|

市場調査レポート

商品コード

1237838

直鎖状低密度ポリエチレン(LLDPE)市場- 成長、動向、および予測(2023年-2028年)Linear Low-Density Polyethylene (Lldpe) Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 直鎖状低密度ポリエチレン(LLDPE)市場- 成長、動向、および予測(2023年-2028年) |

|

出版日: 2023年03月03日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

世界の直鎖状低密度ポリエチレン(LLDPE)市場は、予測期間中に5%を超えるCAGRで推移すると予測されています。

COVID-19の影響により、直鎖状低密度ポリエチレンの生産とエチレン原料のサプライチェーンは大きな影響を受けましたが、最終的には2021年に回復しました。衛生面や安全面への懸念から、パッケージング産業が非常に急増し、それによってLLDPE市場の需要が増加し、2022年にはさらに回復すると予想されます。自動車、ヘルスケア、eコマース、パッケージング業界は、直鎖状低密度ポリエチレンの主要なエンドユーザー業界の1つです。

主なハイライト

- 調査した市場の成長を促進する主な要因は、包装需要の増加、フィルムやシートの需要の急増です。

- 一方、他のポリエチレン製品への置き換えやプラスチックの使用禁止は、予測期間中の市場成長を低下させます。

- メタロセン直鎖状低密度ポリエチレン(mLLDPE)は、LLDPEよりも耐貫通性に優れているため、将来的にはチャンスとなる可能性があります。

直鎖状低密度ポリエチレン(LLDPE)の市場動向

LLDPEフィルムの需要増について

- 直鎖状低密度ポリエチレン(LLDPE)は、より高い衝撃強度、引張強度、耐穿孔性、伸びなどの特性を持つため、包装産業で使用されています。

- 飲食品製造会社は、有害な化学物質から製品を保護し、水分含有量を少なくするために、LLDPEフィルムを包装に使用しています。近年、世界的に調理済み製品や調理済みの製品が増えていることから、LLDPEの市場シェアは急上昇しています。

- 可処分所得の増加、ファストフードやフードデリバリーサービスへの嗜好の高まりが、LLDPEフィルムの需要拡大に寄与しました。

- 2020年の落ち込みを経て、2021年にはCOVID-19が多数の最終用途部門に影響を及ぼし、世界のパッケージング産業は安定した成長を再開しました。

- パッケージングは、LLDPEフィルムの最も広範な用途です。中国、米国、日本、インド、ドイツは、世界中のパッケージング産業の成長率が最も速い上位の国々に含まれています。

- eコマース産業の急成長は、eコマース用パッケージのLLDPE需要に直結しています。

- 上記のすべての要因が、予測期間中にパッケージング業界からのLLDPEフィルムの需要に大きな影響を与えると予想されます。

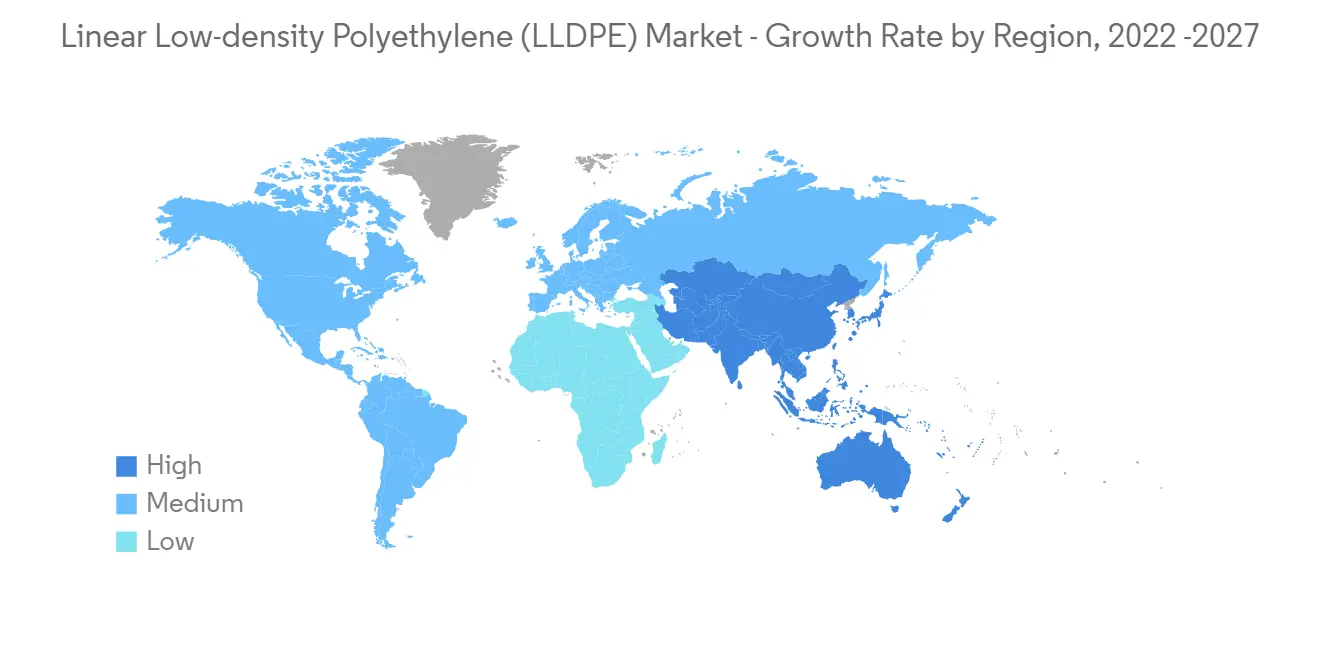

アジア太平洋地域が市場を独占する

- アジア太平洋地域は、急速な工業化とLLDPEベースの包装材需要の高まりにより、直鎖状低密度ポリエチレン(LLDPE)市場で最大のシェアを占めています。アジア市場では、医薬品、食品加工、自動車産業における製造活動の活発化に伴い、包装ビジネスが急ピッチで拡大しています。

- 中国の包装産業は、CAGR6.8%近い驚異的な成長を記録し、2025年には2,000億米ドルに達すると予想されています。このようなパッケージング産業の勢いは、同国におけるLLDPEの市場需要を押し上げると期待されています。

- パッケージング産業では、主にLLDPEフィルムが使用されています。LLDPEは、自動車用プラスチック部品、玩具、水筒などの射出成形製造分野でも使用されています。射出成形の増加もLLDPE市場を増加させます。

- OICAによると、アジア太平洋地域の自動車用プラスチック部品市場は成長が見込まれています。2021年、中国の自動車生産台数は2,608万米ドルに達しました。自動車生産の増加は、調査対象市場の需要を促進すると推定されます。

- インドの食品加工は包装の最大消費者で45%、次いで医薬品とパーソナルケア製品です。これらのエンドユーザー層からの需要の増加は、拡大のための大きな可能性を生み出しています。

- これらの要因から、直鎖状低密度ポリエチレンの市場は、予測期間中、アジア太平洋地域で高い需要が見込まれています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件条件

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- パッケージ業界からの需要増

- フィルム・シートの需要急増

- 抑制要因

- 他のポリエチレン製品への置き換え

- 産業バリューチェーン分析

- ポーターズファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品・代替サービスのスレット

- 競合の度合い

第5章 市場セグメンテーション

- アプリケーション

- フィルム

- 成形

- 射出成形

- その他のアプリケーションタイプ

- エンドユーザー業界

- 農業

- 電気・電子

- パッケージング

- 建設

- その他のエンドユーザー産業

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 中東・アフリカ地域

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢について

- M&A、ジョイントベンチャー、コラボレーション、契約など

- 市場シェア(%)**/ランキング分析

- 主要なプレーヤーが採用した戦略

- 企業プロファイル

- Chevron Phillips Chemical Company

- CNPC

- Exxon Mobil Corporation

- Formosa Plastic Corporation

- INEOS

- LG Chem

- Lyonde Bassells Industries Holdings BV

- Mitsubishi Chemicals

- Nova Chemicals Corporate

- Reliance Industries Limited

- SABIC

- SINOPEC

- The Dow Chemical Company

第7章 市場機会と今後の動向

- 製薬業界におけるLLDPEの需要拡大について

The Global Linear Low-density Polyethylene (LLDPE) market is estimated to register a CAGR of over 5% during the forecast period. Due to the impact of COVID-19, linear low-density polyethylene production and the ethylene raw material supply chain were highly affected but eventually recovered in 2021. Due to hygiene and safety concerns, the packaging industry has seen an enormous surge, thereby increasing the demand for the LLDPE market, which is expected to recover further in 2022. The automotive, healthcare, e-commerce, and packaging industries are among the major end-user industries of linear low-density polyethylene.

Key Highlights

- The major factors driving the growth of the market studied are the rise in demand for packaging and surging demand for film and sheets.

- On the flip side, substituting other polyethylene products and banning plastics reduce market growth during the forecast period.

- The development of Metallocene linear low-density polyethylene (mLLDPE) is likely to act as an opportunity in the future, mLLDPE has relatively more puncture resistance than LLDPE.

Linear Low-density Polyethylene Market Trends

Rise in Demand for LLDPE Films

- Linear low-density polyethylene is used in the packaging industry because of its properties, such as higher impact strength, tensile strength, puncture resistance, elongation, etc.

- Food and beverage manufacturing companies use LLDPE films for packaging to secure their product from harmful chemicals and less moisture content. The recent increase in ready-to-eat and pre-cooked products globally has surged LLDPE's market share.

- The growth in disposable income and the increasing preference for fast food and food delivery services contributed to increasing demand for LLDPE films.

- Following a dip in 2020, the global packaging industry resumed steady growth in 2021, as COVID-19 affected numerous end-use sectors.

- Packaging is the most extensive application of LLDPE films. China, the United States, Japan, India, and Germany are amongst the top countries with the fastest growth rate in the packaging industry across the world.

- Rapid growth in the e-commerce industry directly correlates to the LLDPE demand for e-commerce packaging.

- All the above factors are expected to significantly impact the demand for LLDPE films from the packaging industry during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region accounts for the largest share of the Linear low-density polyethylene (LLDPE) market, owing to rapid industrialization and rising LLDPE-based packaging material demand in the region. The packaging business in the Asian market is expanding at a rapid pace with the increased manufacturing activities in the pharmaceutical, food processing, and automotive industries.

- The packaging industry in China is expected to register tremendous growth with a CAGR of nearly 6.8%, reaching USD 0.2 trillion by 2025. This positive momentum in the packaging industry is expected to boost the market demand for LLDPE in the country.

- The packaging industry primarily uses LLDPE films. LLDPE is also used in the injection molding manufacturing sectors in automotive plastic parts, toys, and water bottles. An increase in injection molding also increases the LLDPE market.

- According to the OICA, the Asia-Pacific automotive plastic parts market is expected to grow. In 2021, automotive production in China reached USD 26.08 million. The increase in automotive production is estimated to drive the demand for the market studied.

- Indian food processing is the largest consumer of packaging at 45%, followed by pharmaceuticals and personal care products. Increasing demand from these end-user segments is creating a huge potential for expansion.

- Due to all these factors, the market for linear low-density polyethylene is expected to have a high demand in the Asia-Pacific region during the forecast period.

Linear Low-density Polyethylene Market Competitor Analysis

The Linear low-density polyethylene LLDPE market is partially consolidated in nature. Some of the major players in the market include INEOS, Formosa Plastic Corporation, Dow, Mitsubishi Chemicals, LG Chem, Exxon Mobil Corporation, SINOPEC, SABIC, Lyondellbasell Industries Holdings BV, Reliance Industries Limited, and Chevron Phillips Chemical Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increase Demand from the Packaging Industry

- 4.1.2 Surging Demand for Film and Sheets

- 4.2 Restraints

- 4.2.1 Substitution of Other Polyethylene Products

- 4.3 Industry Value Chain Analysis

- 4.4 Poter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Thret of Substitute products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Films

- 5.1.2 Molding

- 5.1.3 Injection Molding

- 5.1.4 Other Application Types

- 5.2 End-user Industry

- 5.2.1 Agricultute

- 5.2.2 Electrical and Electronics

- 5.2.3 Packaging

- 5.2.4 Constrution

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chevron Phillips Chemical Company

- 6.4.2 CNPC

- 6.4.3 Exxon Mobil Corporation

- 6.4.4 Formosa Plastic Corporation

- 6.4.5 INEOS

- 6.4.6 LG Chem

- 6.4.7 Lyonde Bassells Industries Holdings BV

- 6.4.8 Mitsubishi Chemicals

- 6.4.9 Nova Chemicals Corporate

- 6.4.10 Reliance Industries Limited

- 6.4.11 SABIC

- 6.4.12 SINOPEC

- 6.4.13 The Dow Chemical Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for LLDPE in the Pharmaceutical Industry