|

市場調査レポート

商品コード

1406049

塞栓防止システム - 市場シェア分析、産業動向・統計、2024年~2029年成長予測Embolic Protection Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 塞栓防止システム - 市場シェア分析、産業動向・統計、2024年~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

調査対象の塞栓防止システム市場は、予測期間中にCAGR 8.6%で成長すると予測されました。

COVID-19は、パンデミックの初期波において多くの神経血管および心臓血管手術が延期またはキャンセルされたため、塞栓防止システム市場に大きな影響を与えました。例えば、2021年2月に発表されたPubMedの論文によると、神経患者はより頻繁な入院を必要とし、退院後に障害を負う可能性が高いため、患者は世界の封鎖のために定期的なモニタリング、手術、神経問題の治療を受けることが困難となり、調査対象市場に大きな影響を与えました。現在、COVID-19関連の規制が緩和され、塞栓防止システムの需要が高まっているため、市場はパンデミック前の環境を取り戻しつつあります。また、神経血管合併症や心臓合併症の増加、塞栓防止システムの採用増加により、市場は今後数年間で成長が見込まれています。

心血管疾患や神経血管疾患の有病率の上昇、低侵襲手術に対する需要の増加などの要因が、予測期間中の市場成長を後押しすると予想されます。

市場成長の主な要因は、心血管および神経血管疾患の有病率の上昇です。例えば、Global Stroke Fact Sheet 2022によると、2022年には世界中で約12,224,551例の虚血性脳卒中が報告されています。同資料によると、世界では毎年1,220万人以上の脳卒中が新たに発生しています。25歳以上の4人に1人が一生のうちに脳卒中を発症することになります。塞栓防止システムは、虚血性脳卒中を管理するのに好まれているため、虚血性脳卒中の症例が増加することで、これらのシステムの需要が促進されると考えられています。したがって、虚血性脳卒中の症例の増加は、治療のために塞栓防止システムを利用し、それによって市場の成長を後押しすると予想されます。

さらに、低侵襲処置に対する需要の高まりや技術進歩の増加が市場成長を後押しすると予想されています。例えば、2022年5月にFrontiers誌に掲載された論文によると、血腫の低侵襲手術(MIS)による排出は有望な結果を示しており、臨床で実施される可能性が高いです。また、低侵襲手術(MIS)は深在性原発性血腫の死亡率を低下させることが証明されています。このように、血腫による死亡率低下の可能性は、低侵襲手術の採用を増加させ、それによって塞栓防止システムの需要を増加させ、市場の成長を促進すると予想されます。

したがって、心臓および神経血管合併症の増加、低侵襲手術の採用増加により、調査対象市場は予測期間中に大きな成長を示すと予想されます。しかし、厳しい規制シナリオや不利な政府政策、熟練した専門家の不足が市場成長の主な欠点となっています。

塞栓防止システムの市場動向

心血管疾患セグメントは予測期間中に顕著な成長が見込まれる

心血管疾患セグメントは、心血管疾患の増加、心血管治療における塞栓防止システムの採用増加などの要因により、調査市場において著しい成長を示すことが期待されます。例えば、BHFのファクトシート2022によると、先天性心疾患は世界的に約110人に1人の出生で診断され、より多くの診断が後年に行われ、年間120万人の赤ちゃんが生まれると推定されています。同様に、AIHWによる2023年2月の更新によると、2021年から2021年の間にオーストラリアの病院に入院した患者に対して報告された冠動脈造影処置は146,000件で、男性が97,200件(67%)、女性が48,900件(33%)でした。また、心臓病に対する低侵襲手術の増加が予測期間中のセグメント成長を促進すると予想されます。例えば、NICOR Adult Cardiac Surgery Report 2022によると、2020~2021年の期間に英国全体で19,333件の成人心臓手術が実施されました。したがって、心臓手術の増加は塞栓防止システムの需要を増加させ、それによって予測期間中のセグメント成長を押し上げると予想されます。

さらに、JACCが2022年2月に実施した調査では、ECBはパクリタキセルでコーティングしたバルーンと比較して、狭窄率の減少や動脈宿主反応の低下に役立つことが判明しています。このような研究結果は、ECBが心血管疾患にもたらす利点を示すものであり、市場セグメンテーションの市場成長を促進するものです。さらに、2022年3月、Saint Luke's Health Systemは、生体弁骨折(BVF)を伴う経カテーテル大動脈弁置換術(VIV TAVR)を受ける患者において、SENTINEL経カテーテル脳塞栓防止(TCEP)デバイスによって捕捉される破片の量を定量化する臨床試験を後援しました。

したがって、心臓合併症の増加、心臓手術症例の増加、塞栓防止を利用した心血管疾患に関連する臨床研究の増加により、研究セグメントは予測期間中に大きな成長を示すと予想されます。

北米は予測期間中、塞栓防止システム市場で大きな市場シェアを占めると予測される

北米は、予測期間を通じて、塞栓防止システム市場全体で大きな市場シェアを占めると予測されます。その主な理由は、心臓および神経疾患の有病率の高さ、ヘルスケア支出の増加、主要企業の存在です。

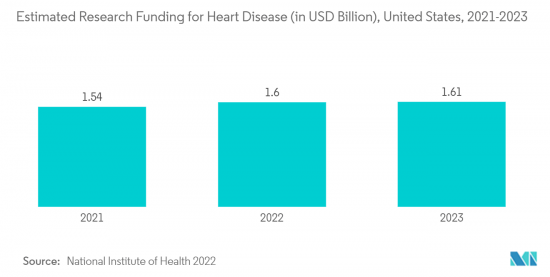

北米人口における心臓合併症の有病率の上昇は、塞栓防止システムの需要を増加させると予想されています。例えば、CIHIの2022年7月の更新によると、約240万人のカナダ人が心臓病を患っています。したがって、この慢性疾患の高い有病率は、予測期間中に塞栓防止システムを利用すると予想されます。また、心臓病や関連疾患に対する研究資金が、予測期間を通じて北米地域の市場成長を後押しすると期待されています。例えば、NIHによる2022年5月の更新によると、冠動脈性心臓病研究のための推定資金は2023年に3億9,700万米ドルです。したがって、心臓病に対するこのような研究費は、予測期間にわたって市場の成長を促進すると予測されます。

さらに、調査地域の組織が実施する塞栓防止に関連する臨床研究は、市場成長を促進する可能性が高いです。例えば、Cleveland Clinicによる2022年9月のアップデートによると、Cleveland Clinic主導の臨床試験から得られた知見は、脳塞栓保護(CEP)デバイスが、経カテーテル大動脈弁置換術(TAVR)の結果生じるカルシウムやその他の断片の小さな破片を、それらが脳に到達する前に捕捉して除去することにより、障害を引き起こす脳卒中のリスクを低減することを示しました。したがって、塞栓防止システムが提供するこのような利点のおかげで、予測期間中の市場成長を強化することが期待されます。

このように、心臓および神経血管疾患の増加、塞栓防止に関連する臨床研究の増加により、北米は予測期間中に大きな成長を示すことが期待されています。

塞栓防止システム産業概要

塞栓防止システム市場の競争は中程度です。主要企業は、新たな進歩と製品開発に注力しています。現在市場を独占している企業には、Boston Scientific Corporation、Abbott、Medtronic、Cardinal Health、Contego Medical, LLC、Silk Road Medical, Inc、Edwards Lifesciences Corporation、Lepu Medical Technologyなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心血管および神経血管疾患の有病率の上昇

- 低侵襲手術に対する需要の増加

- 市場抑制要因

- 厳しい規制シナリオと不利な政府政策

- 熟練労働者の不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- 製品技術タイプ別

- 遠位閉塞デバイス

- 遠位フィルター

- 近位咬合デバイス

- 材料別

- ニチノール

- ポリウレタン

- 用途別

- 神経血管疾患

- 心血管疾患

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Hellman & Friedman LLC(Cordis)

- Boston Scientific Corporation

- Abbott Laboratories

- Medtronic Plc

- Cardinal Health

- Contego Medical, LLC

- Silk Road Medical,Inc

- Edwards Lifesciences Corporation

- Lepu Medical Technology

第7章 市場機会と今後の動向

The embolic protection systems market studied was projected to grow with a CAGR of 8.6% over the forecast period.

COVID-19 had a significant impact on the embolic protection systems market since many neurovascular and cardiovascular surgeries were delayed or canceled during the initial wave of the pandemic. For instance, as per the article from PubMed published in February 2021, since neurological patients require more frequent hospitalization and had a higher chance of disability after discharge, patients had trouble getting regular monitoring, surgery, or treatment for their neurological issues because of the global lockdown, which had a significant impact on the market under study. Currently, the market is gaining its pre-pandemic environment due to the high demand for embolic protection systems as COVID-19-related restrictions have been eased. Also, the market is expected to witness growth in the coming years due to the rise in neurovascular and cardiac complications and an increase in the adoption of embolic protection systems.

Factors such as the rise in the prevalence of cardiovascular and neurovascular diseases and increasing demand for minimally invasive surgeries are expected to bolster market growth over the forecast period.

The major factor attributing to the growth of the market is the rising prevalence of cardiovascular and neurovascular diseases. For instance, as per the Global Stroke Fact Sheet 2022, around 12,224,551 cases of ischemic stroke were reported in 2022 across the globe. The same source further stated that over 12.2 million new strokes occur annually/each year globally. One in four people over age 25 will have a stroke in their lifetime. Since embolic protection systems are largely preferred in managing ischemic stroke, increasing cases of ischemic stroke are believed to propel the demand for these systems. Hence, the rise in cases of ischemic stroke is anticipated to utilize the embolic protection systems for the treatment and thereby boosting the market growth.

Furthermore, rising demand for minimally invasive procedures and increasing technological advancements are expected to boost the market growth. For instance, as per the article published in May 2022, in Frontiers, minimally invasive surgical (MIS) evacuation of the hematoma showed promising results and is likely to be implemented in clinical practice. Also, minimally invasive surgery (MIS) has proven to reduce mortality in deep-seated primary hematomas. Thus, chance of redcution in mortality for hematoms are expected to increase the adoption of minimally invasive surgeries and thereby likely to increase the demand for embolic protection systems and driving market growth.

Hence, due to the rise in cardiac and neurovascular complications, and the increase in the adoption of minimally invasive surgeries, the studied market is expected to witness significant growth over the forecast period. However stringent regulatory scenarios and unfavorable government policies and a lack of skilled professionals are the major drawbacks to market growth.

Embolic Protection Systems Market Trends

Cardiovascular Disease Segment is Expected to Witness a Notable Growth Over the Forecast period

The cardiovascular disease segment is expected to witness significant growth in the studied market owing to the factors such as an increase in cardiovascular diseases, and a rise in the adoption of embolic protection systems in cardiovascular therapies. For instance, as per the BHF fact sheet 2022, congenital heart disease is diagnosed in around 1 in 110 births globally, with more diagnoses later in life, that is an estimated 1.2 million babies a year. Similarly, according to the February 2023 update by AIHW, there were 146,000 coronary angiography procedures reported for patients admitted to hospitals in Australia, 97,200 (67%) for males and 48,900 (33%) for females during 2021-2021. Also, an increase in minimally invasive surgeries for heart diseases is expected to drive segment growth over the forecast period. For instance, as per the NICOR Adult Cardiac Surgery Report 2022, 19,333 adult heart operations were performed during the period of 2020-2021 across the United Kingdom. Thus, an increase in cardiac surgeries is expected to increase the demand for embolic protection systems and thereby boosting the segment growth over the forecast period.

Furthermore, in a survey conducted by JACC in February 2022, it was found that ECB can help in the reduction of stenosis rates and lower arterial host reaction compared to paclitaxel-coated balloons. Hence, such studies show the advantages offered by the ECB in cardiovascular disease, thereby increasing market growth in the studied segment. Moreover, in March 2022, Saint Luke's Health System sponsored a clinical trial to quantify the amount of debris captured by the SENTINEL transcatheter cerebral embolic protection (TCEP) device in patients undergoing valve in valve transcatheter aortic valve replacement (VIV TAVR) with bioprosthetic valvular fracture (BVF), Such clinical studies and researchers utilizing the embolic protection are estimated to increase the market growth.

Therefore, due to the rise in cardiac complications, the increase in cardiac surgery cases, and the increase in clinical studies associated with cardiovascular diseases utilizing embolic protection, the studied segment is expected to witness significant growth over the forecast period.

North America is Anticipated to Hold a Significant Market Share in the Embolic Protection Systems Market Over the Forecast Period

North America is expected to hold a significant market share in the overall embolic protection systems market, throughout the forecast period, mainly due to the high prevalence of cardiac and neurology diseases, an increase in healthcare expenditures, and the presence of key players.

The rise in the prevalence of cardiac complications among the North American population is expected to increase the demand for embolic protection systems. For instance, as per the July 2022 update from CIHI, about 2.4 million Canadians have heart disease. Hence, the high prevalence of the chronic disease is expected to utilize embolic protection systems over the forecast period. Also, research funding for heart and related diseases is expected to bolster the market growth in the North American region, over the forecast period. For instance, as per the May 2022 update by NIH, the estimated funding for Coronary Heart Disease research is USD 397 million in 2023. Thus, such research funding for heart diseases is estimated to bolster market growth over the forecast period.

Moreover, clinical studies relating to embolic protection conducted by organizations in the studied region are likely to drive market growth. For instance, as per the September 2022 update by Cleveland Clinic, findings from a Cleveland Clinic-led trial showed that a Cerebral Embolic Protection (CEP) device reduced the risk of disabling strokes by capturing and removing tiny pieces of calcium and other fragments resulting from transcatheter aortic valve replacement (TAVR) before they can reach the brain. Hence, owing to such advantages offered by embolic protection systems are expected to bolster the market growth over the forecast period.

Thus, due to the rise in cardiac and neurovascular diseases, and the increase in clinical studies associated with embolic protection, North America is expected to witness significant growth over the forecast period.

Embolic Protection Systems Industry Overview

The embolic protection systems market is moderately competitive. The major players are focusing on new advancements and product development. Some of the companies which are currently dominating the market are Boston Scientific Corporation, Abbott, Medtronic, Cardinal Health, Contego Medical, LLC, Silk Road Medical, Inc, Edwards Lifesciences Corporation, and Lepu Medical Technology among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Prevalence of Cardiovascular and Neurovascular Diseases

- 4.2.2 Increasing Demand for Minimally Invasive Surgeries

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Scenarios and Unfavorable Government Policies

- 4.3.2 Lack of Skilled Labor

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Product Technology Type

- 5.1.1 Distal Occlusion Devices

- 5.1.2 Distal Filters

- 5.1.3 Proximal Occlusion Devices

- 5.2 By Material

- 5.2.1 Nitinol

- 5.2.2 Polyurethane

- 5.3 By Application

- 5.3.1 Neurovascular Diseases

- 5.3.2 Cardiovascular diseases

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Hellman & Friedman LLC (Cordis)

- 6.1.2 Boston Scientific Corporation

- 6.1.3 Abbott Laboratories

- 6.1.4 Medtronic Plc

- 6.1.5 Cardinal Health

- 6.1.6 Contego Medical, LLC

- 6.1.7 Silk Road Medical,Inc

- 6.1.8 Edwards Lifesciences Corporation

- 6.1.9 Lepu Medical Technology