|

|

市場調査レポート

商品コード

1404469

自動車用コックピットエレクトロニクス:市場シェア分析、産業動向と統計、2024~2029年の成長予測Automotive Cockpit Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用コックピットエレクトロニクス:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 70 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

自動車用コックピットエレクトロニクス市場の現在の市場規模は403億6,000万米ドルです。

予測期間中のCAGRは8.5%を超え、今後5年間で656億8,000万米ドルに成長すると予想されます。

乗員の快適性と安全性に対する意識の高まりと、安全機能を義務付ける政府規制を背景に、ADAS機能を統合した自動車の生産台数が増加しており、市場の需要を牽引すると予想されます。さらに、自動運転車や自動運転車の受け入れが増加していることも、市場の成長強化に貢献しています。

安全性と快適性を高めるためのデジタル化とコネクティビティに対する需要の高まりが、自動車のコックピットエレクトロニクス市場を牽引しています。消費者の需要に加えて、様々な政府や安全機関が課す厳しい規制規範が、自動車用コックピットエレクトロニクス市場の成長をさらに後押ししています。

北米は2022年まで自動車用コックピットエレクトロニクスの最大市場であり、アジア太平洋と西欧がこれに続く。しかし、アジア地域は自動車用コックピットエレクトロニクス・システムの製造と利用の主要市場になると推定され、インドでは自動車部品やコンポーネントの製造拠点が徐々に全国に拡大しています。

乗用車ではセンサーや最新の自動車制御設備が幅広く使用されているため、ドライバーからアクセス可能な自動車制御機能に対する需要が高まっています。

自動車用コックピットエレクトロニクス市場動向

インダッシュ・ナビゲーション・システムに対する顧客の嗜好の高まり

ここ数年、自動車のダッシュボード内ナビゲーションシステムに対する顧客の嗜好が大幅に高まっています。技術の進歩、GPS対応スマートフォンの普及、シームレスで便利な運転体験への欲求など、いくつかの要因がこの動向を後押ししています。顧客は、すべての機能を体験するために、シリーズの最上位モデルを好んで購入します。

インダッシュ・ナビゲーション・システムの主要利点のひとつは、スマートフォンのアプリや紙の地図を使うよりも信頼性が高く正確なナビゲーションができることです。インダッシュ・ナビゲーション・システムを使えば、ドライバーはターン・バイ・ターンの道案内、リアルタイムの交通情報、近隣の観光スポット情報などに簡単にアクセスできます。ドライバーは、より迅速かつ効率的に目的地に到着することができ、道に迷ったり渋滞に巻き込まれたりするリスクを減らすことができます。

インダッシュ・システムは、より優れたナビゲーション機能を提供するだけでなく、より統合された直感的なユーザー体験も提供します。最新のシステムのほとんどは、使いやすい大型の高解像度タッチスクリーンを搭載しており、エンターテインメント、空調制御、車両診断など、ナビゲーション以外のさまざまな機能にアクセスできます。これにより、ドライバーは道路に集中しやすくなり、運転中に別のデバイスやアプリをいじる必要が少なくなります。例えば

- 2023年2月、MapmyIndiaは、高度な車両GPSトラッカー、ダッシュカメラ、ダッシュ内ナビゲーションシステムを含む車載用Mapplsガジェットの新ラインを発表しました。

ダッシュボード内ナビゲーションシステムの人気の高まりを促進するもう一つの要因は、音声コマンド、予測ルーティング、スマートホームデバイスとの統合などの高度な機能の利用可能性の増加です。例えば、ドライバーの位置や運転習慣に基づいて、自宅の温度や照明を自動的に調整できるシステムもあります。一方、機械学習アルゴリズムを使って、リアルタイムの交通データに基づいて最も効率的なルートを提案するシステムもあります。

全体として、ダッシュボード内ナビゲーション・システムに対する顧客の嗜好の高まりは、より高度で統合された便利な自動車技術に対する需要の高まりを反映しています。これらのシステムが進化を続け、より洗練されていくにつれて、今後数年のうちに、運転体験にさらに欠かせないものとなっていくことが予想されます。

北米がコックピットエレクトロニクス市場で大きなシェアを占める

コックピットエレクトロニクス市場は近年大きな成長を遂げ、北米はこの市場の主要地域のひとつに浮上しました。この市場の成長は、高度な安全機能に対する需要の増加やコネクテッドカーの動向の高まりなど、いくつかの要因に起因しています。

北米には、General Motors、Ford、Teslaなど、世界最大級の自動車メーカーがあります。これらの企業は、ADAS(先進運転支援システム)やインフォテインメント・システムなどの新技術の開発に多額の投資を行っており、コックピットエレクトロニクス市場の成長を牽引しています。例えば、2022年度、米国自動車業界は約286万台の自動車を販売しました。同年、米国における自動車と小型トラックの総販売台数は約1,375万台でした。

自動車産業に加えて、北米の航空宇宙セクターもコックピットエレクトロニクス市場の成長に貢献しています。同地域には、ボーイングやエアバスなど、民間機や軍用機向けの先進的なアビオニクス・システムを開発している大手航空宇宙企業があります。これらのシステムには、高度なフライト・ディスプレイ、ナビゲーション・システム、通信システムなどが含まれ、空の旅の安全性と効率を確保するために不可欠です。

コネクテッド・カーに対する需要の高まりも、北米におけるコックピットエレクトロニクス市場の主要促進要因です。消費者は、車内Wi-Fi、スマートフォンとの統合、音声操作などの機能を備えた自動車を求めるようになっています。これらの機能には高度なコックピットエレクトロニクス・システムが必要であり、新車への搭載が一般的になりつつあります。

さらに、電気自動車やハイブリッド車の採用も北米のコックピットエレクトロニクス市場の成長に寄与しています。これらの車両には、車両のコックピットエレクトロニクス・システムに統合された高度なバッテリー管理システムが必要です。

さらに米国政府は、アダプティブ・クルーズ・コントロール、リア・クロス・パス・ディテクション、フロント・ペデストリアンディテクションなど、新車に搭載される多くのADASシステムを規制しています。また、道路安全保険協会(IIHS)は、すべての新型乗用車に自動緊急ブレーキ(AEB)を搭載すると発表しました。

自動車用コックピットエレクトロニクス産業概要

自動車用コックピットエレクトロニクス市場は、Visteon Corporation、Alpine Electronics Inc.、Panasonic Corporation、Continental AG、Harman International Industries Inc.、Delphi Automotive(Aptiv PLC)、Clarion、Luxoft Holding Inc.などの複数の参入企業によって支配されています。これらの企業は、競合他社よりも優位に立てるよう、革新的な新製品によって事業を拡大しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- コネクテッドカー需要の増加

- ヒューマンマシンインターフェース(HMI)技術の進歩

- 市場抑制要因

- 急速な技術進歩

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模(単位:米ドル))

- 製品

- ヘッドアップディスプレイ

- インフォメーションディスプレイ

- インフォテインメントとナビゲーション

- インストルメントクラスター

- テレマティクス

- その他の製品

- 車種

- 乗用車

- 商用車

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Visteon Corporation

- Panasonic Corporation

- Harman International Industries Inc.

- Clarion Co. Ltd

- Alpine Electronics Inc.

- Continental AG

- Magneti Marelli SPA

- Yazaki Corporation

- Denso Corporation

- Garmin Ltd

- Nippon-Seiki Co. Ltd

- Tomtom International BV

第7章 市場機会と今後の動向

- 人工知能(AI)の統合

- ユーザーエクスペリエンスとヒューマンマシンインターフェース(HMI)への注目の高まり

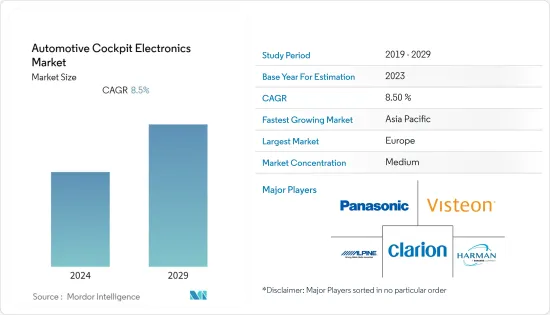

The automotive cockpit electronics market is valued at USD 40.36 billion in the current year. It is expected to grow to USD 65.68 billion within the next five years by registering a CAGR of over 8.5% during the forecast period.

Growing production of vehicles with integrated ADAS features in the wake of rising awareness toward the comfort and safety of passengers and government regulations mandating safety features are expected to drive demand in the market. Moreover, the rising acceptance of self-driving or automated vehicles further contributes to the enhanced growth of the market.

The rising demand for digitization and connectivity to enhance safety and comfort features is driving the market for cockpit electronics in vehicles. In addition to consumer demand, the stringent regulatory norms posed by various governments and safety organizations are further boosting the growth of the automotive cockpit electronics market.

North America was the largest market for automotive cockpit electronics until 2022, followed by Asia-Pacific and Western Europe. However, the Asian region is estimated to become the key market for the manufacturing and usage of automotive cockpit electronics systems, with India gradually expanding its automotive parts and components-manufacturing hubs across the country.

The increasing demand for automotive control functions, which are accessible by the driver, is growing in automobiles due to the wide-ranging use of sensors and modern automotive control amenities in passenger cars.

Automotive Cockpit Electronics Market Trends

Increasing Customer Preference for In-Dash Navigation System

Over the past few years, there is a significant increase in customer preference for in-dash navigation systems in their vehicles. Several factors, including advances in technology, the growing popularity of GPS-enabled smartphones, and the desire for a seamless and convenient driving experience, are driving this trend. Customers prefer to buy top-end models in the series of cars to experience all the features.

One of the primary benefits of in-dash navigation systems is that they offer a more reliable and accurate way to navigate than using a smartphone app or paper maps. With an in-dash navigation system, drivers can easily access turn-by-turn directions, real-time traffic updates, and information on nearby points of interest. It helps drivers reach their destination more quickly and efficiently and reduces the risk of getting lost or stuck in traffic.

In addition to providing better navigation capabilities, in-dash systems also offer a more integrated and intuitive user experience. Most modern systems feature large, high-resolution touchscreens that are easy to use and provide access to a range of features beyond navigation, such as entertainment, climate control, and vehicle diagnostics. It makes it easier for drivers to stay focused on the road and reduces the need to fumble with separate devices or apps while driving. For instance,

- In February 2023, MapmyIndia launched its new line of Mappls Gadgets for cars, including advanced Vehicle GPS trackers, Dash Cameras, and In-Dash navigation systems.

Another factor driving the growing popularity of in-dash navigation systems is the increasing availability of advanced features such as voice commands, predictive routing, and integration with smart home devices. For example, some systems can automatically adjust the temperature and lighting in a driver's home based on their location and driving habits. In contrast, others can use machine learning algorithms to suggest the most efficient route based on real-time traffic data.

Overall, the increasing customer preference for in-dash navigation systems reflects a growing demand for more advanced, integrated, and convenient automotive technologies. As these systems continue to evolve and become more sophisticated, we can expect to see them become an even more essential part of the driving experience in the years ahead.

North America Holds a Significant Share in the Cockpit Electronics Market

The cockpit electronics market experienced significant growth in recent years, and North America emerged as one of the leading regions for this market. The growth of this market can be attributed to several factors, including the increasing demand for advanced safety features and the rising trend of connected cars.

North America is home to some of the largest automotive manufacturers in the world, including General Motors, Ford, and Tesla. These companies are investing heavily in the development of new technologies, including advanced driver assistance systems (ADAS) and infotainment systems, which are driving the growth of the cockpit electronics market. For instance, IN FY 2022, The United States auto industry sold nearly 2.86 million cars in 2022. That year, total car and light truck sales were approximately 13.75 million in the United States.

In addition to the automotive industry, the aerospace sector in North America is also contributing to the growth of the cockpit electronics market. The region is home to some of the largest aerospace companies, such as Boeing and Airbus, which are developing advanced avionics systems for commercial and military aircraft. These systems include advanced flight displays, navigation systems, and communication systems, which are essential for ensuring the safety and efficiency of air travel.

The increasing demand for connected cars is also a key driver of the cockpit electronics market in North America. Consumers are increasingly seeking vehicles that are equipped with features such as in-car Wi-Fi, smartphone integration, and voice-activated controls. These features require advanced cockpit electronics systems, which are becoming increasingly common in new vehicles.

Furthermore, the adoption of electric and hybrid vehicles is also contributing to the growth of the cockpit electronics market in North America. These vehicles require sophisticated battery management systems, which are integrated into the cockpit electronics systems of the vehicle.

In addition, the government of the United States regulates many ADAS systems in new vehicles, such as adaptive cruise control, rear cross-path detection, and front pedestrian detection. The Insurance Institute for Highway Safety (IIHS) also announced that all new passenger vehicles would include automatic emergency braking (AEB).

Automotive Cockpit Electronics Industry Overview

The automotive cockpit electronics market is dominated by several players, such as Visteon Corporation, Alpine Electronics Inc., Panasonic Corporation, Continental AG, Harman International Industries Inc., Delphi Automotive (Aptiv PLC), Clarion Co. Ltd, and Luxoft Holding Inc. These companies are expanding their business by new innovative products so that they can hold an edge over their competitors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for Connected Cars

- 4.1.2 Advancements in Human-Machine Interface (HMI) Technologies

- 4.2 Market Restraints

- 4.2.1 Rapid Technological Advancements

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value in USD)

- 5.1 Product

- 5.1.1 Head-up Display

- 5.1.2 Information Display

- 5.1.3 Infotainment and Navigation

- 5.1.4 Instrument Cluster

- 5.1.5 Telematics

- 5.1.6 Other Products

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles*

- 6.2.1 Visteon Corporation

- 6.2.2 Panasonic Corporation

- 6.2.3 Harman International Industries Inc.

- 6.2.4 Clarion Co. Ltd

- 6.2.5 Alpine Electronics Inc.

- 6.2.6 Continental AG

- 6.2.7 Magneti Marelli SPA

- 6.2.8 Yazaki Corporation

- 6.2.9 Denso Corporation

- 6.2.10 Garmin Ltd

- 6.2.11 Nippon-Seiki Co. Ltd

- 6.2.12 Tomtom International BV

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration of Artificial Intelligence (AI)

- 7.2 Increasing Focus on User Experience and Human-Machine Interface (HMI)