|

市場調査レポート

商品コード

1404447

エアデータシステム:市場シェア分析、産業動向・統計、成長予測、2024~2029年Air Data Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エアデータシステム:市場シェア分析、産業動向・統計、成長予測、2024~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

エアデータシステム市場は、2024年に8億7,242万米ドルと評価され、予測期間中のCAGRは5.86%を記録し、2029年には10億9,000万米ドルに成長すると予測されています。

エアデータシステムは、幅広いアタック角や対気速度角の正確な測定など、航空機の飛行制御に不可欠な情報を提供します。世界中の航空会社や軍隊による新型航空機の需要増加が、エアデータシステム市場の主な促進要因となっています。先進的なエアデータシステムの開発に向けた研究開発投資は、今後数年間の市場成長をさらに促進する可能性があります。クラウドコンピューティング、人工知能、リアルタイムデータ監視の技術的進歩は、市場の成長を後押しするいくつかの追加要因です。エアデータシステムメーカーは、顧客のニーズに合わせて最新技術で製品を継続的に更新しています。しかし、複数のデータタイプ、フォーマット、構造をより優れた効率で管理するシステムの開発は、メーカーにとって依然として課題となっています。

エアデータシステム市場の動向

市場セグメンテーションでは商業セグメントが最も高いシェアを占める

商業セグメントが市場で最も高いシェアを占めており、予測期間中もその支配が続いています。この成長の背景には、航空交通量の増加、新型機需要の高まり、航空分野への支出の増加があります。国際航空運送協会(IATA)によると、全体の航空旅客数は2024年に40億人に達します。さらに、ボーイング社の商業市場見通し2023-2042によると、今後20年間に旅客機と貨物機の両方で4万2,000機以上の民間航空機の新規需要が見込まれます。

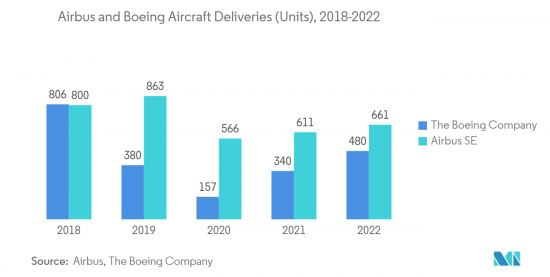

商業航空部門は、旅客輸送量の急増に牽引されて2022年に大幅な成長を示し、その結果、航空機OEM最大手の2社であるエアバス社とボーイング社の両方が、世界中で運航する航空会社からの大幅な受注増を記録しました。2022年、エアバスは合計661機の民間航空機を84の顧客に引き渡し、1,078機の新規受注を記録しました。ボーイング社は合計480機の民間航空機を納入しました。ボーイングB737 MAXモデルの再認証により、ボーイングB737 MAXファミリーの需要が回復しました。2022年、ボーイング社はボーイングB737 MAXを合計561機受注しました。また、同時期にボーイング社は、B777-8貨物機50機の受注を含む、213機のワイドボディと78機の貨物機の受注も獲得しました。このように、民間航空機の納入数の増加と新規航空機受注の増加が市場の成長を牽引しています。

予測期間中に最も高い成長を遂げるのはアジア太平洋地域

アジア太平洋地域は、予測期間中に高い成長率を記録すると予想されます。市場成長の主な促進要因は、中国、インド、インドネシア、ベトナム、タイなどの国々から民間航空機の調達が増加していることです。同地域における航空輸送量の増加により、民間航空会社は新世代の航空機を調達して機体を拡大せざるを得なくなった。例えば、2022年11月、リース会社7社が中国商用飛機総公司(COMAC)と300機の新型機C919と30機のARJ21の調達契約を締結しました。同様に、2023年2月、エア・インディアは、機材拡大計画の一環として、エアバス社およびボーイング社から470機の航空機を新たに調達する計画を発表しました。エアバスA320neoを210機、エアバスA350を40機、ボーイングB737MAXを190機、ボーイングB787を20機、ボーイングB777Xを10機調達すると発表しました。一方、この地域の国々は新しい軍用機も調達しています。中国は最新鋭戦闘機の開発と配備に多額の投資を行う一方、AEW&Cや爆撃機の運用能力も拡大しています。日本は、老朽化したF-4戦闘機に代わるF-35A戦闘機を大量に購入しており、韓国は、自国製(KF-X)と外国製(F-35A)の両方の航空機を追加することに注力しています。このように、新しい航空機の調達が増加していることがエアデータシステムの需要を生み出し、市場の成長を促進しています。

エアデータシステム産業の概要

エアデータシステム市場は、少数のプレーヤーが大きなシェアを占めているため、その性質上、統合されています。市場の著名なプレーヤーには、Honeywell International Inc.、RTX Corporation、Curtiss-Wright Corporation、AMETEK, Inc.、Meggitt PLCなどがあります。これらの企業がエアデータシステム市場で大きなシェアを占めています。各社はエアデータシステムの研究開発に多額の投資を行い、市場シェアを拡大するために新製品を発売しています。RTX Corporation傘下のCollins Aerospace社は、最新世代のSmartProbe Air Data Systemsを発売しました。これは、センシングプローブ、圧力センサー、強力なエアデータコンピューター処理を統合し、ピトー圧力、静圧、空気、速度、高度、迎角、横滑り角などの重要なエアデータパラメーターをすべて提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 商業

- 軍事

- コンポーネント

- 電子ユニット

- プローブ

- センサー

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Honeywell International Inc.

- THOMMEN AIRCRAFT EQUIPMENT Ltd.

- Collins Aerospace(RTX Corporation)

- Curtiss-Wright Corporation

- AMETEK.Inc

- Astronautics Corporation of America

- Shadin L.P.

- Meggitt PLC

- Aeroprobe Corporation

- THALES

第7章 市場機会と今後の動向

The air data systems market is valued at USD 872.42 million in 2024 and is anticipated to grow to USD 1.09 billion by 2029, registering a CAGR of 5.86% during the forecast period.

Air data systems provide vital information for aircraft flight control, such as accurate measurements over a wide range of attack and airspeed angles. Increasing demand for new aircraft by airlines and armed forces across the globe is the major driving factor for the air data systems market. The R&D investments in developing advanced air data systems may further propel the growth of the market in the coming years. Technological advancements in cloud computing, artificial intelligence, and real-time data monitoring are a few additional factors boosting the growth of the market. Air data system manufacturers continually update their products to suit their customers' needs with the latest technologies. However, developing systems for managing multiple data types, formats, and structures with even better efficiency continues to remain a challenge for manufacturers.

Air Data Systems Market Trends

Commercial Segment Holds Highest Shares in the Market

The commercial segment held the highest shares in the market and continued its domination during the forecast period. The growth is attributed to the increasing air traffic, rising demand for new aircraft, and growing expenditure on the aviation sector. According to the International Air Transport Association (IATA), the overall air passenger number will reach 4 billion in 2024. Furthermore, as per the Boeing Company's Commercial Market Outlook 2023-2042, there will be a demand for more than 42,000 new commercial aircraft, both passenger and cargo aircraft, during the next two decades.

The commercial aviation sector witnessed substantial growth in 2022, driven by a rapid rise in air passenger traffic, which resulted in both Airbus and Boeing Company, two of the largest aircraft OEMs, recording significant increases in orders from airlines operating across the globe. In 2022, Airbus delivered a total of 661 commercial aircraft to 84 customers and registered 1,078 gross new orders. The Boeing Company delivered a total of 480 commercial airplanes. The recertification of the Boeing B737 MAX models caused a resurgence in the demand for the Boeing B737 MAX family of aircraft. On this note, in 2022, the Boeing Company received a total of 561 orders for Boeing B737 MAXs. During the same timeframe, the Boeing Company also received orders for 213 widebodies and 78 freighters, including 50 orders for the B777-8 freighters. Thus, growing deliveries of commercial aircraft and the increasing number of new aircraft orders are driving the growth of the market.

Asia-Pacific to Experience the Highest Growth during the Forecast Period

The Asia-Pacific region is expected to experience a high growth rate during the forecast period. The primary driver for the growth of the market is the increasing procurement of commercial aircraft from countries like China, India, Indonesia, Vietnam, and Thailand. The increasing air traffic in the region forced the commercial airlines to expand their fleet by procuring new-generation aircraft. For instance, in November 2022, seven leasing companies signed a contract with the Commercial Aircraft Corporation of China (COMAC) for the procurement of 300 new C919 planes and 30 ARJ21 aircraft. Similarly, in February 2023, Air India announced its plans to procure 470 new aircraft from Airbus and the Boeing Company as part of its fleet expansion plans. The airline announced procuring 210 Airbus A320neo, 40 Airbus A350s, 190 Boeing B737 MAXs, 20 Boeing B787s, and 10 Boeing B777X. On the other hand, the countries in the region are also procuring new military aircraft. China is investing heavily in the development and deployment of advanced fighter aircraft while also expanding its operational capabilities with respect to AEW&C and bomber aircraft. Japan is buying substantial numbers of F-35A fighters to replace its aging F-4 fleet, while South Korea is focused on adding both indigenous (KF-X) and foreign-made aircraft (F-35A) to its fleet. Thus, the growing procurement of new aircraft is creating a demand for air data systems, thereby propelling the growth of the market.

Air Data Systems Industry Overview

The air data systems market is consolidated in nature due to the presence of a few players holding significant shares in the market. Some of the prominent players in the market are Honeywell International Inc., RTX Corporation, Curtiss-Wright Corporation, AMETEK, Inc., and Meggitt PLC. These players together account for a major share of the air data systems market. Companies are investing significantly in the research and development of air data systems and are launching new products to increase their market share. Collins Aerospace, an RTX Corporation company, launched the latest generation of SmartProbe Air Data Systems. It integrates sensing probes, pressure sensors, and powerful air data computer processing to provide all critical air data parameters, including pitot and static pressure, air, speed, altitude, angle of attack, and angle of sideslip.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Commercial

- 5.1.2 Military

- 5.2 Component

- 5.2.1 Electronic Units

- 5.2.2 Probes

- 5.2.3 Sensors

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Qatar

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 THOMMEN AIRCRAFT EQUIPMENT Ltd.

- 6.2.3 Collins Aerospace (RTX Corporation)

- 6.2.4 Curtiss-Wright Corporation

- 6.2.5 AMETEK.Inc

- 6.2.6 Astronautics Corporation of America

- 6.2.7 Shadin L.P.

- 6.2.8 Meggitt PLC

- 6.2.9 Aeroprobe Corporation

- 6.2.10 THALES