|

市場調査レポート

商品コード

1406018

骨壊死治療:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Osteonecrosis Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 骨壊死治療:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

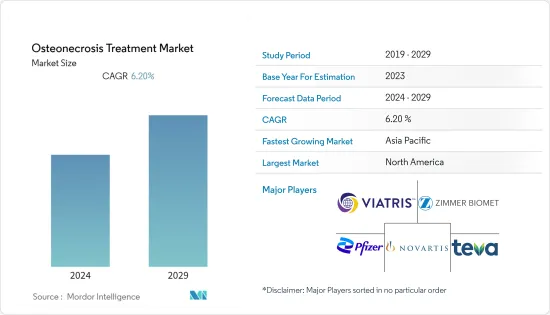

骨壊死治療市場は、予測期間中にCAGR 6.2%を記録する見込みです。

COVID-19パンデミックは、骨壊死または血管壊死がCOVID-19患者に見られる非常に一般的な合併症であったため、調査対象市場に大きな影響を与えました。パンデミック初期のCOVID-19患者の増加は、骨壊死患者の増加にもつながった。

例えば、MDPIが2021年11月に発表した論文によると、血管壊死(AVN)は重症COVID-19感染症や長期COVID-19感染症のステロイド治療後の合併症として知られています。AVNはまた、ステロイド治療前でなくてもCOVID-19感染直後に発症することもあります。明らかに、COVID-19感染のみがAVN発症の危険因子であり、平均して、AVNはCOVID-19発症後2週間で始まると推定され、長期にわたるCOVID-19後期発症AVNとは対照的です。このように、パンデミックは市場の成長に大きな影響を与えました。しかし、パンデミックが沈静化するにつれて、COVID-19-骨壊死症例は減少し始めているため、本調査の予測期間中、他の様々な要因による本疾患の高負担により、調査対象市場は安定した成長が見込まれます。

高齢者人口の増加は、世界的に骨壊死の発生率を増加させる。非侵襲的治療に対する需要の高まりと、骨壊死に対するより良い治療のための技術進歩が、骨壊死治療市場の主な促進要因となっています。

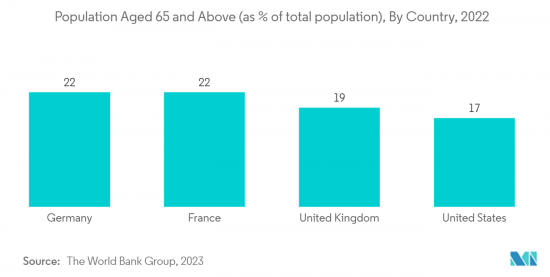

高齢化はしばしば骨壊死の有病率の増加と関連しています。例えば、NCBIが2022年11月に更新した論文によると、SONK(膝の自然骨壊死)は高齢者に多く、単顆人工膝関節置換術は比較的短いリハビリ期間で良好な機能的転帰をもたらします。さらに、WHOが2022年10月に発表したデータによると、2030年には世界の6人に1人が60歳以上の高齢者となり、60歳以上の人口に占める割合は14億人に増加すると推定されています。このように、老人人口の増加は、骨壊死治療製品に対する需要を増加させると予想されます。

さらに、骨壊死治療のための様々な非侵襲的ツールの市場開拓は、市場の成長を高めると予想されます。例えば、2022年9月にPubMed Centralが発表した論文によると、薬剤性顎骨壊死(MRONJ)は、主に骨修飾剤(BMA)に起因する重篤な副作用と考えられており、手術に適さない病期が進行した患者に対しては、長期の内科的治療が必要となり、その結果、抗生物質の過剰使用や抗生物質耐性のリスクが伴う。

特に、複雑な症例や医学的課題に対して、手術(侵襲的)処置がさらなる負担となる可能性がある場合、オゾン注入は、非手術的MRONJ治療のための革新的で強力かつ効果的な非侵襲的ツールになりうると、前述の論文も述べています。従って、オゾン注入のような非侵襲的手技の開拓は、市場の成長を押し上げると予想されます。

さらに、市場参入企業によるさまざまな開拓も市場成長を高めると予想されます。例えば、2022年4月、Genexa社は成人用のクリーンなアセトアミノフェン鎮痛剤を発売しました。アセトアミノフェンは骨壊死の治療に用いられることが多いです。

したがって、高齢者人口の増加や非侵襲的な治療法の市場開拓の高まりといった前述の要因により、本調査の予測期間中に市場は成長を遂げると予想されます。しかし、骨壊死治療に伴う副作用が市場成長の妨げになると予想されます。

骨壊死治療市場の動向

骨壊死治療市場では、骨置換デバイス/インプラントセグメントが大きな市場シェアを占める見込み

骨移植(グラフト)手術は、血管壊死に罹患した骨の部位を強化するのに役立ち、使用されるグラフトは体の別の部位から採取した健康な骨の一部です。関節置換術は、罹患した骨が崩壊していたり、他の治療法では効果がない場合にも行われます。手術によって、関節の損傷部分をプラスチックや金属の部品に置き換えることができます。骨置換手術の利点が増加していることが、市場の成長を促進する主な要因です。骨壊死の有病率増加に伴う老人人口の増加も、骨置換術を増加させています。

NCBIが2022年11月に更新した記事によると、股関節骨壊死の患者の多くは、非侵襲的な処置や投薬が効果的でないことが判明したため、最終的に人工股関節全置換術が必要になります。同論文はまた、股関節骨壊死に対して人工股関節全置換術が適応となるのは、患者が40歳以上で病変が大きい場合、または若年で大腿骨頭の崩壊が進行し寛骨臼が変性している場合であると述べています。大腿骨と寛骨臼の両方にセメントを使用しない人工骨臼が主に使用され、痛みの軽減と機能的改善という点で、通常、治療成績は良好です。このように、骨置換術によってもたらされる利点が、この分野の成長を押し上げると予想されています。

さらに、国連のWorld Population Prospects 2022によると、2022年には世界人口の10%が65歳以上の高齢者になると推定されており、2050年には16%に上昇すると予想されています。高齢者は骨置換術を採用する可能性が高いため、高齢者人口の増加はこのセグメントの成長を高めると予想されます。

このように、老年人口の増加や骨置換術が提供する利点などの前述の要因により、調査対象セグメントは調査予測期間中に成長を経験すると予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米は、高齢者人口の増加や、同地域における疾患の診断に関する人々の意識の高まりにより、骨壊死治療市場において大きな市場シェアを占めると予想されています。例えば、カナダ統計局(Statistics Canada)が2022年7月に発表したデータによると、2022年のカナダの65歳以上の人口は約733万1,605人で、総人口の18.8%を占め、40~44歳の人口は約257万3,624人と推定されています。

さらに、同地域では骨壊死の有病率が高いことも、市場の成長を高めると予想されています。例えば、NCBIが2022年11月に更新した論文によると、米国では人工股関節全置換術の10%が血管壊死または骨壊死によるものと推定されており、一般的に30~65歳が罹患しています。さらに、米国では老年人口が増加していることも、市場の成長を大きく伸ばすと予想されています。例えば、国連人口基金2022年ダッシュボードによると、米国では2022年に17%の人が65歳以上になると推定されています。

さらに、市場プレイヤーによる様々な開拓も市場成長を高めると予想されます。例えば、2022年6月、Strides Pharma社はイブプロフェンOTC経口懸濁液50mg/1.25mLの米国FDA(USFDA)承認を取得しました。イブプロフェンは非ステロイド性抗炎症薬で、骨壊死の治療によく使用されます。

このように、高齢者人口の増加や骨壊死の有病率の上昇といった前述の要因により、調査対象市場は調査予測期間中に同地域で成長を遂げると予想されます。

骨壊死治療産業の概要

骨壊死治療市場は適度に細分化されており、複数の主要企業で構成されています。市場各社は新製品開発のための研究開発に注力しています。市場で事業を展開している大手企業には、Novartis AG、Pfizer Inc.、Teva Pharmaceutical Industries Ltd.、Viatris Inc.、Zimmer Biomet、Merck &Co.Inc.、Enzo Biochem Inc.、Atnahs、Bone Therapeutics SA、Vericel Corporationなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高齢者人口の増加に伴う世界の骨壊死の負担増

- 非侵襲的治療への需要の高まりと技術の進歩

- 市場抑制要因

- 骨壊死治療に伴う副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- 治療タイプ別

- 医薬品

- 非ステロイド性抗炎症薬

- コレステロール低下薬

- 血液希釈剤

- その他の薬剤

- 骨補填器具/インプラント

- 医薬品

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Novartis AG

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd

- Viatris Inc.

- Zimmer Biomet

- Enzo Biochem Inc.

- Bone Therapeutics SA

- Exactech, Inc.

- Strides Pharma Science Limited

- Perrigo Company plc

- Dr. Reddy's Laboratories

- AFT Pharmaceuticals

第7章 市場機会と今後の動向

The osteonecrosis treatment market is expected to register a CAGR of 6.2% during the forecast period.

The COVID-19 pandemic had a significant impact on the studied market, as osteonecrosis or avascular necrosis was a very common complication that was found in COVID-19 patients. Thus, the rising COVID-19 cases during the early pandemic also increased osteonecrosis cases among patients.

For instance, According to an article published by MDPI in November 2021, avascular necrosis (AVN) is a known complication after steroid treatment of severe COVID-19 infections or long-term COVID-19 infections. AVN can also develop shortly after a COVID-19 infection without prior steroid treatment. Apparently, COVID-19 infection alone may represent a risk factor for developing AVN, and it is estimated that, on average, AVN begins 2 weeks after COVID-19 onset in contrast to long COVID-19 late-onset AVN. Thus, the pandemic had a significant impact on market growth. However, as the pandemic has subsided, COVID-19-osteonecrosis cases have started to decrease, so the studied market is expected to have stable growth due to the high burden of the disease due to various other factors during the forecast period of the study.

The rise in the geriatric population increases the incidence of osteonecrosis worldwide. The growing demand for non-invasive treatment and technological advancements for a better treatment for osteonecrosis are the key driving factors in the osteonecrosis treatment market.

Old age is often associated with the increasing prevalence of osteonecrosis. For instance, according to an article updated by NCBI in November 2022, SONK (Spontaneous Osteonecrosis of the Knee) is more common in older persons, and a unicompartmental knee replacement provides a good functional outcome with a relatively short rehabilitation time. Moreover, according to the data published by WHO in October 2022, it is estimated that 1 in 6 people in the world will be aged 60 years or over by 2030, and the share of the population aged 60 years and over will increase to 1.4 billion by 2030. Thus, the rising geriatric population is expected to increase the demand for osteonecrosis treatment products.

Moreover, the development of various non-invasive tools for the treatment of osteonecrosis is expected to enhance the growth of the market. For instance, according to an article published by PubMed Central in September 2022, medication-related osteonecrosis of the jaw (MRONJ) is considered a serious adverse reaction, mainly due to bone-modifying agents (BMA), and for patients with advanced disease stages who are unsuitable for surgery, prolonged medical treatment is required, which comes with a consequent risk of the overuse of antibiotics and antibiotic resistance.

The abovementioned article also stated that ozone injections could be an innovative, powerful, and effective non-invasive tool for nonoperative MRONJ treatments, especially when operative (invasive) procedures could be an additional burden for complicated cases and medical challenges. Thus, the development of non-invasive techniques, such as ozone injections, is expected to boost the market growth.

Additionally, various developments by market players are also expected to enhance market growth. For instance, in April 2022, Genexa launched a clean acetaminophen pain relief product for adults. Acetaminophen is often used for the treatment of osteonecrosis.

Hence, due to the aforementioned factors, such as the rising geriatric population and the rising development of non-invasive treatment options, the market is expected to experience growth during the forecast period of the study. However, adverse side effects associated with osteonecrosis treatment are expected to impede market growth.

Osteonecrosis Treatment Market Trends

The Bone Replacement Devices/Implants Segment is Expected to Hold a Significant Market Share in the Osteonecrosis Treatment Market

The bone transplant (graft) procedure can help strengthen the area of bone affected by avascular necrosis, and the graft used is a section of healthy bone taken from another part of the body. Joint replacement surgery is also performed if the affected bone has collapsed or other treatments aren't helping. Surgery can replace the damaged parts of the joint with plastic or metal parts. The increasing advantages of bone replacement surgeries are a major factor driving the growth of the market. The rising geriatric population associated with the increasing prevalence of osteonecrosis is also increasing bone replacement procedures.

According to an article updated by NCBI in November 2022, many patients with hip osteonecrosis will ultimately need a total hip arthroplasty as non-invasive procedures and medications prove to be ineffective. The article also stated that total hip arthroplasty is indicated for hip osteonecrosis when patients are older than 40 years and have large lesions or are young with more advanced femoral head collapse and degenerated acetabulum. Cementless prosthesis for both the femur and acetabulum is predominantly used, and outcomes are usually good in terms of pain reduction and functional improvement. Thus, the advantages offered by bone replacement procedures are expected to boost segment growth.

Moreover, according to the United Nations World Population Prospects 2022, it is estimated that 10% of the global population will be aged 65 years or older in 2022, and this is expected to rise to 16% by 2050. As older people are more likely to adopt bone replacement procedures, the rising geriatric population is expected to enhance the growth of the segment.

Thus, due to the aforementioned factors, such as the rising geriatric population and the advantages offered by bone replacement procedures, the studied segment is expected to experience growth during the forecast period of the study.

North America is Expected to Hold a Significant Share in the Market during the Forecast Period

North America is expected to hold a significant market share in the osteonecrosis treatment market due to an increase in the geriatric population and growing awareness among people about the diagnosis of the disease in this region. For instance, according to the data published by Statistics Canada in July 2022, it is estimated that around 7,330,605 people were aged 65 years or older in Canada in 2022; this accounts for 18.8% of the total population, and around 2,573,624 people were aged 40 to 44 in Canada.

Furthermore, the high prevalence of osteonecrosis in the region is also expected to enhance market growth. For instance, according to an article updated by NCBI in November 2022, it has been estimated that ten percent of total hip arthroplasties in the United States are due to avascular necrosis or osteonecrosis, and it typically affects ages 30 to 65 years old. Moreover, the rising geriatric population in the United States is also expected to significantly increase the market growth. For instance, according to the United Nations Population Fund 2022 dashboard, it is estimated that 17% of people are 65 years and older in the United States in 2022.

Additionally, various developments by market players are also expected to enhance market growth. For instance, in June 2022, Strides Pharma received the United States FDA (USFDA) approval for ibuprofen OTC oral suspension 50mg/1.25mL. Ibuprofen is an NSAID that is often used for the treatment of osteonecrosis.

Thus, due to the aforementioned factors, such as the rising geriatric population and the rising prevalence of osteonecrosis, the studied market is expected to experience growth in the region during the forecast period of the study.

Osteonecrosis Treatment Industry Overview

The osteonecrosis treatment market is moderately fragmented and consists of several major players. The market players are focusing on research and development for development of new products. Some of the leading companies operating in the market include Novartis AG, Pfizer Inc., Teva Pharmaceutical Industries Ltd, Viatris Inc., Zimmer Biomet, Merck & Co. Inc., Enzo Biochem Inc., Atnahs, Bone Therapeutics SA, and Vericel Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Burden of Osteonecrosis Worldwide Coupled with Rise in Geriatric Population

- 4.2.2 Growing Demand for Non-invasive Treatment and Technological Advancements

- 4.3 Market Restraints

- 4.3.1 Adverse Side Effects Associated with Osteonecrosis Treatment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Treatment Type

- 5.1.1 Drugs

- 5.1.1.1 Nonsteroidal Anti-Inflammatory Drugs

- 5.1.1.2 Cholesterol-Lowering Drugs

- 5.1.1.3 Blood Thinners

- 5.1.1.4 Other Drugs

- 5.1.2 Bone Replacement Devices/Implants

- 5.1.1 Drugs

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Novartis AG

- 6.1.2 Pfizer Inc.

- 6.1.3 Teva Pharmaceutical Industries Ltd

- 6.1.4 Viatris Inc.

- 6.1.5 Zimmer Biomet

- 6.1.6 Enzo Biochem Inc.

- 6.1.7 Bone Therapeutics SA

- 6.1.8 Exactech, Inc.

- 6.1.9 Strides Pharma Science Limited

- 6.1.10 Perrigo Company plc

- 6.1.11 Dr. Reddy's Laboratories

- 6.1.12 AFT Pharmaceuticals