|

|

市場調査レポート

商品コード

1439877

硬化剤:市場シェア分析、業界動向と統計、成長予測(2024-2029)Curing Agent - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 硬化剤:市場シェア分析、業界動向と統計、成長予測(2024-2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

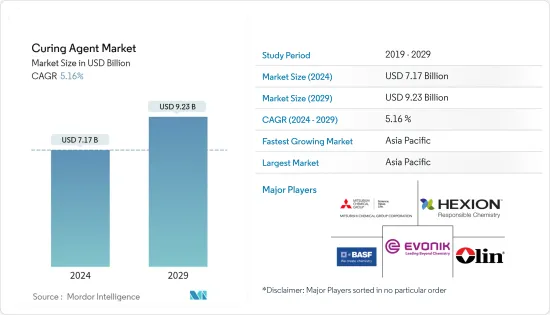

硬化剤市場規模は2024年に71億7,000万米ドルと推定され、2029年までに92億3,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.16%のCAGRで成長します。

硬化剤市場は、新型コロナウイルス感染症(COVID-19)のパンデミックにより、塗料やコーティング、建築や建設などの業界が封じ込め措置や経済的理由から生産の遅延を余儀なくされ、生産と移動が鈍化し、悪影響を受けました。混乱。現在、市場はパンデミックから回復しています。市場は2022年にパンデミック前の水準に達し、今後も着実に成長すると予想されています。

塗料およびコーティング、建築および建設業界からの需要の増加により、市場の成長が促進されると予想されます。

しかし、揮発性有機化合物(VOC)の排出を削減するための硬化剤に関連する厳しい環境規制が市場の拡大を妨げると予想されます。

環境に優しい低VOCまたは非VOC剤の開発は、市場が繁栄する機会を提供すると予想されます。

アジア太平洋地域が世界中の市場を独占しており、中国、インド、日本などの国々が最大の消費国となっています。

硬化剤市場動向

建築・建設業界におけるエポキシ硬化剤の需要の拡大

- 硬化剤の中でも、エポキシ硬化剤はさまざまな用途に使用されており、予測期間中に市場で最大のシェアを占めると予想されます。

- 建設業界では、耐環境性と優れた強度を提供する熱硬化性接着剤を製造するためにエポキシ硬化剤が使用されています。

- エポキシ硬化剤は、建築インフラを提供し、建設上の課題を克服するために、建築および建設用の軽量複合材料を開発するために使用されます。

- エポキシ樹脂は、コンクリートを湿気から保護するためにプライマー、シーラー、防水剤として広く使用されています。エポキシ樹脂は、コンクリートに優れた接着性、速乾性、高い機械的強度を与えるため、コンクリートの硬化に使用されます。

- オックスフォード・エコノミクスによると、世界の建設産業は2025年までに13兆3,000億米ドルに達すると予想されており、2020年からの5年間で2兆6,000億米ドルの生産高が増加します。

- アジア太平洋地域の建設セクターは世界最大です。中国とインドの住宅建設市場の拡大により、アジア太平洋地域で住宅が最も高い成長を記録すると予想されています。これら2つの地域は、2030年までに世界の中産階級の43.3%以上を占めると予想されています。

- また、中国国家統計局によると、中国の建設生産高は2022年に約4兆1,100億米ドルでピークに達しました。結果として、これらの要因により市場の需要が増加する傾向があります。

- したがって、上記のような要因により、調査対象の市場は予測期間中に大幅に成長すると予想されます。

アジア太平洋地域が市場を独占

- アジア太平洋地域は、中国、インド、日本などの主要国における塗料、コーティング、接着剤、建設などの産業の拡大により、予測期間中に硬化剤の最大の市場を占めると予想されています。

- 硬化剤は、プライマー、粉体塗装、トップコートの配合、軽量複合材の製造、モルタル、電気鋳物などに使用されます。水中で硬化できるため、海洋用途にも適しています。

- 硬化剤は、低温または高温での硬化、可変ポットライフ、高強度、優れた耐食性など、幅広い特性を備えているため、さまざまな用途に使用できます。

- 中国塗料工業協会によると、アジア太平洋は引き続き塗料業界の主要な成長原動力となっています。中国は1,000社を超えるコーティング会社が操業しており、業界の主要企業となっています。

- この成長により、日本ペイント、アクゾノーベル、中国マリンペイント、PPGインダストリーズ、BASF SE、アクサルタコーティングスなど、中国に製造拠点を設けている世界の大手塗料メーカーからの投資が集まっています。

- 2022年7月、BASF SEは子会社のBASF Coatings(Guangdong)(BCG)を通じて、中国南部の広東省江門市にある同社のコーティング拠点で自動車補修用コーティングの製造能力を拡張しました。同社はこの拡張プロジェクトにより生産能力を年間3万トンに増強しました。

- さらに、インドの塗料およびコーティング産業も過去20年間で大幅な成長を遂げました。この業界は3,000社以上の塗料メーカーで構成されており、国内には主要な世界的企業が存在します。

- 2023年1月、アジアンペイントは、インドのマディヤプラデーシュ州に年間4億リットルの生産能力を持つ新しい水性塗料製造工場への200億ルピー(2億4,053万米ドル)の投資を承認しました。この施設の製造は3年以内に稼働開始される予定です。

- したがって、上記の要因は、アジア太平洋市場の成長する建設産業が予測期間中に調査対象市場にプラスの影響を与えることを示しています。

硬化剤業界の概要

硬化剤市場は本質的に部分的に細分化されています。調査対象市場の主要企業(順不同)には、BASF SE、Hexion、Olin Corporation、三菱化学株式会社、およびEvonik Industries AGなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 塗料およびコーティング業界からの需要の増加

- 建築・建設業界におけるエポキシ硬化剤の需要の拡大

- その他の 促進要因

- 抑制要因

- 厳しい環境規制

- その他の拘束具

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベースの市場規模)

- タイプ

- エポキシ

- ポリウレタン

- ゴム

- アクリル

- その他のタイプ(シリコン等)

- 用途別

- 建築と建設

- 複合材料

- 塗料とコーティング

- 接着剤およびシーラント

- 電気および電子

- その他の用途(風力エネルギーなど)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- サウジアラビア

- 南アフリカ

- その他中東およびアフリカ

- アジア太平洋

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 市場シェア(%)**/ランキング分析

- 有力企業が採用した戦略

- 企業プロファイル

- Alfa Chemicals

- BASF SE

- Cardolite Corporation

- DIC Corporation

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Mitsubishi Chemical Corporation

- Olin Corporation

- Supreme Polytech Pvt. Ltd.

第7章 市場機会と将来の動向

- 環境に優しい低VOCまたは非VOC硬化剤の開発

- その他の機会

The Curing Agent Market size is estimated at USD 7.17 billion in 2024, and is expected to reach USD 9.23 billion by 2029, growing at a CAGR of 5.16% during the forecast period (2024-2029).

The curing agent market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as paints and coatings, building and construction, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The increasing demand from the paints and coatings and building and construction industries is expected to fuel market growth.

However, stringent environmental regulations associated with curing agents to reduce volatile organic compounds (VOC) emissions are anticipated to hamper market expansion.

The development of environmentally friendly low or non-VOC agents is expected to provide opportunities for the market to flourish.

The Asia-Pacific region dominated the market around the world, with countries like China, India, and Japan being the biggest consumers.

Curing Agent Market Trends

Growing Demand for Epoxy Curing Agents In Building and Construction Industry

- Among curing agents, epoxy curing agents are used for a variety of applications and are expected to account for the largest share of the market during the forecast period.

- In the construction industry, epoxy curing agents are used to produce thermosetting adhesives that provide environmental resistance and superior strength.

- Epoxy curing agents are used to develop lightweight composites for building and construction to provide architectural infrastructure and overcome construction challenges.

- Epoxy resins as primers, sealers, and waterproofing agents are extensively used to protect concrete from moisture. Epoxy resins are used in curing concrete as they provide great adhesion, fast drying, and high mechanical strength to concrete.

- According to Oxford Economics, the global construction industry is expected to reach USD 13.3 trillion by 2025 - adding USD 2.6 trillion to output in five years from 2020.

- The construction sector in the Asia-Pacific region is the largest in the world. The highest growth for housing is expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India. These two regions are expected to represent over 43.3% of the global middle class by 2030.

- Also, according to the National Bureau of Statistics of China, China's construction output peaked in 2022 at about USD 4.11 trillion. As a result, these factors tend to increase the market demand.

- Therefore, owing to such factors mentioned above, the studied market is expected to grow significantly during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to account for the largest market for curing agents during the forecast period owing to the expanding industries such as paints and coatings, adhesives, construction, etc., in major countries such as China, India, Japan, etc.

- Curing agents are used in primer, powder coating, and topcoat formulations, production of lightweight composites, mortars, electrical castings, and many more. They are even suitable for marine applications because of their underwater cure.

- Curing agents can be used for a variety of applications because of their wide range of properties, such as low or high-temperature cure, variable pot life, higher strength, and excellent corrosion resistance.

- According to the China Paint Industry Association, Asia-Pacific continues to be a major growth driver for the coatings industry. With more than 1000 coating companies in operation, China has become a major player in the industry.

- This growth has attracted investments from leading global coating manufacturers such as Nippon Paint, AkzoNobel, Chugoku Marine Paints, PPG Industries, BASF SE, and Axalta Coatings, which have established manufacturing bases in China.

- In July 2022, BASF SE, through its subsidiary BASF Coatings (Guangdong) Co., Ltd. (BCG), expanded its manufacturing capabilities for automotive refinish coatings at its coatings site in Jiangmen, Guangdong Province in South China. The company increased its production capacity to 30,000 tons annually through this expansion project.

- Further, the Indian paint and coatings industry also witnessed significant growth over the past two decades. The industry comprises more than 3,000 paint manufacturers, with the presence of major global players in the country.

- In January 2023, Asian Paints approved an investment of INR 20 billion (USD 240.53 million) for a new waterborne paint manufacturing plant with 400 million liters per annum capacity in Madhya Pradesh, India. The facility's manufacturing is expected to be commissioned in three years.

- Therefore, the factors mentioned above indicate a positive influence of the growing construction industry in the Asia-Pacific market on the studied market over the forecast period.

Curing Agent Industry Overview

The curing agent market is partially fragmented in nature. The major players in the studied market (not in any particular order) include BASF SE, Hexion, Olin Corporation, Mitsubishi Chemical Corporation, and Evonik Industries AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Paints and Coatings Industry

- 4.1.2 Growing Demand for Epoxy Curing Agents in Building and Construction Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Rubber

- 5.1.4 Acrylic

- 5.1.5 Other Types (Silicone, etc.)

- 5.2 By Application

- 5.2.1 Building and Construction

- 5.2.2 Composites

- 5.2.3 Paints and Coatings

- 5.2.4 Adhesives and Sealants

- 5.2.5 Electrical and Electronics

- 5.2.6 Other Applications (Wind Energy, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alfa Chemicals

- 6.4.2 BASF SE

- 6.4.3 Cardolite Corporation

- 6.4.4 DIC Corporation

- 6.4.5 Evonik Industries AG

- 6.4.6 Hexion

- 6.4.7 Huntsman International LLC

- 6.4.8 Mitsubishi Chemical Corporation

- 6.4.9 Olin Corporation

- 6.4.10 Supreme Polytech Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Environmental Friendly Low or Non-VOC Curing Agents

- 7.2 Other Opportunities