|

市場調査レポート

商品コード

1690862

世界の使い捨て血液バッグ市場:シェア分析、産業動向・統計、成長予測(2025年~2030年)Global Disposable Blood Bags - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の使い捨て血液バッグ市場:シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

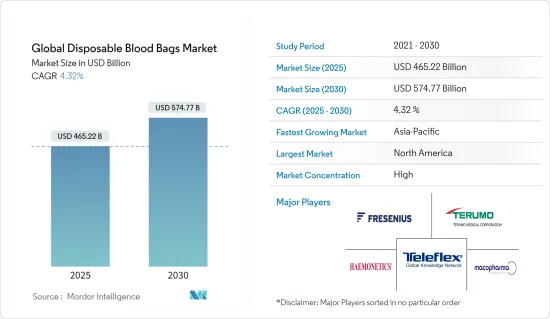

使い捨て血液バッグの世界市場規模は、2025年に4,652億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.32%で、2030年には5,747億7,000万米ドルに達すると予測されます。

外傷や傷害の増加、血液関連疾患やその他の慢性疾患の負担増、輸血に対する政府のイニシアチブの増加が、予測期間中の市場成長を後押しすると予想されます。

事故、外傷、輸血を必要とするその他の医療緊急事態の負担増は、使い捨て血液バッグ市場の主要促進要因です。交通事故は、幼児や若年成人(5~29歳)の負傷の大きな原因であり、彼らの健康と幸福に大きな脅威を与えています。例えば、2023年12月に世界保健機関(WHO)が発表したデータによると、2,000万人から5,000万人が非致死的な怪我に苦しんでおり、その多くが障害を負っています。致命的な負傷の治療や出血量の回復を目的とした外科手術の際には、こうした重傷者に輸血活動が伴うことが多いです。したがって、輸血を必要とする交通事故による負傷は、使い捨て血液バッグの調達率を高め、予測期間中の市場成長を促進すると予想されます。

血友病、鎌状赤血球症、血液がん、白血病などの血液関連疾患やその他の慢性疾患の有病率は増加しており、入院につながる可能性があるため、輸血の需要がさらに必要となります。例えば、世界血友病連盟が発表したデータによると、2023年3月には世界で40万人以上が血友病を患っており、治療のために定期的な輸血を必要としています。従って、血友病患者におけるこの定期的な輸血処置は、使い捨て血液バッグの需要を促進し、市場成長に寄与しています。

さらに、希少な血液疾患の発生率や慢性貧血の患者数は、血液由来材料の需要を増加させ、輸血バッグの需要に拍車をかけると予測されています。例えば、世界保健機関(WHO)によると、2023年5月には、全世界で6~15歳の幼児のほぼ40%、15~49歳の妊婦の約10人に3人が貧血に罹患しており、そのため重大なケースでの輸血の必要性が高まっています。したがって、市場の成長にプラスの影響を与えると予想されます。

さらに、新たな技術の進歩や新製品発売の増加も、市場における使い捨て血液バッグの利用可能性を促進し、それゆえ予測期間中の市場成長を促進すると予想されます。例えば、2023年8月、Fresenius KabiはDEHPフリーの血液バッグシステムの開発進捗を発表しました。同社は、PVC/BTHC材料から作られた赤血球バッグを備えた新しい血液バッグシステムを明らかにしました。こうした市場の開拓は、市場の成長を後押しすると予想されます。

したがって、外傷や傷害の数の増加、血液関連の負担の増加などの上記の要因のために、市場は分析期間中に成長を示すと予想されます。しかし、献血や輸血に伴う高いリスクは、予測期間中の市場成長を阻害すると考えられます。

使い捨て輸血バッグ市場の動向

輸血バッグは予測期間中に大幅な成長が見込まれる

輸血バッグは、赤血球や血漿のような血液やその成分を保持します。これらのバッグは細いチューブに接続されて静脈に挿入され、血液製剤が人体に直接流入します。

輸血バッグセグメントは、予測期間中に大きな市場シェアを占めると予想されています。心臓外科手術、血管外科手術など、外科手術中に失われた血液を回復させるために輸血を必要とする外科手術の件数が増加していることなどが、同セグメントの成長を後押しすると予想されています。さらに、血友病、貧血、サラセミアなどの血液関連疾患や慢性疾患の有病率の増加は、定期的な輸血を必要とし、市場における使い捨て輸血バッグの需要をさらに促進しています。

高齢化人口の増加、複雑な手術、外傷治療の向上などに起因する輸血ニーズの増加は、医療施設全体で輸血バッグに対する直接的な需要を生み出しています。例えば、Starpearlsが2023年6月に発表した記事によると、毎年約500万人のアメリカ人が急性出血、手術、血友病、がんのために輸血を必要としています。輸血の件数が増えれば、必然的に輸血バッグの需要も増えます。このように、輸血の症例数の増加に伴い、研究セグメントは予測期間中に成長すると予想されます。

さらに、メーカーは効果的な流通チャネルや買収戦略を採用することで、より多くの顧客を獲得し、市場シェアを拡大することを目指しています。例えば、2022年1月、SpotSeeは医療機器メーカーであるBiosynergy, Inc.の資産買収に調印しました。この買収は、血液バッグに血液温度モニタリングデバイスを組み込むことで製品の損傷を減らすという同社の目標を強化することを目的としており、これにより製品供給とコールドチェーンをさらに改善することができます。このような開発は、予測期間中のセグメント成長を押し上げると予想されます。

このように、輸血症例の増加や買収などの戦略に注力するメーカーなど、上記の要因がセグメントの成長を高め、予測期間中の市場成長を押し上げると予想されます。

北米が市場で大きなシェアを占め、予測期間中も同様

北米地域の市場成長を促進する要因としては、高齢者に伴う血液関連疾患の有病率の増加、交通事故や傷害の負担増、新製品の発売などが挙げられます。

高齢者は、外科手術を必要とする慢セクシャルヘルス状態により輸血を必要とする可能性が高く、そのため米国では安全で容易に入手可能な血液供給に対する需要が高まっています。また、血液の需要は地域全体で増加しており、ある場所からによる場所へ血液を収集し輸送するための様々な使い捨て血液バッグの必要性を推進しています。例えば、米国赤十字2024年更新版が発表したデータによると、米国では毎日約2万9,000個の赤血球、約5,000個の血小板、6,500個の血漿が必要とされています。米国では毎年約1,600万個の血液成分が輸血されています。

さらに、交通事故による負担が、外科手術の際の血液供給の需要だけでなく、失われた血液を回復させる需要にも拍車をかけています。例えば、Fatal Car Crash Statistics 2024が発表したデータによると、米国では2022年に約4万2,795件の死亡自動車事故が報告されています。

人口の間で貧血、白血病、サラセミア、血友病の有病率が上昇しているため、赤血球を補充し、全身への酸素供給を改善するために、患者への頻繁な輸血が必要です。例えば、米国がん協会によると、2024年1月には、米国で新たに約6万2,770例の白血病と8,570例のホジキンリンパ腫が診断されると予想されています。さらに、Leukemia and Lymphomaが発表した2023年の最新データによると、2023年には米国で新たに約184,720例の白血病、リンパ腫、骨髄腫が記録されました。

さらに、Canadian Cancer Staticsが2023年に発表したデータによると、2022年には約23万9,100人のカナダ人ががんと診断されました。したがって、貧血、白血病、サラセミアの有病率の上昇は、輸血と血液成分療法の必要性の増加による使い捨て血液バッグの需要を促進する重要な要因であり、市場の成長に寄与しています。

したがって、患者の血液検査数の増加、輸血の増加、交通事故事例の増加、同地域における白血病、リンパ腫、骨髄腫事例の増加など、上記の要因のおかげで、市場の成長は予測期間中に北米地域で増加すると予想されます。

使い捨て血液バッグ産業概要

使い捨て血液バッグ市場は、世界的に事業を展開する多くの企業が存在するため、その性質上細分化されています。競合情勢には、市場シェアを保有し知名度の高い数社の国際企業と地元企業の分析が含まれます。主要企業は、市場での地位を維持するために、新製品の発売や提携などの重要な戦略的活動を採用しています。主要市場参入企業には、MacoPharma、AdvaCare Pharma、Fresenius SE & Co.KGaA、Teleflex Incorporated、Haemonetics Corporation、Terumo Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 樽腫と傷害の増加

- 血液関連疾患とその他の慢性疾患の負担増

- 献血に対する政府の取り組みの増加

- 市場抑制要因

- 献血と輸血に伴う高いリスク

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- バッグタイプ別

- 採血バッグ

- 一重採血バッグ

- 二重血液バッグ

- 三重血液バッグ

- 四重バッグ

- 輸血バッグ

- 採血バッグ

- エンドユーザー別

- 血液バンク

- 病院

- 非政府組織、その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AdvaCare Pharma

- Fresenius SE & Co. KGaA

- Genesis BPS

- Grifols SA

- Haemonetics Corporation

- HLL Lifecare Limited

- INNVOL

- JMS Co. Ltd

- SB-KAWASUMI LABORATORIES, INC.

- MacoPharma

- Neomedic International

- Poly Medicure Limited

- Teleflex Incorporated

- Terumo Corporation

第7章 市場機会と今後の動向

The Global Disposable Blood Bags Market size is estimated at USD 465.22 billion in 2025, and is expected to reach USD 574.77 billion by 2030, at a CAGR of 4.32% during the forecast period (2025-2030).

The increasing number of trauma and injuries, the rising burden of blood-related and other chronic disorders, and increasing government initiatives for blood transfusions are expected to boost market growth over the forecast period.

The increasing burden of accidents, trauma, and other medical emergencies requiring blood transfusions is the primary driver of the disposable blood bag market. Road accidents are a significant cause of injuries among children and young adults (5-29 years old), posing a significant threat to their health and well-being. For instance, according to data published by the World Health Organization in December 2023, between 20 and 50 million people suffer from non-fatal injuries, with many incurring a disability. Blood transfusion activities often accompany these severe injuries during surgical procedures to treat fatal injuries as well as to recover blood loss. Hence, road accident injuries that necessitate blood transfusion increase the procurement rate of disposable blood bags, which is expected to propel the market growth during the forecast period.

The prevalence of blood-related and other chronic diseases, such as hemophilia, sickle cell disease, blood cancer, and leukemia, is increasing, which can lead to hospitalization, which further necessitates the demand for blood transfusion. For instance, as per the data published by the World Federation of Hemophilia, in March 2023, over 400,000 individuals lived with hemophilia globally, requiring regular blood transfusions for treatment. Thus, this routine blood transfusion procedure among hemophilia patients propels the demand for disposable blood bags, contributing to market growth.

Additionally, the incidence of rare blood disorders and the number of people with chronic anemia are predicted to increase the demand for blood-derived materials, fueling the demand for blood transfer bags. For instance, according to the World Health Organization, in May 2023, almost 40% of children aged 6-15 and about 3 in 10 pregnant women aged between 15 and 49 years old suffer from anemia worldwide, thus raising the need for blood transfusion in critical cases. Hence, it is expected to have a positive impact on the market growth.

Furthermore, emerging technological advancements and increasing new product launches are also expected to fuel the availability of disposable blood bags in the market, hence anticipated to drive the market growth over the forecast period. For instance, in August 2023, Fresenius Kabi stated its progress in developing a DEHP-free blood bag system. The company revealed a new blood bag system with a red cell bag made from PVC/BTHC material. These developments are anticipated to boost the market growth.

Therefore, owing to the factors above, such as the rising number of trauma and injuries and the growing burden of blood-related, the market is anticipated to witness growth over the analysis period. However, the high risk associated with blood donation and transfusion will impede market growth over the forecast period.

Disposable Blood Bags Market Trends

Blood Transfusion Bags is Expected to Witness Significant Growth Over the Forecast Period

Blood transfusion bags hold blood or its components, like red blood cells or plasma. These bags are connected to a thin tube and inserted into a vein, allowing the blood products to flow directly into the human body.

The blood transfusion bags segment is anticipated to hold a significant market share over the forecast period. Factors such as the growing number of surgical procedures such as cardiac surgery, vascular surgery, and others that require a blood transfusion to recover the blood loss during surgical procedures are expected to boost segment growth. In addition, the increasing prevalence of blood-related and chronic conditions such as hemophilia, anemia, and thalassemia require regular blood transfusions, further propelling the demand for disposable blood transfusion bags in the market.

The increasing need for blood transfusions, owing to the growing aging population, complex surgeries, and improved trauma care, creates a direct demand for blood transfusion bags across healthcare facilities. For instance, according to the article published by Starpearls in June 2023, around 5 million Americans require a blood transfusion each year for acute blood loss, surgery, hemophilia, or cancer. As the number of blood transfusions rises, the demand for blood transfusion bags inevitably increases. Thus, with the rising cases of blood transfusion, the studied segment is anticipated to grow over the forecast period.

Moreover, manufacturers aim to reach more customers and expand their market share by adopting effective distribution channels and acquisition strategies. For instance, in January 2022, SpotSee signed the acquisition of the assets of Biosynergy, Inc., a medical device manufacturer. This acquisition aims to strengthen the company's goal of reducing product damage by incorporating blood temperature monitoring devices in blood bags, which can further improve product supply and cold chain. Such developments are anticipated to boost segment growth during the forecast period.

Thus, the factors above, such as the rising cases of blood transfusion and manufacturers focusing on strategies such as acquisition, are expected to increase the segment growth, thereby boosting the market growth over the forecast period.

North America Holds a Significant Share in the Market and Do the Same during the Forecast Period

Some of the factors driving the market growth in the North American region include the increasing prevalence of blood-related disorders coupled with the elderly population, the rising burden of road accidents and injuries, and new product launches.

Elderly individuals are more likely to require a blood transfusion due to chronic health conditions that require surgical procedures, hence raising the demand for safe and readily available blood supplies in the United States. Also, the demand for blood is increasing across the region, propelling the need for various disposable blood bags to collect and transport blood from one place to another. For instance, according to the data published by the American National Red Cross 2024 update, approximately 29,000 red blood cells, nearly 5,000 platelets, and 6,500 plasma units are needed daily in the United States. About 16 million blood components are transfused each year in the United States.

Furthermore, the burden of road accidents has propelled the demand for blood supply during surgical procedures as well as to recover the blood loss. For instance, according to the data published by Fatal Car Crash Statistics 2024, about 42,795 fatal car crashes were reported in the United States in 2022.

The rising prevalence of anemia, leukemia, thalassemia, and hemophilia among the population necessitates frequent blood transfusions to patients to replenish red blood cells and improve oxygen delivery throughout the body. For instance, according to the American Cancer Society, in January 2024, about 62,770 new cases of leukemia and 8,570 new cases of Hodgkin lymphoma were expected to be diagnosed in the United States. Additionally, according to the 2023 updated data published by Leukemia and Lymphoma, about 184,720 new leukemia, lymphoma, and myeloma cases were recorded in the United States in 2023.

Furthermore, according to the data published by Canadian Cancer Statics in 2023, about 239,100 Canadians were diagnosed with cancer in 2022. Hence, the rising prevalence of anemia, leukemia, and thalassemia is a significant factor driving the demand for disposable blood bags due to the increased need for blood transfusions and blood component therapy, contributing to the market growth.

Therefore, owing to the factors mentioned above, such as the growing blood test counts among patients, rising blood transfusion, growing cases of road accidents, and increasing cases of leukemia, lymphoma, and myeloma in the region, the growth of the market is anticipated to increase in the North American region over the forecast period.

Disposable Blood Bags Industry Overview

The disposable blood bags market is fragmented in nature due to the presence of many companies operating globally. The competitive landscape includes an analysis of a few international as well as local companies that hold market shares and are well known. The key players are adopting key strategic activities such as new product launches and collaborations to maintain their market position. Some of the key market players are MacoPharma, AdvaCare Pharma, Fresenius SE & Co. KGaA, Teleflex Incorporated, Haemonetics Corporation, and Terumo Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing number of Taruma and Injuries

- 4.2.2 Rising Burden of Blood Related and Other Chronic Disorders

- 4.2.3 Increasing Government Initiatives for Blood Donations

- 4.3 Market Restraints

- 4.3.1 High Risk Associated with Blood Donation and Transfusion

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type of Bag

- 5.1.1 Blood Collection Bags

- 5.1.1.1 Single Blood Bags

- 5.1.1.2 Double BloodBags

- 5.1.1.3 Triple Blood Bags

- 5.1.1.4 Quadruple Blood Bags

- 5.1.2 Blood Transfusion Bags

- 5.1.1 Blood Collection Bags

- 5.2 By End User

- 5.2.1 Blood Banks

- 5.2.2 Hospitals

- 5.2.3 Non-Government Organization and Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AdvaCare Pharma

- 6.1.2 Fresenius SE & Co. KGaA

- 6.1.3 Genesis BPS

- 6.1.4 Grifols SA

- 6.1.5 Haemonetics Corporation

- 6.1.6 HLL Lifecare Limited

- 6.1.7 INNVOL

- 6.1.8 JMS Co. Ltd

- 6.1.9 SB-KAWASUMI LABORATORIES, INC.

- 6.1.10 MacoPharma

- 6.1.11 Neomedic International

- 6.1.12 Poly Medicure Limited

- 6.1.13 Teleflex Incorporated

- 6.1.14 Terumo Corporation