|

|

市場調査レポート

商品コード

1189951

自動車用インフォテインメントシステム市場- 成長、動向、予測(2023年~2028年)Automotive Infotainment Systems Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 自動車用インフォテインメントシステム市場- 成長、動向、予測(2023年~2028年) |

|

出版日: 2023年01月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

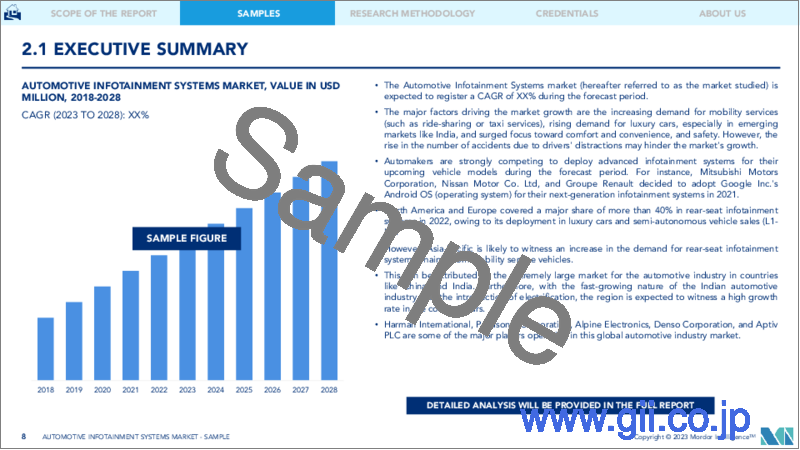

現在、自動車用インフォテインメントシステム市場は245億4000万米ドルで、予測期間中にCAGR6.76%を記録し、366億米ドルに達すると予想されています。

自動車用インフォテインメントシステム市場は、主に自動車の販売台数と生産台数の増加によって牽引されているため、COVID-19の大流行が市場に与える影響は避けられないものでした。製造装置の施錠や停止が続いたため、2020年には自動車の生産と販売が低迷しました。しかし、2020年前半には、世界の自動車生産と販売はペースを取り戻し始め、2021年も成長の勢いを維持しました。2021年の世界の自動車販売台数は、2020年と比較してかなりの伸びを示しました。しかし、主に世界の半導体不足により、市場は2019年の水準まで回復しなかっています。パンデミック後、プレイヤーはパンデミックの影響を克服するために、協力し合い、新しい革新的な製品を開発しています。例えば、以下のようなものです。

主なハイライト

- 2022年9月、ルネサスエレクトロニクス株式会社(以下、ルネサス)は、ベトナムの新興自動車メーカーであるVinFast社と電気自動車の技術開発で協業を拡大すると発表しました。両社はインフォテインメントシステムで協業しており、ルネサスはVinFastの電気SUV「VF8」「VF9」に同社の車載SoC「R-Car」とアナログ製品を提供しています。

自動車メーカーは、予測期間中に発売する車種に先進的なインフォテインメントシステムを展開するため、強い競争を行っています。例えば、三菱自動車工業、日産自動車、Groupe Renaultは、次世代インフォテインメントシステムにGoogle Inc.のAndroid OS(オペレーティングシステム)を採用しています。また、IVI(In-Vehicle Infotainment)の需要は、消費者行動の変化や携帯電話とシステムのシームレスな接続に対する要求により、急拡大すると予想されます。

高級車の販売台数の増加や、インダッシュ型インフォテインメントシステムに対する顧客の嗜好は、市場の大きな促進要因の一つとなっています。しかし、促進要因の注意力散漫による事故件数の増加も、市場の成長を阻害する要因になりかねません。世界の主要自動車メーカーは、オーディオユニット、ディスプレイユニット、ナビゲーションシステム、総合システムなどの領域で活躍する技術系OEMと幅広く連携しています。例えば

主なハイライト

- 2022年10月、トヨタとGoogle Cloudは、トヨタとレクサスの次世代オーディオマルチメディアシステムに加え、Google CloudのAIベースの音声サービスにも提携を拡大しました。顧客は、トヨタカローラ、タンドラ、セコイア、レクサス NX、RX、オール電化車RZなどの2023年モデルに搭載される最新世代のトヨタオーディオマルチメディアおよびレクサスインターフェースインフォテインメントシステムで、この協業の最初の成果を見ることができます。

さらに、商用車にナビゲーションや車両制御ユニットを導入することで、緊急時の対応時間を短縮し、事故のリスクをなくすことができます。さらに、いくつかの自動車メーカーが低価格のインフォテインメントシステムを提供しているため、製品の購入しやすさが向上しています。さらに、スマートフォンの普及が進んでいることと、インターネットへの接続性が高いことが、世界レベルでの市場成長に大きな影響を与えています。

予測期間中は、北米と欧州に次いで、アジア太平洋地域の市場が急速に成長すると予想されます。アジア太平洋市場の拡大は、世界で最も多くの自動車を製造している中国、日本、インドなどの国々で、自動車用インフォテインメントシステムの採用率が高いことに起因しています。このため、自動車用インフォテインメントシステムのサプライチェーン全体において技術革新が進んでいます。例えば、以下のようなものがあります。

主なハイライト

- 2022年8月、ローム(Rohm)は、インフォテインメントシステムやADAS(先進運転支援システム)の車載カメラ向けDC/DCコンバータIC「BD9S402MUF-C」の開発を発表しました。

主な市場動向

インフォテインメントシステムの高度化の進展

車載インフォテインメントシステムへのスマートフォン機能の搭載が進んでいます。北米・欧州では成人の90%以上が携帯電話からインターネットにアクセスしており、これは他の地域と比べても高い割合です。携帯電話の利用が増えるにつれて、同じ目的でスマートフォンを自動車に搭載する動きも出てきました。

自動車メーカーも、ハードウェアのモジュール設計を選択するようになっています。これにより、インフォテインメントシステムを購入する際のコストを下げることができます。スマートフォンの機能を車載インフォテインメントシステムに低コストで組み込むための技術開発が進んでいます。メーカー各社は、処理能力とシステム競争力の両立に取り組んでいます。自動車メーカーがコネクテッドカーの性能を向上させるためには、デジタルサービスによって膨大なデータが発生します。

- 2021年8月、現代自動車は現代、起亜、ジェネシスのヒューマンマシンインターフェース(HMI)技術パートナーとして、世界のソフトウェア技術企業であるQTを選定しました。この技術により、現代自動車は車両インフォテインメントシステム全体でコネクテッド・カー・オペレーティング・システムを開発することができるようになります。

- 2021年9月、LG電子はドイツ・ミュンヘンで開催されたIAA Mobilityheldで車載インフォテインメントシステムを発表しました。車載インフォテインメントシステムは、Google Android automotiveとAndroid 10をベースに、コネクティビティと利便性を最適化したものでした。車載インフォテインメントシステムのソフトウェアは、ルノーのパートナーシップにより開発され、2022年2月に発売されたルノーメガーヌ E-TECHエレクトリックに搭載されました。

車載インフォテインメントシステムは、大規模な技術的変革を迎えています。スマートフォンの普及に伴い、ADASや自律走行技術(自動運転車)の採用が進んでいます。オートモーティブシステム車のような技術、特に助手席の技術は、過度に身近なものとなっています。エンジニアが革新的なバージョンの車載インフォテインメントシステムを開発するにつれ、これらの機能は自動車の電子システムに不可欠な貢献者になるでしょう。

AIとクラウドサービスの導入は、車載インフォテインメントシステムの技術的進歩を促進すると予想されます。ほとんどの企業は、インフォテインメントシステムを既存のGoogleとAppleのエコシステムに依存しています。一部のプレイヤーは、インフォテインメントシステムのOSを自社開発することを好みます。

中国がアジア太平洋市場を牽引

中国は過去10年間、自動車販売台数が最も多かったため、アジア太平洋地域の自動車産業の中で大きなシェアを占めています。自動車メーカーによる新エネルギー車(NEV)への注目が高まっていることから、予測期間中も引き続き自動車販売台数はプラスになると予想されます。

シンプルなオーディオシステムから、ナビゲーション、Apple CarPlay、Android Auto、テレマティクスなどの複数の機能をサポートするタッチスクリーンインフォテインメントシステムへの移行が、同国におけるインフォテインメントシステムの需要を促進しています。

中国は世界最大級の自動車市場であり、2020年の中国国内での乗用車販売台数は2,017万台を超え、2021年には中国全体の自動車販売台数は約2,148万台となりました。しかし、中国の自動車メーカーは、インテリジェント・コックピットの開発を先駆的に進めており、急速に現代の運転体験に不可欠な要素になりつつあります。インテリジェント・コックピットは、スマートテクノロジーと、車両コマンドの音声認識やエンターテインメント、ナビゲーションシステムなどのさまざまな運転機能を組み合わせたものです。例えば

- 2022年9月、NVIDIA Corporation(以下、NVIDIA)は、自律走行/ADAS(先進運転支援システム)と車載インフォテインメントシステムを統合できる車載用集中型コンピュータ「ドライブソア」の開発を発表しています。

さらに、2021年7月の世界人工知能会議では、インテリジェントコックピット関連の特許出願件数が82,300件を超え、中国の自動車市場がトップ、次いで日本が31,900件、米国が19,300件となりました。インテリジェントコックピットは、現代の運転体験において重要な技術になりつつあり、音声認識や複数の駆動機能を持つナビゲーションシステムは、インテリジェントカーのコックピットに統合される主要技術の一つです。

その他の特典。

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- 産業の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション(市場規模:10億米ドル)

- 車載タイプ別

- インダッシュ型インフォテインメント

- リアシートインフォテイメント

- 車種別

- 乗用車

- 商用車

- 地域別情報

- 北米

- 米国

- カナダ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- ブラジル

- 南アフリカ共和国

- その他の国

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Denso Corporation

- Robert Bosch GmbH

- Continental AG

- Harman International Industries Inc.

- Magnetic Marelli SpA

- Kenwood Corporation

- Alpine Electronics Inc.

- Mitsubishi Electric Corporation

- Visteon Corporation

- Pioneer Corporation

- Aptiv PLC

第7章 市場機会と今後の動向

Currently, The Automotive Infotainment Systems market is valued at USD 24.54 billion, and it is expected to reach USD 36.60 billion, registering a CAGR of 6.76% during the forecast period.

The impact of the COVID-19 pandemic on the automotive infotainment systems market was inevitable as the market is primarily driven by increasing vehicle sales and production. As there were continuous lockdowns and shutting down of manufacturing units, production and sales of vehicles experienced a slump in 2020. However, in the first half of 2020, global vehicle production and sales started to pick up the pace and continued their growth momentum in 2021. Global vehicle sales witnessed considerable growth in 2021 when compared to 2020. However, the market did not rebound to the levels of the year 2019, primarily due to the global semiconductor shortage. Post-pandemic, players are collaborating and developing new and innovative products to overcome the impact of the pandemic. For instance,

Key Highlights

- In September 2022, Renesas Electronics Corporation (Renesas) announced an expansion of its collaboration with VinFast, a Vietnamese emerging vehicle manufacturer, for the technological development of electric vehicles. Both companies have worked together on infotainment systems, and Renesas provides R-Car, its onboard SoC, and analog products for the VinFast electric SUVs VF8 and VF9.

Automakers are strongly competing to deploy advanced infotainment systems for their upcoming vehicle models during the forecast period. For instance, Mitsubishi Motors Corporation, Nissan Motor Co. Ltd, and Groupe Renault have adopted Google Inc.'s Android OS (operating system) for their next-generation infotainment systems. In addition, demand for IVI (In-Vehicle Infotainment) is expected to witness a steep rise with changing consumer behavior and demand for seamless connectivity of phones with the system.

An increase in luxury vehicle sales and customer preference for in-dash infotainment systems are some of the biggest drivers of the market. However, the rise in the number of accidents due to driver distraction may also hinder the market's growth. The world's leading automobile manufacturers are extensively working with technological OEMs, which work in domains such as audio units, display units, navigation systems, and comprehensive systems. For instance,

Key Highlights

- In October 2022, Toyota and Google Cloud expanded their partnership to include Toyota and Lexus's next-generation audio multimedia systems as well as Google Cloud's AI-based speech services. Customers can see the first fruits of the collaboration in the latest generation Toyota Audio Multimedia and Lexus Interface infotainment systems, which will be available in 2023 models such as the Toyota Corolla, Tundra, and Sequoia, as well as the Lexus NX, RX, and all-electric RZ.

Furthermore, implementing navigation and vehicle control units in commercial vehicles helps reduce the response time during emergencies, thereby eliminating the risk of accidents. Besides this, several automobile manufacturers are also offering low-cost infotainment systems, thereby increasing product affordability. Additionally, the rising adoption of smartphones, along with high internet connectivity, has a significant impact on the market growth on a global level.

The Asia-Pacific market is expected to grow rapidly during the forecast period, followed by North America and Europe. The Asia-Pacific market's expansion can be attributed to the high adoption rate of automotive infotainment systems in countries such as China, Japan, and India, which manufacture the most vehicles globally. This, in turn, is driving technological innovations across the supply chain of the automotive infotainment system. For instance,

Key Highlights

- In August 2022, Rohm Co., Ltd (Rohm) announced the development of the BD9S402MUF-C DC/DC converter IC for infotainment systems and advanced driver assistance system onboard cameras.

Key Market Trends

Growing Advancements in Infotainment Systems

Smartphone functions are increasingly being integrated into in-vehicle infotainment systems. Over 90% of adults in North America and Europe have access to the internet via their mobile phones, which is one of the highest rates among other regions. As the use of mobile phones has increased, so has the use of smartphones in cars for the same purposes.

Automobile manufacturers are also opting for modular hardware design. This allows them to lower the cost of purchasing infotainment systems. They are developing technologies that allow smartphone functions to be integrated into in-vehicle infotainment systems at a low cost. Manufacturers are working to combine processing power and system competitiveness. For car manufacturers to improve the performance of connected vehicles, digital services generate massive amounts of data.

- In August 2021, Hyundai Motors selected QT, a global software technology company, as its human-machine interface (HMI) technology partner for Hyundai, Kia, and Genesis. This technology would allow Hyundai Motors to develop a connected car operating system across its vehicle infotainment systems.

- In September 2021, LG Electronic unveiled their in-vehicle infotainment system in IAA Mobilityheld in Munich, Germany. The in-vehicle infotainment system was based on Google Android automotive and Android 10 to optimize connectivity and convenience. The in-vehicle infotainment system's software was developed with Renault's partnership, and it is equipped with the Renault Megane E-TECH electric, launched in February 2022.

The automotive infotainment system is undergoing massive technological transformations. With growing smartphone usage, there is an increase in the adoption of ADAS and Autonomous driving technology (self-driving cars). Technologies like Automotive systems vehicles, especially for passenger seating, have become excessively familiar. As engineers develop innovative versions of in-vehicle infotainment systems, these features will become essential contributors to the vehicle's electronic system.

The introduction of AI and cloud services is expected to drive technological advancements in automotive infotainment systems. Most companies rely on the existing Google and Apple ecosystems for their infotainment systems. Although some players prefer to develop their infotainment system OS in-house,

China is Driving the Asia-Pacific Market

China occupied a significant share of the Asia-Pacific automotive industry among Asia-Pacific countries due to its highest vehicle sales over the past decade. The country is anticipated to continue to see positive vehicle sales during the forecast period, owing to the growing focus on new energy vehicles (NEV) among automakers.

The shift from simple audio systems to touchscreen infotainment systems that support multiple features, such as navigation, Apple CarPlay, Android Auto, and telematics, is driving the demand for infotainment systems in the country.

China is one of the world's largest automotive markets, with over 20.17 million passenger cars sold in the country in 2020, and overall car sales in China reached around 21.48 million vehicles in 2021. However, Chinese automakers are pioneering the development of the intelligent cockpit, which is quickly becoming an essential component of the modern driving experience. Intelligent cockpits combine smart technologies with various driving functions, such as voice recognition for vehicle commands and entertainment and navigation systems. For instance,

- In September 2022, NVIDIA Corporation (NVIDIA) announced the development of Drive Soar, a centralized in-vehicle computer capable of integrating autonomous driving/advanced driver assistance systems (ADAS) and in-vehicle infotainment systems.

Further, In July 2021, World artificial intelligence conference, China's automobile market was leading in the development of smart cockpits with more than 82,300 patents application related to intelligent cockpits, followed by Japan and the United States at 31,900 and 19,300, respectively. Intelligent cockpits are becoming a critical technology in the modern driving experience; voice recognition and multiple drive functions navigation systems are some of the prime technologies integrated into intelligent vehicle cockpits.

Competitive Landscape

Major players such as Robert Bosch, Alpine Electronics, Panasonic Corporation, HARMAN International, and Mitsubishi Electric Corporation dominate the automotive infotainment systems market. These companies have strong distribution networks at a global level and offer an extensive product range. These companies adopt strategies such as new product developments, collaborations, and contracts and agreements to sustain their market positions.

- In September 2022, Mercedes-Benz AG and Qualcomm Technologies, Inc. announced a collaboration to use Snapdragon Digital Chassis solutions to bring the most advanced digital capabilities to future Mercedes-Benz vehicles. Mercedes-Benz is using Qualcomm Cockpit Platforms to power intuitive and intelligent infotainment systems. These next-generation systems will include highly intuitive AI experiences for in-car virtual assistance.

- In June 2022, Mercedes-Benz Group AG announced a collaboration with ZYNC, a California-based technology company. Under this partnership, the latter company will provide a premium in-car digital entertainment platform for the OEM.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in USD Billion)

- 5.1 By Installation Type

- 5.1.1 In-dash Infotainment

- 5.1.2 Rear-seat Infotainment

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 South Africa

- 5.3.4.3 Other Countries

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Denso Corporation

- 6.2.2 Robert Bosch GmbH

- 6.2.3 Continental AG

- 6.2.4 Harman International Industries Inc.

- 6.2.5 Magnetic Marelli SpA

- 6.2.6 Kenwood Corporation

- 6.2.7 Alpine Electronics Inc.

- 6.2.8 Mitsubishi Electric Corporation

- 6.2.9 Visteon Corporation

- 6.2.10 Pioneer Corporation

- 6.2.11 Aptiv PLC