|

市場調査レポート

商品コード

1258779

非経口栄養市場- 成長、動向、予測(2023年-2028年)Parenteral Nutrition Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 非経口栄養市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年04月14日

発行: Mordor Intelligence

ページ情報: 英文 116 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

予測期間中、非経口栄養市場はCAGR 7.7%で成長すると予想されています。

COVID-19のパンデミックは、非経口栄養市場にプラスの影響を与えました。非経口栄養は、世界中の患者のCOVID-19感染関連栄養失調の治療に大きな役割を果たします。2020年、欧州臨床栄養代謝学会は、SARS-CoV-2感染者の栄養管理に関連するガイドラインを制定しました。このガイドラインでは、COVID-19に感染した人の免疫力を高めるための栄養補給が急務であるとされ、欧州各国での非経口栄養の需要が高まっています。COVID-19に感染すると、食欲不振などの症状がひどくなり、筋肉量の低下や免疫防御力の低下が進みます。それゆえ、診療所や病院では、診療時点における栄養補給に一層力を入れるようになっていました。このような新興国市場の開拓により、静脈栄養投与に対する患者の需要が高まり、導入が進みました。したがって、COVID-19パンデミックは、市場の成長に大きな影響を与えました。

市場成長を牽引している主なものは、早期出産の増加、慢性疾患の増加、低・中所得国における栄養失調の増加です。

栄養失調とは、ミネラルやビタミンが十分に摂取できていないこと、栄養不足であること、過体重や肥満であること、食生活の乱れによって引き起こされる非伝染性疾患であることを指します。2022年7月に発表されたユニセフのデータでは、栄養不足の有病率は2019年から2020年にかけて8.0%から9.3%に急上昇し、2021年は9.8%と緩やかなペースで上昇しました。さらに、5歳未満の子どものうち3,900万人が太りすぎ、1億4,900万人が食事に栄養豊富な食品が慢性的に不足している結果、成長と発達が阻害されており、4,500万人が消耗症に苦しんでいます。したがって、体重不足の子どもの負担は大きく、今後数年間は臨床栄養の需要を促進し、市場の成長を後押しすると考えられます。

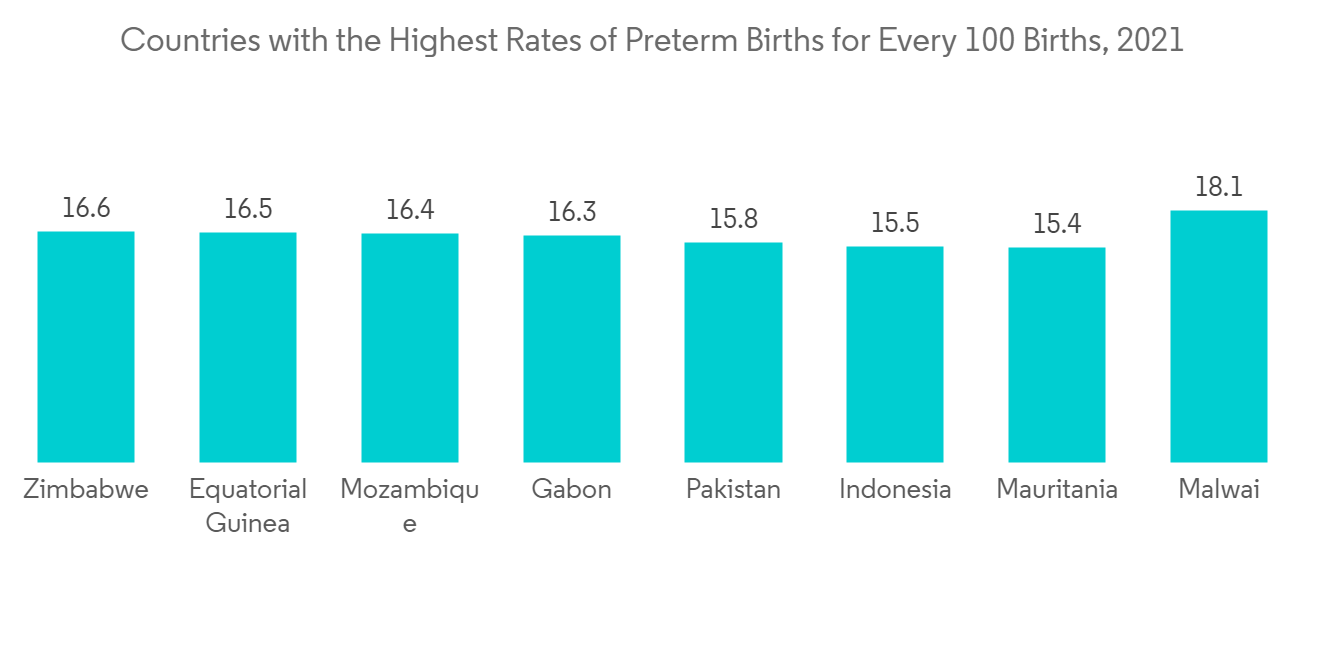

さらに、早産率の高さが市場成長に寄与しています。2021年のWHOの更新によると、早産率は2021年に184カ国で生まれた赤ちゃんの5%から18%に及んでいます。同年の早産の60%以上はアフリカと南アジアで発生しており、世界の問題になっています。同資料では、低所得国では平均12%の赤ちゃんが早産であるのに対し、高所得国では9%であるとしています。2021年に早産が多い10カ国は、インド(9,519,100人)、中国(1,172,300人)、ナイジェリア(773,600人)、パキスタン(748,100人)、インドネシア(675,700人)、米国(517,400人)、バングラデシュ(424,100人)、フィリピン(344,900人)、コンゴ民主共和国(344,400人)、ブラジル(279,300人)。したがって、各国で早産が多いことから、非経口栄養の需要が高まると予想されます。

しかし、一部の新興諸国では、人々が非経口栄養についてあまり知らないため、市場の成長が鈍化しています。

非経口栄養の市場動向

非経口栄養市場では病院セグメントが主要な市場シェアを占めると予想される

非経口栄養の多くは病院で投与されており、これが病院の主要なシェアを占める要因となっています。

同市場で事業を展開する主要企業は、病院に恩恵をもたらす革新的な製品を発表しています。例えば、2021年7月、輸液療法に特化した医療機器企業であるMicrel Medicalと臨床栄養の世界的リーダーであるBaxter Healthcareは、非経口栄養(PN)用輸液ポンプMicrel Mini RythmicPN+のオーストラリアとニュージーランド全域での販売に関する協定を締結しました。このような動きは、非経口栄養の需要を押し上げ、セグメントの成長を促進すると予想されます。

そのほか、2021年3月に発表されたMedical Nutrition International Industry(MNI)のデータによると、ベルギーではCOVID-19で入院した患者の最大50%が栄養失調であり、病院全体で非経口栄養の需要を急増させました。

入院患者の栄養失調の有病率は一般的に高く、特に高齢者では顕著です。2022年2月に発表されたPubMedの論文によると、病院に入院している老人患者の55%以上が栄養失調であったといいます。重病の成人患者6,518人を対象とした観察研究では、外科集中治療室で治療を受けた患者の生存率が栄養失調と関連していることが示されました。栄養不良は、重症患者の28日間死亡リスクの上昇と関連しています。したがって、栄養不良の有病率が高いことから、このセグメントは今後数年間で健全な成長を遂げると予想されます。

また、病院にはより良い治療の選択肢があり、長期的な病気の人に完全な非経口的ケアを行うための設備が整っていることから、患者はより頻繁に病院に行きたいと思うようになると考えられます。例えば、2022年6月に発表されたPubMedのデータによると、病院では慢性腸閉塞の人に完全非経口栄養を投与しています。非経口栄養は、病院における栄養の重要な要素の1つです。したがって、このセグメントは今後数年間で力強い成長が見込まれています。

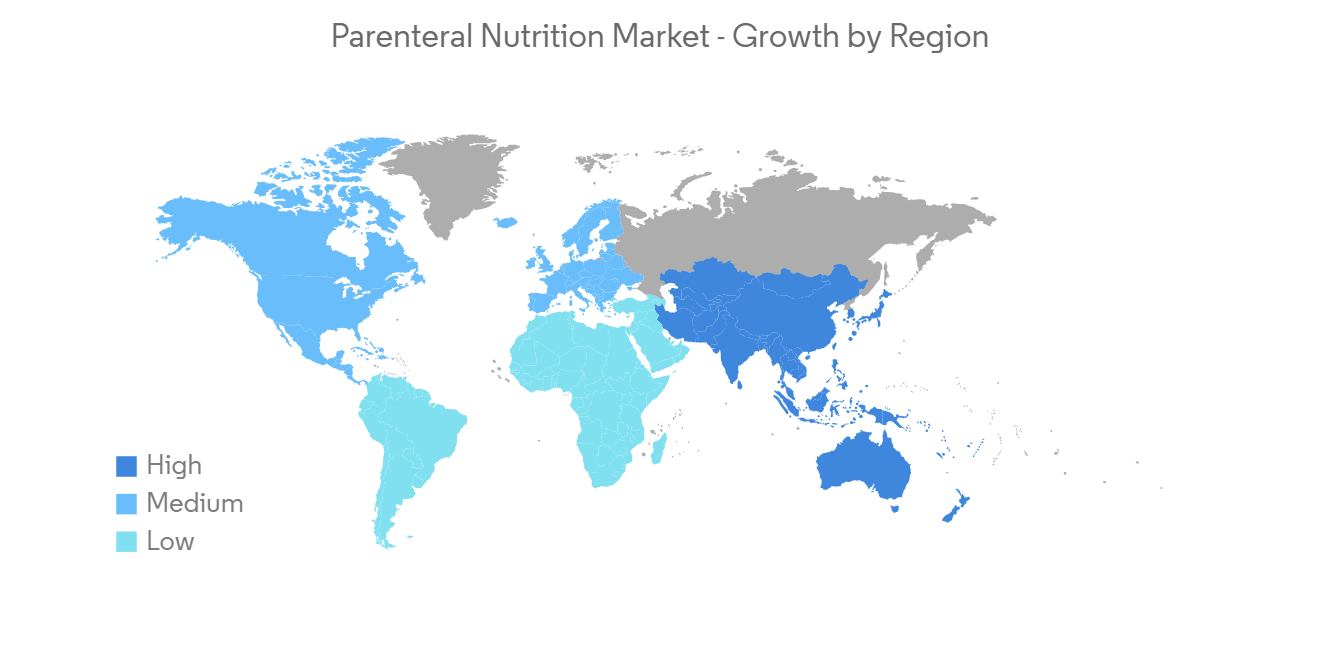

予測期間中、北米が市場の重要なシェアを占めると予想される

北米のシェアが大きく、今後数年間は米国がこの領域を支配するとの見方が大勢を占めています。

米国では多くの入院患者が非経口栄養を投与されています。例えば、2021年のメディケアのデータでは、米国では全体で毎年約34,000人の患者さんが重篤な病気で非経口栄養(PN)を受けています。同国では非経口栄養を受ける人の数が多いため、研究対象となる市場は今後大きな成長を遂げると予想されます。

さらに、米国非経口・経腸栄養学会(ASPEN)が提供するデータによると、2021年1月時点で、マルチビタミン輸液(成人・小児)、アミノ酸、酢酸カリウム注射(USP)、酢酸ナトリウム注射(USP)、塩化ナトリウムなど特定の非経口製品の注射が23.4%不足していました。この不足は、非経口製剤の需要が高いことが主な原因となっています。

2022年5月に更新された米国国立心肺血液研究所のメタボリックシンドロームに関する論文によると、米国ではメタボリックシンドロームが非常に多く、米国成人の約3人に1人がメタボリックシンドロームの一種を患っているといいます。メタボリックシンドロームの増加に伴い、非経口栄養の需要が高まっており、市場の成長を後押しすることが期待されています。

以上のような要因から、北米では予測期間中に市場が大きく成長すると予想されます。

非経口栄養の産業概要

非経口栄養の競争は中程度であり、複数の大手企業で構成されています。市場シェアの面では、現在いくつかの大手企業が市場を独占しており、現在市場を独占している企業には、Fresenius Kabi AG、B.Braun Melsungen AG、Baxter、ICU Medical、Abbottです。

その他の特典です:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件条件と市場の定義

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 未熟児出産の割合が増加

- 慢性疾患の負担増加

- 栄養失調の割合増加

- 市場抑制要因

- 新興国における認識の甘さ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 栄養タイプ別

- 炭水化物

- 非経口的脂質エマルジョン

- アミノ酸単回投与液

- 微量元素

- その他の栄養タイプ

- 患者タイプ別

- 新生児

- 子供

- 成人

- エンドユーザー別

- 病院

- クリニック

- ホームケア

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ地域

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 北米

第6章 競合情勢について

- 企業プロファイル

- Fresenius Kabi AG

- B. Braun Melsungen AG

- Baxter International

- ICU Medical

- Option Care Health Inc.

- Abbott

- Kelun

- Otsuka Pharmaceutical India Pvt. Ltd.

- Amanta Healthcare

- Aculife

第7章 市場機会と今後の動向

During the time frame of the forecast, the parenteral nutrition market is expected to grow at a CAGR of 7.7%.

The COVID-19 pandemic positively impacted the parenteral nutrition market. Parenteral nutrition plays a major role in treating COVID-19 infection-related malnutrition in patients across the globe. In 2020, the European Society for Clinical Nutrition and Metabolism established a guideline relating to the nutritional management of people infected with the SARS-CoV-2 infection. These guidelines stated that there is an urgent need for nutrition for people suffering from COVID-19 to increase their immunity, which boosted the demand for parenteral nutrition in European countries. The COVID-19 infection resulted in a severe lack of appetite, as well as other symptoms, which led to an increase in loss of muscle mass and deterioration of immune defenses. Hence, clinics and hospitals were focusing more on the provision of nutrition at the point of care. Such developments increased patient demand for and adoption of intravenous nutrition administration.Hence, the COVID-19 pandemic had a significant impact on market growth.

The main things that are driving market growth are the rise in early births, the rise in chronic diseases, and the rise in malnutrition in low- to middle-income countries.

Malnutrition includes not getting enough minerals or vitamins, being undernourished, being overweight or obese, and having a non-communicable disease that is caused by a bad diet. As per the UNICEF data published in July 2022, the prevalence of undernourishment jumped from 8.0% to 9.3% from 2019 to 2020 and rose at a slower pace in 2021 to 9.8%. Additionally, 39 million children under the age of five are overweight, 149 million have stunted growth and development as a result of a chronic lack of nutrient-rich food in their diets, and 45 million suffer from wasting.Hence, the huge burden of underweight children is likely to propel the demand for clinical nutrition and boost market growth in the coming years.

Furthermore, the high rate of premature births contributes to market growth. As per the WHO update of 2021, the rate of preterm birth ranged from 5% to 18% of babies born across 184 countries in 2021. More than 60% of preterm births occurred in Africa and South Asia in the same year and are becoming a global problem. The same source stated that in low-income countries, on average, 12% of babies are born too early, compared to 9% in high-income countries. The 10 countries with the greatest number of preterm births in 2021 include India (9,519,100), China (1,172,300), Nigeria (773,600), Pakistan (748,100), Indonesia (675,700), the United States of America (517,400), Bangladesh (424,100), the Philippines (348,900), the Democratic Republic of the Congo (341,400), and Brazil (279,300). Hence, with the high number of preterm births in various countries, the demand for parenteral nutrition is expected to rise.

But in some developing countries, people don't know much about parenteral nutrition, which slows the growth of the market.

Parenteral Nutrition Market Trends

The Hospital Segment is Expected to Hold a Major Market Share in the Parenteral Nutrition Market

Most of the parenteral nutrition is given in hospitals, which is the major factor responsible for a major share of hospitals.

Key companies operating in the market are coming up with innovative products that are benefiting hospitals. For instance, in July 2021, Micrel Medical, a medical device company specializing in infusion therapy, and Baxter Healthcare, a global leader in clinical nutrition, signed an agreement for the distribution of the Micrel Mini RythmicPN+ infusion pump for parenteral nutrition (PN) across Australia and New Zealand. Such developments are expected to boost demand for parental nutrition, driving segment growth.

Besides, as per the Medical Nutrition International Industry (MNI) data published in March 2021, up to 50% of the patients hospitalized with COVID-19 were malnourished in Belgium, which surged the demand for parenteral nutrition across the hospitals.

The prevalence of malnutrition in hospitalized patients is generally high, especially in the elderly. As per the article from PubMed published in February 2022, more than 55% of geriatric patients in hospitals were malnourished. An observational study of 6,518 seriously ill adult patients demonstrated that the survival of patients treated in surgical intensive care units is linked to malnutrition. Malnutrition is associated with an increased risk of 28-day mortality in critically ill patients.Hence, with the high prevalence of malnutrition, the segment is expected to witness healthy growth in the coming years.

Also, the fact that hospitals have better treatment options and facilities to give complete parenteral care to people with long-term illnesses is likely to make patients want to go to hospitals more often. For example, according to data from PubMed that was published in June 2022, hospitals give people with chronic intestinal obstruction total parenteral nutrition. Parenteral nutrition is one of the crucial elements of nutrition in hospitals. Thus, the segment is believed to witness strong growth in the coming years.

North America is Expected to Hold a Significant Share of the Market Over the Forecast Period

North America is expected to have a big share, and most people think that in the coming years, the United States will rule the area.

Many hospitalized patients in the United States receive parenteral nutrition. For instance, as per the Medicare data of 2021, overall, approximately 34,000 patients in the United States receive parenteral nutrition (PN) every year for critical ailments. With the high number of people receiving parenteral nutrition in the country, the market studied is expected to witness significant growth in the future.

Furthermore, as per the data provided by the American Society for Parenteral and Enteral Nutrition (ASPEN), as of January 2021, there was a 23.4% shortage of injections for certain parenteral products, including multi-vitamin infusion (adult and pediatric), amino acids, potassium acetate injection (USP), sodium acetate injection (USP), and sodium chloride. The shortage was largely attributed to the high demand for parenteral products.

According to a National Heart, Lung, and Blood Institute of the National Institute of Health article on metabolic syndrome, updated in May 2022, metabolic syndrome is very common in the United States, and around one in three American adults suffer from a type of metabolic syndrome. With the increasing occurrence of metabolic syndrome, there is a growing demand for parenteral nutrition, which is expected to boost market growth.

Due to the above-mentioned factors, it is expected that the studied market will grow significantly in North America during the forecast period.

Parenteral Nutrition Industry Overview

Parenteral nutrition is moderately competitive and consists of several major players. In terms of market share, a few of the major players are currently dominating the market and some of the companies which are currently dominating the market are Fresenius Kabi AG, B. Braun Melsungen AG, Baxter, ICU Medical, and Abbott.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Rate of Pre-Mature Births

- 4.2.2 Increasing Burden of Chronic Conditions

- 4.2.3 Rising Prevalence of Malnutrition

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness in Developing Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Nutrition Type

- 5.1.1 Carbohydrates

- 5.1.2 Parenteral Lipid Emulsion

- 5.1.3 Single Dose Amino Acid Solution

- 5.1.4 Trace Elements

- 5.1.5 Other Nutrition Types

- 5.2 By Patient Type

- 5.2.1 Newborn

- 5.2.2 Children

- 5.2.3 Adults

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Clinics

- 5.3.3 Homecare

- 5.3.4 Other End-Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fresenius Kabi AG

- 6.1.2 B. Braun Melsungen AG

- 6.1.3 Baxter International

- 6.1.4 ICU Medical

- 6.1.5 Option Care Health Inc.

- 6.1.6 Abbott

- 6.1.7 Kelun

- 6.1.8 Otsuka Pharmaceutical India Pvt. Ltd.

- 6.1.9 Amanta Healthcare

- 6.1.10 Aculife