|

市場調査レポート

商品コード

1404354

神経刺激装置-市場シェア分析、産業動向・統計、2024~2029年成長予測Neurostimulation Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 神経刺激装置-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

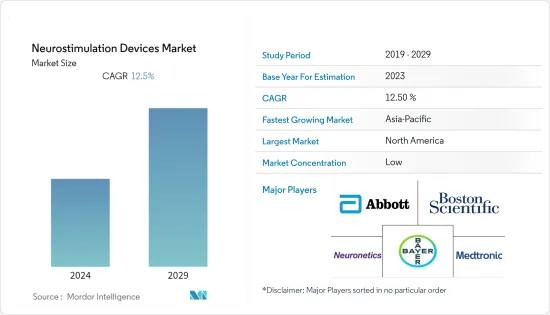

神経刺激装置市場は、2024年に82億1,000万米ドルと評価され、予測期間(2024~2029年)のCAGRは12.5%を記録し、148億2,000万米ドルに達すると予測されています。

神経刺激装置市場は、サプライチェーンの混乱、病院やクリニックによる手術サービスの延期、エンドユーザー産業からの需要の低下により、特にその初期段階において、COVID-19パンデミックによって大きな影響を受けました。例えば、PubMedが2022年3月に発表した研究によると、経頭蓋磁気刺激療法(TMS)の障害には、必要のない手技の中止、人員不足、PPEや消毒用品の入手制限、社会的距離を置く勧告を遵守するための設備が整っていないクリニックや事業所などがあった。これは臨床現場における神経刺激装置の需要に顕著な影響を与えました。パーキンソン病(PD)とジストニア患者は、COVID-19パンデミックの間、社会的制限措置に関連した慢性的ストレスのリスクにさらされていました。しかし、COVID-19の蔓延が下火になるにつれて、神経刺激装置の急速な技術進歩に加え、世界中でパイプライン製品が増加したため、市場は今後1年間で大きな成長を遂げることが予想されます。

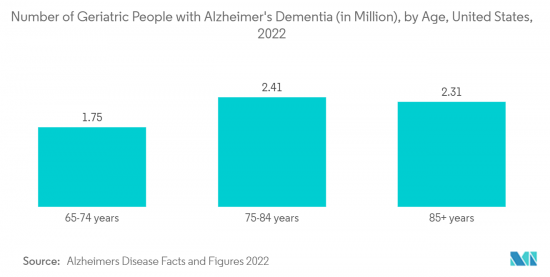

神経疾患の有病率の上昇や神経刺激装置の技術進歩などの要因が、予測期間中の市場成長を後押しすると予想されています。例えば、世界保健機関(WHO)の2021年9月の報告書によると、世界中で約5,500万人が認知症を患っており、毎年1,000万人近くの症例が報告されています。したがって、神経疾患の有病率の上昇に伴い、神経刺激装置の需要が増加することが予想され、これが調査対象市場の成長に影響を与えると予測されます。さらに、NHSが2023年1月に発表したPrimary Care Dementia Dataによると、2023年1月にイングランドで65歳以上の男性7,355人、女性6,693人が認知症と報告されています。このように、神経疾患の罹患率が高いことから、神経刺激装置の需要は増加し、予測期間中の市場成長を促進すると予想されます。

さらに、製品の発売や提携など、主要企業による戦略的活動の増加や、規制当局による製品承認の急増も市場の成長を後押しします。例えば、2022年1月、TensCare社は、Arab Health 2022において、糖尿病性神経障害、腰痛、坐骨神経痛、変形性関節症、出産時の急性疼痛の緩和などの慢性疼痛の長期治療において、薬物を使用しない疼痛緩和に広く使用される経皮的電気神経刺激の最新製品を展示しました。同様に、2022年11月、商業段階のバイオエレクトロニクス医療企業であるElectroCore, Inc.は、非侵襲性迷走神経刺激装置(nVNS)であるガンマコア・サファイア(γCore Sapphire)について、ベルギー製薬協会からユニーク・ナショナル・プロダクト・コード・ナンバーを取得しました。さらに2022年8月、Medtronic Private Limitedはインドで、運動障害やてんかんに伴う症状を治療するための深部脳刺激(DBS)療法用指向性リードシステムSenSightを発売しました。脳深部刺激療法(DBS)は、振戦、こわばり、歩行障害などのパーキンソン病の症状に対する治療法です。

このように、神経疾患の増加や主要企業による戦略的活動により、調査対象市場は予測期間中に大幅な成長が見込まれます。しかし、神経刺激装置に関連する合併症や厳しい装置承認規制などの要因が、予測期間中の市場成長を抑制すると予想されます。

神経刺激装置の市場動向

予測期間中は脊髄刺激装置が市場を独占する見込み

脊髄刺激装置分野は、うつ病や慢性疼痛などの他の疾患と相まって神経疾患の有病率が増加していることや、技術的に高度な製品の採用が増加していることなどの要因により、予測期間中に大きな成長が見込まれます。例えば、National Spinal Cord Injury Statistical Center(NSCISC)によると、米国におけるSCIの発症率は2022年には約3億3,400万人でした。また、外傷性脊髄損傷(tSCI)の年間発症率は、米国では100万人あたり約54件で、これは年間約1万8,000件の新たなtSCI症例に相当します。したがって、脊髄損傷の増加に伴い、脊髄刺激装置の需要も増加しています。

さらに、脊髄刺激装置の発売の増加、規制当局の承認、装置の進歩は、予測期間中の市場成長を促進すると予想されます。例えば、2022年12月、Abbott社は、同社のEterna脊髄刺激(SCS)システムのFDA承認を取得しました。このシステムは、慢性疼痛を治療するために現在利用可能な最小の植え込み型充電式脊髄刺激装置です。さらに、市場に多相脊髄刺激装置を導入することで、同分野の成長が促進されると予想されます。例えば、2023年4月、Biotronikは脊髄刺激(SCS)システムであるProsperaのFDA承認を取得しました。このシステムは、Embrace Oneと組み合わせた初の多相刺激パラダイムであるRESONANCEを特徴としています。この患者中心のモデルは、自動的で客観的な毎日の遠隔モニタリングと継続的な管理とサポートを提供することにより、プロアクティブケアを可能にします。同様に、2022年9月、台湾の医療装置メーカーであるGIMER Medicalは、同社の脊髄刺激システムについて、FDAから条件付き治験装置適用除外(IDE)承認を取得しました。この埋め込み型装置は、特許技術により患者の慢性疼痛を緩和することを目的としています。GIMER MedicalのNeuroBlock SCSシステムは、脊髄に500kHzの新しい高周波刺激を放出することにより、効果的な疼痛管理を提供します。

したがって、脊髄損傷の増加、主要企業による規制当局の承認と戦略的製品の発売の急増により、研究セグメントは予測期間中に成長すると予想されます。

北米は予測期間中に大幅な成長が見込まれる

北米は、高齢者人口の増加、神経疾患の増加、主要企業による戦略的製品投入により、神経刺激装置市場で健全な成長が見込まれます。例えば、Parkinson's Foundationの2022年最新情報によると、米国では約100万人がパーキンソン病(PD)と共に生活しています。この数は2030年までに120万人に増加すると予想されています。パーキンソン病は、アルツハイマー病に次いで2番目に多い神経変性疾患です。さらに、2021年11月にParkinson's Canadaが発表した報告書によると、10万人以上のカナダ人がパーキンソン病を患っており、毎日25人以上がパーキンソン病と診断されています。したがって、神経疾患の有病率の高さは、北米の市場成長を後押しする可能性が高いです。

さらに、主要参入企業の存在とその戦略的製品発売、提携、協力関係が、予測期間中の市場成長を後押しすると予想されます。例えば、2021年1月、Boston Scientific Corporationは、個別化された疼痛緩和のための治療オプションを組み合わせた脊髄刺激装置(SCS)システムポートフォリオであるWaveWriter Alphaを発売しました。同様に、2022年1月、Nevro CorpはSenza Spinal Cord Stimulation(SCS)システムの非外科的難治性腰痛(NSRBP)治療に対する表示拡大の承認をFDAから取得しました。また、2022年1月には、Medtronicが、糖尿病性末梢神経障害(DPN)に伴う慢性疼痛の治療用として、充電式神経刺激装置Intellisと充電不要の神経刺激装置VantaのFDA承認を取得しました。

このように、この地域では神経障害の症例が増加しており、企業活動も活発化していることから、予測期間中の市場成長が期待されています。

神経刺激装置産業概要

神経刺激装置市場は、世界的に事業を展開する複数の企業が存在するため、その性質上断片化されています。主要企業は、買収、提携、研究開発活動や新製品の発売への多額の投資など、さまざまな戦略を採用しています。主要企業には、Abbott、Bayer AG、Boston Scientific Corporation、Laborie、LivaNova PLC、Neuronetics、NeuroPace, Inc.、Nevro Corp.、Medtronic、Synapse Biomedical Inc.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 神経疾患の有病率の上昇

- 神経刺激装置の技術進歩

- 市場抑制要因

- 神経刺激装置に関連する合併症

- 厳しい装置承認規制

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 装置タイプ別

- 植込み型装置

- 脊髄刺激装置

- 脳深部刺激装置

- 仙骨神経刺激装置

- 迷走神経刺激装置

- 胃電気刺激装置

- その他の装置

- 外部装置

- 経頭蓋磁気刺激(TMS)

- 経皮的電気神経刺激(TENS)

- その他の外部装置

- 植込み型装置

- 用途別

- パーキンソン病

- てんかん

- うつ病

- ジストニア

- 疼痛管理

- その他の用途

- エンドユーザー別

- クリニック

- 病院

- リハビリセンター

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott

- Curonix LLC

- Boston Scientific Corporation

- Aleva Neurotherapeutics

- LivaNova PLC

- Neuronetics

- NeuroPace, Inc

- Nevro Corp

- Medtronic

- Synapse Biomedical Inc.

第7章 市場機会と今後の動向

The neurostimulation devices market is valued at USD 8.21 billion in 2024 and is expected to reach USD 14.82 billion registering a CAGR of 12.5% over the forecast period (2024-2029).

The neurostimulation devices market was significantly impacted by the COVID-19 pandemic, particularly in its early stages, due to the disruptions in the supply chain, postponements of surgical services by hospitals and clinics, and low demand from end-user industries. For instance, according to a study published in March 2022 by PubMed, the barriers to transcranial magnetic stimulation (TMS) included suspension of nonessential procedures, staffing shortages, limited access to PPE and sanitization supplies, and clinics or offices ill-equipped to comply with social distancing recommendations. This notably impacted the demand for neurostimulation devices in clinical settings. Patients with Parkinson's disease (PD) and dystonia were at risk of chronic stress related to social restriction measures during the COVID-19 pandemic. However, as the spread of COVID-19 came down, the market is expected to witness significant growth in the coming year due to the rapid technological advancements in neurostimulation devices coupled with a rise in pipeline products across the globe.

Factors such as the rising prevalence of neurological disorders and the technological advancements in neurostimulation devices are expected to bolster market growth over the forecast period. For instance, according to the September 2021 report of the World Health Organization, about 55 million people around the world were living with dementia, and nearly 10 million cases were reported every year. Thus, with the rise in the prevalence of neurological diseases, the demand for neurostimulation devices is expected to increase, which is anticipated to impact the growth of the studied market. Furthermore, according to the Primary Care Dementia Data, published in January 2023 by NHS, 7,355 males and 6,693 females of age 65 and above were reported with Dementia in England in January 2023. Thus, owing to the high incidence of neurological diseases, the demand for neurostimulation devices is expected to rise, fuelling market growth over the forecast period.

Furthermore, an increase in strategic activities by the key players, such as product launches and collaborations, and a surge in product approvals by the regulatory authorities bolsters market growth. For instance, in January 2022, TensCare showcased its latest in transcutaneous electrical nerve stimulation widely used for drug-free pain relief in the long-term treatment of chronic pain conditions such as diabetic neuropathy, backache, sciatica, osteoarthritis and the relief of the acute pain of childbirth at Arab Health 2022. Similarly, in November 2022, ElectroCore, Inc., a commercial-stage bioelectronic medicine company, received a Unique National Product Code Number from the Belgian Pharmaceutical Association for its gammaCore Sapphire non-invasive vagus nerve stimulator (nVNS). Further, in August 2022, Medtronic Private Limited launched the SenSight directional lead system for Deep Brain Stimulation (DBS) therapy to treat symptoms associated with movement disorders and epilepsy in India. Deep brain stimulation (DBS) is a treatment for symptoms of Parkinson's disease, including tremors, stiffness, and trouble walking.

Thus, owing to the increase in neurological diseases and strategic activities by the key players, the studied market is expected to witness significant growth over the forecast period. However, factors such as the complications associated with neurostimulation devices and stringent device approval regulations are expected to restrain the market growth during the forecast period.

Neurostimulation Devices Market Trends

Spinal Cord Stimulator is Expected to Dominate the Market During the Forecast Period

The spinal cord stimulators segment is expected to witness significant growth over the forecast period owing to factors such as the increasing prevalence of neurological disorders coupled with other diseases such as depression and chronic pain and the increasing adoption of technologically advanced products. For Instance, as per the National Spinal Cord Injury Statistical Center (NSCISC), the incidence of SCI in the United States was about 334 million in 2022. Also, the annual incidence of traumatic spinal cord injury (tSCI) was approximately 54 cases per one million people in the United States, which equals about 18,000 new tSCI cases yearly. Hence, the demand for spinal cord stimulators is increasing with the increase in spinal cord injuries.

Furthermore, the increase in spinal cord stimulator launches, regulatory approvals, and advancements in the device are expected to bolster the market growth over the forecast period. For Instance, in December 2022, Abbott received FDA approval for the company's Eterna spinal cord stimulation (SCS) system, the smallest implantable, rechargeable spinal cord stimulator currently available for treating chronic pain. Further, introducing multiphase spinal cord stimulators to the market is expected to fuel the segment's growth. For Instance, in April 2023, Biotronik received FDA approval for Prospera, a spinal cord stimulation (SCS) system. The system features RESONANCE, the first multiphase stimulation paradigm, paired with Embrace One. This patient-centric model makes proactive care possible by offering automatic, objective, daily remote monitoring and ongoing management and support. Similarly, in September 2022, Taiwanese medical device manufacturer GIMER Medical received conditional Investigational Device Exemption (IDE) approval from the FDA for the company's spinal cord stimulation system. The implantable device aims to relieve patients' chronic pain with its patented technology. GIMER Medical's NeuroBlock SCS system offers effective pain management by releasing a novel high-frequency stimulation of 500 kHz to the spinal cord.

Therefore, due to the increase in spinal cord injuries and the surge in regulatory approvals and strategic product launches by the key players, the studied segment is expected to grow over the forecast period.

North America is Expected to Witness a Significant Growth Over the Forecast Period

North America is expected to witness healthy growth in the neurostimulation devices market owing to the rising geriatric population, increasing neurological disorders, and strategic product launches by the key players. For instance, as per the 2022 update from the Parkinson's Foundation, nearly one million people in the United States are living with Parkinson's disease (PD). This number is expected to rise to 1.2 million by 2030. Parkinson's is the second-most common neurodegenerative disease after Alzheimer's disease. Additionally, as per the report published by Parkinson's Canada in November 2021, more than 100,000 Canadians live with Parkinson's, and more than 25 people are diagnosed with Parkinson's disease every day. Hence, the high prevalence of neurological diseases will likely boost the market growth in North America.

Furthermore, the presence of key players and its strategic product launches, partnerships, and collaborations are expected to bolster the market growth over the forecast period. For instance, in January 2021, Boston Scientific Corporation launched the WaveWriter Alpha, a Spinal Cord Stimulator (SCS) system portfolio that combines therapy options for personalized pain relief. Similarly, in January 2022, Nevro Corp received approval from the FDA for expanded labeling for its Senza Spinal Cord Stimulation (SCS) System for treating Non-Surgical Refractory Back Pain (NSRBP). Also, in January 2022, Medtronic received FDA approval for its Intellis rechargeable neurostimulator and Vanta recharge-free neurostimulator for treating chronic pain associated with diabetic peripheral neuropathy (DPN).

Thus, the increasing cases of neurological disorders and increasing company activities in the region are expected to augment the market growth over the forecast period.

Neurostimulation Devices Industry Overview

The neurostimulation devices market is fragmented in nature due to the presence of several companies operating globally. The key players are adopting various strategies, such as acquisitions, partnerships, and heavy investments in research and development activities and new product launches. The major players include Abbott, Bayer AG, Boston Scientific Corporation, Laborie, LivaNova PLC, Neuronetics, NeuroPace, Inc., Nevro Corp., Medtronic, and Synapse Biomedical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Prevalence of Neurological Disorders

- 4.2.2 Technological Advancements in Neurostimulation Devices

- 4.3 Market Restraints

- 4.3.1 Complications Associated with Neurostimulation Devices

- 4.3.2 Stringent Device Approval Regulations

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Device Type

- 5.1.1 Implantable Devices

- 5.1.1.1 Spinal Cord Stimulators

- 5.1.1.2 Deep Brain Stimulators

- 5.1.1.3 Sacral Nerve Stimulators

- 5.1.1.4 Vagus Nerve Stimulators

- 5.1.1.5 Gastric Electric Stimulators

- 5.1.1.6 Other Device Types

- 5.1.2 External Devices

- 5.1.2.1 Transcranial Magnetic Stimulation (TMS)

- 5.1.2.2 Transcutaneous Electrical Nerve Stimulation (TENS)

- 5.1.2.3 Other External Devices

- 5.1.1 Implantable Devices

- 5.2 By Application

- 5.2.1 Parkinson's Disease

- 5.2.2 Epilepsy

- 5.2.3 Depression

- 5.2.4 Dystonia

- 5.2.5 Pain Management

- 5.2.6 Other Applications

- 5.3 By End-Users

- 5.3.1 Clinics

- 5.3.2 Hospitals

- 5.3.3 Rehabilitation Centers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 Curonix LLC

- 6.1.3 Boston Scientific Corporation

- 6.1.4 Aleva Neurotherapeutics

- 6.1.5 LivaNova PLC

- 6.1.6 Neuronetics

- 6.1.7 NeuroPace, Inc

- 6.1.8 Nevro Corp

- 6.1.9 Medtronic

- 6.1.10 Synapse Biomedical Inc.