|

市場調査レポート

商品コード

1851921

デガウスシステム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Degaussing Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| デガウスシステム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月01日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

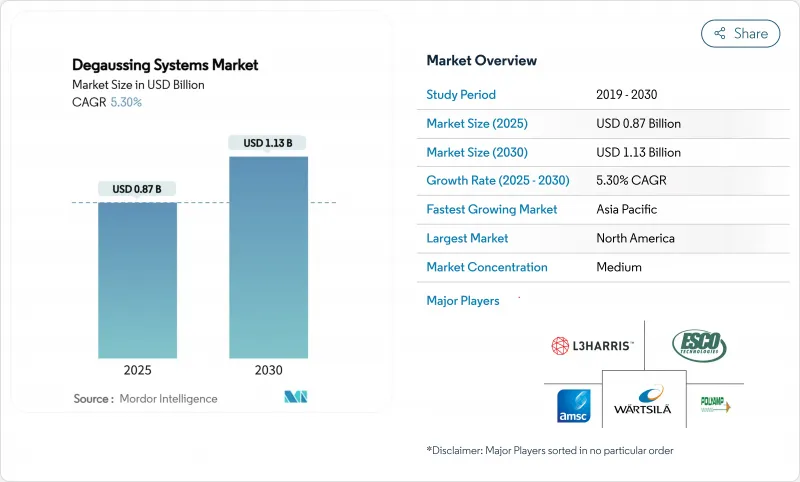

デガウスシステムの市場規模は2025年に8億7,000万米ドルと推計され、2030年には11億3,000万米ドルに達し、CAGR 5.3%で成長すると予測されています。

海軍経費の増加、磁気影響型機雷の高度化、艦隊寿命延長プログラムの着実なペースがこの拡大を支えています。北米の駆逐艦や巡洋艦のアップグレード、欧州の機雷掃海艇の調達、アジア太平洋の潜水艦フリートの拡大が、電磁シグネチャ制御の広範な顧客基盤を確保しています。高温超電導(HTS)コイルとソフトウエア定義制御ユニットが技術更新サイクルを促進する一方、人工知能(AI)アルゴリズムがコイル電流をリアルタイムで調整することで性能のしきい値を押し上げます。レトロフィット需要が契約活動を支配しているのは、海軍がシグネチャーマネジメントを、新造船に出費することなく船の寿命を延ばす費用対効果の高い方法と見なしているからです。HTSテープと希土類磁気センサーをめぐるサプライチェーンの圧力は短期的な成長を抑制するが、垂直統合されたコンポーネントラインを持つティアワンベンダーは、ほとんどの混乱を緩和します。

世界のデガウスシステム市場の動向と洞察

海軍近代化予算の増加がデガウスシステムへの投資を加速

国防予算の着実な増加により、複数年にわたる艦船のアップグレードパイプラインが活発化しています。米国海軍の駆逐艦寿命延長パッケージでは、電子戦強化の中核としてシグネチャ管理の改修が予定されています。イタリアの機雷掃海艇プログラムでは、低磁気音響技術が基本的な装備として盛り込まれています。フィリピンとカナダにおける同様の調達青写真は、デガウスシステム市場の長期的な滑走路を確固たるものにしています。

磁気影響型海底地雷の配備拡大が磁気信号制御の需要を促進

最新の地雷は磁気、音響、圧力センサーを組み合わせ、精密な磁場抑制の要件を高めています。インドのマルチインフルエンス地雷の検証は、海軍プランナーが対抗しなければならない殺傷力の高まりを例証しています。歴史的な損失数値は、機雷が依然として最も費用対効果の高い対水上兵器であることを明らかにしており、ブルーウォーターおよび沿岸の艦船全体で強固なディガウスの必要性を裏付けています。

高騰する設備投資と長期的なメンテナンス・コストは、より広範な採用を制限します。

先進的なデガウスシステムに関連する多額の先行投資と継続的な運用費用は、特に予算が限られている小規模な海軍部隊にとっては、採用の障壁となります。総合的なデガウス設備は、船舶の総建築費の2~5%を占め、HTSベースのパッケージは、銅コイルによる代替品を40~60%上回るプレミアムを要求されます。極低温冷却プラント、ヘリウムのロジスティックス、認定された技術者など、特殊なライフサイクル・サポートは、中型の戦闘艦の10年間のメンテナンスに200万~400万米ドルを追加します。このような財政的な現実から、海軍はしばしば、優先順位の低い船体に磁気フットプリントを残すことを受け入れながら、全領域のシグネチャ管理を空母、潜水艦、および最前線の駆逐艦に限定せざるを得なくなります。その結果、新興の海洋国家への市場浸透は遅れ、その理由は資本費用が他の戦闘システムのアップグレードを圧迫するからです。

セグメント分析

セグメント合計は、目立たないプラットフォームがいかに支出を支えているかを浮き彫りにしています。潜水艦カテゴリーは2024年のデガウスシステム市場売上高の29.65%を占めるが、水雷対策艦はCAGR7.89%で最も急速に拡大します。この性能差は、影響力のある機雷による脅威が顕著であることと、氷点下や沿岸での隠蔽が戦略上重要であることを反映しています。オーストラリア、インド、韓国の潜水艦計画では、設計段階でフルハルコイルセットを統合しており、後付けが一般的な水上艦とは対照的です。水雷掃海艇の船体はすでに低フェライト複合材で作られているが、残留磁気を砕くために分散型マイクロループを追加しています。駆逐艦やフリゲート艦は、レーダーやソナーの更新サイクルと時期を同じくして中期のアップグレードが行われるため、デガウスの作業範囲に相乗効果が生まれ、大きな需要を維持しています。

海軍は予算を配分する際、艦船固有のリスク・エクスポージャーを考慮します。潜水艦は継続的な受動的探知リスクに直面するため、ハイスペックな独自素材が正当化されます。逆に、コルベットは、地域の磁気条件に合わせて定格化された標準化されたコイルモジュールを使用してコストを分散するモジュールアーキテクチャを採用しています。このような微妙な組み合わせにより、サプライヤーは、制御コードを書き換えることなく、30メートルの無人船から10万トンの輸送船まで、設定可能なシステムを実戦投入することを余儀なくされています。

2024年の売上高の60.90%を占めたのは連続的なデガウスシステムであり、これがベースラインとして適合していることを強調しています。脱磁力は依然として中核であるが、最新の鋼材は極地通過を繰り返しても高い残留磁力を維持するため、脱磁力が再浮上しています。2030年までのCAGRが6.12%であることは、海軍が地雷のあるチョークポイントに配備する前に、定期的な消磁を重要な保険と見なしていることを裏付けています。現在の桟橋側の消磁ケージは、従来の半分の処理時間で95.5%の磁束密度低減が可能なパルス直流技術を採用しています。さらに、持ち運び可能な駆除マットにより、フリゲート艦はホームドックに戻ることなく、パトロール中にシグネチャをリセットすることができます。

より小さなニッチではあるが、測距施設は経験的な磁場データを提供することでフィードバックループを閉じる。ソフトウェア解析は、これらの測定値をコイル電流設定値に外挿し、低収益セグメントでさえ、より利益率の高いデジタルサービスへのプルスルーを生み出すことを実証しています。

地域分析

北米は2024年の売上の34.17%を占めました。米国海軍の駆逐艦と巡洋艦の耐用年数延長契約だけで、国産のコイル、磁力計、制御ユニットを好む数十億米ドルのパイプラインが維持されています。カナダのキングストン級のデガウス改修と同盟国の対外軍事販売(FMS)事例は、この地域の地位をさらに強化しています。3つのHTSテストベッドが認定され、北米のヤードは世界で最も先進的な超電導配備プログラムをホストしています。

アジア太平洋地域は、2030年まで最高のCAGR 8.80%を記録します。防衛予算の増加とシーレーンの争奪が需要を促進します。日本は、もがみ級フリゲート艦のHTS試験を拡大し、オーストラリアのAUKUS潜水艦の試みは、従来の基準を上回る磁気シグネチャ管理基準を統合します。インドの水雷計画は、東南アジアの沿岸艦隊の拡大と相まって、無人プラットフォーム用のマイクロデガウス・ソリューションの採用を加速させています。中国の造船所は、新造の054B型にAI駆動のフィールドチューニング・ソフトウェアを組み込み、この地域の技術ペースを設定し、同業他社に追いつくよう促しています。

欧州は、NATOのバルト海と北極圏の態勢によって活気づき、依然として極めて重要です。イタリアの機雷掃海構想やフランスのFDIフリゲート艦シリーズには、システム・オブ・システムズの調達を推進する駆逐と測距の組み合わせが組み込まれています。英国の31型計画では、デジタル・ツインで検証されたコイル・レイアウトが標準仕様となっており、磁気衛生に対する地域のコミットメントが強調されています。極地調査砕氷船への並行投資は、戦闘機以外の収益源を多様化し、デガウジングベンダーに民間海事ニッチを導入します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 海軍近代化予算の増加により消磁システムへの投資が加速

- 磁気の影響を受ける海上機雷の配備が増加し、磁気シグネチャー制御の需要が高まる

- 旧式の水上艦艇を対象としたレトロフィット・イニシアチブの拡大。

- コンパクトで効率的なシステムを可能にする高温超電導(HTS)コイル技術の出現

- リアルタイムのシグネチャ管理のためのAIを活用した適応アルゴリズムの統合

- ステルス性の高い無人地上・水中ビークルのシステムに対する要求の高まり

- 市場抑制要因

- 高騰する資本支出と長期的なメンテナンス・コストにより、より広範な採用が制限されます。

- 複雑な防衛調達手続きによる取得スケジュールの延長

- 新興レールガンおよび指向性エネルギー兵器システムへの資源再配分により、資金調達の可能性が低下

- HTSテープと希土類ベースの磁気センサーのサプライチェーンの脆弱性が生産の拡張性を妨げる

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 船舶タイプ別

- 航空母艦

- 駆逐艦

- フリゲート

- コルベット

- 潜水艦

- 対機雷戦艦艇

- その他の船舶タイプ

- ソリューション別

- デガウジング

- デパーミング

- レンジング

- コンポーネント別

- コントロールユニット(DCU)

- パワーアンプ

- コイルとケーブル

- 磁力計とセンサー

- ソフトウェアと分析

- 設置タイプ別

- 新設

- レトロフィット

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州地域

- 南米

- ブラジル

- その他南米

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- L3Harris Technologies Inc.

- Wartsila Corporation

- Polyamp AB

- Larsen & Toubro Limited

- Exail SAS

- IFEN S.p.A.

- American Superconductor Corporation(AMSC)

- Dayatech Merin Sdn Bhd

- DA Group

- Ultra Electronics Holdings Ltd.

- Babcock International Group

- Thales Group

- ESCO Technologies inc.