心血管治療薬の市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Cardiovascular Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 118 Pages

- 納期

- 2~3営業日

- 商品コード

- 1851196

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

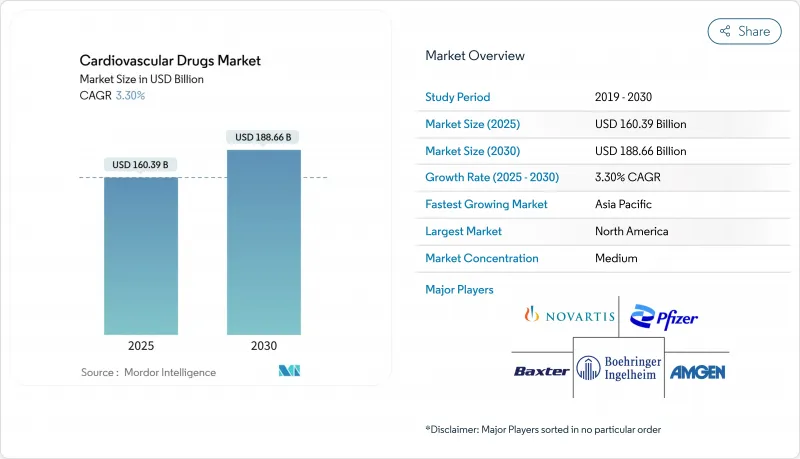

心血管治療薬市場規模は2025年に1,603億9,000万米ドルに達し、2030年には1,886億6,000万米ドルに拡大すると予測され、予測期間中のCAGRは3.30%です。

トップラインの着実な成長には、人口の高齢化、技術革新サイクルの加速、伝統的な臨床試験のエンドポイントよりも実臨床でのエビデンスに報いる政策転換によって形成された深い変化が隠されています。需要は依然として抗凝固薬が中心だが、第XI因子阻害薬、ミネラルコルチコイド受容体拮抗薬、GLP-1受容体作動薬が治療の境界を再定義しつつあります。デジタル販売、サプライチェーンのローカライズ、AIを活用した探索ツールにより、データ主導型の多国籍企業と中小企業との競争格差が広がっています。同時に、特許満了リスクの高まりと単一地域のAPI依存が目先の楽観論を弱め、メーカーはライフサイクル管理への投資と次世代パイプラインへの賭けのバランスを取る必要に迫られています。

世界の心血管治療薬市場の動向と洞察

高齢化社会におけるCVDの有病率の上昇

心不全患者は、2025年の670万人から2030年には850万人に達すると予測されています。高齢の患者は複数の併存疾患を抱えていることが多く、併用レジメンや個別化投与戦略の導入が進んでいます。アジア太平洋地域はこの人口動向を反映しており、慢性疾患管理への需要が高まっています。先進国市場の支払者は、複雑な症例に対する先進的薬剤の償還をすでに行っており、心血管治療薬市場全体の持続的な数量増加を示唆しています。

NOACsとSGLT2阻害薬の急速な普及

新規経口抗凝固薬は引き続きワルファリンに取って代わる一方、SGLT2阻害薬は糖尿病治療から心不全管理へと移行しており、これはFINEARTS-HFにおけるファインレノンの16%のイベント減少が証明しています。セマグルチドなどのGLP-1アゴニストは、心血管系死亡リスク低減の適応でFDAの承認を取得し、代謝と心血管系の治療経路の収束を強調しています。このような治療上の重複は、心血管治療薬市場において新たな対応可能なニッチを開くものです。

特許切れとジェネリックによるブロックバスター・ブランドの侵食

ルピンが発売したリバーロキサバンのジェネリック医薬品は、初年度に最大60%のシェアを獲得する可能性があり、ブランド収益を削り、抗凝固薬クラス全体に価格圧力がかかります。EntrestoとCorlanorにも同様の力学が待ち受けており、既存企業は価値ベースの契約と適応症の多様化を追求せざるを得なくなります。

セグメント分析

抗凝固薬の2024年の心血管治療薬市場シェアは45.14%であり、多様な適応症における血栓塞栓症予防の中心的役割が強調されています。抗凝固薬の心血管治療薬市場規模は、リバーロキサバンのジェネリック医薬品が登場し、ブランド企業が次世代第XI因子阻害薬に移行すれば、近い将来収益の縮小に直面すると予想されます。アベラシマブはリバーロキサバンに対して出血を62~69%減少させ、差別化された代替薬として位置づけられています。一方、心不全治療薬のCAGR 3.70%は、駆出率が維持された患者に対するミネラルコルチコイド受容体拮抗薬とSGLT2阻害薬に対する臨床医の信頼を反映しています。

第2層のカテゴリーは、異なる道を示しています。抗高血圧薬はガイドラインの閾値が拡大され、着実な販売量の伸びを支えています。脂質低下剤は、現在第3相試験が進行中のMK-0616のような経口PCSK9候補薬のおかげで再び勢いを増しています。肺高血圧症治療薬は、希少疾患治療薬のインセンティブから恩恵を受け、抗不整脈薬は、アドヒアランスとモニタリングを向上させるデバイスと薬剤の統合によって関連性を増しています。

高血圧症は2024年の心血管治療薬市場規模において28.90%のシェアを維持しており、これは年齢層にわたる幅広い有病率を反映しています。しかし、心不全治療薬は、これまで満たされていなかったニーズに対応するファインレノン製剤とGLP-1製剤を中心に、CAGR 4.01%で拡大する見込みです。心血管治療薬市場では、ティルゼパチドのようなGLP-1作動薬が非糖尿病性心不全患者に有意義な結果をもたらし、対象患者を拡大することが期待されます。冠動脈疾患治療は抗炎症戦略を採用して残存リスクに対処し、脂質異常症治療はリポ蛋白(a)を標的とするRNAベースの治療法へと進化します。

地域別分析

アジア太平洋地域は2024年に34.35%のシェアを獲得して心血管治療薬市場をリードし、中国の調達改革とインドのインフラ拡張によりCAGRは5.25%で他地域を上回る。NRDLの新規上場の71%を地元企業が占めるようになり、多国籍企業に対する国内競争圧力の強化を示唆しています。日本の承認スケジュールの合理化は、最先端治療薬の市場参入をさらに容易にし、GLP-1製剤や次世代抗凝固薬の着実な普及を促進しています。

北米は、画期的な治療薬を迅速に吸収する償還の枠組みに支えられ、依然として極めて重要なイノベーションの中心地です。しかし、インフレ抑制法は価格交渉の不確実性をもたらし、高価値の心血管治療薬の上市戦略を再編する可能性があります。

欧州は、Brexitに関連したロジスティクスの調整が続くもの、並行申請を加速させる規制の調和されたパスウェイの恩恵を受けています。ラテンアメリカでは、ブラジルの優先的マージンに代表されるように、国内生産に向けた政策的な動きが進んでおり、現地化とコスト管理という二重の要請を生み出しています。中東とアフリカは、心血管疾患啓発キャンペーンに沿った段階的な成長を記録しているが、インフラの格差が依然として高コストの生物学的製剤の普及を制限しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高齢化社会におけるCVD有病率の上昇

- NOACsとSGLT2阻害薬の急速な普及

- 新興市場における償還の拡大

- 規制当局によるラベル拡大のための実データへの依存

- AIによるインシリコ再利用がCVパイプラインを加速する

- 市場抑制要因

- 特許切れとジェネリックによるブロックバスターブランドの侵食

- 生物学的製剤と遺伝子ベースのCV治療薬の高コスト

- サプライチェーン・リスクを生む単一地域の原薬調達

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 薬剤クラス別

- 抗高血圧薬

- 抗凝固剤

- 抗血小板剤

- 脂質低下薬

- 心不全治療薬

- 抗不整脈薬

- 肺高血圧症治療薬

- 疾患適応症別

- 高血圧

- 冠動脈疾患

- 心不全

- 不整脈

- 脂質異常症

- 静脈血栓塞栓症

- 投与経路別

- オーラル

- 注射/点滴

- 経皮その他

- 流通チャネル別

- 病院薬局

- 小売薬局

- オンライン薬局

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- Competitive Benchmarking

- 市場シェア分析

- 企業プロファイル

- Pfizer

- Bristol Myers Squibb

- Novartis

- AstraZeneca

- Johnson & Johnson

- Merck & Co.

- Bayer

- Eli Lilly

- Boehringer Ingelheim

- Sanofi

- AbbVie

- Amgen

- Daiichi Sankyo

- Novo Nordisk

- GSK

- Takeda

- Abbott Laboratories

- Roche

- Servier

- Otsuka Pharma

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 118 Pages

- 納期

- 2~3営業日