|

市場調査レポート

商品コード

1690936

シングルユースバイオプロセシングプローブおよびセンサー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Single-Use Bioprocessing Probes And Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シングルユースバイオプロセシングプローブおよびセンサー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 153 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

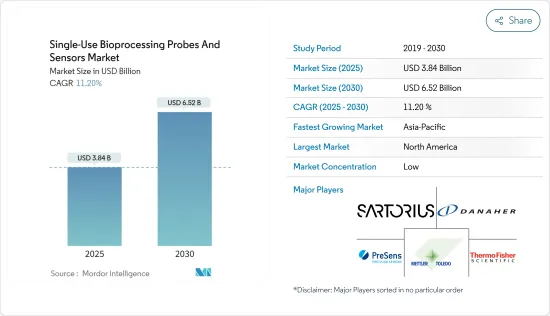

シングルユースバイオプロセシングプローブおよびセンサー市場規模は2025年に38億4,000万米ドルと推定・予測され、2030年には65億2,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは11.2%です。

COVID-19の大流行は、普及と収益成長の面で市場に大きな恩恵をもたらしました。パンデミックは、治療薬やワクチン製造の技術需要を満たすために、センサーを含むシングルユースソリューションの適用を加速させました。例えば、American Pharmaceutical Review誌が2023年4月に発表したデータによると、パンデミックの間、世界中で生物製剤やワクチンの製造のためにシングルユースバイオプロセシングシステムの需要が急増しました。また、商業規模のシングルユースバイオプロセシングシステムの採用がCOVID-19中に顕著に増加し、2019年の32.5%から2022年には43%に増加したことが観察されました。この増加は、パンデミック危機時のバイオ生産の柔軟性と迅速な展開に対する需要に一因があります。したがって、パンデミック時にシングルユースバイオプロセシングシステムの採用が増加したことで、市場成長が大幅に改善しました。

ステンレス製バイオプロセス製品に対する商業的優位性や、シングルユースバイオプロセシング施設拡張のための投資増加などの要因が、予測期間中の市場成長を促進すると予想されます。

シングルユースバイオプロセシング施設の拡張に対する企業による多額の投資は、市場成長を促進する主な要因です。例えば、2022年2月、サーモフィッシャーサイエンティフィック社は、米国ペンシルバニア州ミラーズバーグにあるシングルユースバイオプロセシング技術製造施設を拡張するために4,000万米ドルを投資しました。この拡張は、柔軟性、拡張性、信頼性の高いシングルユースバイオプロセシング生産能力を提供する同社の能力を強化するための6億5,000万米ドルの複数年投資の一環でした。このように、シングルユースバイオプロセシング施設の拡張に対する多額の投資により、シングルユースバイオプロセシング用プローブおよびセンサーの使用量が増加し、調査期間中の市場成長が促進されると予想されます。

さらに、市場プレーヤーは市場シェア拡大のために買収や提携など様々な戦略的取り組みを行っており、これが調査期間中の市場成長を押し上げると予想されます。例えば、2021年3月、メトラー・トレドは、シングルユースバイオプロセスプローブおよびセンサー市場での存在感を高めるために、シングルユースセンサーの主要サプライヤーの1つであるPendoTECH社を買収しました。この両社の統合は、バイオプロセス業界で利用可能な包括的なセンサーの提供を通じて、顧客の経験を向上させることを目的としています。このように、シングルユースバイオプロセス設備の拡張のための新規投資や市場プレイヤーの戦略など、上記の要因が予測期間中の市場成長を促進すると予想されます。

しかし、環境面や技術面での課題は、予測期間中の市場成長を抑制する可能性が高いです。

シングルユースバイオプロセシングプローブおよびセンサー市場動向

予測期間中、pHセンサーセグメントが市場の主要シェアを占める見込み

シングルユースpHセンサーは、バイオ医薬品製造におけるpH測定のためにシングルユースプロセスに組み込むための、工場で校正されガンマ線滅菌可能なセンサーです。pHセンサセグメントは、使用量と入手可能性の点で製品の普及率が最も高いため、予測期間中に大きなシェアを占めると予想されます。

シングルユースpHセンサーの技術的進歩の高まりは、これらのセンサーの需要をさらに増加させ、それによって市場成長を促進すると予測されています。例えば、2021年10月のBiopharmaceutical Applicationsに掲載されたシングルユースpHセンサに関する記事によると、シングルユースpHセンサの進歩により、品質、信頼性、サプライヤサポートのレベルが向上しています。したがって、この進歩により、pHセンサはバイオプロセスのシングルユースアプリケーションに品質と精度を提供するようになりました。

さらに、2023年1月にPharmaceutical Bioprocessing Journalに掲載された研究によると、pHプローブはバイオプロセスのモニタリングと制御に最も頻繁に使用される電気化学センサーの一つです。したがって、バイオリアクターでのpHセンサーの使用傾向が高いことが、予測期間中の市場成長を促進すると予想されます。

予測期間中、北米が市場で最大のシェアを占める見込み

米国は、バイオ製薬部門が確立されており、地域のマーケットリーダーが提供するシングルユースプローブ・センサーが広く利用可能であることから、シングルユースバイオプロセシングプローブおよびセンサーー市場で大きなシェアを占めています。さらに、米国政府によるバイオプロセス産業支援のための投資の増加と、バイオプロセシングプローブおよびセンサーの採用の増加が、予測期間中の市場成長をさらに促進すると予想されています。

米国におけるバイオ医薬品分野への投資の増加は、予測期間中の市場成長をさらに促進すると期待されています。例えば、保健福祉省が2022年9月に発表したファクトシートによると、政府は、医薬品有効成分(API)、抗生物質、必須医薬品の製造に必要な主要出発材料のバイオ製造の役割を拡大するために4,000万米ドルの投資を計画しています。したがって、米国のこのような投資活動は、シングルユースバイオプロセシングプローブおよびセンサー市場の成長にプラスの影響を与える可能性が高いです。

さらに、2022年11月、カーディナル・ヘルスはフロリダ州リバービューにあるシングルユース機器の再処理施設を拡張し、その容量は100,000平方フィートとなりました。したがって、市場プレーヤーによるこのような戦略的拡張のおかげで、シングルユースプローブとセンサーの再処理需要は増加し、それによって予測期間中の市場成長を促進する可能性が高いです。

シングルユースバイオプロセシングプローブおよびセンサー産業概要

シングルユースバイオプロセシングプローブおよびセンサー市場は細分化されており、大企業から中小企業まで複数の企業が参入しています。現在市場を独占している企業には、Thermo Fisher Scientific Inc.、Sartorius AG、Danaher Corporation(Cytiva)、PreSens Precision Sensing GmbH、METTLER TOLEDO(PendoTECH)、Hamilton Companyなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ステンレス製バイオプロセス製品に対する商業的優位性

- シングルユースバイオプロセシング施設拡張のための投資増加

- 市場抑制要因

- 環境および技術的課題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- pHセンサー

- 酸素センサー

- 圧力センサー

- 温度センサー

- 導電率センサー

- 流量計とセンサー

- その他のタイプ

- ワークフロー別

- アップストリーム

- ダウンストリーム

- エンドユーザー別

- バイオ医薬品メーカー

- CMOおよびCRO

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Thermo Fisher Scientific Inc.

- Sartorius AG

- Danaher Corporation(Cytiva)

- PreSens Precision Sensing GmbH

- METTLER TOLEDO(PendoTECH)

- Equflow BV

- Parker-Hannifin Corporation

- Broadley-James Corporation

- Dover Corporation(Malema Engineering Corporation)

- Hamilton Company

- CerCell AS

- Emerson Electric Co.

第7章 市場機会と今後の動向

The Single-Use Bioprocessing Probes And Sensors Market size is estimated at USD 3.84 billion in 2025, and is expected to reach USD 6.52 billion by 2030, at a CAGR of 11.2% during the forecast period (2025-2030).

The COVID-19 pandemic has significantly benefited the market in terms of adoption and revenue growth. The pandemic accelerated the application of single-use solutions, including sensors, to meet the technology demand for therapeutics and vaccine manufacturing. For instance, according to data published by the American Pharmaceutical Review in April 2023, there was a surge in demand for single-use bioprocessing systems during the pandemic for the production of biologics and vaccines around the world. It was also observed that the adoption of commercial-scale single-use bioprocessing systems grew appreciably during COVID-19, increasing from 32.5% in 2019 to 43% in 2022. The increase was partly due to the demand for flexibility and rapid deployment of bioproduction during the pandemic crisis. Thus, the increased adoption of single-use bioprocessing systems during the pandemic significantly improved the market growth.

Factors such as commercial advantages over stainless steel bioprocessing products and rising investment for single-use bioprocessing facility expansion are expected to drive market growth over the forecast period.

Significant investments by companies in the expansion of single-use bioprocessing facilities is a major factor driving the market growth. For instance, in February 2022, Thermo Fisher Scientific invested USD 40 million to expand its single-use bioprocessing technology manufacturing facility in Millersburg, Pennsylvania, United States. The expansion was part of a USD 650 million multi-year investment to enhance the company's ability to provide flexible, scalable, and reliable single-use bioprocessing production capacity. Thus, significant investments in the expansion of single-use bioprocessing facilities are expected to increase the usage of single-use bioprocessing probes and sensors, thus driving market growth over the study period.

Furthermore, market players are undertaking various strategic initiatives such as acquisitions and collaborations to increase the market share, which is expected to boost the market growth over the study period. For instance, in March 2021, Mettler Toledo acquired PendoTECH, one of the major suppliers of single-use sensors, to enhance its market presence in the single-use bioprocess probes and sensors market. This integration of both companies aimed at improving customers' experience through comprehensive sensor offerings available for the bioprocessing industry. Thus, the above-mentioned factors, such as new investments for the expansion of single-use bioprocessing facilities and market player strategies, are anticipated to drive market growth during the forecast period.

However, environmental and technical challenges are likely to restrain the market growth over the forecast period.

Single-Use Bioprocessing Probes And Sensors Market Trends

The pH Sensor Segment is Expected to have Major Share in the Market Over the Forecast Period

Single-use pH sensors are factory-calibrated and gamma-sterilizable sensors for integration into single-use processes for the measurement of pH in biopharmaceutical manufacturing. The pH sensor segment is expected to account for a significant share during the forecast period owing to the highest penetration of the product in terms of usage and availability.

The rising technological advancements in single-use pH sensors are further anticipated to increase the demand for these sensors, thereby driving market growth. For instance, according to an article published on single-use pH sensors in Biopharmaceutical Applications in October 2021, advancements in single-use pH sensors have improved quality, reliability, and the level of supplier support. Therefore, the advancements have led pH sensors to provide quality and accuracy for bioprocess single-use applications.

Furthermore, according to a study published in the Pharmaceutical Bioprocessing Journal in January 2023, a pH probe is among the most often used electrochemical sensors for bioprocess monitoring and control. Therefore, the high propensity of usage of pH sensors in the bioreactors is anticipated to drive the market growth over the forecast period.

North America is Expected to Have Largest Share in the Market Over the Forecast Period

The United States represents a significant share of the single-use bioprocessing probes and sensors market due to its well-established biopharmaceutical sector and widespread availability of single-use assemblies supplied by regional market leaders. Furthermore, an increase in investment by the US government to support the bioprocessing industry and a rise in the adoption of bioprocessing probes and sensors are further expected to promote market growth over the forecast period.

The rise in investment in the biopharma field in the United States is further expected to drive market growth over the forecast period. For instance, as per the fact sheet released in September 2022 by the Department of Health and Human Services, the government planned to invest USD 40 million to expand the role of biomanufacturing for active pharmaceutical ingredients (APIs), antibiotics, and the key starting materials needed to produce essential medications. Hence, such investment activities in the United States are likely to positively impact the growth of the single-use bioprocessing probes and sensors market.

Moreover, in November 2022, Cardinal Health expanded its single-use device reprocessing facility in Riverview, Florida, with a capacity of 100,000 square feet. Thus, owing to such strategic expansions by market players, the demand for reprocessing of single-use probes and sensors is likely to rise, thereby fueling the market growth over the forecast period.

Single-Use Bioprocessing Probes And Sensors Industry Overview

The single-use bioprocessing probes and sensors market is fragmented in nature, with several large to small and medium-sized players. Some companies currently dominating the market are Thermo Fisher Scientific Inc., Sartorius AG, Danaher Corporation (Cytiva), PreSens Precision Sensing GmbH, METTLER TOLEDO (PendoTECH), Hamilton Company, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercial Advantages Over Stainless Steel Bioprocessing Products

- 4.2.2 Rising Investment for Single-use Bioprocessing Facility Expansion

- 4.3 Market Restraints

- 4.3.1 Environmental and Technical Challenges

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type

- 5.1.1 pH Sensor

- 5.1.2 Oxygen Sensor

- 5.1.3 Pressure Sensors

- 5.1.4 Temperature Sensors

- 5.1.5 Conductivity Sensors

- 5.1.6 Flow Meters and Sensors

- 5.1.7 Other Types

- 5.2 By Workflow

- 5.2.1 Upstream

- 5.2.2 Downstream

- 5.3 By End User

- 5.3.1 Biopharmaceutical Manufacturers

- 5.3.2 CMOs and CROs

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Thermo Fisher Scientific Inc.

- 6.1.2 Sartorius AG

- 6.1.3 Danaher Corporation (Cytiva)

- 6.1.4 PreSens Precision Sensing GmbH

- 6.1.5 METTLER TOLEDO (PendoTECH)

- 6.1.6 Equflow BV

- 6.1.7 Parker-Hannifin Corporation

- 6.1.8 Broadley-James Corporation

- 6.1.9 Dover Corporation (Malema Engineering Corporation)

- 6.1.10 Hamilton Company

- 6.1.11 CerCell AS

- 6.1.12 Emerson Electric Co.