|

市場調査レポート

商品コード

1406029

足白癬治療- 市場シェア分析、産業動向・統計、成長予測、2024~2029年Tinea Pedis Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 足白癬治療- 市場シェア分析、産業動向・統計、成長予測、2024~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 112 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

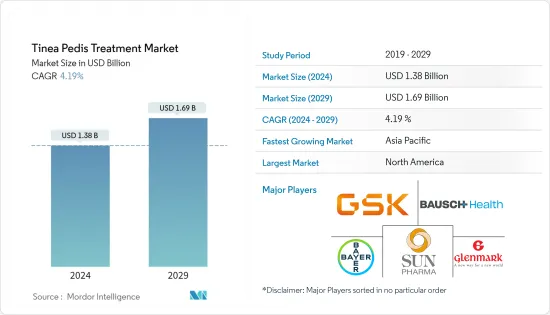

足白癬治療薬市場規模は2024年に13億8,000万米ドルと推定・予測され、2029年には16億9,000万米ドルに達し、予測期間(2024~2029年)のCAGRは4.19%で成長すると予測されます。

COVID-19の大流行時には、COVID-19患者の死亡率に対する懸念が高まり、足白癬治療薬の需要が高まった。COVID-19に真菌が併存すると、併存疾患のないCOVID-19患者と比較して死亡率が高くなります。例えば、2022年8月にNature Microbiologyが発表した論文によると、COVID-19に関連した侵襲性真菌感染症は、重症の入院患者の相当数において重大な合併症でした。したがって、COVID-19のパンデミックは、その前段階において市場に大きな影響を与えました。しかし、パンデミックは現在沈静化しているため、本調査の予測期間中は安定した成長が見込まれます。

市場成長の主な要因は、真菌感染症の有病率の増加です。真菌症は世界的に分布しているが、患者数が最も多いのは熱帯・亜熱帯諸国です。患者数の増加に伴い、市場も拡大しています。さらに、研究開発プログラムの増加とそのための資金援助が市場の成長を後押ししています。

例えば、NCBIが2022年7月に更新した論文によると、全人口の約10%が足指裂部の皮膚糸状菌感染症に罹患していると推定されています。この最も一般的な原因は、閉塞性の靴を長時間履くことです。また、公衆浴場、シャワー、プールを利用する人の間で足白癬の発症率が高いことが観察されていることから、洗い場を共有することで感染の可能性が高まる可能性が高いとしています。また、足白癬は女性よりも成人男性に多いとも言われています。これに加えて、免疫不全患者の増加も市場成長を促進すると予想される要因の1つです。

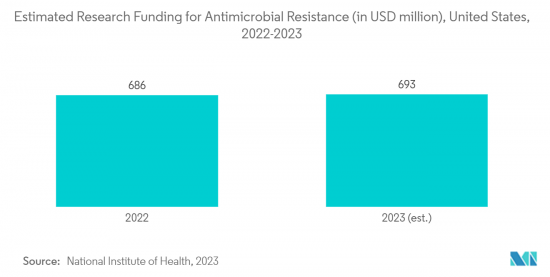

さらに、細菌、ウイルス、真菌による感染症の有病率の上昇により、足白癬治療のための研究開発活動が活発化していることも、市場を牽引しています。世界中で、抗菌剤研究は牽引力を増しており、多くの企業がすでに研究開発活動を開始しています。真菌感染症も抗菌剤研究活動の一部であるため、調査対象市場の成長をさらに押し上げると予想されます。例えば、Global Anti Microbial Resistance R&D Hubの2021年1月のレポートによると、2021年1月8日現在、1,047の真菌研究開発プロジェクトに総額3億6,200万米ドルが投資されており、この投資の大部分はヒト関連の研究プロジェクトに提供されています。報告書によると、真菌の研究開発プロジェクトに投資される資金は、動物分野よりもヒト分野の方が多いです。

そのため、足白癬の有病率の上昇や真菌治療に関する研究開発の増加などが、市場の成長を促進する要因として期待されています。しかし、治療法の認知度の低さや厳しい認可規制が市場成長の制約となっています。

足白癬治療の市場動向

予測期間中、外用薬セグメントが大きな市場シェアを占める見込み

足白癬の外用薬は一般的に、皮膚の上から足の特定の場所に塗布します。他の投与経路と比較して局所投与経路が優れていること、局所抗真菌治療が進歩していることなどから、予測期間中、局所投与セグメントは大きな市場シェアを占めると予想されます。足白癬治療における局所投与の主な利点としては、全身性の有害事象や薬物相互作用のリスクが低いこと、低コストであること、使用する薬剤の量が少量であることなどが挙げられます。例えば、2022年3月にPubMed Centralが発表した論文によると、アゾール系で最も一般的な外用抗真菌薬には、クロトリマゾールなどのイミダゾールの誘導体が含まれます。クロトリマゾールは足白癬の治療に使われる薬です。したがって、このような医薬品が外用剤で入手可能であることが、同分野の成長を押し上げると予想されます。

さらに、2022年8月にPubMed Centralが発表した論文によると、局所用抗真菌製剤には、感染部位を標的とする能力を含む特異的な作用機序など多くの利点があり、治療効果を高め、さらに全身性の副作用のリスクを低減します。真菌性皮膚感染症の治療における局所製剤の有効性とその位置づけは、特にクリーム、軟膏、ゲルなどの適切なビヒクルが使用される場合、患者のコンプライアンスが高いことによってさらに強化されます。このように、局所用抗真菌製剤にはいくつかの利点があるため、局所用セグメントは本調査の予測期間中に成長すると予想されます。

さらに、主要市場参入企業による足白癬外用剤に関する新たな発展や臨床試験も、先進的な製品の開発につながるため、同分野の成長を後押ししています。例えば、2021年1月、標的局所治療薬の開発に注力する臨床段階のバイオテクノロジー企業であるDermBiont社は、足白癬治療用の局所クリーム製品である治験薬DBI-001の第2b相臨床試験を発表しました。その結果、足白癬の徴候や症状が統計学的に有意に改善されました。さらに、抗菌剤耐性に関する研究の増加も、より強力な新規抗真菌剤処方の開発を増加させると予想されます。

このように、新たな発展や主な市場プレイヤー、抗菌剤耐性に関する研究の増加、局所抗真菌製剤の利点など、上記の要因により、この市場セグメントは長期的に成長を示すと予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米は、強固なヘルスケアインフラ、足白癬の高い有病率、治療薬の入手のしやすさなどから、大きな市場シェアを占めると予想されます。北米内では、米国が足白癬市場で大きなシェアを占めているが、これは足白癬に罹患する人口が多いことが主な原因であり、新規の治療アプローチに対する高い需要を生み出しています。

米国における足白癬の有病率の増加は、北米の市場成長を促進すると予想される重要な要因です。例えば、2022年9月にPubMedが発表した論文によると、米国で研究が実施され、研究対象集団のうち6,932人の患者が足白癬に罹患しており、全体の有病率は2.76%でした。このことは、同国における足白癬治療の普及につながる可能性があり、同地域の市場成長を促進すると予想されます。さらに、2021年1月にカナダ家庭医学会(The College of Family Physicians of Canada)が発表した論文によると、足白癬は外用抗真菌薬で70%から75%の患者が治療に成功しているのに対し、プラセボを使用した場合は20%から30%です。このため、この地域では足白癬に対する局所抗真菌薬治療の需要が増加すると考えられます。

また、カナダでも足白癬治療の研究開発が行われています。例えば、ClinicalTrials.govが更新したデータによると、2023年7月現在、カナダでは3件の足白癬関連の臨床試験が実施され、足白癬の治療に対する一酸化窒素放出溶液(NORS)などの様々な製剤の有効性が確認されています。このように、このような臨床試験は、国内で足白癬に関する研究が行われていることを示しており、足白癬を治療するための新しく先進的な製品の開発を後押しすると期待されています。

したがって、足白癬の有病率の高さ、足白癬の新規治療薬の研究開発の活発化などが、北米における同市場の成長を促進すると予想されます。

足白癬治療薬産業の概要

足白癬治療市場は競争が激しく、複数の大手企業で構成されています。市場の主要企業としては、GlaxoSmithKline PLC、Bausch Health、Glenmark Pharmaceuticals、Bayer AG、Sanofi、Sun Pharma、Teva Pharmaceutical などが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 真菌感染症の有病率の増加

- 世界の老年人口の増加

- 市場抑制要因

- 効果的な治療法の認識不足と厳しい承認規制

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模、金額ベース)

- 投与経路別

- 経口

- 局所

- 流通チャネル別

- 病院薬局

- 小売薬局

- eコマース

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- GlaxoSmithKline PLC

- Bausch Health Companies Inc.

- Glenmark Pharmaceuticals Limited

- Bayer AG

- Sun Pharmaceutical Industries Ltd

- Sebela Pharmaceuticals Holdings Inc.

- Teva Pharamceutical Industries Limited

- Amneal Pharmaceuticals Inc.

- Viatris Inc.

- Pfizer Inc.

- Advantice Health(Kerasal)

- Abigail Healthcare Pharmaceutical

第7章 市場機会と今後の動向

The Tinea Pedis Treatment Market size is estimated at USD 1.38 billion in 2024, and is expected to reach USD 1.69 billion by 2029, growing at a CAGR of 4.19% during the forecast period (2024-2029).

During the COVID-19 pandemic, the demand for tinea pedis treatment drugs rose due to increasing concerns about the mortality of patients with COVID-19. Fungal comorbidities in COVID-19 lead to higher mortalities compared to COVID-19 patients without these comorbidities. For instance, according to an article published by Nature Microbiology in August 2022, COVID-19-associated invasive fungal infections were a significant complication in a substantial number of critically ill, hospitalized patients. Hence, the COVID-19 pandemic affected the market significantly in its preliminary phase. However, as the pandemic has currently subsided, the studied market is expected to have stable growth over the forecast period of the study.

The major factor attributing to the growth of the market is the increase in the prevalence of fungal infections. Mycotic diseases are global in distribution, but the maximum cases are recorded from tropical and subtropical countries. As the number of patients increases, the market also grows. Furthermore, the increasing R&D programs and funding for the same are boosting the market growth.

For instance, according to an article updated by NCBI in July 2022, it is estimated that about 10% of the total population is affected by dermatophyte infections of the toe clefts. The most common reason for this is wearing occlusive shoes for long periods. The report also stated that the sharing of washing facilities is likely to increase the chances of infection as the incidence of tinea pedis is observed to be higher among those using community baths, showers, and pools. Tinea pedis is also said to be more common in adult males than in females. In addition to this, the rise in immunocompromised patients is also another factor that is expected to fuel market growth.

Furthermore, the increased R&D activities for the treatment of tinea pedis have been boosted by the rise in the prevalence rate of infectious disorders caused by bacteria, viruses, and fungi, which is driving the market. Around the world, anti-microbial research is gaining traction, and many companies have already initiated R&D activities, which is further expected to boost the growth of the studied market as fungal infections are also part of anti-microbial research activities. For instance, as per the January 2021 report of the Global Anti Microbial Resistance R&D Hub, as of January 8, 2021, a total of USD 362 million has been invested in 1,047 fungal R&D projects, and the majority of this investment is provided to human-related research projects. As per the report, more funds are invested in fungal R&D projects in the human sector than in the animal sector.

Therefore, a rise in the prevalence of tinea pedis and a rise in research and development on fungal treatment, among others, are the factors expected to drive the market growth. However, the lack of awareness of the treatment and stringent approval regulations constrain the market growth.

Tinea Pedis Treatment Market Trends

The Topical Segment is Expected to Hold a Significant Market Share Over the Forecast Period

Topical medications for tinea pedis are generally applied to a particular place in the feet over the skin. The topical segment is expected to have a significant market share during the forecast period due to the advantages of the topical route of administration over other routes and advancements in topical antifungal treatments, among others. The key benefits of topical administration of tinea pedis treatment include the low risk of systemic adverse events and drug interactions, low cost, and smaller amounts of drugs used, among other factors. For instance, according to an article published by PubMed Central in March 2022, the most common antifungal medicines for topical application from the azole class include derivatives of imidazole, such as clotrimazole. Clotrimazole is a medication that is used to treat tinea pedis. Hence, the availability of such medicines in topical form is expected to boost segment growth.

Furthermore, according to an article published by PubMed Central in August 2022, topical antifungal formulations have many benefits, such as their specific mechanism of action, including their ability to target the site of infection, enhance treatment efficacy, and further reduce the risk of systemic side effects. The proven efficacy of topical formulations, and the positioning in the treatment of fungal skin infections, are further enhanced by high patient compliance, especially when appropriate vehicles such as creams, ointments, and gels are used. Thus, owing to the several advantages of topical antifungal formulations, the topical segment is expected to grow during the forecast period of the study.

Moreover, new developments and clinical trials related to topical tinea pedis formulations by key market players are also enhancing segment growth, as it will lead to the development of advanced products. For instance, in January 2021, DermBiont, a clinical-stage biotechnology company focused on developing targeted topical therapeutics, released its phase 2b clinical trial with its investigational drug product, DBI-001, a topical cream product for the treatment of tinea pedis. This resulted in statistically significant improvements in tinea pedis signs and symptoms. Furthermore, the increasing research on antimicrobial resistance is also expected to increase the development of new and more potent topic antifungal formulations.

Thus, owing to the abovementioned factors, such as the new developments and key market players, increasing research on antimicrobial resistance, and the advantages of topical antifungal formulations, the market segment is expected to show growth over time.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is expected to hold a significant market share due to robust healthcare infrastructure, high prevalence of tinea pedis, and easy availability of treatments. Within North America, the United States holds a significant share of the tinea pedis market, which is majorly due to the large population suffering from tinea pedis, creating a high demand for novel treatment approaches.

The increasing prevalence of tinea pedis in the United States is a significant factor expected to boost market growth in North America. For instance, according to an article published by PubMed in September 2022, a study was conducted in the United States, which showed that 6,932 patients had tinea pedis among the study population, with an overall prevalence of 2.76%. This may lead to the increased adoption of tinea pedis treatment in the country, which is expected to drive market growth in this region. Moreover, per an article published by The College of Family Physicians of Canada in January 2021, tinea pedis is successfully treated with topical antifungals in 70% to 75% of patients compared to 20% to 30% using a placebo. This will likely lead to an increased demand for topical antifungal treatment for tinea pedis in the region.

In addition, research and development are also being conducted in Canada for the treatment of tinea pedis. For instance, according to the data updated by ClinicalTrials.gov, as of July 2023, three tinea pedis-related clinical trials were conducted in Canada which checked the efficacy of various formulations such as nitric oxide-releasing solution (NORS) for the treatment of tinea pedis. Thus, such clinical trials show that research is being done on tinea pedis in the country, which is expected to boost the development of new and advanced products for treating tinea pedis.

Therefore, the high prevalence of tinea pedia and the rise in research and development of novel medications for tinea pedis, among others, are expected to drive the growth of this market in North America.

Tinea Pedis Treatment Industry Overview

The tinea pedis treatment market is highly competitive and consists of several major players. Some of the key companies in the market are GlaxoSmithKline PLC, Bausch Health, Glenmark Pharmaceuticals, Bayer AG, Sanofi, Sun Pharma, and Teva Pharmaceutical, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Fungal Infections

- 4.2.2 Rising Geriatric Population Around the World

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness of Effective Treatment and Stringent Approval Regulations

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Route of Administration

- 5.1.1 Oral

- 5.1.2 Topical

- 5.2 By Distribution Channel

- 5.2.1 Hospital Pharmacies

- 5.2.2 Retail Pharmacies

- 5.2.3 E-commerce

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 GlaxoSmithKline PLC

- 6.1.2 Bausch Health Companies Inc.

- 6.1.3 Glenmark Pharmaceuticals Limited

- 6.1.4 Bayer AG

- 6.1.5 Sun Pharmaceutical Industries Ltd

- 6.1.6 Sebela Pharmaceuticals Holdings Inc.

- 6.1.7 Teva Pharamceutical Industries Limited

- 6.1.8 Amneal Pharmaceuticals Inc.

- 6.1.9 Viatris Inc.

- 6.1.10 Pfizer Inc.

- 6.1.11 Advantice Health (Kerasal)

- 6.1.12 Abigail Healthcare Pharmaceutical

7 MARKET OPPORTUNITIES AND FUTURE TRENDS