|

市場調査レポート

商品コード

1644450

ワクチンロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Vaccine Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ワクチンロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

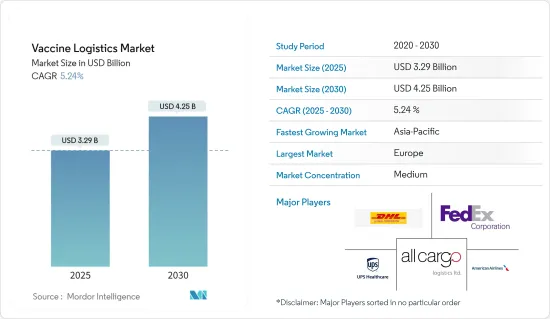

ワクチンロジスティクスの市場規模は2025年に32億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.24%で、2030年には42億5,000万米ドルに達すると予測されます。

新しいワクチン、進化する予防接種スケジュール、革新的なサービス提供戦略、対象人口の拡大、コールドチェーンインフラ需要の高まり、限られた資金が、ワクチン輸送市場のダイナミクスを再構築しています。

気候変動は感染症の様相を大きく変えています。気温の上昇は、蚊やマダニといった疾病媒介動物の生息域を広げ、マラリア、デング熱、ライム病といった疾病の蔓延を促進しています。このようなパターンは、異常気象や生態系の乱れとともに、人獣共通感染症、水系感染症、呼吸器感染症のリスクを高めており、ワクチンの需要が高まっていることを裏付けています。

例えば、ファイザー・バイオンテック・ワクチンは、-112°Fから-76°F(-80℃から-60℃)の超低温を必要とし、温度管理された専用のサーマルシッパーでの保管を義務付けています。同様に、Modernaワクチンはファイザーワクチンほど極端な温度は要求されないもの、-4°F(-20℃)での保管が必要です。このワクチンは、高温に長時間さらされることを避け、製造施設から使用場所まで直接輸送されなければならないです。

温度に敏感なワクチンの輸送は、医薬品の中でも特に難しい課題です。このような重要な製品は、サプライチェーン全体を通して細心の注意が必要であり、正確に調整された温度管理されたロジスティクスに依存しています。一貫した温度を維持することは非常に重要であり、ワクチンは製造から投与まで指定された範囲内に保たれなければなりません。この範囲から逸脱すると、ワクチンの効能や対象疾患に対する予防効果が危険にさらされます。

さらに、ワクチン輸送市場は、進化するワクチン要件、気候変動の影響、厳格な温度管理の必要性により、多くの課題に直面しています。これらの課題に対処することは、世界中でワクチンの有効性と安全性を確保する上で極めて重要です。

ワクチンロジスティクス市場の動向

北米ワクチンロジスティクス市場の成長と変革

北米のワクチンロジスティクス市場は、主に温度管理された輸送・保管ソリューションに対する需要の急増に後押しされ、成長を目の当たりにしています。ロジスティクス・プロバイダーは、輸送中のワクチンの有効性を確実に維持するため、コールドチェーン機能を強化しています。例えば、フェデックスは米国全土に温度管理施設のネットワークを広げ、厳しい温度規制を遵守するワクチンの効率的な取り扱いを促進しています。この戦略的な取り組みは物流面での課題に対処するだけでなく、フィラデルフィアやダラスといった都市に主要施設を設けることでコルドチェーン能力を大幅に強化していまします。

さらに、新ワクチンの導入や予防接種スケジュールの変更により、北米の物流事情は大きく変化しています。2024年、XPOは熱の影響を受けやすいワクチンの全国配送を監督するため、サーモマッピング輸送車両を導入しました。同社はシカゴやヒューストンといった大都市での配送を成功させ、ワクチンが出荷元から医療従事者まで定められた温度範囲内に収まることを保証しています。

結論として、北米のワクチンロジスティクス市場は、コールドチェーン技術の進歩や新ワクチンのイントロダクション牽引され、急速に進化しています。企業はまた、地域全体で効率的で信頼性の高いワクチン流通を確保しています。

ワクチンロジスティクスサービスにおけるコールドチェーン技術革新

まず、コールドチェーンソリューションに対する需要が増加しています。2024年からの過去10年間で、コールドチェーンロジスティクス分野への投資が急増しています。バイオファーマ・コールドチェーンソースブックが報告しているように、2020年には、温度管理されたロジスティクスがバイオファーマのロジスティクス支出の約18%を占めるようになった。この増加傾向に歯止めがかかる兆しはないです。

例えば、ジフテリア、破傷風、百日咳(DTP)、麻疹、おたふくかぜ、風疹(MMR)などのワクチンの多くは熱安定性に欠けます。これらの熱に弱いワクチンは、2℃~8℃に保たなければ、生物学的成分のためにすぐに分解してしまいます。そのため、多段階の冷蔵またはコールドチェーン流通システムに大きく依存しています。

さらに、人工知能(AI)やブロックチェーンのような先進技術の登場により、医薬品セクターはサプライチェーンの可視性向上という重要な動向を目の当たりにしています。温度に敏感な製品の追跡、監視、管理は、これまで以上に多くのデータを生成するようになりました。この可視性を強化するテクノロジーは、腐敗リスクを軽減するだけでなく、規制基準の遵守を確実にします。

さらに、各企業は密閉温度制御システムを備えたハイテク・コンテナを革新しています。これらのコンテナは、温度変化に敏感な貨物を貨物倉庫と航空機の間でシームレスに輸送することを容易にし、特に医薬品分野に対応しています。

例えば、英国のタイン港では、5G対応の自律型ドローンが配備されています。これらのドローンは業務効率を高め、貨物の取り扱いを監督し、プロセスを迅速化することでコールドチェーンを強化し、温度に敏感な物資の遅延を軽減します。

結論として、コールドチェーンソリューションに対する需要の高まりと技術の進歩が相まって、ワクチンロジスティクスの状況は大きく変わりつつあります。サプライチェーンの可視性の向上と革新的な温度管理システムは、ワクチンの安全かつ効率的な流通を確保する上で不可欠です。

ワクチンロジスティクス業界の概要

ワクチンロジスティクス市場は断片化されており、DHL Global Forwarding、AllCargo Logistics、アメリカン航空、フェデックス・コーポレーション、UPSヘルスケアなどの国際企業によって支配されています。これらの大手企業は、主に買収を通じて拡大戦略を追求しています。彼らの確立されたプレゼンスは、中小企業に比べて市場拡大をスムーズにします。

冷蔵倉庫、迅速配送サービス、バルクワクチン輸送の需要は増加傾向にあります。この急増は、政府投資の活発化によってさらに後押しされ、市場プレーヤーにリーチを広げ、時間をかけて効率を高めるチャンスを提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 温度制御包装の技術革新

- ヘルスケアインフラ強化のための国境を越えた協力とイニシアチブ

- 抑制要因

- サプライチェーンの混乱と輸送のボトルネックは、タイムリーなワクチン流通を妨げる可能性があります。

- 規制と適合性の課題

- 機会

- ブロックチェーンとIoT技術の採用により、透明性と追跡可能性が向上します。

- 次世代ワクチン

- 促進要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術動向と自動化

- 政府の規制と取り組み

- 業界のバリューチェーン/サプライチェーン分析

- 環境・温度管理貯蔵への注目

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- サービス別

- 輸送

- 陸上(道路と鉄道)

- 航空

- 海上輸送

- 倉庫

- 付加価値サービス(包装、ラベリングなど)

- 輸送

- エンドユーザー別

- 病院

- 医薬品メーカーおよび流通業者

- その他のエンドユーザー(血液銀行、クリニックなど)

- 地域別

- アジア太平洋

- 中国

- 日本

- オーストラリア

- インド

- シンガポール

- マレーシア

- インドネシア

- タイ

- 韓国

- その他アジア太平洋地域

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- その他欧州

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- コロンビア

- アルゼンチン

- その他南米

- 中東

- エジプト

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アジア太平洋

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- DHL Global Forwarding

- AllCargo Logistics

- American Airlines

- DB Schenker

- FedEx Corporation

- Kuehne Nagel

- Nippon Express

- Yamato Logistics

- Americold Logistics

- lynden international logistics

- DP World

- Coldman Logistics

- Cavalier Logistics*

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済への貢献

- 対外貿易統計-品目別、仕向地・原産地別輸出入額

The Vaccine Logistics Market size is estimated at USD 3.29 billion in 2025, and is expected to reach USD 4.25 billion by 2030, at a CAGR of 5.24% during the forecast period (2025-2030).

New vaccines, evolving immunization schedules, innovative service delivery strategies, a broader target population, heightened cold-chain infrastructure demands, and limited funding are reshaping the dynamics of the vaccine transportation market.

Climate change has significantly altered the landscape of infectious diseases. Rising temperatures are broadening the habitats of disease vectors like mosquitoes and ticks, facilitating the spread of diseases such as malaria, dengue fever, and Lyme disease. This pattern, alongside extreme weather events and ecosystem disruptions, heightens the risk of zoonotic diseases, waterborne illnesses, and respiratory infections, underscoring the growing demand for vaccines.

For example, the Pfizer-BioNTech Vaccine mandates storage in specialized temperature-controlled thermal shippers, requiring ultra-low temperatures between -112°F and -76°F (-80°C to -60°C). Similarly, while the Moderna Vaccine doesn't demand the extreme temperatures of its Pfizer counterpart, it still requires storage at -4°F (-20°C). This vaccine must be transported directly from the manufacturing facility to its point of use, avoiding any prolonged exposure to elevated temperatures.

Transporting temperature-sensitive vaccines stands out as a particularly challenging endeavor among pharmaceuticals. These vital products necessitate meticulous handling throughout the supply chain, relying on precisely coordinated temperature-controlled logistics. Maintaining a consistent temperature is crucial, vaccines must remain within a specified range from production to administration. Deviating from this range jeopardizes the vaccine's potency and its protective efficacy against targeted diseases.

Moreover, the vaccine transportation market faces numerous challenges due to evolving vaccine requirements, climate change impacts, and stringent temperature control needs. Addressing these challenges is crucial to ensuring the efficacy and safety of vaccines worldwide.

Vaccine Logistics Market Trends

Growth and Transformation in the North American Vaccine Logistics Market

The North American vaccine logistics market is witnessing growth, primarily fueled by the surging demand for temperature-controlled transportation and storage solutions. Logistic providers are bolstering their cold chain capabilities to ensure vaccines retain their efficacy during transit. For example, FedEx has broadened its network of temperature-controlled facilities throughout the U.S., facilitating the efficient handling of vaccines that adhere to stringent temperature regulations. This strategic move not only addresses logistical challenges but also significantly enhances its cold chain capabilities, with key facilities in cities like Philadelphia and Dallas.

Furthermore, the rollout of new vaccines and the shifting immunization schedule are transforming North America's logistics landscape. In 2024, XPO has rolled out its thermally mapped transportation fleet to oversee the distribution of heat-sensitive vaccines nationwide. The company has successfully orchestrated deliveries in major cities like Chicago and Houston, guaranteeing that vaccines stay within the mandated temperature ranges from their origin to healthcare providers.

In conclusion, the North American vaccine logistics market is evolving rapidly, driven by advancements in cold chain technology and the introduction of new vaccines. Companies are also ensuring efficient and reliable vaccine distribution across the region.

Cold Chain Innovations in Vaccine Logistics Services

First, the demand for cold chain solutions is on the rise. Over the past decade from 2024, investments in the cold chain logistics sector have surged. As reported by the Biopharma Cold Chain Sourcebook, in 2020, temperature-controlled logistics made up nearly 18% of biopharma logistics expenditures. This upward trend shows no signs of slowing down.

For instance, many vaccines, such as those for diphtheria, tetanus, pertussis (DTP), and measles, mumps, and rubella (MMR), lack thermal stability. These heat-sensitive vaccines, if not kept between 2°C and 8°C, degrade quickly due to their biological components. Consequently, they depend heavily on a multi-stage refrigerated or cold-chain distribution system.

Moreover, with the advent of advanced technologies like artificial intelligence (AI) and blockchain, the pharmaceutical sector is witnessing a crucial trend: enhanced supply chain visibility. The tracking, monitoring, and management of temperature-sensitive products now generate more data than ever. Technologies that bolster this visibility not only mitigate spoilage risks but also ensure adherence to regulatory standards.

In addition, companies are innovating high-tech containers equipped with closed temperature-controlled systems. These containers facilitate the seamless transport of temperature-sensitive goods between cargo warehouses and aircraft, specifically catering to the pharmaceutical sector.

For instance, at the Port of Tyne in the UK, 5G-enabled autonomous drones have been deployed. These drones boost operational efficiency and oversee cargo handling, bolstering the cold chain by expediting processes and reducing delays for temperature-sensitive supplies.

In conclusion, the increasing demand for cold chain solutions, coupled with technological advancements, is transforming the vaccine logistics landscape. Enhanced supply chain visibility and innovative temperature-controlled systems are critical in ensuring the safe and efficient distribution of vaccines.

Vaccine Logistics Industry Overview

The vaccine logistics market is fragmented and is dominated by international companies, such as DHL Global Forwarding, AllCargo Logistics, American Airlines, FedEx Corporation and UPS Healthcare . These giants are pursuing expansion strategies, primarily through acquisitions. Their established presence allows for smoother market expansion compared to smaller players.

The demand for refrigerated warehouses, expedited delivery services, and bulk vaccine transportation is on the rise. This surge is further bolstered by heightened government investments, offering market players a chance to broaden their reach and enhance efficiency over time.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Technology innovation in temperature controlled packaging

- 4.2.1.2 Cross Border collaborations and initiative to enhance healthcare infrastructure

- 4.2.2 Restraints

- 4.2.2.1 Supply chain distruption and transportation bottlenecks can hinder timely vaccine distribution

- 4.2.2.2 Regulatory and Compiliance Challenges

- 4.2.3 Opportunities

- 4.2.3.1 Adoption of blockchain and IoT technology can improve transparency and tracebility

- 4.2.3.2 Next-Generation Vaccines

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers/Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technological Trends and Automation

- 4.5 Government Regulations and Initiatives

- 4.6 Industry Value Chain/Supply Chain Analysis

- 4.7 Spotlight on Ambient/Temperature-controlled Storage

- 4.8 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Land (Road and Rail)

- 5.1.1.2 Air

- 5.1.1.3 Sea

- 5.1.2 Warehousing

- 5.1.3 Value-added Services (Packaging, Labeling, etc.)

- 5.1.1 Transportation

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Drug Manufacturers and Distributors

- 5.2.3 Other End Users (Blood Banks, Clinics, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 Australia

- 5.3.1.4 India

- 5.3.1.5 Singapore

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Thailand

- 5.3.1.9 South Korea

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 North America

- 5.3.3.1 United States

- 5.3.3.2 Canada

- 5.3.3.3 Mexico

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Colombia

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Egypt

- 5.3.5.2 Qatar

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Rest of the Middle East

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 DHL Global Forwarding

- 6.2.2 AllCargo Logistics

- 6.2.3 American Airlines

- 6.2.4 DB Schenker

- 6.2.5 FedEx Corporation

- 6.2.6 Kuehne Nagel

- 6.2.7 Nippon Express

- 6.2.8 Yamato Logistics

- 6.2.9 Americold Logistics

- 6.2.10 lynden international logistics

- 6.2.11 DP World

- 6.2.12 Coldman Logistics

- 6.2.13 Cavalier Logistics*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 External Trade Statistics - Exports and Imports by Product and by Country of Destination/Origin