|

市場調査レポート

商品コード

1851257

肥満手術デバイス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Bariatric Surgery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 肥満手術デバイス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月27日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

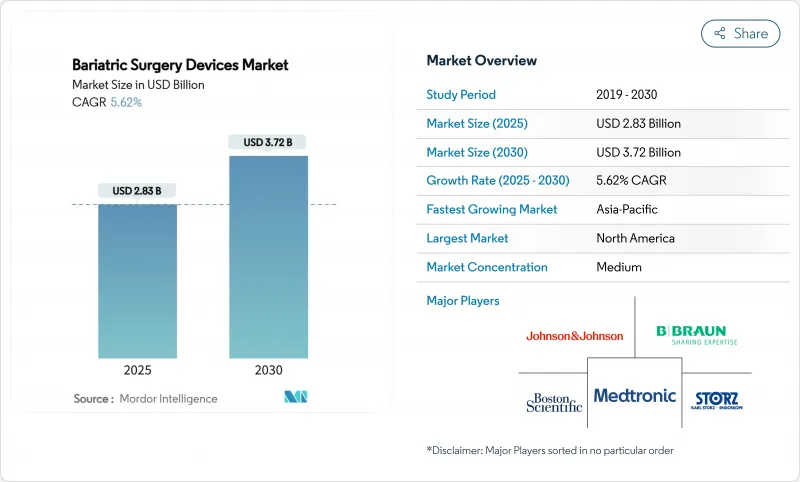

肥満手術デバイス市場規模は2025年に28億3,000万米ドル、2030年には37億2,000万米ドルに達すると予測され、期間中のCAGRは5.62%で推移します。

機器ベースのソリューションがGLP-1受容体作動薬と統合され、長期的な体重管理の成果を改善する柔軟なハイブリッドレジメンをプロバイダーに提供することで、持続的な成長が展開されます。ロボットステープリング、磁気圧迫システム、嚥下可能なバルーンなどの急速な進歩は、手術の精度を高め、回復時間を短縮し、合併症発生率を低下させ、支払者と患者の双方にとって肥満手術デバイス市場の価値提案を強化しています。同時に、競争の激しい分野では、トータル・コスト・オブ・ケアの節約にますます報いるようになる償還基準の進化に適応しつつあり、その結果、病院や外来手術センター全体での技術導入が加速しています。北米は手術件数で主導権を維持しているが、アジア太平洋地域の需要曲線は、肥満が若年層で急増するにつれて急勾配となり、特殊な機器に対する将来的な需要の大きさを裏付けています。これらの要因を総合すると、肥満手術デバイス市場は2030年まで1桁台半ばの着実な拡大が続くと予想される、回復力のある市場です。

世界の肥満手術デバイス市場の動向と洞察

病的肥満の急激な増加

現在、9億人以上の成人が肥満を抱えて生活しており、この集団はあらゆる主要地域で増加し続けており、メタボリック治療への対応可能な患者層を直接的に拡大しています。体格指数が50kg/m2を超える患者の需要は特に強く、このような患者はしばしば、高価格で取引される、より強固なステープル留置術や吻合術を必要とします。アジア太平洋諸国では重度の肥満が最も急増しており、保健省は下流の心血管コストを抑制するために介入の閾値を引き下げています。若い患者は現在、外科手術の候補者の中で不釣り合いな割合を占めており、サプライヤーはより長い機能寿命を持つ器具の開発に拍車をかけています。こうした人口動態の変化は、肥満手術デバイス市場の長期的な拡大基調を補強しています。

代謝外科手術の保険適用拡大

支払い側の政策改革は、歴史的な支払い障壁を解体しつつあります。2026年、メディケアは肥満を手術や抗肥満薬を含む包括的治療が必要な慢性疾患と認定します。ブルークロス・ブルーシールドなどの大手民間保険会社はすでに事前承認のハードルを取り払い、承認にかかる平均時間を14日短縮しています。ルイジアナ州の上院法案106により、2024年にはさらに100万人の住民が強制的な民間保険適用となり、地域の手術件数は直ちに増加しました。持続的な償還の追い風は、2030年までの同分野のCAGRを1.2ポイント押し上げ、肥満手術デバイス市場を生涯薬物療法に代わる費用対効果の高い選択肢として確固たるものにすると予測されます。

長時間作用型GLP-1製剤への嗜好の高まり

セマグルチドとチルゼパチドの週1回製剤と隔週1回製剤は急速に普及したため、処方数の増加のピーク時には米国の肥満治療薬の処方数は25.6%減少しました。それにもかかわらず、外科的手術と薬物療法を組み合わせたレジメンは、過剰体重減少率を高め、合併症の再発を低下させることが縦断的データから示唆されています。したがって、市場参入企業は、器具を基礎的な介入と位置づけ、薬物療法を補助療法とする傾向が強まっています。この連携が逆風を和らげ、CAGRのマイナス影響を1%ポイント以下に緩和しています。

セグメント分析

2024年の肥満手術デバイス市場シェアでは、補助器具が59.63%を占め、ステープルライン補強材、電動ステープラー、先進エネルギーシステムがこれを支えています。製品の進化の中心はリーク軽減であり、3列カートリッジ形状とリアルタイムインピーダンスモニタリングにより、術後合併症発生率は着実に低下しています。ロボットステープリングモジュールは現在、高BMI患者によく見られる厚い胃壁に対応する適応クランプ力機能を組み込んでおり、臨床的信頼性をさらに高めています。予測期間中、補助器具はCAGR 5.78%で拡大すると予測されるが、これはORの標準化とリピート購入を促す継続的なアップグレードを反映しています。

植え込み型器具は、売上ベースでは小さいもの、縫合糸やステープルを使わずに吻合部を形成する磁石対応の圧迫リングなど、価値の高い革新的なレイヤーが追加されつつあります。経口腔的に留置できるスマートバルーンは、手術を望まない患者や手術に適さない患者に対する介入の敷居を低くしています。このサブセグメントの新たな役割には戦略的価値があります。すなわち、デバイスを用いた減量治療に新たな顧客層を導入し、より侵襲的な治療への将来的なパイプラインを構築することで、市場セグメンテーションのアクセス可能な総パイを拡大することができます。

スリーブ胃切除術は2024年の肥満手術デバイス市場規模の43.49%を占め、中等度から重度の肥満に対してスリーブを推奨する臨床ガイドラインに支えられています。メーカー各社は、手術時間を最大18%短縮するために、先端が曲がったステープラーやあらかじめ装填されたバットレス材の改良を続けています。しかし、内視鏡的スリーブ胃形成術(ESG)はその差を縮めつつあり、12ヵ月後の総体重減少率13.6%を最小限の有害事象で示した臨床エビデンスにより、6.45%のCAGRを記録しています。病院はESGを、複雑な再置換術のために手術室のキャパシティを解放する日帰り手術の代替手段と位置づけるようになっており、間接的に高度な縫合プラットフォームや内視鏡用アクセサリーの売上を刺激しています。

費用対効果のデータでは、ESGはセマグルチドと比較して5年間で3万3,583米ドルの節約となり、自費診療を行う雇用主にとって魅力的な薬剤となっています。機器メーカーは、内視鏡縫合ツールにAIガイド付きナビゲーションをバンドルし、縫合位置の精度を高めることで対応しています。一方、ロボット支援によるRoux-en-Yは、超肥満患者や重度の逆流がある患者に依然として関連しており、30mmリロードステープラーやシングルサイトトロッカーキットの需要を支えています。多様な手技のポートフォリオが肥満手術デバイス市場の対応可能領域を拡大します。

地域分析

北米は2024年の世界売上高の42.10%を占め、幅広い保険適用範囲と確立された外科医ネットワークに後押しされました。GLP-1の導入により2024年の症例数は減少したが、手術件数は脱落による転換を経て回復し、2030年までのCAGRは5.15%と堅調な見通しです。カナダは米国のダイナミクスを反映しているが、州の助成金上限が定期的な待機患者数の変動をもたらし、四半期ごとの機器出荷を形成しています。

アジア太平洋地域は、2030年までのCAGRが7.02%と予測され、最も急速に成長する地域です。これは、アジア太平洋地域の肥満負担の急増と中間層の可処分所得の拡大を反映しています。中国とインドは2024年に合わせて18万件以上の手術を行うが、普及率はまだ対象者の2%未満であり、未開拓の余地が大きいです。医療ツーリズムの中心地であるタイと韓国では、欧米市場よりも30~50%安い費用で手術が受けられるが、国際的な患者の流れは認定ステータスへの感度を高めており、プロバイダーは信頼保証のためにグローバルブランドの機器を採用するようになっています。

欧州は、エビデンスに基づく医療機器導入を支持する国民皆保険制度に支えられ、5.46%の緩やかな拡大を維持しています。2025年に発表された新しい医療ツーリズム安全基準は、海外の肥満治療センターに対し、機器のトレーサビリティと外科医の資格証明書を文書化するよう求めています。南米と中東・アフリカは、合わせても現在の売上高の10%未満に過ぎないが、民間病院への投資と質の高い医療を求める外国人人口の増加によって活気づき、CAGR約6%で成長します。これらの新興市場が成熟するにつれて、現地に根ざしたトレーニングイニシアティブと流通を一致させるサプライヤーは、さらなるシェアを獲得することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 病的肥満の急増

- 代謝外科手術の保険適用拡大

- 低侵襲&ロボットプラットフォームの採用

- スリーブ状胃切除術の急増

- GLP-1薬の脱落が外科手術への転換を促す

- 磁気吻合器とスマートバルーンパイプライン

- 市場抑制要因

- 長時間作用型GLP-1製剤への嗜好の高まり

- 新興市場では肥満外科医の数は限られている

- 高い医療機器と手技コスト

- ステープラーとバンドに関するFDAの厳しいリコール

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- デバイスタイプ別

- インプラントデバイス

- 胃バンド

- 胃バルーン

- 胃電気刺激システム

- 十二指腸-空腸バイパススリーブ

- アシストデバイス

- ステープル留め器具

- 縫合機器

- トロッカー&アクセスシステム

- ベッセルシールデバイス

- その他のアシストデバイス

- インプラントデバイス

- 手技タイプ別

- スリーブ状胃切除術(SG)

- Roux-en-Y胃バイパス術(RYGB)

- アジャスタブル・ガストリック・バンディング(AGB)

- 十二指腸スイッチ併用胆膵転換術(BPD-DS)

- 内視鏡的スリーブ胃形成術(ESG)

- 胃内バルーン

- 新興磁気&VBLOC手技

- 手術タイプ別

- 低侵襲

- 非侵襲性

- エンドユーザー別

- 病院

- 肥満外科クリニック

- 外来手術センター

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Allurion Technologies, Inc.

- Apollo Endosurgery

- Asensus Surgical

- Aspire Bariatrics

- B. Braun Melsungen AG

- BariaTek Medical

- Boston Scientific

- Changzhou Ankang Medical Instruments Co., Ltd.

- Cousin Surgery

- GI Dynamics

- IntraPace

- Intuitive Surgical

- Johnson & Johnson

- Karl Storz SE & Co. KG

- Medtronic PLC

- Olympus Corporation

- ReShape Lifesciences Inc

- Silimed Industria de Implantes

- Spatz Medical

- Teleflex Incorporated