|

市場調査レポート

商品コード

1685719

食肉原料- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Meat Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 食肉原料- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

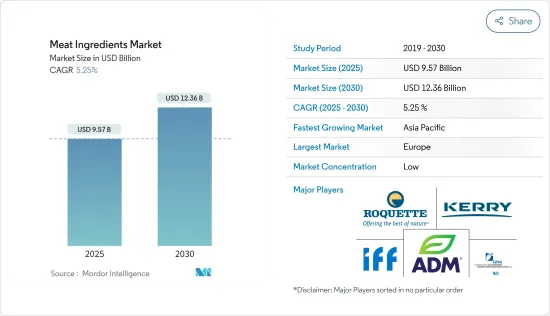

食肉原料市場規模は2025年に95億7,000万米ドルと推定され、予測期間中(2025年~2030年)のCAGRは5.25%で、2030年には123億6,000万米ドルに達すると予測されます。

主なハイライト

- 世界の食肉原料市場は、今年78億3,540万米ドルと評価されました。食肉原料市場を牽引する主な要因の1つは、地域全体で食肉加工製品の需要が増加していることです。食肉原料は食肉加工製品に特別に強化された品質を与えます。

- ミートエクステンダーのニーズは急速に高まっています。ミート・エクステンダーは、炭水化物、タンパク質、その他の栄養素のブレンドを含む植物由来の物質で、食肉製品の栄養的・機能的品質を向上させるために使用されます。これらの成分の栄養価はさておき、ミート・エクステンダーは環境への影響の低さから人気が高まっています。その結果、食肉原料市場は安定した成長率で伸びています。

- 中長期的な視点に立てば、食肉原料市場は急成長しています。この市場を推進している重要な要因は、インスタント肉ベースのスナックなど、コンビニエンス・フードの需要が高いことです。また、食肉、冷凍食肉などの加工食品におけるユーザー用途の増加、栄養と味の融合による調味料や塩の使用量の増加などの要因も、この市場を牽引しています。

- しかし、品質基準、クリーン・ラベリング、健康への懸念といった要因が市場を阻害しています。食肉加工技術もまた、重厚長大な食肉製品の改良に貢献すると思われます。新興諸国市場では、FDA(米国食品医薬品局)やその他の規制機関による規制の強化が、加工食品(主に加工肉と鶏肉)の成長を妨げています。

食肉原料市場の動向

クリーンラベル肉製品に対する需要の増加

- 自然で無添加の食品に対する需要は食品業界を席巻し、衰える気配はないです。今日の消費者は、自分たちが口にする食品にかつてないほど関心を寄せています。こうした製品の人気上昇は、環境の持続可能性、動物福祉、より良い健康的な食品システムの構築に関する意識の高まりの直接的な結果です。

- 便利で健康的な自然食品への強い需要が食肉業界に新たなチャンスをもたらす一方で、クリーン・ラベル革命は課題ももたらしました。最近の研究では、意思決定プロセスの一環として食品表示をより詳細にチェックする消費者が増えていることが実証されています。

- 2021年に国際食品情報協議会(International Food Information Council Foundation)が発表した調査によると、参加者の半数以上(54%)が、包装前(FOP)ラベルが食品や飲食品の購入に影響を与えていると回答し、4分の1近く(24%)がかなりの影響を与えていると同意しています。ほとんどの調査参加者(94%)は、少なくとも1つのFOPラベルをよく知っていました。日付、価格、原産国に加え、原材料の重要性も増しています。特に添加物は、先進国の消費者の間で主な関心事のひとつとなっています。しかし、新興市場の消費者にとっても、添加物はますます重要視されるようになっており、クリーン・ラベルの食品と原材料に新たな機会がもたらされています。

アジア太平洋が急成長地域

- アジア太平洋は最も急成長する市場であり、予測期間中のCAGRは堅調であると予測されます。この成長は主に、特にインド、中国、その他のアジア諸国のような新興諸国において、多数の食品加工・貯蔵産業が存在することによるものです。中国はこの地域で最大の食肉消費国のひとつです。同国では労働人口の増加と急速な都市化により、消費者の簡便食品への志向が高まっています。これが同国の食肉原料市場に拍車をかけています。

- 加えて、同地域の市場成長は、急速な経済開拓、顧客の食生活や嗜好の変化、風味豊かな食肉製品への需要の高まりにより、食肉加工産業への投資が拡大していることが主な要因となっています。

- さらに、食肉加工業界は政府のイニシアティブの恩恵を受けており、これが同市場における食肉原料の需要を促進すると考えられます。

- 例えば、第15回財政委員会サイクルは、プラダン・マントリ・キサンSAMPADAヨジャナ(農産物海洋加工および農産物加工クラスター開発計画)を2026年まで4,600カロールインドルピー(6億2,500万インドルピー)延長しました。PM Kisan SAMPADA Yojanaは以下のプログラムを実施する:統合コールドチェーンと付加価値インフラ、食品加工・保存能力創出(ユニット・スキーム)、農産物加工クラスター向けインフラ、食品安全・品質保証インフラ、人材・制度-研究開発、グリーン作戦です。

- さらに、中国、インド、韓国、シンガポールなどのアジア諸国では、様々な産業から加工肉への需要が増加しており、鶏肉や羊肉のバリエーションが人気であるため、市場は当面急成長すると予想されます。

食肉原料業界の概要

世界の食肉原料市場は、多くの地域レベルおよび国レベルの企業が存在するため、競争の激しい市場で事業を展開しています。食肉原料市場の主要企業には、International Flavors &Fragrances, Inc.、Kerry Group plc、Firmenich SA、Givaudan、Archer Daniels Midland Companyなどが含まれます。新製品発売のほか、企業は合併、買収、提携といった無機的な拡大手段に頼ることが多くなっています。さらに、規模の経済と消費者の高いブランド・ロイヤルティが、これらの企業に優位性を与えています。あらゆるカテゴリーにおける製品ポートフォリオのさらなる拡大は、市場における企業の地位を高める可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 原料

- 結合剤

- エクステンダー

- 充填剤

- 着色料

- 香料

- 防腐剤

- テクスチャー剤

- 塩類

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- 主要企業の戦略

- 市場シェア分析

- 企業プロファイル

- International Flavors & Fragrances, Inc.

- Kerry Group plc

- Firmenich SA

- Archer Daniels Midland Company

- Suddeutsche Zuckerrubenverwertungs-Genossenschaft eG(Beneo)

- Roquette Freres

- Tate & Lyle PLC

- Koninklijke DSM N.V.

- Ingredion Incorporated

- Cargill, Incorporated

- Corbion N.V.

- Givaudan SA

第7章 市場機会と今後の動向

The Meat Ingredients Market size is estimated at USD 9.57 billion in 2025, and is expected to reach USD 12.36 billion by 2030, at a CAGR of 5.25% during the forecast period (2025-2030).

Key Highlights

- The global meat ingredients market was valued at USD 7,835.4 million in the current year. One of the primary factors driving the meat ingredients market is the increasing demand for processed meat products across the regions. Meat ingredients give processed meat products special enhanced qualities.

- The need for meat extenders is rapidly increasing. Meat extenders are plant-based substances that include a blend of carbohydrates, proteins, and other nutrients and are used to improve the nutritional and functional qualities of meat products. Aside from the nutritional value of these components, meat extenders are becoming more popular due to their lower environmental impact. As a result, the meat ingredients market is growing at a steady growth rate.

- From a medium- to long-term perspective, the meat ingredients market is growing rapidly. A significant factor propelling this market is the high demand for convenience foods, such as instant meat-based snacks. Other factors, such as the increasing user application in processed foods, such as meat, frozen meat, etc., along with nutrition and taste convergence, which increased the usage of flavoring agents and salts, are also driving this market.

- However, factors like quality standards, clean labeling, and health concerns hinder the market. Meat processing technology will also contribute to the improvement of heavily extended meat products. Increased regulations by the FDA and other regulatory bodies in the developed markets are hindering the growth of processed food, mainly processed meat and poultry, in the countries.

Meat Ingredients Market Trends

Increasing Demand for Clean Label Meat Products

- The demand for natural, additive-free food has taken the food industry by storm and shows no sign of abating. Today's consumers are more concerned about the food they eat than ever before. The rise in popularity of these products has been a direct result of increasing awareness regarding environmental sustainability, animal welfare, and creating better and healthier food systems.

- While the strong demand for convenient, healthy, and natural products has opened up new opportunities for the meat industry, the clean label revolution has also brought challenges. Recent studies have demonstrated that an increasing number of consumers check food labels more thoroughly as part of the decision-making process.

- According to a study published by the International Food Information Council Foundation in 2021, over half (54%) of participants indicated that front-of-package (FOP) labels have an impact on food and beverage purchases, and nearly a quarter (24%) agree that they have a considerable impact. Most survey participants (94%) were familiar with at least one FOP label. Besides the date, price, and country of origin, ingredients are becoming increasingly important. In particular, additives are one of the main concerns among consumers in developed countries. Still, it is also a growing consideration for consumers in emerging markets, opening up new opportunities for clean-label foods and ingredients.

Asia Pacific is the Fastest Growing Region

- The Asia-Pacific region is projected to be the fastest-growing market, with a robust CAGR during the forecast period. This growth is mainly due to a large number of food processing and storage industries, particularly in developing countries such as India, China, and a few other Asian countries. China is one of the largest countries of meat consumers in the region. The consumer's inclination toward convenience food has increased due to the rising working population and rapid urban urbanization in the country. This is fueling the meat ingredients market in the country.

- Additionally, the region's market growth is mainly attributed to the growing investment in the processed meat industry due to the rapid economic development, changing customer dietary habits and preferences, and increasing demand for flavorful meat products.

- Further, the meat processing industry benefits from government initiatives, which will likely drive the demand for meat ingredients in the market.

- For instance, the 15th Finance Commission cycle extended the Pradhan Mantri Kisan SAMPADA Yojana (Scheme for Agro-Marine Processing and Development of Agro-Processing Clusters) by INR 4,600 crores (625 million) until 2026. PM Kisan SAMPADA Yojana will implement the following programs: Integrated Cold Chain and Value Addition Infrastructure, Food Processing and Preservation Capacity Creation (Unit Scheme), Infrastructure for Agro-processing Clusters, Food Safety and Quality Assurance Infrastructure, Human Resources and Institutions - Research and Development, Operation Greens.

- Moreover, owing to the increasing demand for processed meat from various industries and the popularity of chicken and mutton variants in Asian countries like China, India, South Korea, Singapore, and others, the market is expected to grow rapidly in the foreseeable future.

Meat Ingredients Industry Overview

The Global meat ingredients market facilitates its operation in a highly competitive market, owing to the presence of many regional and country-level players. The key players in the meat ingredients market include International Flavors & Fragrances, Inc., Kerry Group plc, Firmenich SA, Givaudan, and Archer Daniels Midland Company, among others. Besides new product launches, companies are increasingly resorting to inorganic means of expansion, such as mergers, acquisitions, and collaborations. Further, economies of scale and high brand loyalty among consumers give these companies an upper edge. Further expansion of the product portfolio within all categories may enhance the companies' positions in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Ingredient

- 5.1.1 Binders

- 5.1.2 Extenders

- 5.1.3 Fillers

- 5.1.4 Coloring Agents

- 5.1.5 Flavoring Agents

- 5.1.6 Preservatives

- 5.1.7 Texturing Agents

- 5.1.8 Salts

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Spain

- 5.2.2.5 Italy

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 Australia

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East & Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East & Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategy Adopted by Key Players

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 International Flavors & Fragrances, Inc.

- 6.3.2 Kerry Group plc

- 6.3.3 Firmenich SA

- 6.3.4 Archer Daniels Midland Company

- 6.3.5 Suddeutsche Zuckerrubenverwertungs-Genossenschaft eG (Beneo)

- 6.3.6 Roquette Freres

- 6.3.7 Tate & Lyle PLC

- 6.3.8 Koninklijke DSM N.V.

- 6.3.9 Ingredion Incorporated

- 6.3.10 Cargill, Incorporated

- 6.3.11 Corbion N.V.

- 6.3.12 Givaudan SA