|

市場調査レポート

商品コード

1910626

機能安全:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Functional Safety - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 機能安全:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

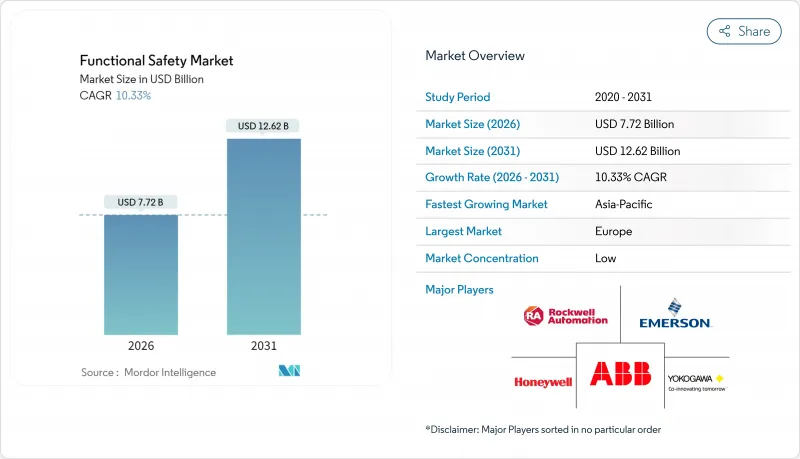

2026年の機能安全市場規模は77億2,000万米ドルと推定され、2025年の70億米ドルから成長が見込まれます。

2031年には126億2,000万米ドルに達し、2026年から2031年にかけてCAGR10.33%で拡大する見通しです。

堅調な需要は、より厳格な世界の基準とインダストリー4.0の導入が交差する現状に起因しており、メーカーは設計段階から安全機能を中核的な自動化プラットフォームに組み込むことを迫られています。石油・ガス・電力施設における事故調査後の規制強化も導入を促進し、急速なデジタル化はハードワイヤードリレーよりもプログラム可能な安全ロジックを好む使用事例を生み出しています。ベンダー各社は、機能安全と企業サイバーセキュリティの統合ニーズからも恩恵を受けています。この動向は、プロセス安全とサイバーレジリエンスを同一分野の二つの側面として扱うISA/IEC 62443ガイドラインによって強化されています。その結果、SIL準拠とサイバーセキュア設計を単一ソリューションで検証可能なプロバイダーが、明確な競争優位性を獲得しています。

世界の機能安全市場の動向と洞察

厳格化する世界の安全規制と基準

IEC 61508は現在、業界横断的な製品承認の基盤となっており、2024年のISO 26262改訂版ではAIと機械学習に関する明確なガイダンスが追加され、設計段階での安全性の統合が義務付けられています。したがって、世界の市場への参入を目指す製造業者は、SIL認定コンポーネントとシステムレベルの検証を必要としており、これにより認定試験機関への予測可能な需要が持続します。同時に、EU機械指令、OSHA指令、および日本や中国における同等の規制により、施行の厳格化が進んでいます。これに加え、非準拠に対する罰則の強化も相まって、これらの枠組みは企業に対し、監査の簡素化とプラント承認の迅速化を図るため、スタンドアロンのリレーから統合型で認証取得済みの安全コントローラへの置換を促しています。

インダストリー4.0の拡大が安全システム統合を加速

デジタルトランスフォーメーションにより運用データがクラウド化される中、安全機能はイーサネットベースのネットワークとネイティブに連携しつつ、確定的な応答時間を維持する必要があります。スマートファクトリーではデジタルツインを活用した予知保全が行われ、AI解析によりSIL目標を脅かす前にセンサードリフトを検知します。こうした使用事例では、複数プロトコルに対応し、診断機能をMESやERP層へ上流に押し上げられるプログラマブルロジックが有利です。したがって、認証ステータスを維持したままリモートでパッチ適用が可能な柔軟な安全PLCやソフトウェアフレームワークへの需要が高まっています。

高い導入コストが中小企業の採用の課題となる

SIL 3認証の取得には、厳格な第三者試験と文書化が求められるため、プロジェクト総予算の15~25%が追加費用として発生します。多くの中小企業はアップグレードを延期するか、より低いSIL目標を選択するため、軽工業や個別生産分野での普及が遅れています。サブスクリプションモデルは助けになりますが、資本集約度は依然として短期的な成長の主な抑制要因であり、特に現地での規制がまだ成熟段階にある地域では顕著です。

セグメント分析

安全センサーの収益は、物理的危険と制御システムを結びつける主要な役割を反映し、2025年の機能安全市場規模において最大の27.62%を占めました。光学解像度と自己診断機能の継続的な改善によりセンサーの信頼性が向上し、メーカーは証明試験間隔を延長し、ダウンタイムを削減できるようになりました。非接触センシングが汚染リスクを最小限に抑えるクリーンルームや食品グレード環境での採用も増加しています。

プログラマブル安全システムの需要は、2031年までにCAGR11.05%と予測され、デバイスカテゴリーの中で最も高い伸び率を示します。インダストリー4.0の普及に伴い、ユーザーは頻繁な製品切り替えに対応可能なソフトウェア設定型ロジックを好んで採用しており、これにより制御盤の配線変更が不要となります。オムロンの「Sysmac Studio」などのプラットフォームはプログラミング時間を90%削減し、認定エンジニア不足というボトルネックの解消に貢献しています。最終制御機器(バルブ、アクチュエータ、ドライブ)も勢いを増しています。プロセス産業では老朽化した機械式ガバナーを、状態監視をサポートするSIL認定デジタル機器に置き換えているためです。予測期間中、検証を効率化する統合型センサー・コントローラーパッケージにより、個別部品からバンドルソリューションへの支出シフトが進み、プラットフォームプロバイダーへの動向が強化される見込みです。

緊急停止(ESD)システムは、プロセス異常時の迅速な遮断を必要とする石油・ガス・化学プラントを基盤として、2025年の機能安全市場シェアの23.55%を占めました。市場密度は、高価値資産と厳格な規格により多層的な保護が求められる海洋プラットフォームおよびLNGプラントで最も高くなっています。ベンダー各社は、より少ないI/OポイントでSIL 3を達成しライフサイクルコストを削減するため、診断機能と投票アーキテクチャの強化を継続しています。

高信頼性圧力保護システム(HIPPS)は、深海プロジェクトにおいて大型フレアスタックの回避や排出量削減を目的として採用が進み、10.95%のCAGRで成長が見込まれています。北海資産での導入成功により、2,500万米ドルの設備投資(CAPEX)削減を実現し、堅調な投資利益率(ROI)事例を創出しました。バーナー管理およびターボ機械制御は、電力・精製分野で安定した需要を維持しています。一方、火災・ガス検知システムは、炎、有毒ガス、熱検知を単一の分析ダッシュボードに統合するフルカバレッジモデルを義務付ける規制により、需要が押し上げられています。

地域別分析

欧州は2025年時点で機能安全市場シェア28.40%を維持し首位を堅持。EU機械指令とドイツ・イタリア・北欧諸国における高度自動化の普及が基盤となっています。再生可能エネルギー及び洋上風力分野での導入が加速しており、高価値資産と遠隔地特性から、遠隔診断機能を備えたSIL 3準拠シャットダウン装置が求められています。

北米はOSHA主導の労働者安全プログラムと、精製・石油化学・製薬分野の広範な生産能力に支えられ、僅差で続きます。同地域は成熟したIT-OT統合技術と豊富な認定技術者を背景に、安全とサイバーセキュリティの融合を先導しています。半導体工場向け連邦政府の刺激策により、IEC 61508とISA/IEC 62443の両要件を満たすプログラマブル安全プラットフォームの新規導入が促進されています。

アジア太平洋地域は2031年までにCAGR11.25%という最速の伸びが見込まれます。中国の継続的な製造業高度化と日本の精密ロボット投資が相まって、プログラマブル安全PLCやスマートライトカーテンの大量購入を促進しています。東南アジア諸国では、多額の設備投資を伴わずに高まる職場安全への期待に応えるため、サブスクリプション型安全サービスが採用されています。一方、インドの新たな化学プロセス安全ガイドラインにより、新規プラントは最初からSIL 2以上の仕様レベルで設計されます。中東・アフリカ地域では、サウジアラビア、カタール、UAEにおけるNOC(国営石油会社)およびIOC(国際石油会社)プロジェクトが、新規LNG・水素施設においてHIPPS(高信頼性プロセス制御システム)と高度な火災・ガス検知システムの標準化を推進し、漸増的な成長をもたらしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 厳格な世界の安全規制および基準(IEC 61508、ISO 26262)

- インダストリー4.0および産業オートメーションの拡大

- 石油・ガスおよび電力セクターにおける事故関連の監視強化

- 機能安全と産業用サイバーセキュリティの統合

- SIL認証取得済みAI/MLシャットダウンアルゴリズムの登場

- 中小企業向け「サービスとしての安全性」サブスクリプションモデルの台頭

- 市場抑制要因

- SIL認証済みコンポーネントおよびシステムの高い初期費用

- 既存のブラウンフィールド施設への改修の複雑さ

- 認定機能安全エンジニアの不足

- OTAによる安全上重要なソフトウェア更新における責任の曖昧さ

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場におけるマクロ経済動向の評価

第5章 市場規模と成長予測

- デバイスタイプ別

- 安全センサー

- 安全制御装置/モジュール/リレー

- 安全スイッチ

- プログラマブル安全システム

- 非常停止装置

- 最終制御機器(バルブ、アクチュエータ)

- その他のデバイス種別

- 安全システム別

- バーナー管理システム(BMS)

- ターボ機械制御(TMC)システム

- 高信頼性圧力保護システム(HIPPS)

- 火災・ガス監視制御システム

- 緊急停止システム(ESD)

- 監視制御およびデータ収集(SCADA)システム

- 分散制御システム(DCS)

- サービス別

- 試験、検査および認証

- 設計、エンジニアリング、および保守

- トレーニングおよびコンサルティングサービス

- エンドユーザー業界別

- 石油・ガス

- 発電

- 食品・飲料

- 製薬

- 自動車

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- シンガポール

- オーストラリア

- マレーシア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Rockwell Automation Inc.

- Emerson Electric Company

- Honeywell International Inc.

- ABB Ltd

- Yokogawa Electric Corporation

- Schneider Electric SE

- Siemens AG

- General Electric Company

- Omron Corporation

- SICK AG

- Panasonic Corporation

- Pepperl+Fuchs SE

- Banner Engineering Corporation

- Pilz GmbH and Co. KG

- HIMA Paul Hildebrandt GmbH

- Mitsubishi Electric Corporation

- Phoenix Contact GmbH and Co. KG

- Turck GmbH and Co. KG

- Balluff GmbH

- IDEC Corporation