|

市場調査レポート

商品コード

1405376

航空機用オートパイロットシステム:市場シェア分析、産業動向・統計、成長予測、2024年~2029年Aircraft Autopilot System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用オートパイロットシステム:市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

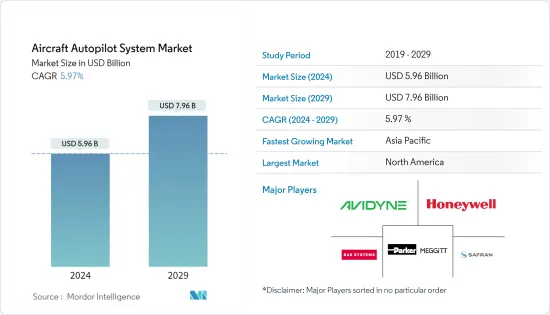

航空機用オートパイロットシステム市場規模は2024年に59億6,000万米ドルと推定され、2029年には79億6,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは5.97%で成長する見込みです。

航空業界の安全要件の強化が市場を牽引しています。フライ・バイ・ワイヤ(FBW)コンセプトの出現により、航空機に高度なフライトコンピュータを搭載する必要があります。さらに、最適な安全レベルを確保し、パイロットの状況認識を強化するため、世界の航空規制機関は、フライトディレクターシステムと連動したオートパイロットシステムの搭載を義務付けています。

自動飛行が可能な先進的な航空機の開拓は、航空機用オートパイロットシステムの研究開発を推進しており、この技術が完全に開発され商業的に実現可能になれば、市場プレイヤーの事業見通しが向上すると予想されます。

さらに、オートパイロットシステムの利用に関する航空当局の厳しい規制により、開発者はオートパイロットシステムの認証を取得するために研究開発の範囲を拡大する必要があります。例えば、欧州連合航空安全機関(EASA)は、航空会社がパイロット1人で航空機を運航するためのさまざまな方法を開発するための提案を提出しました。EASAは、早ければ2027年にも移行が実現するかもしれないと予想しています。EASAの計画では、最小有人運航の拡大(eMCO)とシングルパイロット運航(SiPO)という2つのコンセプトを取り入れる必要があります。このような開発は、シングルパイロット自律化システムとエラーに強いコックピット設計を要求するため、オートパイロットシステム市場を活性化させると思われます。

航空機用オートパイロットシステム市場動向

商業セグメントが市場シェアを独占

ICAOの予測によると、航空輸送需要は20年間で平均して前年比4.3%増加する見込みです。旅客輸送量の増加に対応するため、航空会社は新世代の航空機の調達に乗り出しています。エアバスとボーイングは、2022年に合わせて1,000機以上の航空機を納入し、2023年にはさらに納入を増やす予定です。2022年、ボーイングは737 MAXを561機、ワイドボディを213機、ボーイングの貨物機ラインを78機受注しました。ボーイングはまた、777-8貨物機を50機受注しました。コリンズ・エアロスペースのアビオニクス部門は、エアバスA320、A330、A350 A380、ボーイングB737、B767型機にADF900自動方向探知機を提供しています。また、ボーイングB777型機に冗長デジタル自動操縦装置を備えた自動飛行制御システムを供給しています。ガーミンはエアバスA220型機のオートパイロットシステムのサプライヤーです。

米連邦航空局(FAA)や欧州航空安全機関(EASA)といった主要な航空規制機関は、いくつかの安全上の懸念に対処するため、民間航空機へのオートパイロットシステムの搭載を義務付けています。例えば、2023年8月、アスペンアビオニクスとトリオアビオニクスは、12機種以上の一般旅客機向けに、アスペンエボリューションE5フライトディスプレイとトリオプロパイロットオートパイロットを組み合わせたパッケージで、手頃な価格のデジタルオートパイロット/電子フライトディスプレイ(EFIS)システムをリリースしました。同様に2023年8月には、ユーロコプターAS350 B2でのデモフライトで、ガーミンはGFC 600Hオートパイロットシステムを展示しました。ガーミンは、GFC 600Hシステムの追加型式証明書(STC)の承認取得に取り組んでいます。

アジア太平洋地域が予測期間で市場をリード

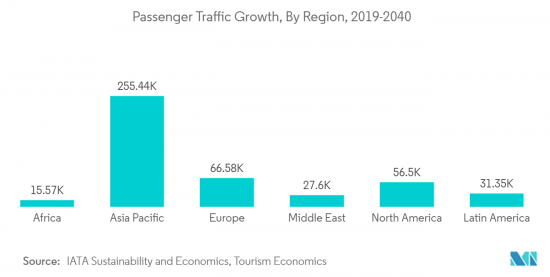

国際空港評議会(ACI)によると、アジア太平洋地域の航空機移動シェアは、2021年の32.5%から2041年には45.2%になると予想されています。中国は、航空輸送量において世界最大の航空市場になると予想されています。同期間中、インドは世界第3位の航空市場に成長すると予想され、インドネシアやタイなどの他の国々は世界市場トップ10に入ると予測されます。新型航空機の需要は、同地域で増え続ける旅客輸送量に牽引されています。

国際的な戦略情勢が大きく変化しているため、国際安全保障システムの構成は、地域紛争の拡大によって損なわれています。軍事力を強化するため、中国やインドなどいくつかの国は、安全保障上の脅威に効果的に対応し、緊急かつ重要で危険な戦略的任務を達成するために、新たな調達に頼っています。例えば、インド空軍は2023年8月、軽戦闘機(LCA)のMk1A型100機を80億米ドルでヒンドゥスタン・エアロノーティックス・リミテッド(HAL)に発注する予定です。Mk1Aバージョンには、最新のアビオニクス、レーダー、電子戦スイート、ミサイル機能が装備されています。

最新の戦闘機には、パイロットの全体的な状況認識を強化するための高度なオートパイロットシステムとフライト・コンピューターが装備されています。航空機需要の増加は、予測期間中、この地域の市場プレイヤーの事業見通しを強化すると予想されます。数多くの軍用機のプロトタイプが開発されている一方で、軍用機の世界の需要に応えるため、現在いくつかの軍事調達プログラムが進行中です。軍用戦闘機メーカーは、タイムリーな納入を確実にするため、生産能力を強化しようとしています。

航空機用オートパイロットシステム産業概要

航空機用オートパイロット市場は断片化されており、市場には少数の世界プレーヤーが存在しています。市場の著名なプレーヤーには、BAE Systems plc、Honeywell International Inc.、Meggitt(Parker Hannifin Corporation)、Avidyne Corporation、Safranなどがあります。航空交通のほか、いくつかの国々で地政学的不安が高まっていることに煽られた新たな安全保障環境が、航空機の需要拡大をもたらしています。長期契約を獲得し、世界のプレゼンスを拡大するため、プレーヤーは新たな航空資産の調達に多額の投資を行っています。さらに、継続的な研究開発により、統合オートパイロット技術と関連サブシステムの精度と効率の向上が促進されています。例えば、2021年10月、Garmin Ltd.は、同社のGFC 500オートパイロットが、Beechcraft 19 Sport、Beechcraft 23 Musketeer/Sundowner、およびBeechcraft 24 Musketeer/Sierra航空機モデルで使用するための補足型式証明(STC)を米連邦航空局(FAA)から取得したと発表しました。同様に2021年6月、ベル・テキストロン社は、ベル505ヘリコプターに組み込まれたジェネシス・ヘリサス自動操縦装置が英国民間航空局(CAA)から認証を取得したと発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- システム

- 姿勢・方位基準システム

- フライトディレクターシステム

- 飛行制御システム

- アビオニクスシステム

- アプリケーション

- 民間・商業

- 軍事

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- BAE Systems plc

- Safran

- Avidyne Corporation

- Honeywell International Inc.

- Meggitt(Parker Hannifin Corporation)

- Collins Aerospace(RTX Corporation)

- Dynon Avionics

- Genesys Aerosystems

- Lockheed Martin Corporation

- Moog Inc.

- THALES

- Garmin Ltd.

第7章 市場機会と今後の動向

The Aircraft Autopilot System Market size is estimated at USD 5.96 billion in 2024, and is expected to reach USD 7.96 billion by 2029, growing at a CAGR of 5.97% during the forecast period (2024-2029).

The enhanced safety requirements of the aviation industry drive the market. The advent of the fly-by-wire (FBW) concept necessitates the integration of advanced flight computers onboard an aircraft. Furthermore, to ensure optimal safety levels and enhance the situational awareness of the pilots, the global aviation regulatory agencies have mandated the installation of an autopilot system in conjunction with the flight director system.

The development of advanced aircraft capable of automated flights is driving the ongoing R&D aspect for aircraft autopilot systems and is anticipated to enhance the business prospects of the market players once the technology is fully developed and becomes commercially feasible.

Moreover, stringent regulations from aviation authorities regarding the utilization of autopilot systems will require the developers to increase their scope of R&D to get their autopilot systems certified. For instance, the European Union Aviation Safety Agency (EASA) has filed a proposal to develop various ways for airlines to operate aircraft with a single pilot. EASA anticipates that the transition might happen as early as 2027. The EASA plan has two concepts that need to be incorporated: extended minimum manned operations (eMCO) and single pilot operations (SiPO). Such developments are going to fuel the autopilot systems market as this will demand single pilot autonomy systems and error-tolerant cockpit designs.

Aircraft Autopilot System Market Trends

Commercial Segment to Dominate Market Share

As Per ICAO estimates, the demand for air transport will likely increase by 4.3% YoY on average over the two decades. To address the passenger traffic growth, airline operators have initiated procurement drives for new-generation aircraft. Airbus and Boeing together exceeded 1,000 aircraft deliveries in 2022, and both are planning to ramp up more deliveries in 2023. In 2022, Boeing received 561 orders for 737 MAX, 213 orders for widebodies, and 78 orders for Boeing's freighter line. Boeing also received 50 orders for 777-8 Freighter aircraft. Collins Aerospace's avionics division is providing ADF 900 Automatic direction finder to Airbus A320, A330, A350 A380, Boeing B737, and B767 aircraft. It also supplies Automatic flight control systems with redundant digital autopilot to Boeing B777 aircraft. Garmin is the supplier of autopilot systems for Airbus A220 aircraft.

The dominant aviation regulatory agencies, such as the Federal Aviation Administration (FAA) and the European Aviation Safety Agency (EASA), have mandated the installation of autopilot systems in commercial aircraft to address several safety concerns. For instance, in August 2023, Aspen Avionics and Trio Avionics released an affordable digital autopilot/electronic flight display (EFIS) system with combined packages of Aspen Evolution E5 flight display and Trio Pro Pilot autopilot for more than 12 general aviation aircraft models. Similarly, in August 2023, in a demo flight in a Eurocopter AS350 B2, Garmin showcased its GFC 600H autopilot system. Garmin is working to receive supplemental-type certificate (STC) approvals for the GFC 600H system.

Asia-Pacific Region to Lead the Market in the Forecast Period

According to Airports Council International (ACI), the Asia-Pacific region is expected to have an aircraft movement share of 45.2% in the year 2041, from 32.5% in the year 2021. China is anticipated to become the world's largest aviation market in terms of air traffic. During the same period, India is anticipated to develop into the world's third-largest aviation market, while other countries, such as Indonesia and Thailand, are forecasted to enter the top 10 global markets. The demand for new aircraft is driven by the ever-growing passenger traffic in the region.

On account of the profound changes in the international strategic landscape, the configuration of the international security system has been undermined by the growing regional conflicts. To enhance military prowess, several countries, such as China and India, have resorted to new procurements to effectively respond to security threats and accomplish urgent, critical, and dangerous strategic missions. For instance, in August 2023, the Indian Air Force plans to give a contract of USD 8 billion for 100 Mk1A variants of Light Combat Aircraft (LCA) to Hindustan Aeronautics Limited (HAL). The Mk1A version is equipped with modern avionics, radar, electronic warfare suite, and missile capabilities.

Modern fighter aircraft are equipped with advanced autopilot systems and flight computers for augmenting the overall situation awareness of the pilot. An increase in demand for aircraft is anticipated to bolster the business prospects of the market players in the region during the forecast period. While numerous military aircraft prototypes are being developed, several military procurement programs are currently underway to cater to the global demand for military aircraft. Military fighter aircraft manufacturers are trying to enhance their production capabilities to ensure timely deliveries.

Aircraft Autopilot System Industry Overview

The aircraft autopilot market is fragmented, with a handful of global players present in the market. Some of the prominent players in the market include BAE Systems plc, Honeywell International Inc., Meggitt (Parker Hannifin Corporation), Avidyne Corporation, and Safran, among others. Besides air traffic, the emerging security environment, fueled by the growing geopolitical unrest in several countries, is resulting in the growing demand for aircraft. In order to gain long-term contracts and expand their global presence, players are investing significantly in the procurement of new aerial assets. Furthermore, continuous R&D has been fostering the advancements of accuracy and efficiency of integrated autopilot technologies and associated subsystems. For instance, in October 2021, Garmin Ltd. announced that its GFC 500 autopilot received Supplemental Type Certification (STC) from the Federal Aviation Administration (FAA) for use in Beechcraft 19 Sport, Beechcraft 23 Musketeer/Sundowner, and Beechcraft 24 Musketeer/Sierra aircraft models. Similarly, in June 2021, Bell Textron Inc. announced that the Genesys HeliSAS autopilot incorporated into the Bell 505 helicopter had received certification from the UK's Civil Aviation Authority (CAA).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 System

- 5.1.1 Attitude and Heading Reference System

- 5.1.2 Flight Director System

- 5.1.3 Flight Control System

- 5.1.4 Avionics System

- 5.2 Application

- 5.2.1 Civil and Commercial

- 5.2.2 Military

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 Safran

- 6.2.3 Avidyne Corporation

- 6.2.4 Honeywell International Inc.

- 6.2.5 Meggitt (Parker Hannifin Corporation)

- 6.2.6 Collins Aerospace (RTX Corporation)

- 6.2.7 Dynon Avionics

- 6.2.8 Genesys Aerosystems

- 6.2.9 Lockheed Martin Corporation

- 6.2.10 Moog Inc.

- 6.2.11 THALES

- 6.2.12 Garmin Ltd.