|

市場調査レポート

商品コード

1404451

航空母艦(空母):市場シェア分析、産業動向・統計、成長予測、2024~2029年Aircraft Carrier Ship - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空母艦(空母):市場シェア分析、産業動向・統計、成長予測、2024~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

航空母艦(空母)市場は2024年に12億3,000万米ドルと評価され、2029年には23億9,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは14.15%で成長する見込みです。

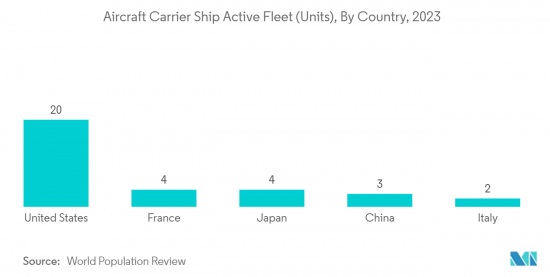

地政学的な問題や各国間の領土紛争の増加が空母の調達につながり、これが市場成長の要因と考えられます。また、既存の空母を新世代の空母に置き換えるための投資が増加していることも、市場の成長を加速させると思われます。空母は、海軍部隊に戦力を提供することで、数年間運用を続けることができます。しかし、空母に関連する高い維持費は、様々な地域にとって足かせとなります。アジア太平洋は世界の軍事紛争のホットスポットのひとつです。この地域で領土問題が増加しているため、各国は先進的な空母を調達するようになりました。

空母の市場動向

市場を独占する原子力搭載セグメント

予測期間中、原子力セグメントが市場を独占すると予想されます。その理由は、従来型動力に比べて航空機燃料を2倍以上搭載できる能力が大きいためです。耐久性に加え、原子炉を搭載しているため、航空燃料、兵器、備蓄のためのスペースが大きくなり、これは石油動力空母に対する重要な利点です。通信、推進、ミサイル防衛など、艦艇に搭載されるさまざまなシステムのメーカーと造船会社が協力し、維持費の安い先進的な空母を開発・配備することは、このセグメントの成長を促進すると予想されます。

さらに、海洋安全保障への注目の高まりと原子力エネルギーの高い利用率が、市場を牽引する主な要因となっています。2022年9月、インドは同国固有の原子力空母であるINSヴィクラントを就役させました。同年、フランスの造船会社ナバル・グループは、パリで開催された2022年ユーロナバル貿易会議において、原子力空母コンセプトPANGを発表しました。PANGは、最大32機の戦闘機と多数のヘリコプターを搭載できるよう設計されています。しかし、マレーシアやタイのような国々は、原子力空母の維持費がかさむため退役させました。これは、このセグメントの成長にとって大きな課題のひとつです。

予測期間中、北米が大きな成長を見せる

北米は、国防支出が多く、研究開発投資が急増していることから、予測期間中に最も高い成長を示すと予想されます。米国海軍の艦艇への投資は、2030年までに355隻体制という目標達成に向けた艦隊拡張計画を支援するために増加しています。この調達計画には、ジェラルド・R・フォード級空母5隻(2022年から2034年の間に引き渡し・配備予定)と、USSエンタープライズ(CVN 80)空母(CVN 65空母の後継)が含まれており、2028年から2032年の間に引き渡される予定です。

さらに米国海軍は、既存空母の近代化にも力を入れています。海軍の空母を建造するHIIのニューポート・ニューズ造船は、2022年に造船所での空母の作業量が過去最高を記録しました。ジョン・F・ケネディ(CVN-79)はニューポートニューズで建造の最終段階にあり、2024年に海軍に引き渡される予定です。2023年3月、米国海軍はニミッツを2026年5月まで5ヵ月半のメンテナンス期間として延長する計画を発表しました。上記の要因は、予測期間中の同地域の市場成長をサポートすると予想されます。

空母産業の概要

空母市場は統合された性質を持っています。空母市場の有力企業は、NAVANTIA, SA、BAE Systems plc、General Dynamics Corporation、HUNTINGTON INGALLS INDUSTRIES, INC.(HII)、Naval Groupです。造船会社は各国政府と空母建造の長期契約を結んでいます。HIIは米国の空母建造計画を支援しています。Naval Group、BAE Systems、NAVANTIAは、欧州の空母計画を支援する企業の一部です。アジア太平洋地域では、多くの官民パートナーシップが空母建造を支援しています。例えば、INS Vishal Indigenous Aircraft Carrier 2(IAC-2)は、インド海軍のためにCochin Shipyard Limitedが建造する予定の空母で、2030年代に就役する予定です。同計画は初期段階にあるため、今後数年のうちに多くの企業が同計画の一員となるチャンスを得ることになります。今後予定されている調達や保守・近代化プログラムは、各企業の成長戦略を支えるものと予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 水陸両用艇

- ヘリ空母

- 正規空母

- 技術

- 従来型動力

- 原子力

- 構成

- CATOBAR

- STOBAR

- STOVL

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- インド

- 中国

- 韓国

- 日本

- その他アジア太平洋地域

- その他の地域

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Lockheed Martin Corporation

- BAE Systems plc

- Naval Group

- General Dynamics Corporation

- HUNTINGTON INGALLS INDUSTRIES, INC.

- Northrop Grumman Corporation

- THALES

- FINCANTIERI S.p.A.

- Leonardo S.p.A

- NAVANTIA, S.A.

第7章 市場機会と今後の動向

The aircraft carrier ship market is valued at USD 1.23 billion in 2024 and is expected to reach USD 2.39 billion by 2029, growing at a CAGR of 14.15% during the forecast period (2024-2029).

The increasing geopolitical issues and territorial disputes between various nations led to the procurement of aircraft carrier ships, which can be attributed to the growth of the market. Also, the increasing investments in replacing the existing fleet with newer generation carrier ships will accelerate market growth. Aircraft carrier ships may continue operations for several years by providing strength to the naval forces. However, the high maintenance costs associated with such ships shall prove to be a restraint for various regions. Asia-Pacific is one of the global hotspots for military conflicts. The increasing number of territorial issues in the region propelled the countries to procure advanced aircraft carrier ships.

Aircraft Carrier Ship Market Trends

The Nuclear Powered Segment to Dominate the Market

The nuclear-powered segment is anticipated to dominate the market during the forecast period. It is because of the larger capacity of carrying over twice the volume of aircraft fuel as compared to the conventionally powered aircraft carrier. In addition to endurance, its nuclear reactors give the ship greater space for aviation fuel, ordnance, and stores, which are important advantages over oil-powered carriers. The collaboration of shipbuilding companies with manufacturers of various systems onboard naval vessels, like communication, propulsion, and missile defense, to develop and deploy advanced aircraft carriers with a low cost of maintenance is anticipated to drive the growth of the segment.

Furthermore, increased focus on maritime security and high usage of nuclear energy are the main factors driving the market. In September 2022, India inducted INS Vikrant, the country's indigenous nuclear-powered aircraft carrier. In the same year, French shipbuilding firm Naval Group introduced its nuclear-powered aircraft carrier concept PANG during the 2022 Euronaval trade conference in Paris. PANG will be designed to carry up to 32 fighter jets and a large number of helicopters. However, countries like Malaysia and Thailand decommissioned their nuclear aircraft carriers as they incur high maintenance costs. It is one of the major challenges for the growth of the segment.

North America Will Showcase Significant Growth in the Market During the Forecast Period

North America is anticipated to show the highest growth during the forecast period due to the high defense spending and rapidly increasing R&D investments in this region. The US Navy's investment in naval vessels is increasing to support its fleet expansion plans to reach its goal of 355 ship fleets by 2030. The procurement plan included five Gerald R. Ford-class aircraft carriers (to be delivered and deployed between 2022 and 2034) and USS Enterprise (CVN 80) carriers (replacing CVN 65 aircraft carriers), which will be delivered during 2028-2032.

In addition, the US Navy is focusing on the modernization of existing aircraft carriers. HII's Newport News Shipbuilding, which builds the Navy's aircraft carriers, had a record amount of aircraft carrier work at its shipyard in 2022. John F. Kennedy (CVN-79) is in the final stages of construction at Newport News and is slated to deliver to the Navy in 2024. In March 2023, the US Navy announced its plan to extend Nimitz as part of a five-and-a-half-month maintenance availability that will carry the carrier into May 2026. The factors above are anticipated to support the growth of the market in the region during the forecast period.

Aircraft Carrier Ship Industry Overview

The aircraft carrier ship market is consolidated in nature. The prominent players in the aircraft carrier ship market are NAVANTIA, SA, BAE Systems plc, General Dynamics Corporation, HUNTINGTON INGALLS INDUSTRIES, INC. (HII), and Naval Group. The shipbuilding companies form long-term contracts with governments for the construction of aircraft carriers. HII supports US aircraft carrier construction programs. Naval Group, BAE Systems, and Navantia are some of the companies that support aircraft carrier programs in Europe. In the Asia-Pacific region, many public-private partnerships support aircraft carrier construction in the region. For instance, INS Vishal Indigenous Aircraft Carrier 2 (IAC-2) is a planned aircraft carrier to be built by Cochin Shipyard Limited for the Indian Navy, which is to be commissioned in the 2030s. As the program is in its nascent stages, many companies will include a chance to become a part of the program in the coming years. The upcoming procurements and maintenance and modernization programs are anticipated to support the growth strategies of the companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Amphibious Assault Ship

- 5.1.2 Helicopter Carrier

- 5.1.3 Fleet Carrier

- 5.2 Technology

- 5.2.1 Conventional Powered

- 5.2.2 Nuclear Powered

- 5.3 Configuration

- 5.3.1 Catapult-assisted Take-off Barrier Arrested-recovery (CATOBAR)

- 5.3.2 Short Take-off but Arrested Recovery (STOBAR)

- 5.3.3 Short Take-off but Vertical Recovery (STOVL)

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 South Korea

- 5.4.3.4 Japan

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 BAE Systems plc

- 6.2.3 Naval Group

- 6.2.4 General Dynamics Corporation

- 6.2.5 HUNTINGTON INGALLS INDUSTRIES, INC.

- 6.2.6 Northrop Grumman Corporation

- 6.2.7 THALES

- 6.2.8 FINCANTIERI S.p.A.

- 6.2.9 Leonardo S.p.A

- 6.2.10 NAVANTIA, S.A.