|

市場調査レポート

商品コード

1640507

バイオソリッド-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Biosolids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バイオソリッド-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

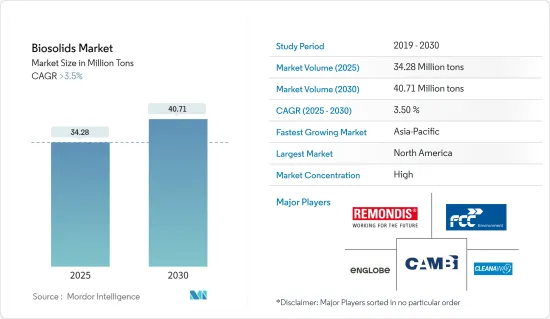

バイオソリッド市場規模は2025年に3,428万トンと予測され、2030年には4,071万トンに達すると予測され、予測期間(2025~2030年)のCAGRは3.5%を超えると予測されます。

COVID-19パンデミックは2020年のバイオソリッド市場にマイナスの影響を与えました。しかし、農地でのバイオソリッド需要の高まりが、パンデミック以降の産業全体の成長を後押ししています。

主要ハイライト

- 市場を牽引している主要要因のひとつは、危険な化学肥料を代替する必要性と、世界各国における厳しい排出規制です。

- 一方、一般に入手可能なバイオソリッドに関する矛盾した情報は、調査した市場の成長を鈍らせると予想されます。

- アジア太平洋、主に中国とインドにおける汚泥処理への注目の高まりは、まもなく産業成長の新たな道を提供すると予想されます。

- 北米は、環境に優しい技術に対する政府と公的支援により、バイオソリッド市場を独占しています。

バイオソリッド市場の動向

農地利用が市場を独占

- バイオソリッドは、農地、森林、放牧地、または埋め立てが必要な攪乱地で使用することができます。

- 消費量では、農地利用が最も多くバイオソリッドを消費しています。アジア太平洋と北米の一貫した人口増加は、農業用収量の必要性を増大させることが予想され、これはこのセグメントにおけるバイオソリッドの消費にプラスの影響を与える可能性があります。

- 国際穀物協会によると、2021~2022年度の世界の穀物総生産量は約22億9,400万トンで、前年度より約3.05%増加しました。さらに、同協議会の予測によると、2022~2023年度の世界の穀物総生産量は22億6,700万トンに減少します。しかし、2023~2024年度には2,310トンに達すると予想されています。

- 中国は世界の穀物生産全体の約7%を占め、世界人口の22%を養っています。同国は、米、綿花、ジャガイモ、その他の作物を含む様々な作物の最大の生産国です。

- 農業・農業従事者福祉省による農作物生産の第3次事前予測によると、2022~23年の国内の総食糧穀物生産量は、3億5,560万トン(MT)から3億3,050万トン(MT)となりました。

- 科学者や農業従事者は、作物の生産性を向上させ、不均衡な人口増加から生じる食糧需要を満たすための新技術を求めています。さらに、米国などでは過去10年間で、利用可能な農地面積が減少しています。

- バイオソリッドは、肥料や土壌改良剤として、人間の作物生産に効果的に利用できます。バイオソリッドは通常、従来の農機具を使って土壌に投入されます。また、畜産用の肥料としても利用されています。

- 大企業や農業従事者は、畜産や肉製品で存在感を示すようになってきています。彼らは畜産物生産の需要を増大させており、それが畜産物生産用の肥料としてバイオソリッドを利用する原動力となっています。このため、農地利用におけるバイオソリッドの需要が増加しています。

- バイオソリッドは肥料コストの削減にも役立ち、作物の成長に必要な微量栄養素を多く供給します。世界人口の増加により、農業へのニーズが高まることが予想され、このことが農業セグメントでのバイオソリッドの使用に影響を与える可能性があります。

- したがって、予測期間中、農地利用が市場を独占すると予想されます。

北米が市場を独占する

- 北米は、米国やカナダなどの国々における環境に優しい技術に対する政府や公的支援により、市場を独占しています。

- 米国では、バイオソリッド市場は、政府も一般市民も環境に良い技術を使いたがっているという事実が大きな原動力となっています。

- 米国環境保護庁(EPA)は、高品質の下水処理汚泥を、汚染物質を大量に含む生汚泥と区別するため、「バイオソリッド」という名称を採用しました。

- 再利用できない廃水からのバイオソリッドを処分する方法(埋立地に入れるなど)と、良い方法で利用する方法(バイオガスやエネルギー回収を伴う埋め立てなど)があります。

- バイオソリッドは廃水処理過程で発生し、米国環境保護庁の40 CFR Part 503規制を満たすために広く利用されています。

- 現在国内で発生するバイオソリッドの大半は、低レベルの汚染物質を含むEQまたはPCバイオソリッドと予想されます。国内で発生するバイオソリッドの約半分は、土壌改良に有益に利用されています。

- 米国では、バイオソリッドはリサイクルされるか、肥料として施用され、生産性の高い土壌を改善・維持し、植物の成長を促しています。下水汚泥を処理することで、バイオソリッドは埋立地やその他の処分場で場所を取る代わりに、貴重な肥料として利用されます。バイオソリッドの約半分は土地にリサイクルされています。

- 米国の人口増加に伴い、食糧需要は急速に伸びています。2022年には、米国の平均世帯の食料支出は約12.72%増加し、9,343米ドルとなりました。

- 農業部門の増加は、バイオソリッドの消費をさらに押し上げると予想されます。農業と関連産業は、2022年の米国の国内総生産(GDP)の約5.5%に寄与しています。

- したがって、上記の要因から、予測期間中は北米が最大の市場シェアを占めると予想されます。

バイオソリッド市場の産業概要

バイオソリッド市場は部分的に統合されています。主要企業(順不同)には、REMONDIS SE &Co.KG、Cambi ASA、FCC Group、Englobe、Cleanawayなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 北米における有害化学肥料からの置き換え

- 政府の厳しい排出規制

- その他の促進要因

- 抑制要因

- バイオソリッドに関する正しい知識と認識の欠如

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- タイプ

- クラスA

- クラスA EQ(エクセプショナル・クオリティ)

- クラスB

- 形態

- ケーキ

- 液体

- ペレット

- 用途

- 農地利用

- 人用作物生産用肥料/土壌改良剤

- 畜産用肥料-牧草地

- 非農地利用

- 森林作物(土地の修復と林業)

- 土地の埋め立て(道路と都市湿地)

- 鉱山跡地の埋め立て

- 造園、レクリエーション場、家庭内利用

- エネルギー回収エネルギー生産

- 熱生成、焼却、ガス化

- 石油とセメント生産

- 商業利用

- 農地利用

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析

- 主要企業の戦略

- 企業プロファイル

- Agrivert Ltd

- Aguas Andinas SA

- Alan Srl

- Allevi Srl

- BCR Environmental

- C.R.E.-Centro di Ricerche Ecologiche

- Cambi ASA

- Casella Waste Systems Inc.

- Cleanaway

- DC Water

- Eco-trass

- Englobe

- FCC Group

- Lystek International

- Merrell Bros. Inc.

- Parker Ag Services LLC

- Recyc Systems Inc.

- REMONDIS SE & Co. KG

- Saur

- SYLVIS

- Synagro Technologies

- Terrapure BR Ltd

- Walker Industries

第7章 市場機会と今後の動向

- アジア太平洋における汚泥治療への注目の高まり

- その他の機会

The Biosolids Market size is estimated at 34.28 million tons in 2025, and is expected to reach 40.71 million tons by 2030, at a CAGR of greater than 3.5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the biosolids market in 2020. However, the growing demand for biosolids on agricultural land has fueled overall industry growth since the pandemic.

Key Highlights

- One of the main things driving the market that was looked at is the need to replace dangerous chemical fertilizers and strict emission laws in many countries around the world.

- On the other hand, contradictory information about biosolids that is available to the public is expected to slow the growth of the market studied.

- The rising focus on sludge treatment in the Asia-Pacific, mainly in China and India, is anticipated to offer new avenues for industry growth shortly.

- North America dominated the biosolids market due to government and public support for environmental-friendly technologies.

Biosolids Market Trends

Agricultural Land Application to Dominate the Market

- Biosolids can be used on agricultural land, in forests, on rangelands, or in disturbed land needing reclamation.

- In terms of consumption, agricultural land applications consume the most biosolids. Consistent population growth across Asia-Pacific and North America is expected to augment the need for agricultural yields, which may positively affect the consumption of biosolids in the sector.

- According to the International Grains Council, in FY 2021-2022, the total grain production globally was about 2,294 million metric tons, about 3.05% more than the previous year. Furthermore, as per the council's estimation in FY 2022-2023, the total global grain production will decrease to 2,267 million metric tons. However, it is anticipated to reach 2,310 in FY 2023-2024.

- China accounts for about 7% of the overall crop production globally, thus feeding 22% of the world's population. The country is the largest producer of different crops, including rice, cotton, potatoes, and other crops.

- According to the Third Advance Estimates for crop production by the Ministry of Agriculture and Farmers Welfare, total foodgrain production in the country in 2022-23 was valued at 330.5 million tonnes (MT) from 315.6 MT.

- Scientists and farmers are looking for new technologies to increase the productivity of crops and meet the food demand arising from disproportionate population growth. In addition, there has been a decrease in the total available cropland area in countries such as the United States over the last decade.

- Biosolids can be effectively used as fertilizers and soil conditioners for human crop production. These are usually incorporated into the soil with conventional farm equipment. They are also used as fertilizer for animal crop production.

- Big enterprises and farmers are increasingly making their presence felt in cattle farming and meat products. They are augmenting the demand for animal crop production, which is providing impetus to the application of biosolids as fertilizers for animal crop production. This has led to an increase in demand for biosolids in agricultural land applications.

- They also help reduce fertilizer costs and provide many micronutrients for crop growth. The increasing world population is expected to give rise to a growing need for agriculture, which may impact the use of biosolids in the sector.

- Hence, agricultural land application is expected to dominate the market studied during the forecast period.

North America to Dominate the Market

- North America dominated the market owing to the government and public support for environmental-friendly technologies in countries such as the United States and Canada.

- In the United States, the biosolids market is mostly driven by the fact that both the government and the public want to use technologies that are good for the environment.

- The US EPA adopted the name "biosolids" to differentiate high-quality treated sewage sludge from raw sewage sludge, which contains large amounts of pollutants.

- There are two ways to get rid of biosolids from wastewater that cannot be used again (like putting them in a landfill) and ways to use them in a good way (like landfilling with biogas and energy recovery).

- Biosolids are generated during wastewater treatment processes and are extensively used to satisfy the US EPA's 40 CFR Part 503 regulations.

- The majority of the biosolids that are currently generated in the country are expected to be EQ or PC biosolids containing low levels of pollutants. About half of the biosolids produced in the country are being beneficially used to improve soils.

- In the United States, biosolids are either recycled or applied as fertilizer to improve and maintain productive soils and stimulate plant growth. By treating sewage sludge, the biosolids are used as valuable fertilizer instead of taking up space in a landfill or other disposal facility. Approximately half of all biosolids are recycled to land.

- The demand for food is growing rapidly with the rising population in the United States. In 2022, the average household spending in the United States on food increased by about 12.72% and was valued at USD 9,343.

- The rising agriculture sector is expected to further boost the consumption of biosolids. Agriculture and related industries contributed to about 5.5% of the US gross domestic product (GDP) in 2022.

- Therefore, due to the above factors, North America is anticipated to have the largest market share during the forecast period.

Biosolids Market Industry Overview

The biosolids market is partially consolidated in nature. The major players (not in any particular order) include REMONDIS SE & Co. KG, Cambi ASA, FCC Group, Englobe, and Cleanaway, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Replacing Hazardous Chemical Fertilizers in North America

- 4.1.2 Stringent Government Emission Laws

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Lack of Proper Knowledge and Awareness on Biosolids

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Class A

- 5.1.2 Class A EQ (Exceptional Quality)

- 5.1.3 Class B

- 5.2 Form

- 5.2.1 Cakes

- 5.2.2 Liquid

- 5.2.3 Pellet

- 5.3 Application

- 5.3.1 Agriculture land Application

- 5.3.1.1 Fertilizer/Soil Conditioner for Human Crop Production

- 5.3.1.2 Fertilizer for Animal Crop Production - Pastures

- 5.3.2 Non-agricultural Land Application

- 5.3.2.1 Forest Crops (Land Restoration and Forestry)

- 5.3.2.2 Land Reclamation (Roads and Urban Wetlands)

- 5.3.2.3 Reclaiming Mining Sites

- 5.3.2.4 Landscaping, Recreational Fields, and Domestic Use

- 5.3.3 Energy Recovery Energy Production

- 5.3.3.1 Heat Generation, Incineration, and Gasification

- 5.3.3.2 Oil and Cement Production

- 5.3.3.3 Commercial Uses

- 5.3.1 Agriculture land Application

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Agrivert Ltd

- 6.4.2 Aguas Andinas SA

- 6.4.3 Alan Srl

- 6.4.4 Allevi Srl

- 6.4.5 BCR Environmental

- 6.4.6 C.R.E. - Centro di Ricerche Ecologiche

- 6.4.7 Cambi ASA

- 6.4.8 Casella Waste Systems Inc.

- 6.4.9 Cleanaway

- 6.4.10 DC Water

- 6.4.11 Eco-trass

- 6.4.12 Englobe

- 6.4.13 FCC Group

- 6.4.14 Lystek International

- 6.4.15 Merrell Bros. Inc.

- 6.4.16 Parker Ag Services LLC

- 6.4.17 Recyc Systems Inc.

- 6.4.18 REMONDIS SE & Co. KG

- 6.4.19 Saur

- 6.4.20 SYLVIS

- 6.4.21 Synagro Technologies

- 6.4.22 Terrapure BR Ltd

- 6.4.23 Walker Industries

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Focus on Sludge Treatment in Asia-Pacific

- 7.2 Other Opportunities