|

市場調査レポート

商品コード

1639383

低VOC塗料:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Low VOC Paint - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 低VOC塗料:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

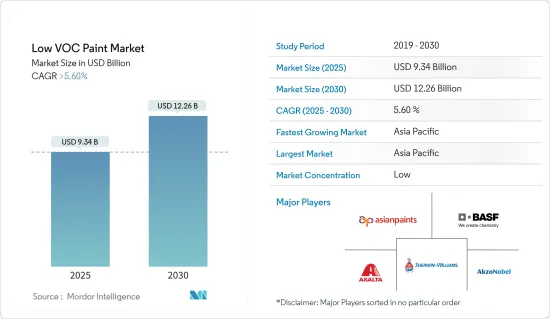

低VOC塗料市場規模は2025年に93億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.6%を超え、2030年には122億6,000万米ドルに達すると予測されます。

主要ハイライト

- COVID-19の大流行は、2020年と2021年の低VOC塗料市場に影響を及ぼし、建設と工業生産高の減少と相まって経済・商業活動の縮小をもたらしました。しかし、市場は近年回復し、この期間中に成長すると予測されます。

- 環境に優しく安全に使用できる低VOC塗料とは相反する、従来の塗料の有害性に対する意識の高まりが、予測期間中の市場の成長を促進すると予想されます。

- 一方、従来型塗料に比べ低VOC塗料のコストが高いことが市場成長の妨げになると予想されます。

- グリーンビルディングの建設の増加、環境に優しい化学品へのシフト、低VOC塗料のリサイクルは、予測期間中に調査された市場に機会を提供すると考えられます。

- アジア太平洋は、建築産業からの低VOC塗料の消費量が多いため、世界市場を独占しています。

低VOC塗料市場の動向

市場を独占する建築・装飾セグメント

- 装飾用塗料は、表面を天候の影響から保護し、防水性を高め、シロアリの攻撃から表面を保護し、表面の耐久性を向上させ、建物に美的魅力を与えます。

- 加えて、腐食、バクテリア、紫外線、カビ、浸水、藻類からの保護も提供し、構造物の寿命を延ばします。

- 低VOC塗料の需要は、世界の住宅・商業建築の増加に牽引され、建築・装飾産業が大部分を占めています。

- 中国の成長の原動力は、主に住宅と商業施設の急速な拡大です。同国の建設生産高は2022年にピークに達し、約4兆6,400億米ドル(31兆2,000億元)に達しました。その結果、これらの要因が予測期間中の市場需要を増加させる傾向にあります。

- 米国国勢調査局によると、商業施設の完成額は景気後退前の水準まで回復し、2022年には1,150億米ドルに達します。米国で着工された商業開発で最も人気のあるタイプは、倉庫と個人事務所です。さらに、2023年1~8月期の建設支出は1兆2,847億米ドルに達し、2022年同期の1兆2,334億米ドルから4.2%増加しました。

- さらに、Eurostatによると、EU復興基金からの新規投資により、2022年の欧州の建設部門は2.5%成長しました。2022年の主要建設プロジェクトは非住宅建設(オフィス、病院、ホテル、学校、工業用建物)で、活動全体の31.3%を占めます。

- このような建設活動は、低VOC塗料などの需要を予測期間中に増加させると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋が世界市場を独占しています。インド、中国、フィリピン、ベトナム、インドネシアなどの国々では、住宅や商業施設の建設への投資が増加しており、低VOC塗料市場は今後数年間で拡大すると予想されます。

- 低VOC塗料は通常の塗料に比べて環境に優しいため、建設産業で広く使用されています。低VOC塗料は、内外壁、天井、トリム、コンクリート床、金属表面、家具、キャビネットの塗装など、さまざまな用途に使用されています。

- 建設産業は、第14次5カ年計画(FYP 2021~2025)の一環としてのインフラ投資に支えられ、2024~2027年にかけて年平均4.3%の成長率を記録すると予想されています。さらに、2030年までにインフラ建設プロジェクトに6兆8,000億人民元(1兆1,000億米ドル)の政府資金が投入されることも、産業の成長を後押しします。2022年、国家開発改革委員会(NDRC)は、1兆5,000億人民元(2,223億米ドル)相当の109の固定資産投資プロジェクトを承認しました。

- 中国政府によると、2023年1月、新たな信用施策が発表され、中国国内の都市部の住宅販売を促進することを目的としています。中国での住宅販売を促進するため、多くの地方当局がバウチャー制度を発表しました。また、2022年初めには、政府は290億米ドルの特別融資を発表し、建設会社が停滞しているプロジェクトを完了できるようにしました。

- さらに、インド政府は今後7年間で約1兆3,000億米ドルを住宅に投資するようです。これにより、6,000万戸の住宅が新たに建設される見込みです。こうしたプロジェクトが建設産業における低VOC塗料市場を牽引しています。

- さらに、インドネシア政府は、インドネシア全土に約100万戸の住宅を建設するプログラムを開始し、そのための予算として約10億米ドルを計上しています。このため、市場の成長は著しく高まっています。

- 低VOC塗料は従来の塗料に比べてVOCの含有量が大幅に少ないため、より環境に優しく健康的な選択肢となります。自動車産業では、低VOC塗料は自動車の外装や内装、自動車タイヤ部品の塗装、損傷した自動車の再塗装に使用されています。

- 中国汽車工業協会(CAAM)によると、中国は世界で最も重要な自動車生産拠点であり、2022年の自動車総生産台数は約2,702万台と、昨年の2,612万台から3.4%増加します。従って、自動車セクターにおける低VOC塗料の巨大な市場となります。

- このように、上記の要因は予測期間中、同地域における低VOC塗料の需要を促進すると予想されます。

低VOC塗料産業概要

低VOC塗料市場は、その性質上、部分的にセグメント化されています。主要参入企業(順不同)としては、Akzo Nobel N.V.、Asian Paints、BASF SE、Axalta Coating Systems, LLC、The Sherwin-Williams Companyなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 従来型塗料の有害性に関する意識の高まり

- 建築・装飾産業における需要の増加

- その他の促進要因

- 抑制要因

- 従来の塗料に比べてコストが高い

- その他の抑制要因

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ

- 低VOC

- VOCなしまたはゼロ

- 天然

- 配合タイプ

- 水性

- 溶剤型

- 粉末

- 用途

- アーキテクチャと装飾

- 一般工業

- 自動車OEM

- 自動車補修

- 海洋

- 耐久消費財

- その他の用途(医薬品、エレクトロニクスなど)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Akzo Nobel N.V.

- American Formulating & Manufacturing

- Arkema

- Asian Paints

- AURO

- Axalta Coating Systems, LLC

- BASF SE

- Benjamin Moore & Co.

- Berger Paints India Limited

- BioShield Paint Company

- Cloverdale Paint Inc.

- Crown Trade

- Fine Paints of Europe

- Jotun

- Kalekim

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- The Sherwin-Williams Company

第7章 市場機会と今後の動向

- グリーンビルディング建設の増加

- 環境に優しい化学品へのシフト

目次

Product Code: 49060

The Low VOC Paint Market size is estimated at USD 9.34 billion in 2025, and is expected to reach USD 12.26 billion by 2030, at a CAGR of greater than 5.6% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic impacted the low VOC paint market in 2020 and 2021, driven by reduced economic and commercial activities coupled with declines in construction and industrial output. But the market recovered in recent years and is anticipated to grow over the period.

- The increasing awareness about the harmful effects of conventional paints, which is contrary to low VOC paints as they are eco-friendly and safe to use, is expected to drive the market's growth during the forecast period.

- On the other hand, the high cost of low VOC paint compared to conventional paint is expected to hinder the market's growth.

- The increasing construction of green buildings, shift toward eco-friendly chemicals, and recycling of low VOC paint will likely provide opportunities for the market studied during the forecast period.

- Asia-Pacific dominated the global market due to the high consumption of low-VOC paints from the architectural industry.

Low VOC Paint Market Trends

Architectural and Decorative Segment to Dominate the Market

- Decorative paints help protect the surface from the impact of weather, make the surface waterproof, protect the surface from termite attacks, and increase surface durability, providing an aesthetic appeal to the building.

- In addition, they offer protection from corrosion, bacteria, UV radiation, fungus, water seepage, and algae and enhance the structure's life.

- The demand for Low VOC paints is dominated by the architectural and decorative industry, driven by the growing residential and commercial construction activities worldwide.

- China's growth is fueled mainly by rapid residential and commercial building expansion. The country's construction output peaked in 2022 at about USD 4.64 trillion (31.2 trillion yuan). As a result, these factors tend to increase the market demand during the forecast period.

- According to the US Census Bureau, the value of completed commercial construction has rebounded to pre-recession levels, reaching USD 115 billion in 2022. The most popular types of commercial development started in the United States were warehouses and private offices. Additionally, during the first eight months of 2023, construction spending amounted to USD 1,284.7 billion, which increased by 4.2% to USD 1,233.4 billion for the same period in 2022.

- Furthermore, according to Eurostat, the European construction sector grew by 2.5% in 2022 due to new investments from the EU Recovery Fund. The major construction projects in 2022 accounted for non-residential construction (offices, hospitals, hotels, schools, and industrial buildings), accounting for 31.3% of total activity.

- Such construction activities are expected to increase the demand During the forecast period such as low-VOC paints.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region dominated the global market share. With growing investment in residential and commercial construction in countries such as India, China, the Philippines, Vietnam, and Indonesia, the market for low-VOC paints is expected to increase in the coming years.

- Low-VOC paints are widely used in the construction industry as it is eco-friendly compared to regular paints. Low VOC paints are used for various applications, including painting interior and exterior walls, ceilings, trim, concrete floors, metal surfaces, furniture, and cabinets.

- The construction industry is expected to record an average annual growth rate of 4.3% between 2024 and 2027, supported by investment in infrastructure as part of the 14th Five-Year Plan (FYP 2021-2025). Additionally, growth in the industry will also be aided by CNY 6.8 trillion (USD 1.1 trillion) of government funds for infrastructure construction projects by 2030. In 2022, the National Development and Reform Commission (NDRC) approved 109 fixed asset investment projects worth CNY 1.5 trillion (USD 222.3 billion).

- According to the Government of China, in January 2023, announced the new credit policy aims to drive urban housing sales in the country. To drive housing sales in China, many local authorities announced voucher schemes. Earlier in 2022, the government also announced a pledge of USD 29 billion in special loans, thereby allowing construction firms to finish stalled projects.

- Furthermore, the Indian government is likely to invest around USD 1.3 trillion in housing over the next seven years. It is expected to see the construction of 60 million new homes. Such projects are driving the low VOC paints market in the construction industry.

- Moreover, the Indonesian government has started a program to build about one million housing units across Indonesia, for which the government has allocated about USD 1 billion in the budget. Thus boosting the market growth significantly.

- Low VOC paints contain significantly less VOCs than traditional paints, making them a more environmentally friendly and healthier option. In the automotive industry, low VOC paints are used for painting exteriors and interior surfaces of the vehicle, automotive tire parts and refinishing damaged vehicles.

- According to the China Association of Automobile Manufacturers (CAAM), China has the most significant automotive production base in the world, with a total vehicle production of around 27.02 million units in 2022, registering an increase of 3.4 % compared to 26.12 million units produced last year. Thus providing a massive market for low-VOC paint in the automotive sector.

- Thus, the factors above are expected to drive the demand for low-VOC paints in the region during the forecast period.

Low VOC Paint Industry Overview

The low VOC paint market is partially fragmented in nature. The major players (not in any particular order) include Akzo Nobel N.V., Asian Paints, BASF SE, Axalta Coating Systems, LLC, and The Sherwin-Williams Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Awareness about Harmful Effects of Conventional Paint

- 4.1.2 increasing Demand in Architectural and Decorative Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost in Comparison to Conventional Paint

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Low-VOC

- 5.1.2 No or Zero VOC

- 5.1.3 Natural

- 5.2 Formulation Type

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder

- 5.3 Application

- 5.3.1 Architecture and Decorative

- 5.3.2 General Industrial

- 5.3.3 Automotive OEM

- 5.3.4 Automotive Refinish

- 5.3.5 Marine

- 5.3.6 Consumer Durables

- 5.3.7 Other Applications (Pharmaceuticals, Electronics, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 American Formulating & Manufacturing

- 6.4.3 Arkema

- 6.4.4 Asian Paints

- 6.4.5 AURO

- 6.4.6 Axalta Coating Systems, LLC

- 6.4.7 BASF SE

- 6.4.8 Benjamin Moore & Co.

- 6.4.9 Berger Paints India Limited

- 6.4.10 BioShield Paint Company

- 6.4.11 Cloverdale Paint Inc.

- 6.4.12 Crown Trade

- 6.4.13 Fine Paints of Europe

- 6.4.14 Jotun

- 6.4.15 Kalekim

- 6.4.16 Kansai Paint Co.,Ltd.

- 6.4.17 Nippon Paint Holdings Co., Ltd.

- 6.4.18 PPG Industries, Inc.

- 6.4.19 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Construction of Green Buildings

- 7.2 Shift toward Eco-friendly Chemicals