|

市場調査レポート

商品コード

1273432

石膏ボード市場- 成長、動向、および予測(2023年-2028年)Plasterboard Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 石膏ボード市場- 成長、動向、および予測(2023年-2028年) |

|

出版日: 2023年04月14日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

予測期間中、世界の石膏ボード市場は5%以上のCAGRで成長すると予想されます。

COVID-19の発生は、建設業界の成長鈍化により、2020年の石膏ボード市場の成長に影響を与えました。社会の比較的多くの人々の所得が影響を受けたため、お金の流動性に悪影響を及ぼし、それが建設業界の業績に悪影響を及ぼしました。また、原材料や労働者の入手に関する問題も、2020年の建設を減速させた最大の要因のひとつです。しかし、パンデミック後の建築プロジェクトの増加により、石膏ボードを求める人が増えました。

主なハイライト

- 石膏ボード業界の成長の大部分は、住宅建設の増加と耐火性の高い建材の必要性に起因しています。

- 住宅のエンドユーザーの認識不足と、廃石膏ボードを処分する場所の不足が、市場の成長を鈍らせると思われます。

- 今後は、新しい軽量石膏ボードが市場成長のきっかけになると予想されます。

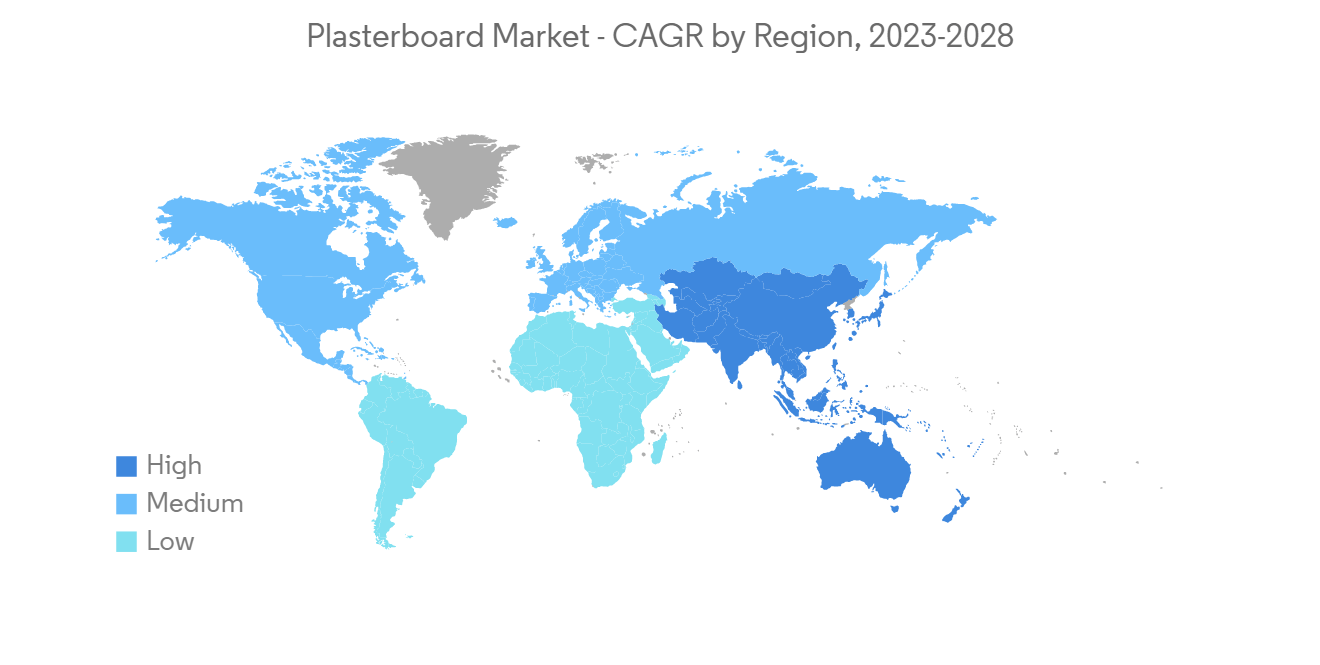

- アジア太平洋が石膏ボードの最大市場であったのは、中国、インド、インドネシアといった新興国の建築産業が急速に成長していたためです。

石膏ボードの市場動向

住宅建設による需要の増加

- 中間層の人数が増え、彼らの可処分所得も上がっています。そのため、中間層の住宅市場が拡大し、今後数年間は石膏ボードの使用量が増加すると考えられています。

- 需要が増えたとはいえ、世界ではまだ住宅が大きく不足しています。このため、投資家やデベロッパーは、さまざまな建築方法を使い、開発を進めるために新しいパートナーシップを結ぶ大きなチャンスに恵まれています。

- アジア太平洋地域が最も成長すると予想されるのは、中国とインドの住宅建設市場が拡大しているためです。中国、インド、東南アジア諸国は、アジア太平洋地域で最大のローコスト住宅建設セグメントを担当しています。

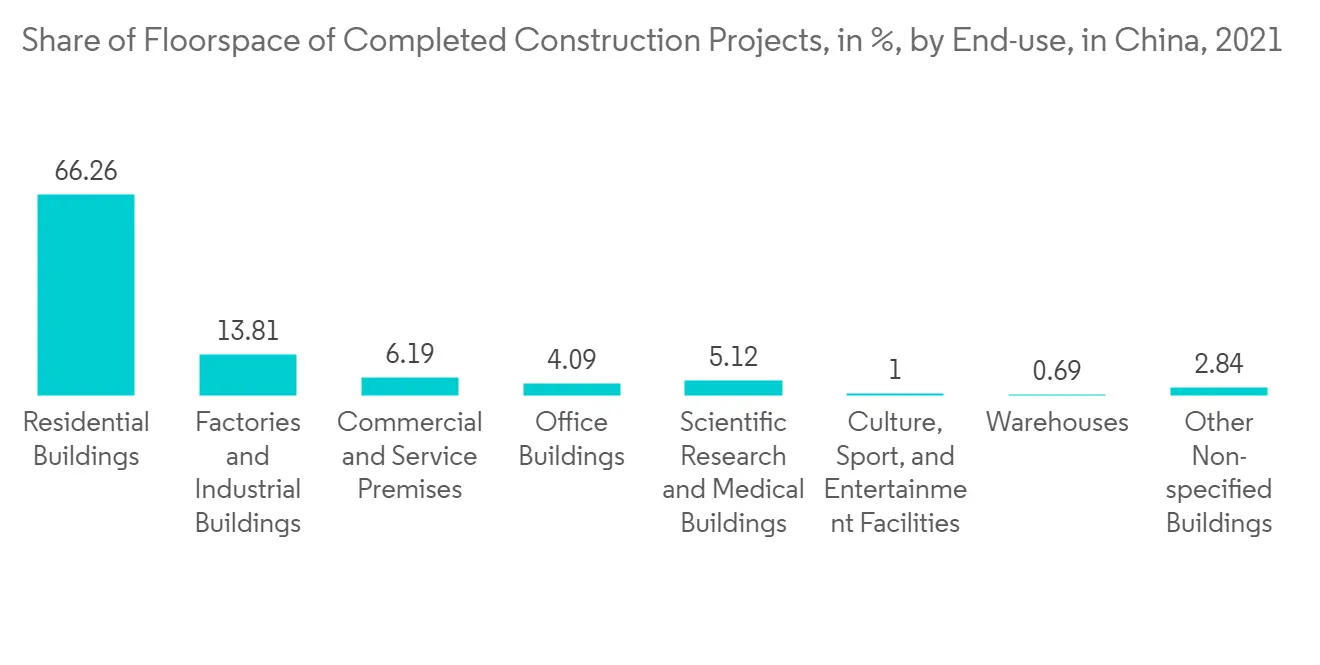

- 2021年、中国における住宅用不動産新築の床面積は約1兆4,600億平方メートルに達するでしょう。2021年に中国で完成した建設物のうち、住宅が最大のシェアを占めています。完成した床面積のほぼ67%が、住宅用に指定された建物に属しています。

- さらに米国では、建設を終えた民間の一戸建て住宅は、2020年1月の94万2,000戸に対し、2021年1月には100万戸を超えていました。さらに、建築許可によって許可された民間所有の住宅は、2022年12月に季節調整済み年率で133万戸となりました。これは、11月の改定値である135万戸を1.6%、2021年12月の190万戸を29.9%下回っています。

- インドでは、政府が「2022年までにすべての人に住宅を」というプロジェクトを開始し、予測期間を通じて同国の低価格住宅建設分野を絶大に牽引することが期待されています。

- 中間層の人口増加や住宅建設、政府の取り組みや投資により、予測期間中、すべての地域の住宅セクターにおける石膏ボードの需要は増加すると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域では、中国がGDPで最大の経済大国となっています。同国の成長率は依然として高いが、高齢化が進み、投資から消費、製造からサービス、外需から内需へと経済のリバランスが進んでいるため、成長率は徐々に低下しています。

- 中国の建設業が急速に成長したのは、政府が経済成長を維持するためにインフラへの投資を推し進めたからです。2021年に中国の建設会社が新たに結んだ契約額は約34兆5,000億元(4,800億米ドル)で、全体の半分以上を占めています。

- 不動産市場の成長が予測できないとはいえ、中国政府は成長する産業・サービス業に対応するため、鉄道や道路のインフラ整備に力を入れてきました。ほとんどの建設会社は政府によって所有されているため、政府支出の増加が国内の建設業を助けているのです。

- 中国はますます都市化が進んでおり、2050年までに2億5,500万人以上の人々が都市で暮らすようになると予想されています。政府は、移住者の社会的住居の確保や大都市での都市施設の拡張を支援するために開始しました。また政府は、都市の「シャントタウン」の修復に1,620億米ドル以上を支出すると発表しています。

- インドは今後数年間で、住宅に約1兆3,000億米ドルの投資を行い、その間に6,000万戸の新しい住宅が建設される見込みです。2024年までに、インドの手頃な価格の住宅数は約70%増加すると予想されています。2022年6月、タウンシップ、住宅、建設インフラ、インフラ開発プロジェクトの建設・開発におけるFDIは286億4,000万米ドルに達しました。

- 全体として、今回調べた市場は高い成長率が見込まれています。これは、この国や地域の建設産業が急速に成長しているためです。

石膏ボードの業界概要

世界の石膏ボード市場には、少数のビッグプレーヤーしか存在しないです。上位5社が市場の大きな部分を占めています。石膏ボード市場の主要企業には、Etex Group、National Gypsum Services Company、Saint-Gobain、Georgia-Pacific、AWI Licensing LLCなどがあります(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 本調査の対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 湿式工法に対する乾式工法の強い需要

- 住宅建設における需要の増加

- 耐火性建材の需要増加

- 抑制要因

- 認知度の低さ

- 石膏ボード廃棄物処理場の不足

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

第5章 市場セグメンテーション

- 形状

- スクエアエッジ

- テーパード

- タイプ

- 防湿石膏ボード

- 耐火石膏ボード

- 耐衝撃石膏ボード

- 断熱石膏ボード

- 耐湿石膏ボード

- 防音石膏ボード

- 標準石膏ボード

- 熱伝導石膏ボード

- 最終用途分野

- 住宅用

- 非住宅用

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- 北欧諸国

- その他欧州諸国

- 南米

- ブラジル

- アルゼンチン

- その他南米諸国

- 中東およびアフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋地域

第6章 競合情勢

- M&A、ジョイントベンチャー、コラボレーション、契約など

- 市場シェア(%)/ランキング分析

- 主要企業が採用した戦略

- 企業プロファイル

- AWI Licensing LLC

- Ahmed Yousuf & Hassan Abdullah Co.(AYHACO GROUP)

- ATISKAN STRUCTURE AND INDUSTRIAL GYPSUM PRODUCTS INDUSTRY. VE TIC. Inc.

- Etex Group

- Fletcher Building

- Georgia-Pacific

- Gyprock

- Gypsemna

- Gyptec Iberica

- Jason Plasterboard Co. Ltd.

- LafargeHolcim

- Mada Gypsum

- National Gypsum Services Company

- ECPlaza Network Inc.

- Saint-Gobain

- USG Boral

- CERTAINTEED

- JN Linrose

- American Gypsum

第7章 市場機会および今後の動向

- 軽量石膏ボードの新たな展開

- その他のビジネスチャンス

During the time frame of the forecast, the global plasterboard market is expected to grow at a CAGR of more than 5%.

The outbreak of COVID-19 impacted plasterboard market growth in 2020 due to slowed construction industry growth. Because the income of a relatively large part of society was affected, it had a negative effect on the liquidity of money, which in turn had a negative effect on the performance of the construction sector. Also, problems with getting raw materials and workers were some of the biggest things that slowed down construction in 2020.But the increase in building projects after the pandemic has made more people want plasterboard.

Key Highlights

- Most of the growth in the plasterboard industry can be attributed to the rise in residential construction and the need for more fire-resistant building materials.

- Lack of awareness among residential end-users and a lack of places to get rid of waste plasterboard are likely to slow the growth of the market.

- In the future, it is expected that new lightweight plasterboards will give the market a chance to grow.

- Asia-Pacific was the biggest market for plasterboard because the building industry in developing countries like China, India, and Indonesia was growing so quickly.

Plasterboard Market Trends

Increasing Demand from Residential Construction

- The number of people in the middle class is growing, and their disposable income is also going up. This has helped the middle-class housing market grow, which will increase the use of plasterboard over the next few years.

- Even though there is more demand, there is still a big shortage of housing around the world.This gives investors and developers a big chance to use different ways of building and make new partnerships to move development forward.

- The Asia-Pacific region is expected to have the most growth because the housing construction market in China and India is growing. China, India, and Southeast Asian nations are in charge of the largest low-cost housing construction segment in Asia-Pacific.

- In 2021, the floor space of new residential real estate construction will amount to around 1.46 trillion square meters in China. Residential buildings accounted for the largest share of completed construction in China in 2021. Almost 67 percent of the completed floor space belonged to buildings designated for housing.

- Furthermore, in the United States, privately owned single-family housing that had finished construction had more than 1 million units in January 2021, as compared to 942 thousand units in January 2020. Moreover, privately owned housing units authorized by building permits were at a seasonally adjusted annual rate of 1.33 million units in December 2022. This is 1.6 percent below the revised November rate of 1.35 million units and 29.9 percent below the December 2021 rate of 1.9 million units.

- In India, the government initiated a project called "Housing for All by 2022," which is expected to immensely drive the low-cost residential construction segment in the country throughout the forecast period.

- Due to the increasing middle-class population and residential building construction, coupled with government initiatives and investments, the demand for plasterboard in the residential sector across all regions is expected to increase during the forecast period.

The Asia-Pacific Region to Dominate the Market

- In Asia-Pacific, China is the largest economy in terms of GDP. The growth rate in the country remains high, but it is gradually diminishing as the population is aging and the economy is rebalancing from investment to consumption, manufacturing to services, and external to internal demand.

- China's construction industry grew quickly because the government pushed for investments in infrastructure to keep the economy growing. The value of new contracts signed by Chinese construction companies in 2021 was approximately CNY 34.5 trillion (USD 0.48 trillion), which is more than half of the total.

- Even though the growth of the real estate market is unpredictable, the Chinese government has put a lot of effort into building rail and road infrastructure to keep up with the growing industrial and service sectors. This has led to a lot of growth in the Chinese construction industry in recent years.Since most construction companies are owned by the government, the increase in government spending is helping the construction business in the country.

- China is becoming more and more urban, and by 2050, 255 million more people are expected to live in cities. started by the government to help migrants find social housing and to expand urban facilities in big cities.The government has also said it will spend more than USD 162 billion to fix up "shantytowns" in cities.

- India is likely to witness an investment of around USD 1.3 trillion in housing over the next few years, during which the country is likely to witness the construction of 60 million new homes. By 2024, the number of affordable homes in India is expected to have grown by about 70%.In June 2022, FDI in the construction and development of townships, housing, built-up infrastructure, and infrastructure development projects stood at USD 28.64 billion.

- Overall, the market that was looked at is expected to grow at high rates. This is because the construction industry in the country and region is growing quickly.

Plasterboard Industry Overview

There are only a few big players in the global plasterboard market. The top five players make up a big chunk of the market. Key players in the plasterboard market include Etex Group, National Gypsum Services Company, Saint-Gobain, Georgia-Pacific, and AWI Licensing LLC, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Strong Demand for Dry Construction Methods over Wet Methods

- 4.1.2 Increasing Demand from Residential Construction

- 4.1.3 Rising Demand for Fire-resistant Construction Materials

- 4.2 Restraints

- 4.2.1 Lack of Awareness

- 4.2.2 Lack of Availability of Plasterboard Waste Disposal Plants

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Form

- 5.1.1 Square-edge

- 5.1.2 Tapered

- 5.2 Type

- 5.2.1 Damp-roof Plasterboard

- 5.2.2 Fire-resistant Plasterboard

- 5.2.3 Impact-resistant Plasterboard

- 5.2.4 Insulated Plasterboard

- 5.2.5 Moisture-resistant Plasterboard

- 5.2.6 Sound-resistant Plasterboard

- 5.2.7 Standard Plasterboard

- 5.2.8 Thermal Plasterboard

- 5.3 End-use Sector

- 5.3.1 Residential

- 5.3.2 Non-residential

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 NORDIC Countries

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AWI Licensing LLC

- 6.4.2 Ahmed Yousuf & Hassan Abdullah Co. (AYHACO GROUP)

- 6.4.3 ATISKAN STRUCTURE AND INDUSTRIAL GYPSUM PRODUCTS INDUSTRY. VE TIC. Inc.

- 6.4.4 Etex Group

- 6.4.5 Fletcher Building

- 6.4.6 Georgia-Pacific

- 6.4.7 Gyprock

- 6.4.8 Gypsemna

- 6.4.9 Gyptec Iberica

- 6.4.10 Jason Plasterboard Co. Ltd.

- 6.4.11 LafargeHolcim

- 6.4.12 Mada Gypsum

- 6.4.13 National Gypsum Services Company

- 6.4.14 ECPlaza Network Inc.

- 6.4.15 Saint-Gobain

- 6.4.16 USG Boral

- 6.4.17 CERTAINTEED

- 6.4.18 JN Linrose

- 6.4.19 American Gypsum

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Lightweight Plasterboards

- 7.2 Other Opportunities