|

市場調査レポート

商品コード

1237840

ネットワークセントリックウォーフェア(NCW)市場- 成長、動向、および予測(2023年-2028年)Network Centric Warfare Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| ネットワークセントリックウォーフェア(NCW)市場- 成長、動向、および予測(2023年-2028年) |

|

出版日: 2023年03月03日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

ネットワークセントリックウォーフェア(NCW)市場は予測期間中に4.5%以上のCAGRで推移すると予想されます。

主なハイライト

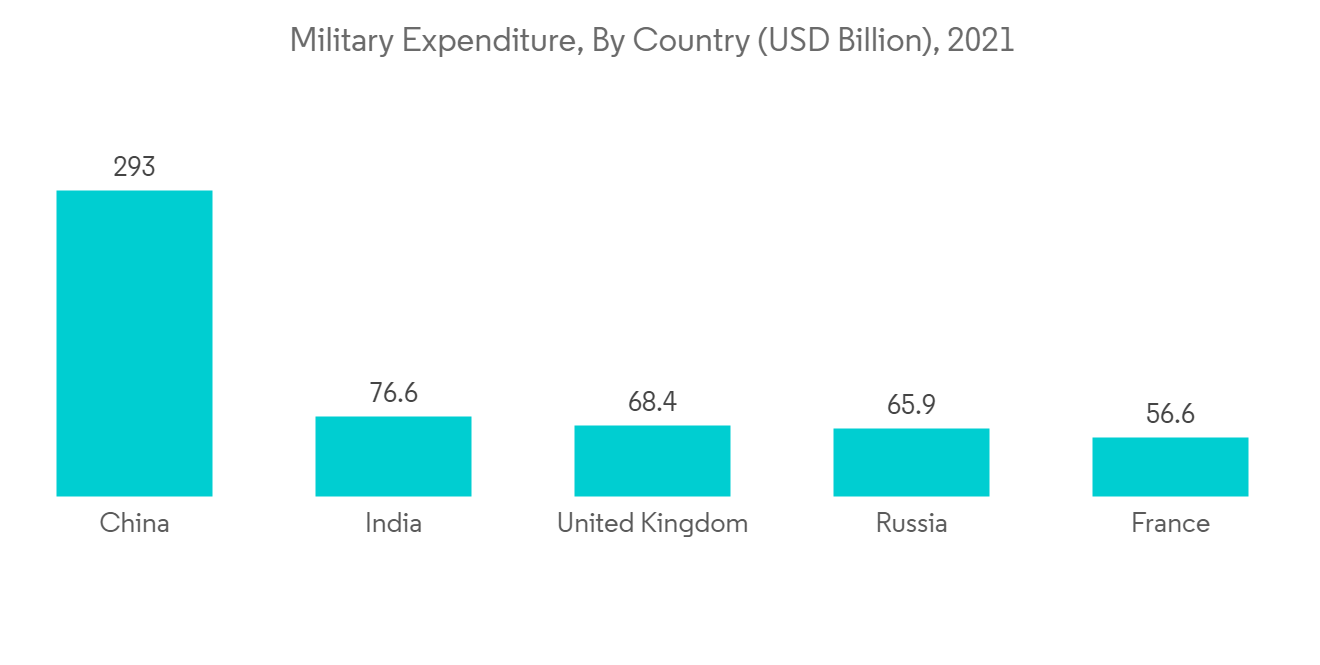

- 世界の防衛分野は、COVID-19パンデミックの影響を最小限に抑えていることがわかります。世界の軍事費は、2021年に約2兆米ドルに達しました。このように、いくつかの国の防衛予算の増大と、防衛分野における先進技術の導入が、防衛分野のダイナミクスを変化させています。International Data Corporation(IDC)の人工知能ガイドによると、AI中心システムを含む人工知能に対する世界の支出は、2022年に1180億米ドルに達しました。

- ネットワークセントリックウォーフェア(NCW)は、決定的な戦争戦闘の優位性を生み出すために、ネットワーク化された部隊が使用する新たな戦術、技術、手順の組み合わせです。センサー、射撃手、意思決定者をネットワーク化し、認識の共有、作戦のテンポの速さ、指揮の速さ、殺傷能力の向上、自己同調の程度、生存率の向上を実現することで、戦闘力の向上を実現します。状況に対する共有意識を高め、より迅速で効果的な意思決定を可能にします。さらに、ロシアとウクライナの戦争は、ロシアによるNATO諸国への不安と脅威の増大のため、欧州諸国によるネットワーク中心ソリューションの需要の高まりにつながっています。

- 主要国は、自国の防衛能力を変革するために、次世代技術への投資を積極的に行っています。人工知能、仮想現実、拡張知能などの先進技術の採用が進むことで、状況認識の向上やリアルタイムの意思決定が可能になります。さらに、防衛におけるAIは、標的認識、戦略的意思決定、脅威の監視、戦闘シミュレーション、サイバーセキュリティなど、さまざまな利点を提供します。

ネットワークセントリックウォーフェア(NCW)の市場動向

情報・監視・偵察(ISR)は予測期間中に目覚ましい成長を見せると予測される

ISR分野は、防衛費の増加やネットワーク中心型ソリューションの利用拡大により、予測期間中に大きな成長を見せると思われます。防衛予算の増加、高度なネットワークソリューションの開拓への支出の増加、意思決定を強化するための次世代技術の導入が、市場の成長を後押ししています。

世界の防衛機関は、戦闘行為におけるミッションの有効性にはリアルタイムの情報が不可欠であることを認識しています。インテリジェントなネットワークは、軍事情報、監視、武器およびITシステム、偵察、指揮統制業務を統合する基盤を提供します。2022年、米国国防総省(DoD)は、軍事情報プログラムに241億米ドルを割り当てました。米国DoDは、プラットフォームの近代化、高度なセンサー、サイバー保護、すべてのデータをメッシュ型ネットワークに結びつけることにより、ISR能力を強化することに重点を置いた。米国DoDは、2023年度予算要求において、世界統合ISRポートフォリオに83億米ドルを割り当てています。このように、軍事能力の向上に対する支出の増加や、戦闘作戦におけるリアルタイムデータのための先進技術の採用が、予測期間中の市場の成長を促進すると予測されています。

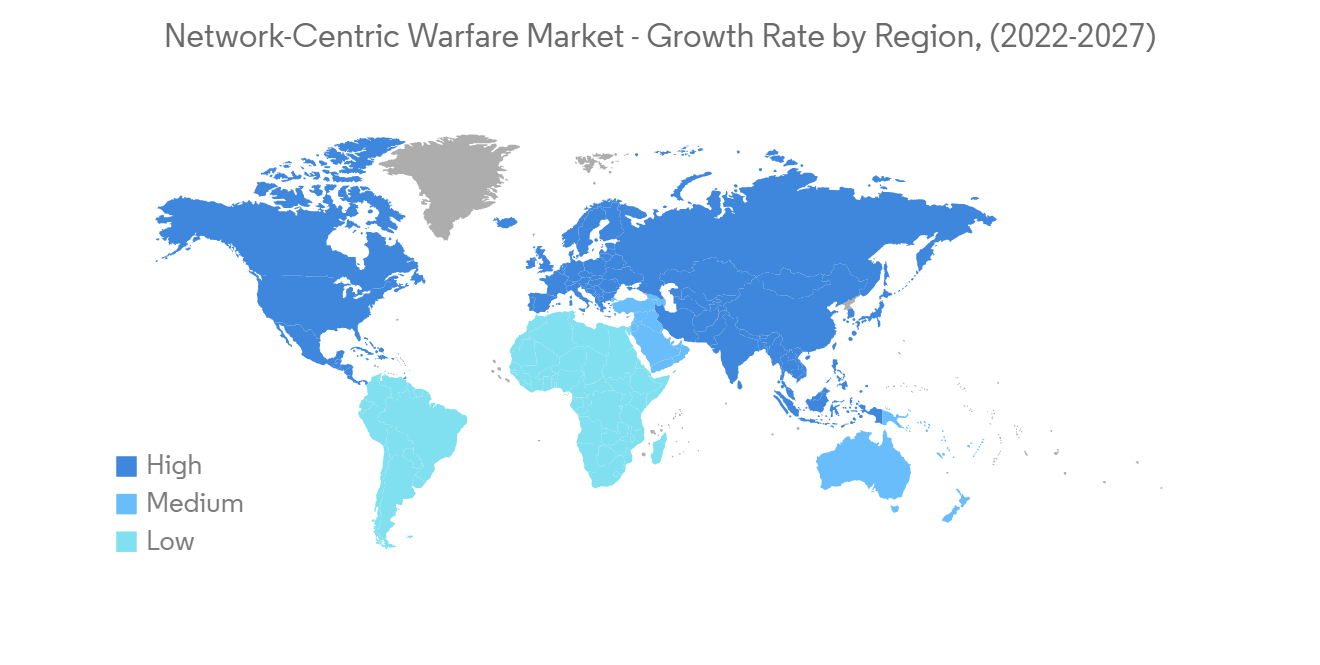

予測期間中、北米が市場を独占すると予測されます。

北米は2022年に最大の市場シェアを占め、予測期間中もその支配が続くと予想されます。この成長は、米国からの防衛費が最も高いことに起因しています。ネットワーク中心ソリューションの採用に対する支出の増加、米国国防総省からの防衛活動用AI対応デバイスの調達の増加が、この地域全体の市場成長を促進します。

米国国防総省(DoD)は、2022年に人工知能(AI)関連技術に8億7,400万米ドルを投資しました。米国DoDは、指揮統制、コンピューティング、ロジスティクスの効率性向上にも力を入れています。米国2023年国防予算要求において、DoDは核指揮統制通信(NC3)プログラムに9億1,900万米ドルを要求しました。また、DoDは、高度なサイバーセキュリティ、サイバー研究開発、サイバー作戦を含むサイバースペース活動に対して112億米ドルを要求しました。

例えば、米国陸軍は2022年1月、General Dynamics Mission Systemsと戦術ネットワーク・オン・ザ・ムーブ通信システムなどの契約を2件締結しました。1つ目の契約は7,499万米ドル相当のサポートサービス、2つ目の契約は2,034万米ドル相当のオン・ザ・ムーブ技術を統合するためのエンジニアリングと技術サポートが含まれています。このように、米国政府による防衛力強化のための支出の増加は、市場の成長を後押ししています。

ネットワークセントリックウォーフェア(NCW)の市場競合分析

ネットワークセントリック市場は、少数のプレーヤーが大きなシェアを占めているため、統合的な市場となっています。

次世代技術のイントロダクションとAI対応防衛装備品の開拓が、市場の成長を促進します。例えば、2021年12月、ルーメン・テクノロジーズは米国陸軍予備軍司令部のネットワーキングソリューションと2,300万米ドル相当の契約を締結しました。この契約により、同社は仮想プライベートネットワークサービスとリモートアクセスソリューションを米国陸軍予備軍の650以上の拠点に提供することになります。このように、防衛軍向けの次世代ネットワーク中心型ソリューションを開発するために、先進技術の利用が増加し、OEMのパートナーシップが拡大していることが、予測期間中の市場の成長を後押しすると考えられます。

その他の特典です。

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件条件

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- アプリケーション

- 情報・監視・偵察(ISR)

- 通信

- コマンド&コントロール

- コンピュータ

- サイバー

- プラットフォーム

- 陸

- 空

- 海

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋地域

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ地域

- 中東・アフリカ地域

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- ベンダーのマーケットシェア

- 企業プロファイル

- Cisco Systems Inc.

- BAE Systems PLC

- General Dynamics Corporation

- Elbit Systems Ltd

- Lockheed Martin Corporation

- Northrop Grumman

- Raytheon Technologies Corporation

- Thales Group

- L3Harris Technologies Inc.

- Lumen Technologies

第7章 市場機会と今後の動向

The network-centric warfare market is expected to register a CAGR of over 4.5% during the forecast period.

Key Highlights

- The global defense sector has witnessed the minimal impact of the COVID-19 pandemic. The global military expenditure reached approximately USD 2 trillion in 2021. Thus, the growing defense budget from several nations and the introduction of advanced technologies in the defense sector are changing the dynamics of the defense sector. According to the International Data Corporation (IDC) artificial intelligence guide, global spending on artificial intelligence, including AI-centric systems, reached USD 118 billion in 2022.

- Network-centric Warfare (NCW) is the combination of emerging tactics, techniques, and procedures used by the networked forces to create a decisive warfighting advantage. It generates increased combat power by networking sensors, shooters, and decision-makers to achieve shared awareness, a high tempo of operations, increased speed of command, greater lethality, a degree of self-synchronization, and raised survivability. It provides an enhanced shared awareness of the situation and enables more rapid and effective decision-making. Furthermore, the Russia-Ukraine war leads to rising demand for network-centric solutions from European countries due to increasing insecurity and threat to NATO countries from Russia.

- Major countries are highly investing in next-generation technologies to transform their defense capabilities. The growing adoption of advanced technologies such as artificial intelligence, virtual reality, and augmented reality leads to improved situational awareness and real-time decision-making. Furthermore, AI in defense provides various advantages, such as target recognition, strategic decision-making, threat monitoring, combat simulation, and cybersecurity.

Network Centric Warfare Market Trends

The Intelligence, Surveillance, and Reconnaissance (ISR) is Projected to Show Remarkable Growth During the Forecast Period

The ISR segment will showcase significant growth during the forecast period owing to the rising defense expenditure and growing use of network-centric solutions. The rising defense budget, increasing spending on the development of advanced network solutions, and introduction of next-generation technologies for enhanced decision-making are driving the growth of the market.

Global defense agencies recognize that real-time information is vital to mission effectiveness in combat operations. An intelligent network provides the foundation to integrate military intelligence, surveillance, weapon and IT systems, reconnaissance, and command and control operations. In 2022, the United States Department of Defense (DoD) allocated USD 24.1 billion for the Military Intelligence Program. The United States DoD focused on enhancing ISR capabilities by modernizing platforms, advanced sensors, cyber protection, and tying all the data into a meshed network. The United States DoD allocated USD 8.3 billion to the global Integrated ISR portfolio in FY 2023 budget request. Thus, increasing expenditure on improving military capabilities and the adoption of advanced technologies for real-time data in combat operations is anticipated to drive the growth of the market during the forecast period.

North America Is Anticipated to Dominate the Market During the Forecast Period

North America held the largest market share in 2022 and is expected to continue its domination during the forecast period. The growth is due to the highest defense expenditure from the United States. Increasing expenditure on the adoption of network-centric solutions and growing procurement of AI-enabled devices for defense operations from the United States Department of Defense drive the growth of the market across the region.

The United States Department of Defense (DoD) invested USD 874 million in artificial intelligence (AI)-related technologies in 2022. The United States DoD also focuses on improving efficiencies in command and control, computing, and logistics. In the United States 2023 defense budget request, the DoD requested USD 919 million for the nuclear command, control, and communication (NC3) program. Also, the DoD requested USD 11.2 billion for cyberspace activities that include advanced cybersecurity, cyber research and development, and cyber operations.

For instance, in January 2022, the United States Army signed two contracts with General Dynamics Mission Systems for the Tactical Network-On-the-Move communication systems and other equipment. The first contract was worth USD 74.99 million for support services, and the second included engineering and technical support to integrate On the Move technology worth USD 20.34 million. Thus, growing spending from the United States government for enhancing defense capabilities drives the growth of the market.

Network Centric Warfare Market Competitor Analysis

The network-centric market is consolidated in nature with few players holding significant shares in the market. Some of the prominent players in the market are Northrop Grumman, Thales Group, BAE Systems, Raytheon Technologies Corporation, and Lockheed Martin Corporation.

The introduction of next-generation technologies and the development of AI-enabled defense equipment drive market growth. For instance, in December 2021, Lumen Technologies signed a contract worth USD 23 million with the United States Army Reserve Command networking solutions. Under the contract, the company would provide virtual private network services and remote access solutions to more than 650 United States Army Reserve locations. Thus, the rising use of advanced technologies and growing partnerships of OEMs to develop next-generation network-centric solutions for defense forces will boost market growth during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.1.2 Communications

- 5.1.3 Command and Control

- 5.1.4 Computer

- 5.1.5 Cyber

- 5.2 Platform

- 5.2.1 Land

- 5.2.2 Air

- 5.2.3 Naval

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Cisco Systems Inc.

- 6.2.2 BAE Systems PLC

- 6.2.3 General Dynamics Corporation

- 6.2.4 Elbit Systems Ltd

- 6.2.5 Lockheed Martin Corporation

- 6.2.6 Northrop Grumman

- 6.2.7 Raytheon Technologies Corporation

- 6.2.8 Thales Group

- 6.2.9 L3Harris Technologies Inc.

- 6.2.10 Lumen Technologies