたLEDとデジタル出力を備えた自己診断型フィードバック装置で、重機械用途のOEMやエンドユーザーに、エンコーダの健全性ステータスにリアルタイムでアクセスし、故障したエンコーダのトラブルシューティングを行う新しい方法を提供します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 先進自動車システムにおける高い採用率

- 産業自動化の需要の高まり

- 市場の課題

- 過酷な条件下での機械的故障

第6章 市場セグメンテーション

- タイプ別

- ロータリーエンコーダ

- リニアエンコーダ

- 技術別

- 光学式

- 磁気式

- 光電式

- その他

- エンドユーザー産業別

- 自動車

- 電子

- 繊維

- 印刷機械

- 産業

- 医療

- その他

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Omron Corporation

- Honeywell International

- Schneider Electric

- Rockwell Automation Inc.

- Panasonic Corporation

- Baumer Group

- Renishaw PLC

- Dynapar Corporation(Fortive Corporation)

- FAULHABER Drive Systems

- Pepperl+Fuchs International

- Hengstler GMBH(Fortive Corporation)

- Maxon Motor AG

- Dr. Johannes Heidenhain GmbH

- POSITAL FRABA Inc.(FRABA BV)

- Sensata Technologies

第8章 投資分析

第9章 市場の将来展望

The Encoder Market size is estimated at USD 3.32 billion in 2025, and is expected to reach USD 4.86 billion by 2030, at a CAGR of 7.91% during the forecast period (2025-2030).

The market is witnessing rapid growth due to the increasing demand for encoders in multiple applications, from data centers to telecommunication.

Key Highlights

- The need for high-end automation and Industry 4.0 are the major factors driving the growth of the market. Industry 4.0 describes the fourth industrial revolution, a new world where factory automation moves beyond manufacturing plants controlled by conventional information technology systems to a cloud-based infrastructure that permits big data analytics and the virtualization of production processes.

- Many countries worldwide have positively responded to Industry 4.0 by developing strategic initiatives to strengthen its implementation. For instance, SAMARTH Udyog Bharat 4.0 is an Industry 4.0 initiative of the Ministry of Heavy Industry & Public Enterprises, Government of India, under its scheme on Enhancement of Competitiveness in the Indian Capital Goods Sector. According to the UNCTAD, China and the United States are leaders in investment and capacity in Industry 4.0 technologies. They are home to the largest digital platforms, accounting for 90% of the market capitalization.

- Furthermore, encoders are central to motion control applications. They can offer feedback on position, speed, and direction to a controller or drive to increase the accuracy and reliability of a drive system. As technology advances, so do encoders, incorporating the latest developments in communications and networking and offering engineers tools to solve challenges they face across a diverse array of motion control applications.

- One of the most significant limitations of encoders is that they can be reasonably complex and comprise some delicate parts. This makes them less tolerant of mechanical abuse and restricts their allowable temperature. One would be hard-pressed to find an optical encoder that will survive beyond 1200C. In addition to this, rising concern about functional safety issues, which is of significant importance in any motion control design, is also a notable limitation for the growth of the market as the acquisition of functional safety certification can be arduous, and there can be some errors associated with the functionality of the motion control encoders. Such limitations pose a challenge to the market's growth.

- Furthermore, the pandemic highlighted the importance of automation, and remote applications in manufacturing resulted in increased investments in automation, potentially boosting demand for various types of encoders. The rise of e-commerce and automation in sectors like warehousing and logistics is anticipated to drive demand for encoders in these applications.

Encoder Market Trends

The Industrial Sector is Expected to Hold a Major Share in the Market

- The use of encoders is rapidly growing in multiple industrial applications, such as linear measurement, registration mark timing, web tensioning, backstop gauging, conveying, and filling. The most standard application is providing feedback on the motion control of electric motors. In the industrial sector, a significant amount of electricity goes to electric power motors, most of which incorporate encoders.

- Robots are experiencing a growing number of application areas, especially for operations like welding, material handling, assembly, and grinding. Since there is typically limited human oversite or monitoring, these robots must have reliable encoders to help guide their movement. In robotics, encoders are essential for controlling robotic arms' and mobile robots' position and movement.

- According to IFR's World Robotics 2023 report, about 553,052 industrial robots were installed in factories across the world. Among the total installed industrial robots, 73% of all newly deployed robots were installed in Asia, 15% in Europe, and 10% in the Americas. China, Japan, the United States, the Republic of Korea, and Germany are among the top countries with a greater number of annual installations of industrial robots in key industries, including electrical/electronics, automotive, and metal and machinery. Such a rise in the adoption of automation in industries is expected to further fuel the demand for encoders in the market.

- As industrial automation rapidly gains momentum, the demand for encoders in various industrial applications is growing. Thus, to cater to this demand, vendors operating in the market are introducing new encoders for industrial applications. For instance, in June 2023, SICK launched a new linear encoder product family for high-precision detection of piston positions in hydraulic cylinders and monitoring linear movements in machines. This new linear encoder product line offers flexibility for countless industrial applications.

Asia-Pacific is Expected to Register the Fastest Growth

- Countries like China, India, and other Southeast Asian countries are experiencing rapid industrialization and expansion of their manufacturing bases, translating to a surge in demand for encoders used in industrial automation for precise positioning and control in robots, CNC machines, and assembly lines and factory machinery that used to improve productivity in various industrial equipment like conveyors and packaging machines.

- Governments across Asia-Pacific are actively promoting automation and Industry 4.0 initiatives, including China's "Made in China 2025" to reduce dependence on foreign technology imports and invest in innovations and India's "National Strategy for Manufacturing" to advocate self-reliance through the technological transformation of the production paradigm. Such initiatives are expected to fuel industrial activities with increased use of automation, creating the need for encoders in various applications.

- Moreover, the rapid expansion of the automotive industry is likely to propel the demand for encoders during the forecast period. The region has the presence of major global automotive manufacturers. Encoders are increasingly used in the manufacturing processes of automotive components and assembly lines. The rise in the production of electric vehicles in the region is expected to drive demand for encoders, as they are essential in advanced motor control and battery management systems.

- In January 2024, Suzuki Motor Corp. announced its plan to expand its operations in Gujarat, India, to nearly double its automotive manufacturing capacity, seeking to roll 4 million units off the assembly lines annually. The plant is planned to start operations in fiscal 2028 and is expected to increase its production capacity to 1 million units annually. Such growth in the automotive manufacturing plant expansion drives demand for encoders by necessitating increased automation, precision control in production lines, enhanced quality control systems, and optimized supply chain management.

Encoder Industry Overview

The encoder market comprises various players, such as Omron Corporation, Honeywell, Heidenhain GmbH, Baumer Group, and Posital Fraba Inc. Companies have the advantage of a large client base, enabling them to produce large volumes of encoders, a key factor in ensuring better profits and economies of scale in the sensor market. As strong brands are synonymous with good performance, long-standing players are expected to have the upper hand. Owing to their market penetration and the ability to offer advanced products, the competitive rivalry is expected to continue to be high.

In November 2023, Baumer, a global sensor and encoder solutions manufacturer, launched the absolute encoder EAM580RS, designed to deliver safety and performance in harsh applications, including mobile machinery and outdoor environments. Additionally, this safety-certified encoder would provide safe automation, which is cost-effective and easy to implement. The magnetic safety encoder has a stainless-steel casing for its protection from harsh outdoor environments, and it is able to withstand industrial factors, like vibrations and shock.

In August 2023, Dynapar, a manufacturer of encoders, launched HS35iQ Encoder with PulseIQ Technology, which is a new programmable hollow shaft encoder. This is a self-diagnosing feedback device with color-coded LEDs and digital output and offers a new way for OEM and end-users in heavy-duty machine applications to troubleshoot faulty encoders with access to encoder health status in real time.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Adoption in Advanced Automotive Systems

- 5.1.2 Rising Demand For Industrial Automation

- 5.2 Market Challenges

- 5.2.1 Mechanical Failures in Harsh Conditions

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Rotary Encoder

- 6.1.2 Linear Encoder

- 6.2 By Technology

- 6.2.1 Optical

- 6.2.2 Magnetic

- 6.2.3 Photoelectric

- 6.2.4 Other Technologies

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Electronics

- 6.3.3 Textile

- 6.3.4 Printing Machinery

- 6.3.5 Industrial

- 6.3.6 Medical

- 6.3.7 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Omron Corporation

- 7.1.2 Honeywell International

- 7.1.3 Schneider Electric

- 7.1.4 Rockwell Automation Inc.

- 7.1.5 Panasonic Corporation

- 7.1.6 Baumer Group

- 7.1.7 Renishaw PLC

- 7.1.8 Dynapar Corporation (Fortive Corporation)

- 7.1.9 FAULHABER Drive Systems

- 7.1.10 Pepperl+Fuchs International

- 7.1.11 Hengstler GMBH (Fortive Corporation)

- 7.1.12 Maxon Motor AG

- 7.1.13 Dr. Johannes Heidenhain GmbH

- 7.1.14 POSITAL FRABA Inc. (FRABA BV)

- 7.1.15 Sensata Technologies