|

市場調査レポート

商品コード

1641974

石油・ガス用センサ-市場シェア分析、産業動向、成長予測(2025年~2030年)Sensors In Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 石油・ガス用センサ-市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

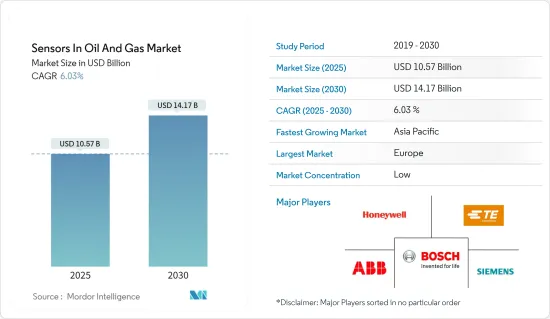

石油・ガス用センサ市場規模は2025年に105億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.03%で、2030年には141億7,000万米ドルに達すると予測されます。

主要ハイライト

- 世界経済は石油・ガス産業に依存しています。石油・ガス産業は、世界の基礎エネルギーの大部分を生産するほか、殺虫剤、肥料、医薬品、溶剤、ポリマーなど、さまざまな化学製品の原料の重要な供給源となっています。石油・ガス産業の効率的で安定した操業には、制御とモニタリングが欠かせないです。生産性を向上させ、コストを削減し、収益性を促進します。石油・ガス産業の制御とモニタリングは、センサに大きく依存しています。

- 市場拡大に影響を与える主要要因は、技術的進歩への注力の高まりと政府の支援施策です。工業化の進展と各種安全・労働衛生規制の厳格化は市場規模を低下させています。大気汚染に対する意識の高まりと、小型化された無線センサの供給拡大により、市場は成長します。市場の急増に寄与するもう1つの要素は、マイクロエレクトロ機械式セグメントの拡大と成長です。

- 石油・ガス産業におけるIIoT(Industrial Internet of Things)センサの採用が増加しているのは、主にコスト削減の必要性によるものです。センサメーカーがエンドユーザーに提供する技術の進歩と簡単な組み立てオプションのおかげで、これらのセンサの設置にかかる時間とコストは少なくて済みます。

- 現在の石油価格環境は、石油・ガス産業全体に大きな変化と困難な決断を促しています。短期的・中期的な市場の需給力学に対応するためには、CAPEXとOPEXを改善する新しい運営モデルと戦略が必要です。安全性と環境性能を強化するサステイナブルソリューションへの長期的な要求は、最優先事項です。ドリルパッドから製油所まで、センサのアプリケーションは、上流、中流、下流の技術革新とソリューションのスペクトルを通じて、オペレーターが独自のバランスを達成するのに役立ちます。

- センサメーカーは、組み立てが簡単なセンサを提供するようになってきています。技術の進歩により、センサの主要メーカーやIoT製品のサービスプロバイダー間の競争は激化しており、石油・ガス産業におけるセンサの採用を後押ししています。

- さらに、石油・ガス産業は熟練労働者不足に悩まされています。浅い人材プールが存在するため、石油・ガス会社は、新しいエネルギー源に取り組むために必要な技術スキルを持つ従業員を新たに雇用することが複雑になっています。さらに、COVID-19期間中の原油価格の高騰や、サウジアラビアとロシアといった国同士の価格競争が、産油企業の生産効率向上と同部門の需要拡大を促すと予想されます。

石油・ガス用センサ市場動向

上流産業が成長の可能性を提供

- 天然ガスと原油は上流部門で発見・生産されます。発電、工業プロセス、輸送は原油に大きく依存しています。天然ガス・原油は岩石層によって地下深くに隠されています。多くの貯留層は水中や、気候の厳しい到達困難な場所にあります。

- そのため、センサやその他の重要な地震画像は、メーカーが正確な掘削位置情報を得るのに役立っています。これにより、掘削に関する追加費用を削減することができます。さらに、石油・ガスの調達プロセスにおけるセンサの需要は、手頃な価格のセンサ、接続性の拡大、計算能力の上昇によって牽引されています。機器に組み込まれたセンサが提供するリアルタイムのデータは、修理のスケジューリングや日常業務の合理化において企業を支援します。

- 石油・ガス部門のシステム、機器、センサは、効率、生産性、健康、安全性を高めるために、データを通信し、互いに学習する必要があります。そのため、ワイヤレス用センサや個人用モニタリングデバイスを利用すれば、作業員が不健康な有害物質にいつさらされるかを簡単に特定できるようになります。その結果、効果的な措置を講じることができます。したがって、上記の要因が予測期間を通じて石油・ガス産業のセンサ市場に好影響を与えると予想されます。

- BP PLCなどの大手企業の上流と低炭素エネルギー事業セグメントは、2022年に894億4,000万米ドルを生み出しました。さらに、Abu Dhabi National Oil Company(ADNOC)は、上流のメタン強度目標を修正し、2025年までに0.15%の達成を目指すと発表しました。中東で最も低いこの新目標は、低炭素エネルギーの倫理的生産におけるADNOCのパイオニアとしての地位を強化するものです。メタン排出のモニタリングを改善するため、ADNOCは衛星モニタリングやドローン搭載センサなどの実験的技術も検討しています。

欧州が大きな市場シェアを占める

- 政府が公害防止とエネルギー効率要件に重点を置くようになったため、石油・ガス用センサはドイツ、フランス、英国を含む欧州諸国で一般的になっています。エンドユーザー基盤の拡大とガス用センサの用途拡大は、このセグメントの市場成長を促進する2つの要因です。

- 欧州連合(EU)における厳しい排ガス規制要件とエネルギー効率促進のための政府活動は、欧州における対象市場の拡大に寄与しています。これらのガス用センサは、同じ原理で作動するガス警報器や煙警報器にも使用されています。さらに、消費者の環境安全に対する意識の高まりが、汚染レベルや揮発性有機化合物を検出する空気モニタリングシステムに使用される商品の採用増加につながっています。現在欧州市場を独占しているのは、赤外線センサタイプのガス用センサ技術です。

- 欧州の先進的な石油・ガス産業は、センサなどのモノのインターネット(IoT)スマートオブジェクトから目をそらし、これらのオブジェクトから得られるデータを使用して、事業の成長に役立つよりインテリジェントなビジネスモデルを構築するための大胆な戦略を開発することに再注目しています。

- 石油・ガス精製工場は、IoTセンサが収集した情報を使って、配送された石油タイプを知ることができます。これにより、企業は製造、在庫、運用に関する重要な決定を下すことができます。IoTセンサと強化された接続性によるリアルタイムの在庫管理は、欧州の石油・ガス産業により効率的なサプライチェーンを提供することができます。

- さらにノルウェー警察は、最近のノルド・ストリーム・ガスパイプラインの損傷に対応し、最近の安全違反を調査するため、ドローン検知システムを海洋石油・ガス施設に設置しました。センサを戦略的に配置することで、未登録のドローンを検知し、その使用を防ぐことができました。

石油・ガス用センサ産業概要

石油・ガス用センサ市場は細分化され、競合が激しいです。上流、中流、下流といった石油・ガス産業のさまざまな活動でセンサの配備が組織レベルで進んでいます。このため、参入企業間の競合環境が形成されています。Honeywell International Inc.、Siemens、ABBなどがその一例です。

2023年3月、電子情報技術省は、IoTセンサのCoEにおいて、スマートデジタル温度計、IoT対応環境モニタリングシステム、多チャネルデータ収集システムを含む3つのIoTセンサベース製品の発売を発表しました。

2022年10月、Honeywellはサステイナブルエネルギーへの移行を支援するため、アブダビ国際石油展示会・会議で最新のセンサ技術を展示しました。展示された技術には、エネルギー貯蔵システム、排出ガスモニタリングシステム、同事業の先進的プラスチックリサイクル技術、作業員安全ソリューションのポートフォリオ、炭素回収と水素生成技術が含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 石油・ガス産業における安全システム需要の高まり

- ワイヤレス用センサセグメントにおける簡素化されたネットワークアーキテクチャへのニーズの高まり

- 市場抑制要因

- 石油・ガス掘削活動に課される厳しい規制

第6章 市場セグメンテーション

- センサタイプ別

- ガス用センサ

- 温度センサ

- 超音波センサ

- 圧力センサ

- 流量センサ

- レベルセンサ

- その他のセンサタイプ

- 接続性別

- 有線

- ワイヤレス

- 活動別

- 上流

- 中流

- 下流

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- その他の欧州

- アジア太平洋

- 中国

- インド

- インドネシア

- その他のアジア太平洋

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Honeywell International Inc.

- TE Connectivity Ltd.

- Robert Bosch GmbH

- ABB Ltd.

- Siemens AG

- Rockwell Automation Inc.

- Analog Devices Inc.

- Emerson Electric Company

- GE Sensing & Inspection Technologies GmbH

- SKF AB

第8章 投資分析

第9章 市場の将来

The Sensors In Oil And Gas Market size is estimated at USD 10.57 billion in 2025, and is expected to reach USD 14.17 billion by 2030, at a CAGR of 6.03% during the forecast period (2025-2030).

Key Highlights

- The global economy depends on the oil and gas industry. In addition to producing most of the world's basic energy, the oil and gas sector also serves as a substantial source of raw materials for various chemical goods, such as insecticides, fertilizers, medicines, solvents, and polymers. Control and monitoring are crucial for efficient and stable oil and gas industry operations. It improves productivity, cuts costs, and promotes profitability. The control and monitoring of the oil and gas industry depend heavily on sensors.

- The primary factors influencing market expansion are a greater focus on technical advancement and supportive governmental policies. Growing industrialization and stricter enforcement of various safety and occupational health regulations reduce market value. The market will grow due to increased awareness of air pollution and the growing supply of miniaturized wireless sensors. Another element contributing to the surge of the market is the expansion and growth of the micro-electromechanical sector.

- The rising adoption of IIoT (Industrial Internet of Things) sensors in the oil and gas industry is mainly driven by the need to reduce costs. The installation of these sensors takes less time and costs less, owing to technological advancements and easy assembling options that sensor manufacturers offer to end users.

- The current oil price environment is driving significant changes and difficult decisions across the oil and gas industry. New operating models and strategies that improve CAPEX and OPEX are required to respond to short- and mid-term market supply and demand dynamics. The long-term requirement for sustainable solutions that reinforce safety and environmental performance is a topmost priority. From drill pad to refinery, the application of sensors helps operators achieve a unique balance through a spectrum of upstream, midstream, and downstream technological innovations and solutions.

- Sensor manufacturers are increasingly offering sensors designed with easy assembling options. Owing to technical advancements, the competition among significant manufacturers of sensors and service providers of IoT products is intensifying, thereby boosting the adoption of these in the oil and gas industry.

- Additionally, the oil and gas industry suffers from a skilled labor shortage. The presence of a shallow talent pool has made it complicated for oil and gas companies to hire new employees who possess the technical skills that are required to work on new energy sources. Moreover, stress with the oil prices during COVID-19 and the price war between countries such as Saudi Arabia and Russia was expected to drive oil-producing companies to enhance their production efficiency and increase the demand in the sector.

Oil & Gas Sensors Market Trends

Upstream Industries Offer Potential Growth

- Natural gas and crude oil are discovered and produced in the upstream sector. Electricity generation, industrial processes, and transportation heavily rely on crude oil. Rock layers hide the deep subterranean locations of natural gas and crude oil. Many reservoirs are located underwater or in hard-to-reach places with harsh climates.

- As a result, sensors and other important seismic images assist manufacturers in obtaining precise drilling location information. This aids them in cutting down on the additional expenses related to drilling. In addition, the demand for sensors during the oil and gas procurement process is driven by affordable sensors, expanding connectivity, and rising computational power. Real-time data provided by sensors built into equipment assist businesses in scheduling repairs and streamlining daily operations.

- The oil and gas sector's systems, equipment, and sensors must communicate data and learn from one another to enhance efficiency, productivity, health, and safety. Therefore, it will be simple to identify when workers are exposed to unhealthy hazardous substances with the aid of wireless sensors and personal monitoring devices. Consequently, effective steps can be taken. Therefore, it is anticipated that the abovementioned factors will favorably affect the oil and gas industry's sensors market throughout the forecast period.

- The upstream and low carbon energy business segment of major firms such as BP PLC generated USD 89.44 billion in 2022. Moreover, the Abu Dhabi National Oil Company (ADNOC) announced that it revised its upstream methane intensity objective and aims to achieve 0.15 percent by 2025. The new goal, the lowest in the Middle East, strengthens ADNOC's position as a pioneer in the ethical production of low-carbon energy. To improve the monitoring of methane emissions, ADNOC is also looking into experimental technologies, including satellite monitoring and drone-mounted sensors.

Europe Holds a Significant Market Share

- Due to governments' increased focus on pollution control and energy efficiency requirements, oil and gas sensors have become more common in European countries, including Germany, France, and the United Kingdom. An expanding end-user base and expanded applications for gas sensors are two factors that would fuel market growth in this sector.

- The strict emission control requirements and government activities in the European Union to promote energy efficiency are credited with expanding the target market in Europe. These gas sensors are also used in gas or smoke alarms, which operate on the same principles. Additionally, consumers' growing awareness of environmental safety is driven by the increased adoption of goods used in air monitoring systems to detect pollution levels and volatile organic compounds. The infrared sensors type of gas sensor technology currently rules the European market.

- The more forward-thinking oil and gas industry in Europe is refocusing its attention away from the Internet of Things (IoT) smart objects like sensors and other devices and toward developing audacious strategies for using the data obtained from these objects to build more intelligent business models that help their business grow.

- Oil and gas refineries can be informed about the sorts of oil that have been delivered using the information gathered by IoT sensors. This allows businesses to decide on crucial manufacturing, inventory, and operational decisions. Real-time inventory management with IoT sensors and enhanced connectivity can provide a more efficient supply chain for the European oil and gas industry.

- Moreover, the Norwegian police put drone detection systems on offshore oil and gas facilities to investigate recent safety violations in reaction to recent damage to the Nord Stream gas pipelines. Strategic placement of the sensors allowed for the detection of unregistered drones and the prevention of their use.

Oil & Gas Sensors Industry Overview

The oil and gas sensors market is fragmented and competitive. The deployment of sensors at different oil and gas industry activities, such as upstream, midstream, and downstream, is growing at an organizational level. This creates a competitive environment among the players. Some players are Honeywell International Inc., Siemens AG, and ABB Ltd.

In March 2023, The Ministry of Electronics and Information Technology announced the launch of three IoT sensor-based products, which include a Smart Digital Thermometer, IoT Enabled Environmental Monitoring System, and a Multichannel Data Acquisition System in the CoE in IoT Sensors.

In October 2022, Honeywell displayed its latest sensor technologies at the Abu Dhabi International Petroleum Exhibition and Conference to help the transition to sustainable energy. The technologies displayed included energy storage systems, emission monitoring systems, the business's advanced plastics recycling technology, its portfolio of worker safety solutions, and carbon capture and hydrogen generation technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Safety Systems in the Oil and Gas Industry

- 5.1.2 Increasing Need for a Simplified Network Architecture in the Wireless Sensor Segment

- 5.2 Market Restraints

- 5.2.1 Rigid Regulations Imposed on Oil and Gas Drilling Activities

6 MARKET SEGMENTATION

- 6.1 By Sensor Type

- 6.1.1 Gas Sensor

- 6.1.2 Temperature Sensor

- 6.1.3 Ultrasonic Sensor

- 6.1.4 Pressure Sensor

- 6.1.5 Flow Sensor

- 6.1.6 Level Sensor

- 6.1.7 Other Sensor Types

- 6.2 By Connectivity

- 6.2.1 Wired

- 6.2.2 Wireless

- 6.3 By Activity

- 6.3.1 Upstream

- 6.3.2 Midstream

- 6.3.3 Downstream

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Indonesia

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Mexico

- 6.4.4.2 Brazil

- 6.4.4.3 Argentina

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 TE Connectivity Ltd.

- 7.1.3 Robert Bosch GmbH

- 7.1.4 ABB Ltd.

- 7.1.5 Siemens AG

- 7.1.6 Rockwell Automation Inc.

- 7.1.7 Analog Devices Inc.

- 7.1.8 Emerson Electric Company

- 7.1.9 GE Sensing & Inspection Technologies GmbH

- 7.1.10 SKF AB