|

市場調査レポート

商品コード

1405720

大麻入り食用製品:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Cannabis Infused Edible Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 大麻入り食用製品:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

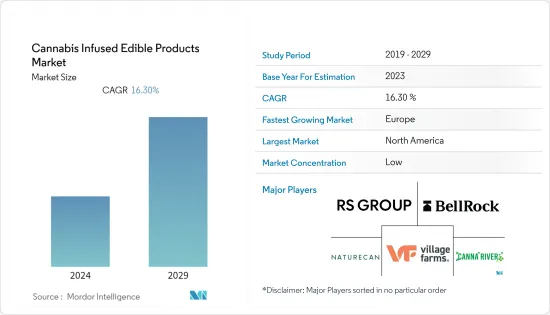

大麻入り食用製品市場規模は、2024年の112億6,000万米ドルから2029年には239億6,000万米ドルに成長すると予測され、予測期間中のCAGRは16.30%です。

主なハイライト

- エディブルは目立たず、消費者が知らず知らずのうちにむさぼることができるという事実が、消費者の嗜好を喫煙からエディブルへとシフトさせています。食品セクターは、消費者の需要に後押しされた新しい大麻ベースの食品をリリースすることで、現在の市場動向に対応しています。これまでのところ、食品に利用されている大麻から抽出された最も一般的な活性化学物質はカンナビジオール(CBD)とテトラヒドロカンナビノール(THC)で、これらは治療特性を示すことが分かっています。大麻を含むと主張する嗜好品の数は、近年爆発的に増加しています。ピザ、ロリポップ、チョコレート、朝のシリアル、グミの一貫品、チョコレートクッキー/ブラウニー、飲食品、牛肉製品などは、大麻を注入し、健康を促進する成分を運ぶと主張する製品のほんの一部であり、したがって、大麻化学物質を食品に組み込む斬新な方法です。

- このような人気の高まりにより、エディブルは米国の小売店のほとんどに浸透しているが、そこでは州によって大麻または大麻を規制する法律が定められています。欧州の大麻エディブル分野は、大麻業界で最も急成長しているカテゴリーと考えられており、グミやインフューズド・ドリンクなどのサブカテゴリーが近年著しい成長を遂げています。例えば、バーゼル大学中毒学部によると、スイスは2023年9月、大麻合法化の効果を調査するため、欧州で初めて大麻販売試験プログラム「ウィード・ケア」を開始する予定です。調査対象は18歳以上のプログラム参加者370人で、調査期間中は参加者の大麻摂取習慣や心身の健康全般がモニターされます。

- さらに、ほとんどの大麻食用は、製品が目立たず、使いやすく、安全で、正確な用量を必要とする現代の消費者の需要に対応しています。例えば、2022年3月、RSグループはCAMU C Plus with Hempを発売し、白ブドウ果汁、麻エキス、γ-アミノ酪酸(GABA)、カムカムエキスをブレンドしたビタミンC飲料のデビューを飾った。さらに、市場初のCBDエキス入り機能性ショットとして、革新的な製品であるCAMU C CBDショットを発表しました。

- スナックや飲料などの大麻入り製品は、インスタグラムやフェイスブックなどのソーシャルメディア動向の影響により、若い世代の消費者の間で特に人気が出ると予想されます。この要因によって、大麻入り製品メーカーが消費者への訴求力を高め、市場で競合優位に立つための製品イノベーションが増加すると予想されます。

大麻入り食用製品の市場動向

マイクロドージングに関する特許とコラボレーションの増加

- エディブルや飲料における大麻の微量摂取は、今後数年間で、いくつかの重要な新たな高みを設定する可能性が高いです。大麻の娯楽的かつ実用的な食品成分としての可能性に対する人々の理解は、より多くの人々が注入されたエディブルを試すにつれて大きく広がっています。

- 食品・飲料業界の大手企業だけでなく、多くの新規事業者が、ここ数年の間に、そうした販売が許可されている州でカンナビノイド入り商品を導入する可能性を調査しています。現在、大麻は世界33の州で医療用として認められており、21歳以上の個人を対象としています。

- コンステレーション・ブランズ、MPX、Gfarmalabs、スプリグといった大手企業が大麻入り飲料の開発に着手しており、それに続き、HEMP20とTHCファーマもこの領域に徐々に進出しています。現在、カナダの研究開発会社Province Brandsのような斬新なブランドが、大麻から醸造した世界初のアルコールフリービールを発売する予定です。HEMP20のような企業は、体内吸収率の向上を可能にするDehydraTECHの技術で特許を取得しています。

- 業界全体のコラボレーションは大規模で、コンステレーションやキャノピー・グロースといったブランドが大麻ベースの飲料市場を開拓しています。一方、AB InBevとTilrayは、カナダ市場向けに例外的に大麻入りノンアルコール飲料を調査するため、1億米ドルのベンチャーを立ち上げました。

北米が大麻入り食用製品市場をリード

- 大麻は、吐き気、嘔吐、痛みといったがん関連の症状やがん治療の副作用を軽減する上で有望な可能性を秘めています。現在、大麻のこのような機能性を安全に実証し、一般の人々の間で使用されるようにするための調査が行われています。大麻の他の潜在的な機能性には、心臓の健康に役立つこと、薬物乱用治療、膠芽腫患者の延命の可能性などがあります。

- 経済協力開発機構(OECD)のデータによると、2028年までにメキシコの医療用大麻市場は13億米ドル以上になると予想されています。また、北米における娯楽用大麻の市場規模は6億5,500万米ドル近くになると予測されています。

- また、2021年のカナダ政府による大麻規制のための調査によると、カナダ人の10人中7人は、大麻に関してオンラインで見つけた情報は、教養ある判断をするのに十分な信頼性があると考えており、過去1年以内に大麻を使用したことがある人は、この割合が約90%に上ります。

- 16歳以上のカナダ人のうち、過去12ヵ月を通じて大麻を使用したと回答した人の割合は、2020年は25%、2021年は26%で、毎日またはほぼ毎日使用する頻度はほぼ一定でした。16歳から24歳のティーンエイジャーとヤングアダルトの使用率は、2020年の23%から2021年には29%に増加しました。喫煙は依然として大麻を摂取する最もポピュラーな方法であるにもかかわらず、VAPEペンのようなデバイスを使ったVAPEや、飲むだけでなく、その局所的な用途への動向は、調査によると2020年以降増加しています。

- さらに、パッケージも売れ行きを左右する大きな役割を果たしており、平均すると、エディブルのパッケージは1食あたり100mg前後で、価格が上乗せされています。一方、カナダも1回分10mg前後のエディブルの小売販売拡大に力を入れています。しかし、カナダでは、エディブルの供給は当初は限定的だが、規制当局がその使用と安全性の肯定的側面を感じ取るにつれて、将来的には増加すると思われます。

大麻入り食用製品産業の概要

世界の大麻入り嗜好品市場は、様々な地域および世界の企業が存在する断片化された市場です。市場に存在する主な企業は、BellRock Brands Inc.(Dixie Elixirs)、Canna River、RS Group、Village Farms International Inc.、Naturecan Ltd.などです。製品イノベーションは、各社が製品ラインナップを拡大し、他の企業に対する競合優位性を獲得するために使用する主要な手段であることが分かっています。

プライベートブランドは、多様な製品を提供し、市場で大きなシェアを占めています。調査対象市場では、ナチュラル、オーガニック、持続可能な実践を謳う確立された主要製品が、小売店の棚やオンライン・チャネルに高い浸透率を示しています。しかし、国内企業は、消費者を結びつけ、製品とともに体験を提供する優れたストーリーで同じセグメントに対応しており、これも成長しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ

- 食品

- チョコレート

- グミ

- ミント&タルト

- ブラウニー&クッキー

- その他の食品

- 飲料

- エナジードリンク

- フルーツジュース

- ハーブティー

- その他の飲料

- 栄養補助食品

- 食品

- 流通チャネル

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- 専門店

- オンラインストア

- その他の流通チャネル

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他の北米

- 欧州

- スペイン

- 英国

- ドイツ

- フランス

- イタリア

- その他の欧州

- アジア太平洋

- 日本

- オーストラリア

- その他のアジア太平洋

- 世界のその他の地域

- アフリカ

- 南米

- 北米

第6章 競合情勢

- 市場シェア分析

- 最も採用されている戦略

- 企業プロファイル

- Naturecan Ltd

- Cannabinoid Creations

- Hempfusion Wellness Inc.

- Botanic Labs

- RS Group(Lifestar)

- Village Farms International Inc.

- Neurogen

- Spring Cannabis Express

- Canna River

- BellRock Brands Inc.(Dixie Elixirs)

- CBDfx

- Gron Confections(GronCBD)LLC

第7章 市場機会と今後の動向

The cannabis-infused edible products market size is expected to grow from USD 11.26 billion in 2024 to USD 23.96 billion by 2029, at a CAGR of 16.30% during the forecast period.

Key Highlights

- The fact that edibles are inconspicuous and allow consumers to devour unknowingly has shifted consumer preferences from smoking to edibles. The food sector has responded to the current market trends by releasing new cannabis-based food products, which have been driven by consumer demand. So far, the most common active chemicals extracted from cannabis utilized in food are cannabidiol (CBD) and tetrahydrocannabinol (THC), which are found to exhibit therapeutic properties. The number of edibles claiming to contain cannabis has exploded in recent years. Pizza, lollipops, chocolate, morning cereal, gummy consistent items, chocolate cookies/brownies, beverages, and beef products are just some of the products infused with cannabis and claim to carry health-promoting components and thus is a novel way to incorporate cannabis chemicals into food products.

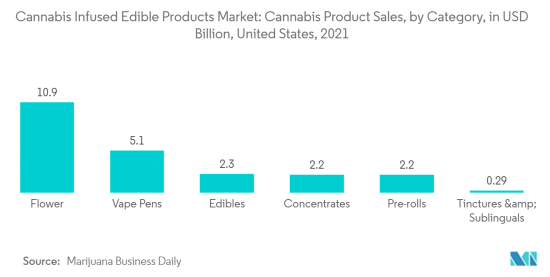

- This growing popularity has led edibles to penetrate most of the United States retail, where the state must have some specific cannabis or marijuana-regulated laws. The cannabis edibles segment in Europe is considered to be the fastest-growing category in the cannabis industry, with the likes of sub-categories such as gummies and infused drinks having witnessed a significant growth trajectory in recent years. For instance, according to the Addiction Department of Basel University, Switzerland is to become the first European country to launch a cannabis sales pilot program, namely the "Weed Care" trial program, to study the effects of cannabis legalization in September 2023, which is expected to run for 2.5 years, until March 2025. The survey will include 370 of the program's participants over the age of 18, and the participants' cannabis consumption habits, as well as their overall physical and mental health, will be monitored during the study.

- Moreover, most of the cannabis edible addresses the demand of modern consumers, where the products need to be discreet, easy to use, safe, and of accurate dosages. For instance, in March 2022, RS Group launched CAMU C Plus with Hemp, marking the debut of a vitamin C beverage blended with white grape juice, hemp extract, gamma-aminobutyric acid (GABA), camu camu extract, boasting an impressive 200% vitamin C content. Additionally, they unveiled CAMU C CBD Shot, an innovative product as the market's inaugural CBD extract-infused functional shot.

- Cannabis-infused products such as snacks and beverages are expected to become especially popular among consumers belonging to younger generations owing to the influence of social media trends on platforms such as Instagram and Facebook. This factor is expected to increase product innovations by cannabis-infused product manufacturers to increase their appeal among consumers and to gain a competitive edge in the market.

Cannabis-infused Edible Products Market Trends

More Patents and Collaborations with Micro-dosing

- The micro-dosing of cannabis in terms of edibles and beverages is likely to set some significant new heights over the coming years. People's understanding of cannabis's potential as a recreational and utilitarian food ingredient has expanded greatly as more people experiment with infused edibles.

- Many new businesses, as well as some of the biggest names in the food and drink industry, have been investigating the potential for introducing cannabinoid-infused goods in states where such sales are permitted within the previous few years. Currently, cannabis is allowed for medical use in 33 states across the globe and for individuals over 21 years of age.

- With the big names in the portfolio, such as Constellation Brands, MPX, Gfarmalabs, and Sprig, which have started their work on cannabis-infused drinks, following them, HEMP20 and THC Pharma are also moving slowly into the domain. New launches are expected from the cannabis industry over the coming years, where, at present, novel brands such as Province Brands, a Canadian Research and development company, are set to release the world's first alcohol-free beer brewed from cannabis. Firms such as HEMP20 have patented a technology on DehydraTECH that enables an increase in the internal absorption rate.

- The collaboration across the industry is massive, and brands such as Constellation and Canopy Growth are developing the market for cannabis-based beverages. On the other hand, AB InBev and Tilray have ventured into a USD 100 million venture to research cannabis-infused non-alcoholic drinks exceptionally for the Canadian Market.

North America Leads the Cannabis-infused Edibles Market

- Cannabis holds promising scope in reducing cancer-related symptoms and side effects of cancer treatment, such as nausea, vomiting, and pain. Currently, research is being conducted to safely demonstrate this functionality of cannabis and bring its use among the general population. Other potential functionalities of cannabis include benefiting heart health, substance abuse treatment, and possible extension of life in those with glioblastoma, among other factors.

- According to the Organisation for Economic Co-operation and Development (OECD) data, by the year 2028, it is expected that the market for medical cannabis in Mexico will be worth more than USD 1.3 billion. The value of the recreational cannabis market in the North American nation is projected to be close to USD 655 million.

- In addition, according to a survey for the regulation of cannabis by the Government of Canada in 2021, 7 out of 10 Canadians believe the information they find online regarding cannabis is reliable enough to help them make educated decisions, and persons who have used cannabis within the past year, this rises to about 90%.

- The percentage of Canadians aged 16 and up who reported using cannabis throughout the previous 12 months was 25% in 2020 and 26% in 2021, with the frequency of daily or practically daily use remaining essentially consistent. Teens and young adults aged 16 to 24 increased their use from 23% in 2020 to 29% in 2021. Even though smoking is still the most popular way to consume cannabis, trends towards vaping with devices like vape pens and drinking it, but its topical applications have increased since 2020, as per the survey.

- Furthermore, packaging has also played a major role in determining sales, where, on average, the packages of edibles were around 100 mg per serving with an add-on price. On the other hand, Canada is also focusing on expanding its retail sales of edibles with single servings, which constitute around 10mg of edibles. However, in Canada, the supply of edibles will be limited to begin with but will increase in the future as regulators sense the positive aspect of its usage and safety.

Cannabis-infused Edible Products Industry Overview

The global cannabis-infused edibles market is a fragmented market with the presence of various regional and global players. The major players present in the market are BellRock Brands Inc. (Dixie Elixirs), Canna River, RS Group, Village Farms International Inc., and Naturecan Ltd., among others. Product innovation is found to be the major tool used by the players to expand their offerings and, thus, gain a competitive advantage over other players.

Private-label brands hold a prominent share of the market with diversified product offerings. In the market studied, established major products that claim to be natural, organic, and involved in sustainable practices have a higher penetration across retail shelves and online channels. However, domestic players cater to the same segment with a better storyline that connects consumers and delivers experiences with the product, which is also growing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Food

- 5.1.1.1 Chocolates

- 5.1.1.2 Gummies

- 5.1.1.3 Mints & Tarts

- 5.1.1.4 Brownies & Cookies

- 5.1.1.5 Other Food

- 5.1.2 Beverages

- 5.1.2.1 Energy Drinks

- 5.1.2.2 Fruit Juices

- 5.1.2.3 Herbal Tea

- 5.1.2.4 Other Beverages

- 5.1.3 Dietary Supplements

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience stores

- 5.2.3 Specialist stores

- 5.2.4 Online Retail Stores

- 5.2.5 Other Distribution Channels

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 Japan

- 5.3.3.2 Australia

- 5.3.3.3 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Africa

- 5.3.4.2 South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Most Adopted Strategies

- 6.3 Company Profiles

- 6.3.1 Naturecan Ltd

- 6.3.2 Cannabinoid Creations

- 6.3.3 Hempfusion Wellness Inc.

- 6.3.4 Botanic Labs

- 6.3.5 RS Group (Lifestar)

- 6.3.6 Village Farms International Inc.

- 6.3.7 Neurogen

- 6.3.8 Spring Cannabis Express

- 6.3.9 Canna River

- 6.3.10 BellRock Brands Inc. (Dixie Elixirs)

- 6.3.11 CBDfx

- 6.3.12 Gron Confections (GronCBD) LLC