|

市場調査レポート

商品コード

1331309

オーガニックベビーフード市場規模・シェア分析-成長動向と予測(2023年~2028年)Organic Baby Food Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オーガニックベビーフード市場規模・シェア分析-成長動向と予測(2023年~2028年) |

|

出版日: 2023年08月08日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

オーガニックベビーフード市場規模は、2023年の45億5,000万米ドルから2028年には81億米ドルに成長し、予測期間(2023~2028年)のCAGRは12.23%と予想されます。

COVID-19の大流行時には、健康危機と食品不安が消費者需要に長期的な影響を与えました。当初は、消費者が食品の安全性を恐れ、個人の健康が製品購入を促進したため、売上が急増しました。中国税関のデータによると、2020年1月から3月までの乳児用粉ミルクの累積輸入量は約430万トンで、2019年に比べて5.4%減少しました。中国では、ママとベビーの店の特殊医療用食品を通じた乳児用食品の販売が増加しており、同地域では高級ベビーフードやオーガニックベビーフードの勢いが生まれ、Feiheの2020年のOrganic Zhizhiを含む高級乳児用調製粉乳シリーズの売上高は16.99%(前年比)増加しました。一方、通常の粉ミルクの売上は25.94%減少しました。

この市場を牽引しているのは、従来の食品生産で使用される有害な化学物質に赤ちゃんがさらされるのを抑えようという消費者の意識の高まりと、オーガニック製品の利点に対する認識です。さらに、世界中で働く女性の人口が増加していることも、調理済みオーガニックベビーフード部門の規模拡大に大きく寄与しており、著しい成長セグメントのひとつとなっています。

市場を牽引しているのは、クリーン・ラベル製品やよりクリーンな食生活を求める動向です。世界中の消費者は、自分自身により新鮮で健康的な食品を求めるようになっており、自分の子供にも同じものを求めるようになっています。

オーガニックベビーフードの市場動向

オーガニックベビーフードへの戦略的投資の急増

オーガニックベビーフードの人気は高まっており、このカテゴリー専用の通路もできています。可処分所得の増加に伴い、親は手作り食品をブランド化されたオーガニックベビーフードで補うことができるようになり、予測期間中、先進国と発展途上国の両方で大きな促進要因となっています。そのため、オーガニックベビーフード分野への投資が増加しています。例えば、2021年にNeptune Wellness Solutions社は植物由来のベビーフード会社Sprout Foods社の50.1%の株式を取得しました。この買収には、600万米ドルの現金支払いと、ネプチューンの普通株式約670万株(1,200万米ドル相当)の発行が含まれていました。同社の年間純収入は2,800万米ドルです。

ベビーフードの新興企業は現在、消化の改善から脳の発達、赤ちゃん主導の離乳食、アレルギー予防まで、特定の健康目標に基づいてブランドを差別化しています。例えば、Advantage Capitalのポートフォリオ会社であるNurturMeは、Grays Peak Capitalに買収されました。NurturMeは、健康的な消化を重視したベビーフードや子供用スナックを提供しています。

オーガニック食品(乳幼児用食品を含む)の開発・普及に向けた投資が増加した結果、ここ数年、需要が増加しています。オーガニック・トレード・アソシエーションが発表したデータによると、2021年に米国はおよそ575億米ドル相当のオーガニック食品を販売しました。とはいえ、企業は基準に従って製品を生産するために研究開発に投資しており、予測期間中にオーガニックベビーフード市場の成長を高めると予想されます。

アジア太平洋地域が最大のシェアを占める

中国の一人っ子政策の緩和も、包装済みベビーフードにプラスの影響を与える可能性があります。富裕層の増加の可能性と新生児数の増加は、中国のベビーフード・飲料メーカーに十分な刺激を与え、より質の高いオーガニックベビーフードや飲料を求める消費者の需要に応えるため、包装済みオーガニック食品を開発します。インドやオーストラリアのような他のアジア諸国も、有機乳幼児用食品の需要が大きく伸びると予想されています。そのため、市場が提供する有利な機会を利用しようと、多くの新興企業が名乗りを上げています。2023年2月、ベンガルールに本社を置き、子供向けの栄養価の高いスナック菓子をパッケージ販売するインドの新興企業ティミオスは、乳幼児向けのオーダーメイドのオーガニックおかゆの新商品を発表し、ベビーフード業界に参入しました。生後6ヶ月から8ヶ月の乳幼児の栄養ニーズを念頭に置いて作られたこの新商品は、12種類のバリエーションがあります。

世界・オーガニック・トレードによると、日本のオーガニック包装食品・飲食品の市場規模は約5億9,740万米ドルで、一人当たり所得は4.71米ドルです。この市場規模と、乳児用の調理済み食品の普及率の高まりも、オーガニックベビーフードの市場に影響を与えています。

オーガニックベビーフード業界の概要

オーガニックベビーフード市場では、各社が新たなマーケティング戦略の開拓に注力し、付加価値の高い原材料をベースにした新製品を投入して競争を繰り広げています。オーガニックベビーフードを生産している主な企業には、ネスレSA、ヘイン・セレスティアル・グループ、ヒーロー・グループ、サンメイド・グロワーズ・オブ・カリフォルニア、ダノンSAなどがあります。プライベートブランドも幅広く、特に先進国市場ではスーパーマーケット/ハイパーマーケット・チェーン、新興経済諸国では伝統的な食料品店/コンビニエンスストア/専門小売店/健康食品店があります。アジア太平洋地域からの需要の増加は、多くのプライベートブランド企業がこの地域に参入していることから、今後数年間で市場力学に変化をもたらすと予想されます。そのため、調査対象市場は細分化されています。同市場のプレーヤーは、製品革新、合併、買収などの戦略を駆使して、調査対象市場で成功を収めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の成果 と前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 調製ミルク

- 調製ベビーフード

- 乾燥ベビーフード

- 流通チャネル

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- オンライン小売店

- その他の流通チャネル

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 主要企業の戦略

- 市況分析

- 企業プロファイル

- Abbott Laboratories

- Nestle SA

- Hero Group

- Danone SA

- Amara Organics

- Sun-Maid Growers of California

- North Castle Partners LLC

- Groupe Lactalis

- Hipp Gmbh & Co.

- The Hein Celestial Group Inc.

- Neptune Wellness Solutions(Sprout Organic Baby Food)

第7章 市場機会と今後の動向

The Organic Baby Food Market size is expected to grow from USD 4.55 billion in 2023 to USD 8.10 billion by 2028, at a CAGR of 12.23% during the forecast period (2023-2028).

Health crises and food scare had a long-term impact on consumer demand during the COVID-19 pandemic. Initially, there was a sales spike, as consumers feared food safety, and personal health drove product purchases. The cumulative import of infant milk powder from January-March 2020 was around 4,30,000 metric ton, which declined by 5.4% compared to 2019, as stated by China custom's data. The increasing sale of infant food products in China via mum-and-baby-store's food for special medical purposes created momentum for premium and organic baby food in the region, with Feihe's sales growth of high-end infant formula series, including Organic Zhizhi, by 16.99% (Y-o-Y) in 2020. In contrast, its regular counterpart sales declined by 25.94%.

The market is driven by the growing awareness among consumers to limit the baby's exposure to the harmful chemicals used in conventional food production and the awareness of the benefits of organic products. Additionally, the rise in the population of working women worldwide largely contributed to the increased size of the prepared organic baby food sector, making it one of the significant growing segments.

The market is driven by the trend toward clean-label products and cleaner diets. Consumers worldwide are increasingly reaching for fresher and healthier food options for themselves, and they are also demanding the same for their children.

Organic Baby Food Market Trends

Escalating Strategic Investments in Organic Baby Food

The popularity of organic baby food is growing, with dedicated aisles for the category. With the increased disposable income, parents can compensate for homemade food with branded organic baby food, posing a great driving factor in both developed and developing countries during the forecast period. Thus, there are increasing investments in the organic baby food sector. For instance, in 2021, Neptune Wellness Solutions acquired a 50.1% share in Sprout Foods plant-based baby food company. The deal included a USD 6 million cash payment and the issuance of approximately 6.7 million in Neptune common shares, valued at USD 12 million. The company registered annual net revenues of USD 28 million.

Baby food start-ups are now differentiating their brands based on specific health goals, from better digestion to brain development, baby-led weaning, and allergy prevention. For example, NurturMe, a portfolio company of Advantage Capital, was acquired by Grays Peak Capital. NurturMe provides baby food and children's snacks that emphasize healthy digestion.

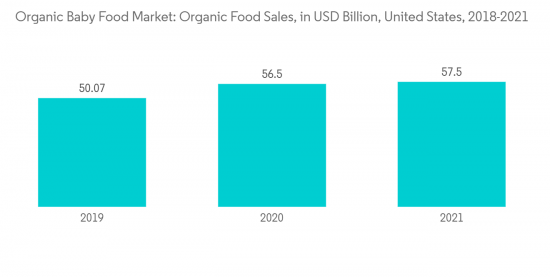

As a result of rising investments in developing and promoting organic food and beverages (including infant food), sales have witnessed a rise in demand over the past few years. As per data published by the Organic Trade Association, in 2021, the United States sold roughly USD 57.5 billion worth of organic food. Nevertheless, companies are investing in R&D to produce products by the standards, which are anticipated to enhance the growth of the organic baby food market during the forecast period.

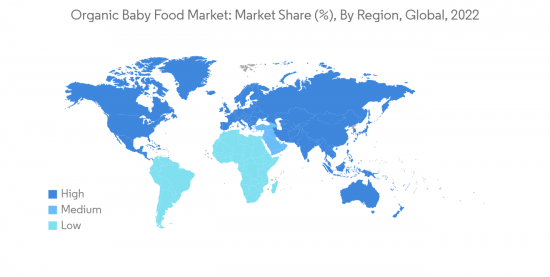

Asia-Pacific Holds the Largest Share

The relaxation of China's one-child policy may also positively impact pre-packaged baby foods. The potential of increasing wealth and the rising number of newborns give China's baby food and drink manufacturers adequate stimulus to develop packaged organic food products to cater to the consumer demand for better quality organic baby food and drink. Other Asian countries like India and Australia are anticipated to exhibit strong growth in demand for organic infant food products. Thus, many start-ups have come forward to take advantage of the lucrative opportunities offered by the market. In February 2023, Timios, an Indian start-up with headquarters in Bengaluru that sells packaged nutritious snacks for kids, entered the baby food industry by introducing its new made-to-order organic porridge variety for infants and toddlers. The new line, which came in 12 variations, was created with the nutritional needs of infants between the ages of 6 and 8 months in mind.

As per the Global Organic Trade, the market for organic packaged food and beverage in Japan was worth around USD 597.4 million, with a per capita income of USD 4.71. This market size and the increasing prevalence of pre-cooked foods for babies also impacted the market for organic baby food.

Organic Baby Food Industry Overview

In the organic baby food market, companies are focused on developing new marketing strategies and introducing new products based on value-added ingredients to compete in the market. Some major organic baby food-producing companies are Nestle SA, The Hain Celestial Group Inc., Hero Group, Sun-Maid Growers of California, and Danone SA. There is a wide range of private-label brands, particularly the supermarket/hypermarket chains in developed markets and traditional grocery stores/convenience stores/specialty retail stores/health stores in developing economies. The growing demand from the Asia-Pacific region is expected to change the market dynamics in the coming years, as many private-label players are entering the region. Hence, the market studied is fragmented in nature. The players in the market have been using strategies like product innovations, mergers, and acquisitions to thrive in the market studied.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Milk Formula

- 5.1.2 Prepared Baby Food

- 5.1.3 Dried Baby Food

- 5.2 Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Online Retail Stores

- 5.2.4 Other Distribution Channels

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Italy

- 5.3.2.6 Spain

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategies Adopted by Leading Players

- 6.2 Market Position Analysis

- 6.3 Company Profiles

- 6.3.1 Abbott Laboratories

- 6.3.2 Nestle SA

- 6.3.3 Hero Group

- 6.3.4 Danone SA

- 6.3.5 Amara Organics

- 6.3.6 Sun-Maid Growers of California

- 6.3.7 North Castle Partners LLC

- 6.3.8 Groupe Lactalis

- 6.3.9 Hipp Gmbh & Co.

- 6.3.10 The Hein Celestial Group Inc.

- 6.3.11 Neptune Wellness Solutions (Sprout Organic Baby Food)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS