オフグリッドソーラーエネルギー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Off-Grid Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 2066631

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

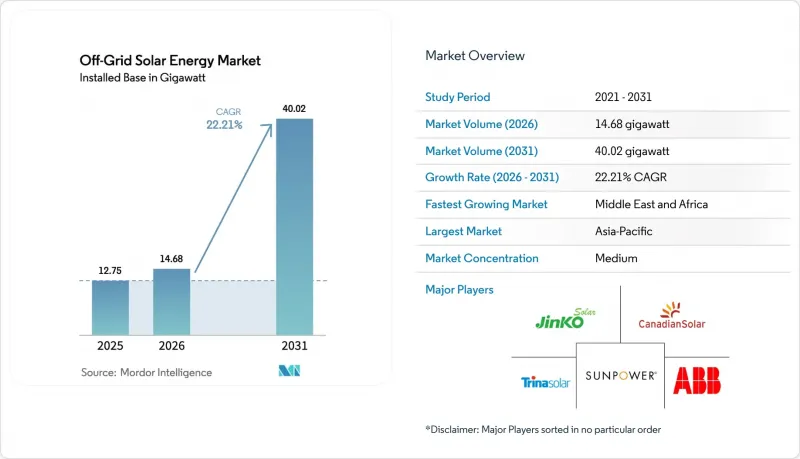

Mordor Intelligenceによると、オフグリッドソーラーエネルギー市場の規模(設置容量ベース)は、2025年の12.75ギガワットから2026年には14.68ギガワットへと拡大し、2026年から2031年にかけてCAGR22.21%で推移し、2031年には40.02ギガワットに達すると予測されています。

本レポートは、技術別(太陽光発電および集光型太陽光発電)、エンドユーザー別(ユーティリティ規模、商業・産業用、住宅用)、地域別(北米、欧州、アジア太平洋、南米、中東・アフリカ)に分類されています。市場規模および予測は、設置容量(GW)ベースで示されています。

世界のオフグリッドソーラーエネルギー市場の動向と洞察

太陽光発電モジュールの価格下落と効率の向上

2026年上半期、ポリシリコンの供給過剰により、中国のFOBモジュール価格は1ワットあたり0.12米ドル前後で推移しましたが、9%の輸出付加価値税還付が終了するとコストは安定し、銀価格の高騰により太陽電池セルの原材料コストが3~4%上昇しました。タンデム技術の革新により、こうした逆風は一部相殺されています。Oxford PVは2024年5月に効率27.3%のモジュールの生産を開始し、2029年までに7.5 GWの生産能力を目指しています。一方、LONGiは2024年4月に実験室での最高効率33.9%を達成しました。効率26%を超える商用モジュールは、2027年までにオフグリッドソーラーエネルギー市場に参入し、システム全体のコストを最大20%削減する可能性があります。LONGiの「Hi-MO 9」のような両面受光型モジュールは、すでに高アルベドの設置地において5~30%の追加発電量を確保しており、薄膜カドミウムテルル系太陽電池は、テルルの供給不足により世界生産量が10GWを下回っているため、依然としてニッチな存在にとどまっています。しかし、ペロブスカイト太陽電池の耐久性や鉛含有量に関する課題は未解決であり、IEC 61215規格の改正により、認証取得に12~18ヶ月の遅れが生じる可能性があります。

高まる農村電化目標

「ミッション300」は、ナイジェリアのDARESプログラムだけで18億5,000万米ドルを動員し、1,350のミニグリッドを統合して1,750万人に電力を供給しています。インドのPM-KUSUMは30.8 GWの目標を設定しましたが、2024年半ば時点で2.8 GWにとどまっています。これは、信用力の低い州において、農家が負担する自己負担金が40~50%に上ったため、導入が停滞したためです。国際太陽エネルギー同盟(ISA)の試算によると、電化されていない3億9,600万人のうち59%はミニグリッドによる供給の方が適しているもの、資金調達ギャップは現在の資本流入額の49倍に上ります。インドネシアの電化されていない2,500の村は、「ラストマイル」のリスクを如実に示しています。PLN(インドネシア電力公社)が設定したkWhあたり0.15米ドルの料金上限により、内部収益率(IRR)が8%を下回ってしまい、政府の支援がない民間入札者を遠ざけています。

大規模システムにおける高額な初期設備投資(CAPEX)

通信ハイブリッドシステムには2万~6万米ドルが必要ですが、ナイジェリアの通信塔については、リスク保証によって金利が300~400ベーシスポイント引き下げられない限り、現地通貨建て債務の金利が依然として12%を超える状況にあります。インドでは、PM-KUSUMコンポーネントAにより、農家の40~50%の共同出資が義務付けられています。信用普及率が30%未満の州では、非公式な18~24%の金利の融資に頼らざるを得ず、これがプロジェクトのIRRを低下させています。ナイジェリア全土のミニグリッド開発業者は、2025年初頭時点で16億米ドルのパイプラインのうちわずか15%についてのみファイナンシャル・クローズを達成しました。これは、貸し手が25%の自己資本IRRを求めているためです。

セグメント分析

2025年には太陽光発電(PV)が設備容量の100%を占め、オフグリッドソーラーエネルギー市場全体の規模の推移を反映しています。集光型太陽光発電(CSP)は、最低10 MWの規模が必要であり、溶融塩蓄熱コストが1 kWhあたり50~80米ドルであるため、オフグリッドソーラーエネルギー市場が活況を呈している50 kW~5 MWの範囲では依然として採算が取れません。予測期間中、2027年までに銀行融資の条件を満たすようになるペロブスカイト・シリコンタンデムセルは、総設置コストを20~30%削減し、ミニグリッド全体の投資回収期間を短縮する可能性があります。両面受光型モジュールはすでに発電量を5~30%向上させており、特にアルベドの高いサヘル地域において、オフグリッドソーラーエネルギー市場における両面受光型モジュールの出荷シェアを拡大しています。しかし、鉛に関連する認証上のハードルがペロブスカイト技術の導入を遅らせ、短期的な成長を抑制する可能性があります。

LFP(リン酸鉄リチウム)電池の価格が継続的に下落していることは、モジュールの効率向上と相まって、オフグリッドソーラーエネルギー市場を急勾配の学習曲線上に維持しています。薄膜カドミウムテルル系太陽電池はテルル供給の制約を受けているため、結晶系およびタンデム型太陽光発電が引き続き出荷量の大部分を占める見込みです。2024年にEnphase社が発売した、グリッド形成機能を備えたエッジ・オブ・グリッド型マイクロインバーターは、単価が1ワットあたり0.25米ドルを超え、接続要件が農村部のネットワークに負担をかけるため、オフグリッドの標準仕様というよりは、グリッド接続型の機能として留まる可能性が高いでしょう。

地域別分析

2025年、アジア太平洋地域はオフグリッドソーラーエネルギー市場において59.87%の容量シェアを占め、市場を席巻しました。しかし、インドの「PM-KUSUM」計画は、2024年半ば時点で30.8 GWという目標のわずか9%しか達成できておらず、豊富な潜在能力があるにもかかわらず、行政手続きの遅れが顕著です。インドネシアの2,500の未電化村落は、政府保証がない場合、内部収益率(IRR)が8%未満に低下することを浮き彫りにしており、これが民間による建設拡大を制約しています。フィリピンは2027年までに全世帯の電化率100%を目標としており、1kmあたりの延伸コストが1万米ドルを超える地域ではミニグリッドに重点を置いていますが、土地所有権をめぐる紛争により、導入までのリードタイムが18ヶ月以上に及んでいます。

中東・アフリカ地域は、世界のオフグリッドソーラーエネルギー市場を上回るCAGR26.3%を記録すると予測されています。ナイジェリアのDARESは、1,350のミニグリッドを展開するために18億5,000万米ドルを調達しており、その一部は付帯サービス収入を得るために系統連系型となっています。ケニアのPAYGoの主要企業は、2025年に100万システムの導入に向けて1億5,600万米ドルを確保した一方、Amea Powerなどの湾岸諸国の投資家は、2027年に稼働開始予定のコートジボワールにおける50MWの発電所へ資金を提供しました。為替相場の変動は依然として主要な足かせとなっています。2024年のナイラ68%安により、d.light社はマルチカレンシー債を通じてヘッジを余儀なくされ、発行スプレッドに150~200ベーシスポイントが上乗せされました。

北米、欧州、南米を合わせても、ほぼ全域に電力網が整備されているため、オフグリッドソーラーエネルギー市場の規模に占める割合は15%未満にとどまっています。カナダは、遠隔地の先住民コミュニティ292カ所におけるディーゼル発電の代替に3億カナダドルを投じましたが、北極圏の緯度のため太陽光発電の稼働率が8~12%に低下し、普及のペースが鈍化しています。ブラジルにおける2023年のネットメータリング制度の見直しにより、2024年の分散型太陽光発電の成長は40%縮小しました。一方、アルゼンチンではペソの切り下げにより、RenovArのパイプラインが凍結されました。欧州での限られた需要は、ディーゼル価格による裁定取引が成立する島嶼部や高地の観光施設に集中しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストによるサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 太陽光発電モジュールの価格下落と効率の向上

- 農村電化目標の引き上げ

- リチウムイオン電池のコスト曲線の低下

- Pay-Goとフィンテックの連携により、手頃な価格を実現

- ESG連動型債務による資本コストの低減

- 電力会社によるミニグリッド入札のバンドリング

- 市場抑制要因

- 大規模システムにおける初期設備投資(CAPEX)の高さ

- 断続的な政策支援/補助金削減

- アーリーアダプター世帯の飽和

- 中古パネルのダンピングが品質への信頼を損なっている

- サプライチェーン分析

- 規制状況と政府の政策

- 技術展望(次世代ペロブスカイト、AIを活用した運用・保守(O&M)など)

- ポーターのファイブフォース

第5章 市場規模と成長予測

- 技術別

- 太陽光発電(PV)

- 集光型太陽熱発電(CSP)

- エンドユーザー別

- ユーティリティスケール

- 商業・産業(C&I)

- 住宅

- コンポーネント別(定性分析)

- 太陽電池モジュール/パネル

- インバータ(ストリング型、集中型、マイクロ型)

- 設置・追尾システム

- システム周辺機器および電気機器

- エネルギー貯蔵およびハイブリッド統合

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- 北欧諸国

- ロシア

- その他の欧州諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- オーストラリア

- その他のアジア太平洋諸国

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米諸国

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- エジプト

- その他の中東・アフリカ諸国

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向(M&A、提携、PPA)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- ABB Ltd.

- Schneider Electric SE

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd.

- SunPower Corporation

- Trina Solar Ltd.

- LONGi Green Energy Technology Co. Ltd.

- JA Solar Technology Co. Ltd.

- Sharp Corporation

- Tesla Inc.

- First Solar Inc.

- Sunrun Inc.

- D.Light Design Inc.

- Bboxx Ltd.

- ENGIE Energy Access

- Zola Electric

- SMA Solar Technology AG

- Enphase Energy Inc.

- Fronius International GmbH

- Powerhive Inc.

- Greenlight Planet Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日