|

市場調査レポート

商品コード

1402995

農業用タイヤ:市場シェア分析、産業動向・統計、成長予測、2024~2029年Agricultural Tires - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 農業用タイヤ:市場シェア分析、産業動向・統計、成長予測、2024~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

農業用タイヤ市場の現在の市場規模は65億7,000万米ドルです。

今後5年間で88億8,000万米ドルに達し、予測期間中のCAGRは5.13%を超えると予想されます。

市場全体のシナリオは明るいもの、需要は農家の収入や農業機械の購入に必ず影響を与える経済の混乱に大きく左右されます。しかし、2020年にはCOVID-19の大流行が農業用タイヤ市場を含む自動車産業に深刻な影響を与えたため、農機具販売の低迷が見られました。

効率的で生産性の高い農業機械の最終製品に対する需要の高まりが、特に先進国市場を牽引しています。中国に次いで、ドイツは農業用タイヤの第2位の輸出・製造国です。人口増加による農産物の需要と農業機械の技術進歩が市場成長を促進する主な要因です。

農業用タイヤのアフターマーケットは非常に細分化されており、この分野のOEMに高いリスクをもたらしています。農業機械の設計が変化し、より新しい未知の地形への浸透が進むと、より新しく強力なゴムコンパウンドのタイヤが必要になる可能性があります。フローテーションタイヤ、林業用タイヤ、トレーラー用タイヤ、スチールフレックスウォール付きコンパウンドゴムタイヤが農業用タイヤ市場の動向です。

農業用タイヤ市場の動向

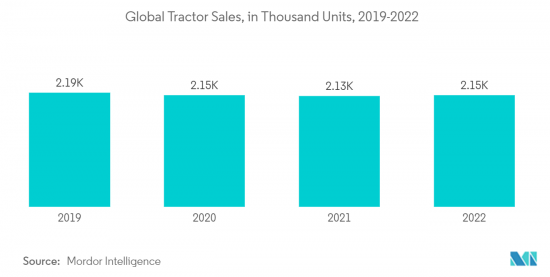

トラクター需要の増加が市場を牽引

農村部から都市部への人口移動、人件費の上昇、ほとんどの新興諸国における熟練労働者の不足がトラクターの販売に拍車をかけています。農業労働力の不足とそのコストの上昇は、農業の機械化が進んでいる主な理由のひとつです。

作業効率に対するニーズの高まりと労働コストの上昇が、農業用トラクターの需要を押し上げると予想されます。予測期間中、農業用トラクター市場は限られた労働力の利用可能性によって牽引されると思われます。

単純な需給経済学と都市部から農村部への労働力の移動を考慮すると、農業労働のコストは、その国の全人口のうち農業に従事する人の割合に直結します。したがって、人手への依存を減らすため、農場主は農業機械に投資し、農業にかかる時間と労力を減らしています。

さまざまな政府が、サプライチェーンのギャップを埋め、農業部門の労働力不足に対処するため、地産地消の新戦略を導入しました。小規模農家を支援するため、政府はいくつかの包括的な税制改革を実施しました。例えば

- インド政府は「農業のマクロ経営スキーム」を実施し、35 PTO HPまでのトラクターに25%の補助金を支給しました。同時に、カナダ政府は「カナダ農業ローン法」を導入し、農家が土地やトラクターを購入する際に最高50万米ドルのローンを提供しました。また、建物の修繕にも利用できます。

農家は、より少ない労働力で最適な能力を発揮するため、農機具への投資を増やしています。こうした設備は初期投資がかさむが、農作物の質と量を全体的に向上させるのに役立ちます。現在、多くの農家が農業経営の規模を縮小し、人件費の上昇を補うために農場の一部を貸し出しています。

より多くの農家が労働力への依存を減らしているため、トラクターの売上は今後数年間で健全な成長を遂げることが予想され、それによって予測期間中のトラクター用タイヤの需要が促進されます。

農業収入の減少にもかかわらず米国で需要が増加

所得水準、購買力、インフラ整備などの要因を含む米国経済の全体的な力強さは、農業用タイヤの需要を促進する役割を担っています。堅調な経済は農業分野への投資を支え、機器やタイヤの需要増につながります。2001年の農業総所得は2,499億米ドルであったが、2022年末には6,041億米ドル以上に大幅に増加しました。

同国は広大で高度に発達した農業部門を有し、相当数の農場と大規模な農業経営が行われています。このような大規模農業には、様々な設備や機械をサポートするために相当数の農業用タイヤが必要です。さらに、2022年には米国に200万の農場があり、2007年の220万から減少しています。同様に農地面積も減少を続け、2002年の9億1,500万エーカーから2022年には8億9,300万エーカーに減少します。平均農地面積は、1970年代の440エーカーから2022年には446エーカーへと少し増加します。

農家数の減少にもかかわらず、米国は農業セクターの統合と近代化により、依然としてトップを維持しています。大規模で技術的に進んだ農場は、規模の経済と専門化の恩恵を受け、生産性と効率の向上を可能にしています。これに農業慣行、設備、インフラの進歩が加わり、米国は主要農業生産国としての地位を維持しています。

さらに、米国は農産物の重要な輸出国であり、食品と日用品を国内外の市場に供給しています。このような輸出志向の農業は、効率的な農法と農業機械に依存しており、農業用タイヤの需要をさらに押し上げています。

米国の農産物輸出は過去25年間に着実に成長し、1997年の628億米ドルから2022年には1,960億米ドルになった。乳製品、肉類、果物、野菜などの高価値品目を含む消費者向け製品は、世界の人口増加、所得の上昇、食生活の多様化により、輸出が大きく伸びた。

このような要因が、米国における農業用タイヤの需要を今後数年間牽引していくと思われます。

農業用タイヤ産業の概要

農業用タイヤ市場は適度に集中しています。農業用タイヤ市場の主要企業は、Bridgestone Corporation(Firestone), Titan International Inc.(Goodyear Tires), BKT, Continental Reifen Deutschland GmbH, Michelinなどです。

その他の業界企業には、Carlisle Companies Incorp.、Trelleborg Wheel Systems、McCreary Tire &Rubber Co.などがあります。市場の優位性を維持するため、主要企業は製品のアップグレードとカスタマイズに注力し、全体的な製品ラインを拡大し、農業用タイヤ市場で強力な製品を提供しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 世界人口の増加

- その他

- 市場抑制要因

- 商品価格の変動

- その他

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 販売チャネルタイプ

- OEM

- 交換/アフターマーケット

- アプリケーションタイプ

- トラクター

- コンバインハーベスター

- 散布機

- トレーラー

- ローダー

- その他

- タイヤタイプ

- バイアスタイヤ

- ラジアルタイヤ

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- その他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Bridgestone Corp.

- Continental AG

- Balakrishna Industries Limited

- Titan International Inc.

- Trelleborg AB

- Michelin

- Nokian Tyres PLC

- Pirelli & C SpA(Prometeon Tyre Group)

- Alliance Tire Group

- Apollo Tyres

- Magna Tyres

第7章 市場機会と今後の動向

- タイヤ空気圧モニタリングシステムの統合

- 環境に優しくエネルギー効率の高い農業用タイヤへのダイナミックなシフト

The agricultural tires market is valued at USD 6.57 billion in the current year. It is expected to reach a value of USD 8.88 billion over the next five years, registering a CAGR above 5.13% during the forecast period.

While the overall scenario of the market is positive, the demand is hugely dependent on the economic turmoil that invariably affects the farmers' income and purchase of farm machinery. However, a downturn in farming equipment sales was witnessed in 2020, as the COVID-19 pandemic severely impacted the automotive industries, including the agriculture tires market.

The rise in demand for efficient and productive agricultural machinery end-products, especially among developed nations, drives the agriculture tires market. After China, Germany is the second-largest exporter and manufacturer of agricultural tires. The demand for farm products from expanding populations and technological advancements in agricultural equipment are the primary factors propelling the market growth.

The agriculture tires aftermarket is highly fragmented and poses a high risk to OEMs in this field. Changing agriculture machinery design and increasing penetration into newer unknown terrain may require tires with newer and stronger rubber compounds. Floatation tires, forestry tires, trailer tires, and compound rubber tires with steel flex walls are the trending tires in the agricultural tires market.

Agricultural Tires Market Trends

The Increasing Demand for Tractors is Driving the Market

The migration of people from rural to urban regions, rising labor costs, and skilled labor lack in most developing countries are fueling tractor sales. Shortage of farm labor and its rising cost are among the main reasons for the increasing mechanization of the farming industry.

The increasing need for operational efficiency and the rise in labor costs are expected to boost the demand for agricultural tractors. Over the forecast period, the market for agricultural tractors will be driven by limited labor availability.

Considering simple demand-supply economics and the transfer of labor from urban to rural areas, the cost of farm labor includes a direct link to the percentage of a country's entire population employed in agriculture. Hence, to reduce dependency on human labor, farm owners are investing in farm equipment, thereby reducing the time and effort taken for farming.

Various governments introduced new strategies to produce and consume locally to bridge the supply chain gaps and address the labor shortage in the agriculture sector. To assist smaller players, the governments implemented a few comprehensive tax reforms. For example:

- The Indian government implemented the 'Macro-Management Scheme of Agriculture,' which provides a 25% subsidy on tractors up to 35 PTO HP. At the same time, the Canadian government introduced the 'Canadian Agricultural Loans Act,' which offers farmers a loan of up to USD 500,000 when purchasing land or a tractor. It may also be used to repair buildings.

Farmers are increasingly investing in farm equipment to work at optimum capacity with a smaller workforce. Although these equipment types come with a high initial investment, they help improve overall crop quality and quantity. Many farmers are now scaling down their agricultural operations and leasing out a portion of their farms to offset rising labor costs.

As more farmers are reducing their dependency on labor, it is expected that tractor sales will witness healthy growth in the coming years, thereby driving the demand for tractor tires over the forecast period.

Increasing Demand in the United States Despite Falling Farm Income

The overall strength of the US economy, including factors such as income levels, purchasing power, and infrastructure development, plays a role in driving demand for agricultural tires. A robust economy supports investments in the agricultural sector, leading to increased demand for equipment and tires. In 2001, the gross farm income totaled USD 249.9 billion, which increased significantly by the end of 2022 to over USD 604.1 billion.

The country holds a vast and highly developed agricultural sector, with a significant number of farms and extensive agricultural operations. This large-scale farming requires a substantial number of agricultural tires to support various equipment and machinery. Moreover, in 2022, 2 million farms were in the United States, down from 2.20 million in 2007. In a similar vein, farmland acres continue to decline, falling from 915 million acres in 2002 to 893 million acres in 2022. The average farm size increased a bit from 440 acres in the 1970s to 446 acres in 2022.

Despite the decrease in the number of farms, the United States remains at the top due to the consolidation and modernization of the agricultural sector. Larger, more technologically advanced farms benefit from economies of scale and specialization, allowing for increased productivity and efficiency. It, combined with advancements in agricultural practices, equipment, and infrastructure, helps the United States maintain its position as a leading agricultural producer.

Additionally, the United States is a significant exporter of agricultural products, supplying food and commodities to both domestic and international markets. This export-oriented agriculture relies on efficient farming practices and equipment, further driving the demand for agricultural tires.

US agricultural exports grew steadily in the past 25 years, from USD 62.8 billion in 1997 to USD 196 billion in 2022. Consumer-oriented products, including high-value items like dairy, meats, fruits, and vegetables, experienced significant export growth due to global population growth, rising incomes, and dietary diversification.

Such factors are likely to drive the demand for agriculture tires in the United States over the coming years.

Agricultural Tires Industry Overview

The agricultural tire market is moderately concentrated. The major players in the agricultural tires market are Bridgestone Corporation (Firestone), Titan International Inc. (Goodyear Tires), BKT, Continental Reifen Deutschland GmbH, and Michelin, among others.

Other companies in the industry include Carlisle Companies Incorp., Trelleborg Wheel Systems, and McCreary Tire & Rubber Co. In order to maintain market dominance, the major companies are focusing on product up-gradation and customization to expand the overall product line, with robust offerings in the agricultural tires market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Global Population

- 4.1.2 Others

- 4.2 Market Restraints

- 4.2.1 Fluctuating Commodity Prices

- 4.2.2 Others

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Sales Channel Type

- 5.1.1 OEM

- 5.1.2 Replacement/Aftermarket

- 5.2 Application Type

- 5.2.1 Tractors

- 5.2.2 Combine Harvesters

- 5.2.3 Sprayers

- 5.2.4 Trailers

- 5.2.5 Loaders

- 5.2.6 Other Application Types

- 5.3 Tire Type

- 5.3.1 Bias Tires

- 5.3.2 Radial Tires

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Bridgestone Corp.

- 6.2.2 Continental AG

- 6.2.3 Balakrishna Industries Limited

- 6.2.4 Titan International Inc.

- 6.2.5 Trelleborg AB

- 6.2.6 Michelin

- 6.2.7 Nokian Tyres PLC

- 6.2.8 Pirelli & C SpA (Prometeon Tyre Group)

- 6.2.9 Alliance Tire Group

- 6.2.10 Apollo Tyres

- 6.2.11 Magna Tyres

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Intergration of Tire Pressure Monitoring System

- 7.2 A Dynamic Shift Towards Eco-Friendly and Energy-Efficient Agriculture Tires