|

市場調査レポート

商品コード

1692493

バイオ医薬品発酵-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Biopharmaceutical Fermentation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バイオ医薬品発酵-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

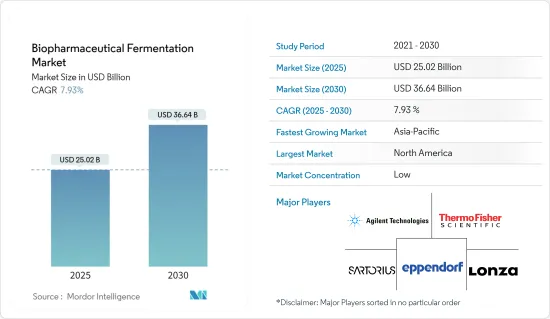

バイオ医薬品発酵市場規模は2025年に250億2,000万米ドルと推定され、予測期間中(2025年~2030年)のCAGRは7.93%で、2030年には366億4,000万米ドルに達すると予測されます。

同市場は、費用対効果の高いバイオシミラーの導入により需要が急増し、バイオテクノロジーに基づく医薬品の普及が進んでいます。発酵は、これらの医薬品の活性物質の生産において極めて重要な役割を果たしています。例えば、MJHライフサイエンス社の2024年1月のレポートでは、がん関連製品の顕著な増加が強調されており、特定のカテゴリーではバイオシミラーの80%のシェアを獲得しています。主要企業は、製品の上市や戦略的イニシアティブを通じて、これらの医薬品の採用をさらに強化しています。その一例として、ベーリンガーインゲルハイムが2023年10月、アッヴィの「ヒュミラ」のノンブランド・バイオシミラーを発売したことが挙げられます。

心血管疾患などの疾病の世界の増加は、バイオテクノロジーに基づく医薬品の需要を押し上げています。2024年1月のブリティッシュ・ハート・ファウンデーションの報告によると、英国では760万人、世界では6億2,000万人が心血管疾患と闘っており、この数字は高齢化とライフスタイルの変化により増加傾向にあります。このようなバイオ医薬品に対する需要の高まりは、市場の成長を促進するものと思われます。

エイコノクラステス・セラピューティクスが2022年11月にフォージ・バイオロジックスと提携したALS標的遺伝子治療薬や、サノフィが2022年8月に提携したJanevent Biologicsのがん治療薬などの企業の取り組みは、業界の勢いを裏付けています。生物製剤開発におけるこれらの提携は、より効果的な治療を実現するために先進的な生物製剤と革新的なドラッグデリバリーシステムを活用するものです。このような進歩は、バイオ医薬品発酵の需要を押し上げ、予測期間中の市場成長を促進すると予想されます。

その結果、がん負担の増加や業界企業による戦略的活動の増加といった要因が市場成長を促進すると予想されます。しかし、バイオ医薬品の発酵と設置に関連する高いコストは、この拡大を抑制する可能性があります。

バイオ医薬品発酵市場の動向

クロマトグラフィー分野は予測期間中に大幅なCAGRで推移する見込み

バイオ医薬品発酵市場では、予測期間中にクロマトグラフィー分野の大幅な成長が予測されます。この成長の原動力は、革新的なバイオ医薬品に対する需要の高まりと新製品の導入です。

クロマトグラフィーは、分子のサイズ、電荷、疎水性、特定のリガンド結合に基づいて分子を分離します。クロマトグラフィーのタイプの選択は、発酵製品の物理的・化学的特性によって決まる。例えば、逆相高速液体クロマトグラフィー(HPLC)は、組換えヒトインスリンの精製や、様々な生物種からの生物学的変異体インスリン分子の分離に採用されています。

新しいクロマトグラフィー装置の導入は、このセグメントの製品ポートフォリオを拡大しています。例えば、2023年11月、3MはHarvest RC Chromatographic Clarifier, BT500でクロマトグラフィークラリファイアーのラインナップを拡充しました。この500mLのシングルユースの清澄化装置は、モノクローナル抗体、組換えタンパク質、生物製剤用に調整されており、5~8%のPCV(充填細胞量)培養からわずか10分で予測収量のサンプルを提供します。

2022年10月、東ソー・バイオサイエンスGmbHは、下流工程の強化のために設計されたOctave BIOマルチカラムクロマトグラフィー(MCC)システムを発表しました。SkillPak BIOプレパックカラムとの組み合わせにより、前臨床プロセス開発を効率化します。Octave BIOは、前臨床から臨床、GMP製造まで、すべての生体分子製造段階をターゲットとしたMCC装置の最初のシリーズのひとつです。

製薬企業とバイオテクノロジー企業との戦略的パートナーシップにより、効率的な下流工程のためのクロマトグラフィーソリューションが強化される予定です。例えば、2024年2月、ピューロライトとレプリジェン・コーポレーションは、二重特異性や組換え抗体断片のような特殊なmAbsの精製用に調整された70μmのアガロースベースのアフィニティー樹脂であるPraesto CH1を発売しました。

このような開発、特に製薬会社とバイオテクノロジー企業間の製品上市や提携を考えると、クロマトグラフィー分野は今後数年で大きく成長する可能性があります。

予測期間中、北米が大きな市場シェアを占める見込み

北米は予測期間中、バイオ医薬品分野で大きな成長を遂げます。この拡大の背景には、バイオ医薬品に対する需要の高まり、研究開発活動の活発化、バイオ医薬品発酵への投資の増加があります。さらに、慢性疾患が流行するにつれて医薬品の消費量が増加し、バイオ医薬品セクターをさらに後押ししています。この動向は、生物製剤やバイオ医薬品の需要を押し上げるだけでなく、バイオ医薬品発酵の重要性を強調しています。

技術的進歩、製品上市、承認、資金調達、提携といった業界各社の戦略的動きは、市場成長を促進すると予想されます。例えば、2024年1月、米国のWuXi Biologics社は、マサチューセッツ州ウースターにある新施設をアップグレードしました。この増強により、同施設の商業用原薬の生産能力は、サービス需要の増大に対応して、2万4,000リットルから3万6,000リットルに引き上げられます。このような能力増強は、バイオ医薬品発酵の利用率を高めることになります。

さらに、北米では関節リウマチ、糖尿病、がんなどの疾病が増加しており、市場を強化しています。これらの疾患は、バイオ医薬品発酵によって生産されるバイオテクノロジーや生物学的薬剤の需要を促進しています。カナダがん協会(CCS)の2023年版レポートは、カナダにおけるがんの負担が増加していることを強調し、新たなバイオ医薬品の機会拡大、ひいては市場成長を示唆しています。

2024年1月、ユーロフィンズCDMOはオンタリオ州に製薬会社向けのパイロット規模の生物製剤開発施設を発表しました。この施設では、上流から下流までの開発、前臨床試験やフェーズ1試験のための供給など、幅広いサービスを提供しています。さらに2023年10月、サーモフィッシャーサイエンティフィックはミズーリ州セントルイスの生物製剤製造能力を増強しました。同社は2023年3月にカリフォルニア州サンフランシスコで細胞治療薬の製造施設を立ち上げ、バイオ医薬品の拠点をさらに拡大しました。

糖尿病やがんなどの疾病負担の増加、バイオ医薬品発酵への需要の高まり、企業活動の活発化を考えると、市場は今後数年で成長する態勢が整っています。

バイオ医薬品発酵産業の概要

数多くの世界的・地域的企業が、バイオ医薬品発酵市場の細分化に寄与しています。競合情勢の主要企業は、国際企業と地元企業の両方を包含しています。大きな市場シェアを持つ注目すべき企業には、Thermo Fisher Scientific Inc.、Danaher Corporation、Sartorius Stedim Biotech、Merck KGaA、Eppendorf AG、F. Hoffmann-La Roche Ltd.、Nova Biomedical Corporation、Lonza Group AG、Agilent Technologies、Becton, Dickinson, and Companyなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- バイオ医薬品に対する需要の増加

- 新規バイオ医薬品を生み出すための研究開発活動の活発化

- 市場抑制要因

- バイオ医薬品の発酵とその設置にかかる高コスト

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- アップストリーム製品

- バイオリアクター/発酵槽

- バイオプロセス分析装置

- プロセスモニタリングシステム

- その他上流製品

- ダウンストリーム製品

- ろ過・分離

- クロマトグラフィー

- 消耗品・アクセサリー

- その他ダウンストリーム製品

- アップストリーム製品

- 用途別

- 抗生物質

- 組み換えタンパク質

- その他の用途

- エンドユーザー別

- バイオ医薬品産業

- 受託研究機関

- 臨床研究機関

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Agilent Technologies

- Thermo Fisher Scientific Inc.

- Lonza Group AG

- Sartorius Stedim Biotech

- Eppendorf AG

- Danaher Corporation

- F. Hoffmann-La Roche Ltd.

- Nova Biomedical Corporation

- Merck KGaA

- Becton, Dickinson and Company

第7章 市場機会と今後の動向

The Biopharmaceutical Fermentation Market size is estimated at USD 25.02 billion in 2025, and is expected to reach USD 36.64 billion by 2030, at a CAGR of 7.93% during the forecast period (2025-2030).

The market has seen a surge in demand due to the introduction of cost-effective biosimilars, enhancing the uptake of biotech-based drugs. Fermentation plays a pivotal role in producing the active substances of these drugs. For instance, a January 2024 report from MJH Life Sciences highlighted a notable increase in cancer-related products, with certain categories capturing an 80% share of biosimilars. Key players, through product launches and strategic initiatives, have further bolstered the adoption of these drugs. A case in point is Boehringer Ingelheim's October 2023 launch of an unbranded biosimilar version of AbbVie's Humira, priced at a striking 81% discount to the original.

The global rise in disease prevalence, such as cardiovascular issues, has driven the demand for biotech-based drugs. A January 2024 British Heart Foundation report noted that 7.6 million individuals in England and 620 million worldwide are grappling with cardiovascular diseases, a figure on the rise due to aging and lifestyle changes. This escalating demand for biotech drugs is poised to propel market growth.

Company initiatives, such as Eikonoklastes Therapeutics' November 2022 partnership with Forge Biologics for ALS-targeting gene therapy and Sanofi's August 2022 alliance with Janevent Biologics for oncology drugs, underscore the industry's momentum. These collaborations in biologics development leverage advanced biologics and innovative drug delivery systems to create more effective treatments. Such advancements are expected to boost demand for biopharmaceutical fermentation, driving market growth during the forecast period.

Consequently, factors like the escalating cancer burden and increased strategic activities by industry players are anticipated to fuel market growth. However, the high costs associated with biopharmaceutical fermentation and installations may temper this expansion.

Biopharmaceutical Fermentation Market Trends

Chromatography Segment Expects to Register a Significant CAGR Over the Forecast Period

Significant growth is projected for the chromatography segment in the biopharmaceutical fermentation market during the forecast period. This growth is driven by rising demand for innovative biopharmaceutical drugs and the introduction of new products.

Chromatography separates molecules based on size, charge, hydrophobicity, and specific ligand binding. The choice of chromatography type depends on the physical and chemical characteristics of the fermentation products. For example, reversed-phase high-performance liquid chromatography (HPLC) is employed to purify recombinant human insulin and separate biological variant insulin molecules from various species.

The introduction of new chromatography devices is expanding the segment's product portfolio. For instance, in November 2023, 3M expanded its chromatographic clarifier lineup with the Harvest RC Chromatographic Clarifier, BT500. This 500-mL, single-use clarifier is tailored for monoclonal antibodies, recombinant proteins, and biologics, delivering predictive yield samples in just 10 minutes from a 5-8% packed cell volume (PCV) culture.

In October 2022, Tosoh Bioscience GmbH unveiled the Octave BIO Multi-Column Chromatography (MCC) system, designed for downstream process intensification. Paired with SkillPak BIO pre-packed columns, it streamlines pre-clinical process development. Octave BIO is the one of the first in a series of MCC instruments targeting all biomolecule manufacturing phases, from pre-clinical to clinical and GMP production.

Strategic partnerships between pharmaceutical and biotechnology firms are set to enhance chromatography solutions for efficient downstream processing. For example, in February 2024, Purolite and Repligen Corporation launched Praesto CH1, a 70μm agarose-based affinity resin, tailored for purifying specialized mAbs like bispecifics and recombinant antibody fragments.

Given these developments, especially product launches and collaborations between pharmaceutical and biotechnology firms, the chromatography segment is poised for substantial growth in the coming years.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America is set for significant growth in the biopharmaceutical sector during the forecast period. This expansion is driven by a rising demand for biotech medications, heightened research and development activities, and increased investments in biopharmaceutical fermentation. Additionally, as chronic diseases become more prevalent, medication consumption rises, further propelling the biopharmaceutical sector. This trend not only boosts the demand for biologics and biotech drugs but also underscores the importance of biopharmaceutical fermentation.

Strategic moves by industry players, such as technological advancements, product launches, approvals, fundraising, and partnerships, are expected to drive market growth. For example, in January 2024, WuXi Biologics in the U.S. upgraded its new facility in Worcester, Massachusetts. This enhancement is set to raise the facility's commercial drug substance capacity from 24,000 liters to 36,000 liters, in response to growing service demand. Such an increase in capacity is poised to amplify the utilization of biopharmaceutical fermentation.

Furthermore, rising disease prevalence in North America, including rheumatoid arthritis, diabetes, and cancer, is bolstering the market. These diseases drive the demand for biotech and biological drugs, produced through biopharmaceutical fermentation. Highlighting this, a 2023 report from the Canadian Cancer Society (CCS) emphasized the escalating cancer burden in Canada, signaling a growing opportunity for new biopharmaceuticals and, consequently, market growth.

In January 2024, Eurofins CDMO unveiled its pilot-scale biologic drug development facility in Ontario, tailored for pharmaceutical companies. This facility offers range of services, such as upstream and downstream development, supplies for preclinical or Phase 1 trials. Additionally, in October 2023, Thermo Fisher Scientific boosted its manufacturing capacity in St. Louis, Missouri, for biologics production. The company further expanded its biopharmaceutical footprint by launching a cell therapy manufacturing facility in San Francisco, California, in March 2023.

Given the rising burdens of diseases like diabetes and cancer, the growing demand for biopharmaceutical fermentation, and heightened corporate activities, the market is poised for growth in the coming years.

Biopharmaceutical Fermentation Industry Overview

Numerous global and regional players contribute to the fragmented nature of the biopharmaceutical fermentation market. Key players in the competitive landscape encompass both international and local firms. Notable companies holding significant market shares include Thermo Fisher Scientific Inc., Danaher Corporation, Sartorius Stedim Biotech, Merck KGaA, Eppendorf AG, F. Hoffmann-La Roche Ltd., Nova Biomedical Corporation, Lonza Group AG, Agilent Technologies, and Becton, Dickinson, and Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Biotech based Drugs

- 4.2.2 Rising Research and Development Activities to Produce Novel Biological Drugs

- 4.3 Market Restraints

- 4.3.1 High Cost of Biopharmaceutical Fermentation and its Installation

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Upstreams Products

- 5.1.1.1 Bioreactors/Fermentors

- 5.1.1.2 Bioprocess Analyzers

- 5.1.1.3 Process Monitoring System

- 5.1.1.4 Other Upstream Products

- 5.1.2 Downstream Products

- 5.1.2.1 Filtration and Seperation

- 5.1.2.2 Chromatography

- 5.1.2.3 Consumables and Acessories

- 5.1.2.4 Other Downstream Products

- 5.1.1 Upstreams Products

- 5.2 By Application

- 5.2.1 Antibiotics

- 5.2.2 Recombinant Proteins

- 5.2.3 Other Applications

- 5.3 By End User

- 5.3.1 Biopharmaceutical Industries

- 5.3.2 Contract Research Organization

- 5.3.3 Acedemic Research Institutes

- 5.3.4 Other End users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Agilent Technologies

- 6.1.2 Thermo Fisher Scientific Inc.

- 6.1.3 Lonza Group AG

- 6.1.4 Sartorius Stedim Biotech

- 6.1.5 Eppendorf AG

- 6.1.6 Danaher Corporation

- 6.1.7 F. Hoffmann-La Roche Ltd.

- 6.1.8 Nova Biomedical Corporation

- 6.1.9 Merck KGaA

- 6.1.10 Becton, Dickinson and Company