|

市場調査レポート

商品コード

1406037

吻合器 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測Anastomosis Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 吻合器 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

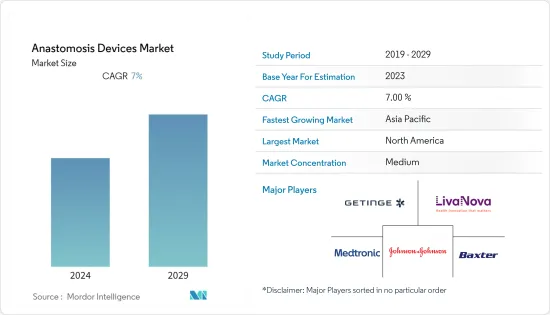

吻合器市場は予測期間中にCAGR 7.0%を記録すると予測されています。

COVID-19の大流行はかつてない健康上の懸念であり、さまざまな外科手術に悪影響を及ぼしています。緊急性のない手術は行わないようにという規制当局の厳しい指導により、パンデミックを通じて手術件数は激減しています。国立医学図書館が2021年10月に世界的に発表した研究によると、一般外科の入院数は42.8%減少しています。このように、COVID-19パンデミック中の外科手術件数の減少は、市場の成長に影響を与えました。しかし、延期された手術は世界中で再開され、パンデミック後の期間の市場の成長を牽引しました。

大腸切除術、CABGなどの外科手術の増加、技術的に進歩した製品の入手可能性、償還政策などの要因が、吻合器市場の成長を後押ししています。例えば、StatPearlsが発表した記事によると、2022年8月には毎年40万件近くのCABG手術が行われており、米国で最も一般的に行われている主要外科手術となっています。さらに、HSRAが2022年3月に発表したデータによると、米国では2021年に約4万件の臓器移植が行われました。また、2021年には米国で26,670件の腎臓移植と9,236件の生体移植が行われました。このように、外科手術の増加は吻合デバイスの需要数を増加させると予想され、それゆえ市場を牽引します。

さらに、外傷、股関節置換術、膝関節置換術、心血管疾患など手術が必須となる慢性疾患による外科手術の件数が増加しています。これが吻合器市場の主な成長要因です。例えば、Journal of Thoracic and Cardiovascular Surgeryが2021年6月に発表した調査研究によると、古典的な意味での心臓外科手術として分類された手術は合計92,809件で、そのうち29,444件が単独の冠動脈バイパス移植手術、35,469件が単独の心臓弁手術であり、単独の心臓移植件数は2%増の340件でした。したがって、心臓の処置や手術の実施件数の多さは、吻合装置市場の成長を後押しすると予想されます。

製品の発売、合併、買収、提携など、主要な市場参入企業によるさまざまな取り組みが、予測期間中の市場成長を後押しすると予想されます。例えば、2021年8月、メディケアパートBは冠動脈バイパスグラフト手術、冠動脈形成術、弁修理&交換、その他の包括的な心臓リハビリテーション(CR)プログラムをカバーします。また、2021年3月には、ジョンソン・エンド・ジョンソン(米国)がECHELON+Staplerを発売しました。ECHELON+Staplerは、より均一な組織圧縮と優れたステープル形成によって手術の合併症を軽減するように設計された電動手術用ステープラーです。このような発展は、予測期間中の市場成長を促進すると予想されます。

以上のような要因が、世界の市場の成長を牽引すると予想されます。しかし、経皮的冠動脈インターベンションのような低侵襲手技の採用や高額の治療費、高度なヘルスケアインフラの不足などが、予測期間中の吻合装置市場の成長を妨げると予想されます。

吻合器市場の動向

外科用縫合糸セグメントが吻合デバイス市場で大きなシェアを占める見込み

縫合糸とは、手術部位を閉鎖するために血管や組織を縫合するために使用されるあらゆる材料の繊維を指します。主に使用される材料の種類によって、専門医が行う縫合層のレベルが決まる。不健康なライフスタイルや慢性疾患の蔓延は、このセグメント市場の成長を促進すると予想されています。例えば、European Heart Networkが2021年に発表したデータによると、欧州連合(EU)では6,000万人以上が心血管疾患を抱えて生活しており、毎年1,300万人近くが新たに心血管疾患と診断されています。このような心血管疾患の有病率の増加は、外科的処置や治療の必要性の増加につながり、吻合装置市場の成長を促進すると予想されています。

製品の発売、合併、買収、提携など、主要な市場参入企業によるさまざまな取り組みが、セグメントの成長を後押しすると期待されています。例えば、2022年3月、C2Dx社はHemostatix Medical Technologies社を買収し、同社の第3の製品ラインとなるサーマルスカルペルシステムを獲得しました。Hemostatix Thermal Scalpelは、血管を切断する際に血管を密封し、効果的に切断と凝固を同時に行う。このような市場開拓は、予測期間中の市場成長を促進すると予想されます。

このように、同分野は上記の要因から予測期間中に大きく成長すると予想されます。

北米が市場で大きなシェアを占め、予測期間中も同様と予測

北米は、手術機器に関する規制の枠組みが整備され、怪我や慢性疾患の問題がある場合に手術に臨む意識が国民の間で高まっていることから、予測期間を通じて市場全体で大きなシェアを占めると予想されます。例えば、アラバマ大学バーミンガム校の2021年4月のデータによると、米国では年間35万件のCABG手術が行われています。心血管障害と肥満の有病率が上昇していることが、この地域における市場の成長に寄与しています。さらに、CDCの2022年最新情報によると、2022年10月には、1,820万人の成人が冠動脈疾患を患っており、これらの患者の約70%が手術を受けています。米国では毎年約3,500万件の入院が記録されています。したがって、このような入院や手術の増加が市場を成長させると予想されます。米国では交通事故による負傷が増加しているため、外科手術が増加し、吻合器具の使用量が増加しています。ASIRT社が2022年3月に発表したデータによると、米国では年間440万人の米国人が医療処置を必要とするほどの重傷を負っています。

Surgical Endoscopyが2021年11月に発表した研究によると、腹腔鏡下胆嚢摘出術は米国で最も一般的な腹部外科治療であり、年間75万件以上の手術が行われています。これらの手術では吻合器具が使用されるため、同国での市場成長が期待されています。

このように、前述の要因によって、予測期間中に北米の市場成長が促進されると予想されます。

吻合器産業の概要

吻合器市場は、世界的および地域的に事業を展開する企業が存在するため、中程度の規模となっています。競合情勢には、バクスター(Synovis Micro Companies Alliance)、Medtronic PLC、LivaNova PLC、Getinge AB、Johnson &Johnson(Ethicon US LLC.)、Meril Life Sciences Pvt. Ltd、Becton、Dickinson and Company、Intuitive Surgical、Boston Scientific Corporation、B. Braun SEなど、市場シェアを持ち知名度の高い国際企業や地元企業の分析が含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 大腸切除術、CABGなどの手術件数の増加

- 技術的に高度な製品の入手可能性と償還政策

- 市場抑制要因

- 経皮的冠動脈インターベンションなどの低侵襲手技の採用

- 高額な治療費と高度なヘルスケアインフラの欠如

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- 用途別

- 使い捨て

- 再利用可能

- タイプ別

- 外科用ステープラー

- 外科用縫合糸

- 外科用シーラントおよび接着剤

- その他のタイプ

- 用途別

- 心臓血管外科

- 消化器外科

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Baxter(Synovis Micro Companies Alliance)

- Medtronic PLC

- LivaNova PLC

- Getinge AB

- Johnson & Johnson(Ethicon US LLC.)

- Meril Life Sciences Pvt. Ltd

- Becton, Dickinson and Company

- Intuitive Surgical

- Boston Scientific Corporation

- B. Braun SE

第7章 市場機会と今後の動向

The anastomosis devices market is anticipated to register a CAGR of 7.0% during the forecast period.

The COVID-19 pandemic is an unprecedented health concern and adversely affects various surgical procedures. Due to regulatory authorities' strict guidance to prevent any non-emergent surgeries, the volume of surgeries has drastically decreased throughout the pandemic. According to the study published in October 2021 by the National Library of Medicine globally, there has been a 42.8% decrease in general surgery admissions. Thus, the reduction in the number of surgical procedures during the COVID-19 pandemic affected the market's growth. However, the postponed surgeries resumed worldwide, driving the market's growth during the post-pandemic period.

Factors such as the rise in several surgical procedures like colectomy, CABG, and others and the availability of technologically advanced products and reimbursement policies are boosting the growth of the market for anastomosis devices. For instance, according to an article published by StatPearls, in August 2022, almost 400,000 CABG surgeries are performed each year making it the most commonly performed major surgical procedure in United States. Additionally, according to the data published by the HSRA in March 2022, about 40,000 organ transplants were performed in the United States in 2021. In addition, 26,670 kidney transplants and 9,236 live transplants were performed in the United States in 2021. Thus, an increase in the surgical procedure is expected to increase the number of anastomosis devices demand, hence driving the market.

Moreover, the number of surgical procedures due to trauma, hip and knee replacements, and chronic diseases such as cardiovascular diseases where surgery is mandatory is growing. This is the primary growth factor for the anastomosis devices market. For instance, as per the research study published in June 2021 by the Journal of Thoracic and Cardiovascular Surgery, a total of 92,809 operations were classified as heart surgery procedures in the classical sense, of which 29,444 were isolated coronary artery bypass grafting procedures, 35,469 were isolated heart valve procedures, and the number of isolated heart transplantations increased by 2% to 340. Hence, the high number of heart procedures and operations being performed is expected to boost the growth of the anastomosis devices market.

Various initiatives taken by the key market players, such as product launches, mergers, acquisitions, and partnerships, are expected to boost the market's growth during the forecast period. For instance, in August 2021, Medicare Part B covers coronary artery bypass graft surgery, coronary angioplasty, valve repair & replacement, and other comprehensive Cardiac Rehabilitation (CR) programs. Also, In March 2021, Johnson & Johnson (US) launched the ECHELON+ Stapler, a powered surgical stapler designed to reduce complications in surgery through more uniform tissue compression and better staple formation. Such developments are expected to drive the growth of the market over the forecast period.

The above-mentioned factors are expected to drive the market's growth worldwide. However, the adoption of minimally invasive procedures like percutaneous coronary interventions and highly expensive treatments, and the lack of advanced healthcare infrastructure are expected to hamper the growth of the anastomosis devices market during the forecast period.

Anastomosis Devices Market Trends

Surgical Suture Segment is Expected to Hold Significant Share in the Anastomosis Devices Market

A suture refers to any strand of material used to litigate blood vessels or tissues to close a surgical site. The type of material used primarily decides the level of sutures layers to be done by a speciality doctor. The growing prevalence of unhealthy lifestyles and chronic diseases is expected to drive the growth of the segmental market. For instance, the data published by the European Heart Network in 2021 reported that in the European Union, more than 60 million people live with Cardiovascular disease, and nearly 13 million new cases of cardiovascular diseases are diagnosed yearly. Such increasing prevalence of cardiovascular diseases, which led to an increasing need for surgical procedures and treatment, is expected to drive the growth of the anastomosis devices market.

Various initiatives taken by the key market players, such as product launches, mergers, acquisitions, and partnerships, are expected to boost segmental growth. For instance, in March 2022, C2Dx acquired Hemostatix Medical Technologies, gaining a thermal scalpel system to become the company's third product line. The Hemostatix Thermal Scalpel seals blood vessels as they're cut, effectively cutting and coagulating simultaneously. Such development is expected to drive the growth of the market over the forecast period.

Thus, the segment is expected to grow significantly over the forecast period due to the abovementioned factors.

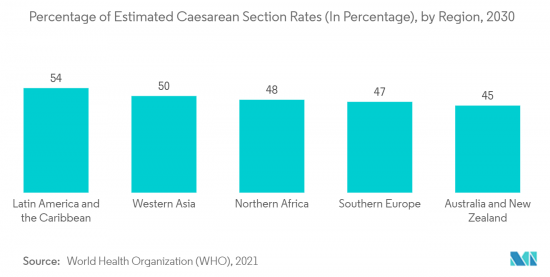

North America Holds a Significant Share in the Market and Expected to do Same in the Forecast Period.

North America is expected to witness a significant share in the overall market throughout the forecast period due to better regulatory practice framework of surgical devices and growing awareness among the population to approach surgeries in case of injuries and chronic disease problems. For instance, according to the April 2021 data from the University of Alabama at Birmingham, 350,000 CABG surgeries are performed annually in the United States. The rising prevalence of cardiovascular disorders and obesity rates is attributed to the market's growth in this region. Furthermore, according to the CDC's 2022 update, in October 2022, 18.2 million adults had coronary artery disease, and approximately 70% of these patients underwent surgery. The United States records nearly 35 million hospital stays each year. Hence, this rise in hospital stays and surgeries is expected to grow the market. The increasing number of injuries due to road accidents in the United States resulted in increased surgical procedures, thereby increasing the usage of anastomosis devices. According to the data published in March 2022 by ASIRT, annually, 4.4 million Americans are injured seriously enough to require medical attention in the United States.

According to a study published in November 2021 by Surgical Endoscopy, laparoscopic cholecystectomy is the most common abdominal surgical treatment in the United States, with over 750,000 procedures performed annually. These procedures use anastomosis devices, which is expected to boost the market's growth in the country.

Thus, the aforementioned factors are expected to boost the market's growth in North America over the forecast period.

Anastomosis Devices Industry Overview

The anastomosis devices market is moderate due to the presence of companies operating globally and regionally. The competitive landscape includes an analysis of a few international and local companies that hold market shares and are well-known, including Baxter (Synovis Micro Companies Alliance), Medtronic PLC, LivaNova PLC, Getinge AB, Johnson & Johnson (Ethicon US LLC.), Meril Life Sciences Pvt. Ltd, Becton, Dickinson and Company, Intuitive Surgical, Boston Scientific Corporation and B. Braun SE, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Number of Surgical Procedures like Colectomy, CABG and Others

- 4.2.2 Availability of Technologically Advanced Products and Reimbursement Policies

- 4.3 Market Restraints

- 4.3.1 Adoption of Minimally Invasive Procedures like Percutaneous Coronary Interventions

- 4.3.2 Highly Expensive Treatments and Lack of Advanced Healthcare Infrastructure

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Usage

- 5.1.1 Disposable

- 5.1.2 Reusable

- 5.2 By Type

- 5.2.1 Surgical Staplers

- 5.2.2 Surgical Sutures

- 5.2.3 Surgical Sealants and Adhesives

- 5.2.4 Other Types

- 5.3 By Application

- 5.3.1 Cardiovascular Surgery

- 5.3.2 Gastrointestinal Surgery

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United states

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Baxter (Synovis Micro Companies Alliance)

- 6.1.2 Medtronic PLC

- 6.1.3 LivaNova PLC

- 6.1.4 Getinge AB

- 6.1.5 Johnson & Johnson (Ethicon US LLC.)

- 6.1.6 Meril Life Sciences Pvt. Ltd

- 6.1.7 Becton, Dickinson and Company

- 6.1.8 Intuitive Surgical

- 6.1.9 Boston Scientific Corporation

- 6.1.10 B. Braun SE